Breaking: All Health Republic plans (Group and Individual) ending on 11/30. according to early reports the healthcare Co-Op Health Republic NY will be shutting down Nov 30, 2015. New York State Department of Financial Services (NYDFS), the New York State of Health Marketplace (NYSOH), and the Centers for Medicare and Medicaid Services (CMS) announced additional actions regarding Health Republic Insurance of New York (“Health Republic”) and a transition plan for Health Republic customers.

TIMELINE:

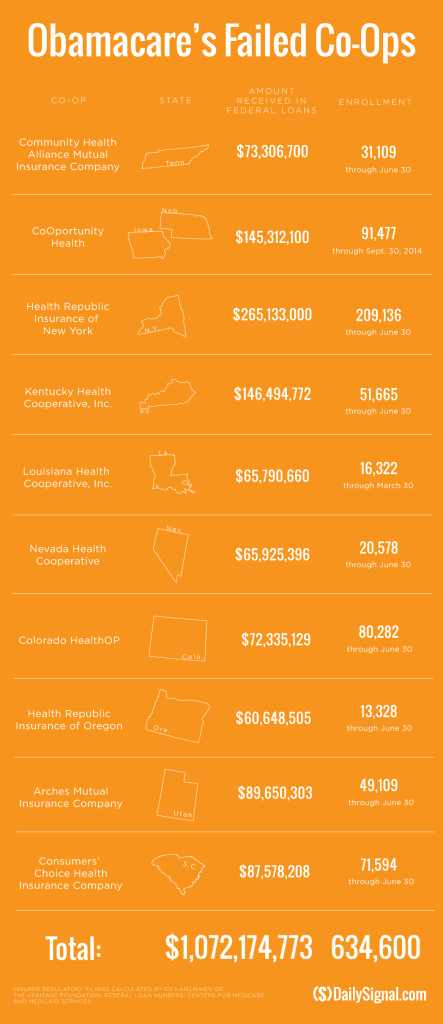

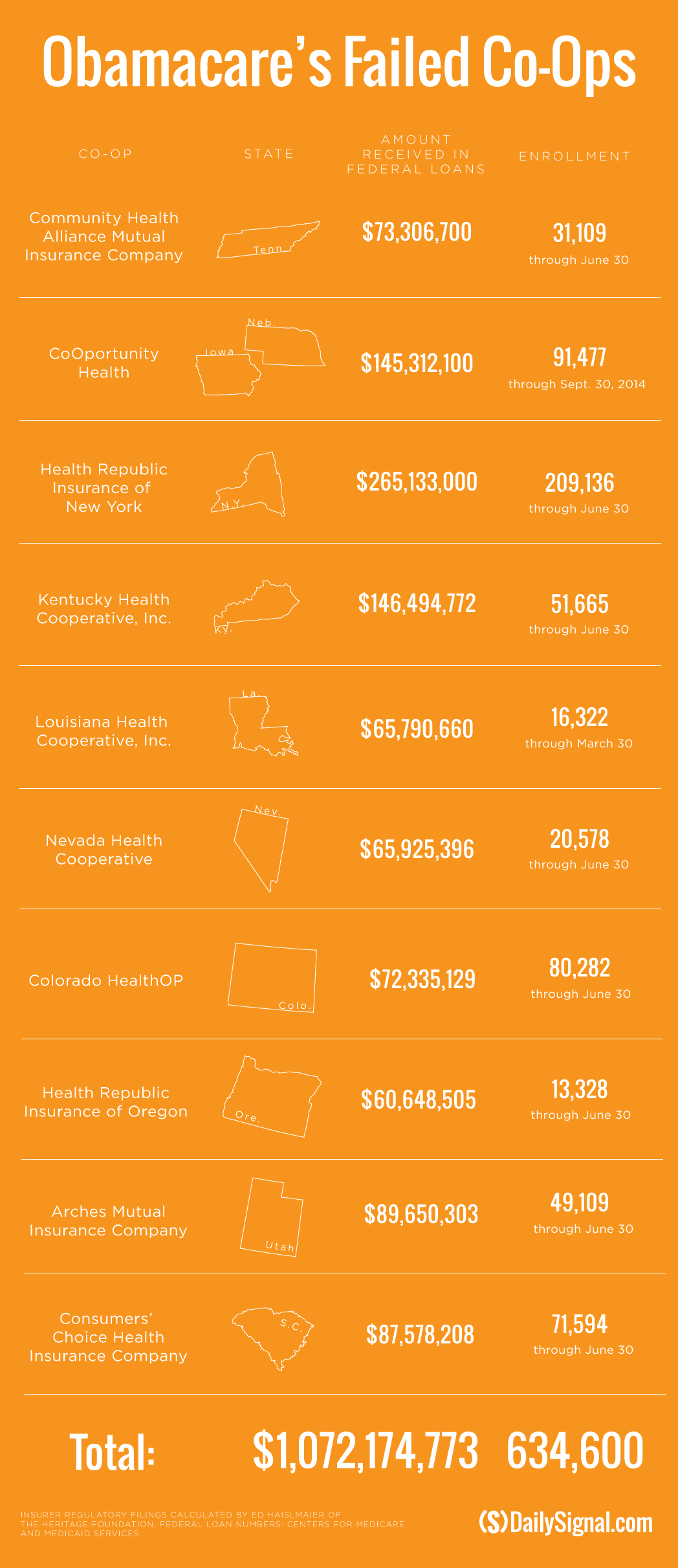

Oct 28th – Utah Healthcare Co-Op shutting down end of 2015. This sis the 5th Co-Op to shut down

June 2015 – With a spike in rate increase of 15-20% for 2016 to reflect unexpected high costs of new 200,000 membership the most affordable health plan was experiencing difficulties. The insurer reported $130 million in losses during its first 18 months of operations, according to financial filings, even as it enrolled more customers than any other insurer. DFS did allow for a 13 percent increase in the second year and a 14 percent increase heading into 2016. Both were lower than what Health Republic requested, though, and were not enough to save the struggling insurer.

May 2015- Health Republic was dealt its death blow when it became clear that the Affordable Care Act’s risk corridor program would not be fully funded, said one source familiar with the company’s finances. A report from Standard & Poor’s in May said the program had only 10 percent of the funds needed to make payments.

Summer 2013 -Health Republic had borrowed $265 million to begin operations.

New Insurance Risk Corridors paid for by a combination of both consumer insurance premium surcharge tax of 2-3% and Health Insurers is suppose to reclaim capital to those that are less profitable. Health Republic was owed approximately $147 million but was told by the Centers for Medicare and Medicaid Services to expect less than half that according to sources.

Regrettably, we all suffer when an Insurer exits the market. Furthermore, it will be a while again when Federal funds earmarked to start a low cost affordable health plans will materialize again. We are pulling for neighboring co-op Health Republic of NJ and hope this trend discontinues.

Our agency will be working closely with our clients to mitigate this exposure and transition smoothly for Dec 1, 2015. Individuals on the Marketplace can contact the New York State Department of Financial Services Consumer Hot Line with questions regarding Health Republic by calling 1-800-342-3736. The Hot Line hours are weekdays (Monday through Friday) from 8:00 a.m. to 8:00 p.m., and Saturday from 9:00 a.m. to 1:00 p.m.

Please Click here to read the full Press Release from NYDFS.

Stay posted, more news to follow. Our Agency as in the past will be out and early in front positioning our clients for best options. For more information on this or to schedule a call please contact us info@medicalsolutionscorp.com today.

November 1, 2015: Open Enrollment starts — first day you can enroll in a 2016 insurance plan through the Health Insurance Marketplace. Coverage can start as soon as January 1, 2016.

2016 plans and prices will be available for preview the third week of October, 2015.

December 15, 2015: Last day to enroll in or change plans for new coverage to start January 1, 2016.

January 1, 2016: 2016 coverage starts for those who enroll or change plans by December 15.

January 15, 2016: Last day to enroll in or change plans for new coverage to start February 1, 2016

January 31, 2016: 2016 Open Enrollment ends. Enrollments or changes between January 16 and January 31 take effect March 1, 2016.

If you don’t enroll in a 2016 health insurance plan by January 31, 2016, you can’t enroll in a health insurance plan for 2016 unless you qualify for a Marketplace Special Enrollment Period.

Penalty: The uninsured penalty rises to $695 or 2.5% of your income, whichever is higher.

Coverage start dates

If you enroll before the 15th of any month, your coverage starts the first day of the next month. If you enroll after the 15th of the month, you’ll have to wait until the month after that for your coverage to start. So, for example, if you enroll on January 16, your coverage would start on March 1.

Enroll using our online comparison shopping tool for both on and off-Exchange Marketplace to be released next week. Email us or Contact us at (855)667-4621.

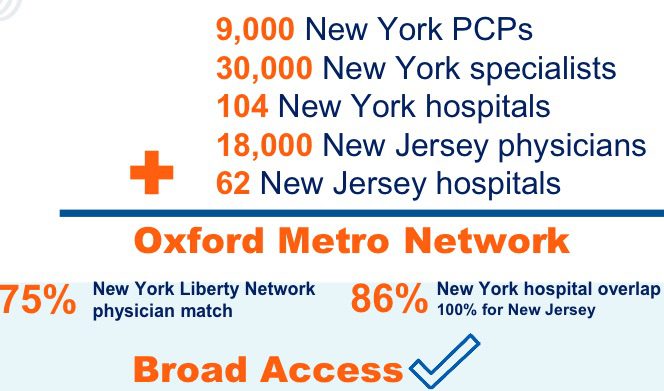

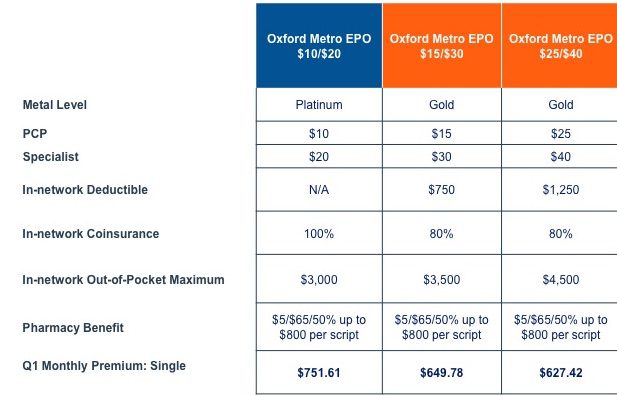

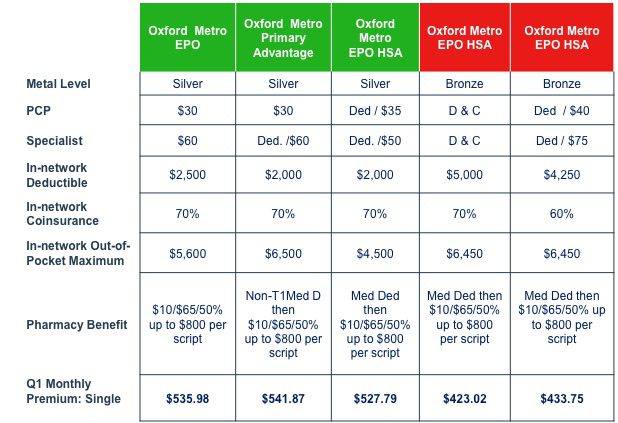

Oxford has released an affordable new plan for 2016 and not a moment too soon. With the recent exit of popular Health Republic of NY, Health Republic NY is Shutting Down, the market is starving for an affordable option.

Today’s largest networks with in-network only GOLD are priced at $9,000/single annually. They typically are accompanied with $50 copays and non-office exposures of $1,000 deductibles and coinsurance percent in network. The new Metro network is approximately 25% smaller than NY Liberty network with up to 15% IN SAVINGS. For example, an Oxford Liberty HMO Gold is $745 vs Oxford Metro Gold $650.

In 2015 Oxford’s Garden State Network originated the same game plan of offering a third network in addition to FREEDOM and LIBERTY. After all what good is a large network when one cannot afford to visit Providers? The third network answers the call for access to Providers with half the copays priced at approximately $1,500 less.

All Metal Levels will be included for all size groups including 1-99 & 100+. The new Oxford Metro plan will be limited to NY and NJ Garden State Network Providers. Referrals will be needed to see Specialists. Importantly, most NY Hospitals will be participating with the EXCEPTION of NYU Health System, North Shore LIJ Health System (NorthWell Health) and Maimonides Medical Center. In addition, certain key medical IPA Groups such as Mt Kisko Medical Group are NOT in the network.

The Healthy NY and off-exchange Individuals will use exclusively this new Oxford Metro Network.

Sign up for upcoming webinars and newsletters. Please contact us TODAY for a customized analysis for your group-specific needs at info@medicalsolutionscorp.com or Call (855) 667-4621.

Jeb Bush, running for the Republican presidential nomination, put out a detailed health proposal yesterday. The Bush campaign says the former Florida governor’s plan, in broad terms, would accomplish three goals: promote innovation, lower costs and return power to states.

Under Bush’s plan, individuals could get higher tax credits for purchasing health insurance and would be allowed higher contribution limits on health savings accounts for out-of-pocket expenses. He also would overhaul the regulations imposed by the Food and Drug Administration to help spur innovation in the healthcare industry and would put limits on malpractice lawsuits. And he would put caps on federal payments to states and create a “transition plan” for 17 million people “entangled” in Obama’s Affordable Care Act.

Bush also proposes to limit the tax-free status of employer-provided health insurance, an idea labor unions fiercely oppose.

Here are some key points to consider:

It would repeal and replace Obamacare.

Bush wants more people to have catastrophic coverage.

Bush would repeal the so-called Cadillac tax

Instead limit the Employer tax-free health benefits at $12,000 a year for an individual and $30,000 for a family.

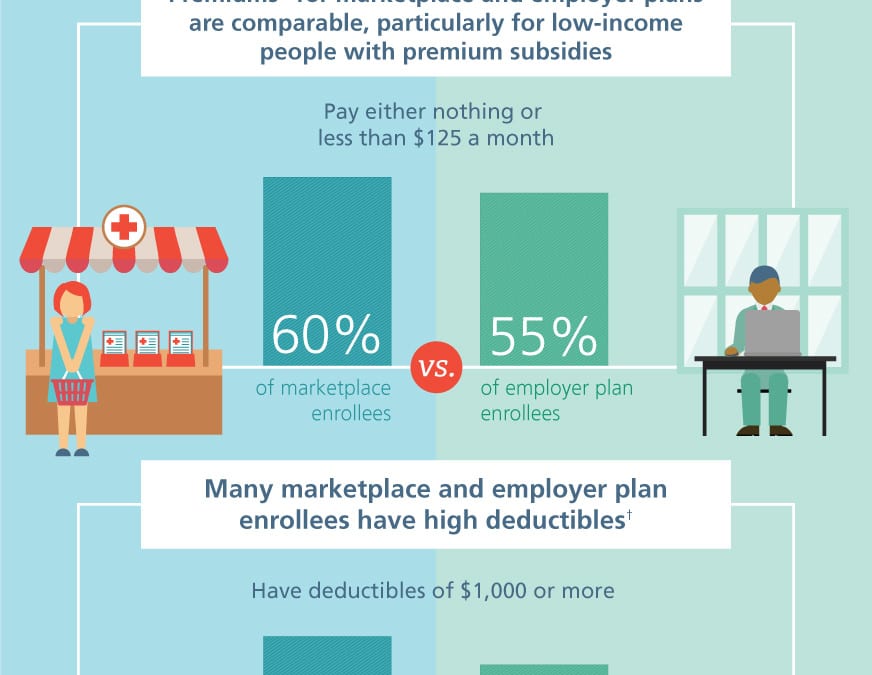

ACA Marketplace and Employer Health Plan Cost Comparison

Are you ready for 2016 Individual Open Enrollment? The #1 question we get form individuals is am I better off staying on the individual plan or joining my small employer group plan?

Starting Nov 1, 2015, the 3rd anniversary of Obamacare’s ACA Marketplace begins. Continuing through 2018, several new parts of the Affordable Care Act that affect costs and benefits will be rolled out. The remaining provisions will take effect against a backdrop of new patterns in health care spending and trends.

A frequent Employer question is how do costs compare on the ACA Marektplace vs. Employer Health Plans. The infographic from the Commonwealth Fund point out that the premiums are more favorable when factoring low income premium subsidies. In order to even the scales, an individual must earn $23,500 for a net subsidized premium of $125/month (click Kaiser calculator). This number represents 60% of marketplace enrollees. The same $125/month contribution amount represents 55% of employer health plans.

One positive point is that U.S. health care spending has slowed in the past few years. In a recent 16-month period, nearly 23 million Americans have enrolled in the Affordable Care Act, while almost 6 million people lost coverage. Research from Rand Corp. finds that of the newly insured:

42 percent are covered through employer-sponsored plans.

29 percent are enrolled in Medicaid.

18 percent have health coverage in individual marketplaces.

Take a look at the infographic:

2016 Open Enrollment Deadlines:

November 1, 2015: Open Enrollment starts — first day you can enroll in a 2016 insurance plan through the Health Insurance Marketplace. Coverage can start as soon as January 1, 2016.

FYI2016 plans and prices will be available for preview the third week of October, 2015.

December 15, 2015: Last day to enroll in or change plans for new coverage to start January 1, 2016.

January 1, 2016: 2016 coverage starts for those who enroll or change plans by December 15.

January 15, 2016: Last day to enroll in or change plans for new coverage to start February 1, 2016

January 31, 2016: 2016 Open Enrollment ends. Enrollments or changes between January 16 and January 31 take effect March 1, 2016.

If you don’t enroll in a 2016 health insurance plan by January 31, 2016, you can’t enroll in a health insurance plan for 2016 unless you qualify for a Marketplace Special Enrollment Period.

Penalty: The uninsured penalty rises to $695 or 2.5% of your income, whichever is higher.

Coverage start dates

If you enroll before the 15th of any month, your coverage starts the first day of the next month. If you enroll after the 15th of the month, you’ll have to wait until the month after that for your coverage to start. So, for example, if you enroll on January 16, your coverage would start on March 1.

Enroll using our online comparison shopping tool for both on and off-Exchange Marketplace to be released next week. Email us or Contact us at (855)667-4621.

BREAKING: The young Co-Op start up of 2014 will be shutting down Dec 31, 2015. With membership totals approx. 200,000+ the early exit comes as a shocking surprise despite their recent losses and 15-20% rate increase approved for 2016.

On Friday, a joint announcement came from the state Department of Financial Services, the Department of Health and the federal Centers for Medicare and Medicaid Services (CMS), with DFS directing Health Republic to cease writing new health insurance policies and begin an orderly wind-down of business.

“Given Health Republic’s financial situation, commencing an orderly wind down process before the upcoming open enrollment period is the best course of action to protect consumers,” said Anthony Albanese, acting superintendent at DFS. “Moving forward, we will work closely with New York State of Health and federal regulators to help ensure continuity of coverage for Health Republic’s customers.”CMS officials said decision was made after state and federal agencies determined it was likely Health Republic would become financially insolvent.

According to recent announcements Health Republic of NY was exiting the small group and individual markets for Mid-Hudson, Albany, and Utica/Watertown regions. These counties include: Albany, Columbia, Delaware, Dutchess, Essex, Greene, Hamilton, Oneida, Orange, Oswego, Putnam, Rensselaer, Saratoga, Schenectady, Sullivan, Ulster, Warren, and Washington. The reasoning was the high delivery costs driven by Provider consolidation, see https://healthrepublicny.org/media/2563/faqs-service-area-reductions.pdf.

With recent exits for Insurers such Atlantis, Emblem Health/GHI and Empire blue Cross the transitions were handled differently. Some allowed groups to see their plan through renewal anniversary date or end of year. Further announcements are expected on transition of coverage.

Our Agency as in the past will be out and early in front positioning our clients for best options. For more information on this or to schedule a call please contact us info@medicalsolutionscorp.com today.

Breaking News: NSLIJ, and Brooklyn’s Maimonides Announce Strategic Partnership on Wednesday. Both side shave been in talks since February.

Eventually North Shore-LIJ and Maimonides will fully integrate, “in a phased approach that will begin immediately,” the two jointly announced Wednesday. In the meantime, both institutions maintain their independence and separate governance structures. Lynam said there was no specific time frame for full integration.

Maimonides gets much-needed cash — tens of millions of dollars — for capital and operational investments. That will help it compete with Presbyterian-backed Methodist and Langone-backed Lutheran. North Shore-LIJ gets its first real foothold in #Brooklyn, one of the most competitive health care markets in the nation. But it does so without the commitment that a full-scale merger would entail. An affiliation agreement also protects North Shore-LIJ from unknown liabilities related to the Federation of Jewish Philanthropies, a malpractice insurer that covers Maimonides and several other hospitals

North Shore-LIJ has made strategic partnerships and acquisitions before. For North Shore-LIJ, the relationship means it has a hospital or hospitals in every borough as well as blanketing Westchester and Long Island. North Shore-LIJ, the country’s 14th largest health care system, owns 19 hospitals. In the city that includes Lenox Hill Hospital in Manhattan, Staten Island University Hospital, and, in Queens, Forest Hills Hospital, Long Island Jewish Medical Center, Cohen Children’s Medical Center and Zucker Hillside Hospital, a behavioral health center.

They are also actively insuring members today in the Downstate NY area under the CareConnect NSLIJ holding company. With important advantages under ACA and mindful of delivering value the insurance arm is priced affordably. In fact they had lowered their rates 15-20% for 2015 and and industry low 3.3% for 2016.

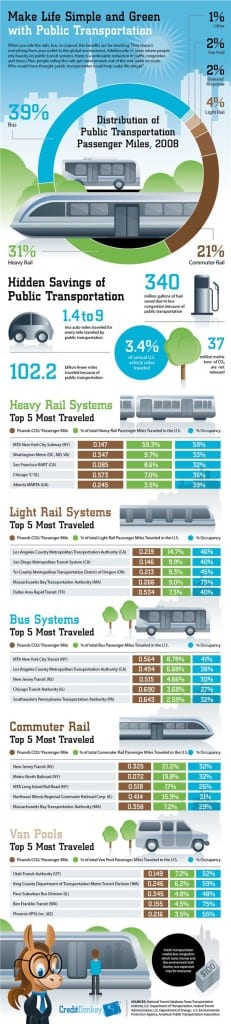

A fun visual transit infographic highlighting the benefits of public transportation by Credit Donkey. With NYC Transit Benefit Mandate for 2016 Employers with 20 or more full-time employees in New York City must sponsor for full-time employees a pre-tax qualified transportation benefit program (excluding parking subsidies). It would mean that an estimated 450,000 more New York City-based employees will have access to the commuter tax break. That’s in addition to the 700,000 who already get the break.

Despite the requirement this visual highlights the inherent win-win of riding public transit. Furthermore, Employers exempt form the mandate such as smaller Employer or outside NYC ought to consider this as a benefit per at work. IMPORTANT: The popularity of the benefit for Employers have been a budget neutral perk that is offset by payroll tax savings. After all, the Employer is not required to fund the Transit/Parking only sponsor the plan.

Tax Savings:

The way the pretax commuter tax break works is employees exclude their transit commuting costs from their taxable wages up to the $130 monthly limit (there’s a separate $250 monthly limit for parking). If you’re in the 40% combined federal and state bracket and you put away $130 a month pretax salary to use for transit, you save $624 a year. This also saves the employer money because the employer doesn’t pay payroll taxes of 7.65% on every dollar set aside by employees pre-tax.

$130 transit maximum

EE Savings @ 40% tax bracket = $624/year

ER Savings (FICA) = $119/year

$250 parking maximum

EE Savings @ 40% tax bracket = $1,200/year

ER Savings (FICA) = $230/year

Next Step:

If you want your employer to add commuter benefits—so you’re eligible for the tax break–petition your HR department, and specifically ask for the pretax commuter benefits program (why wait until 2016?). To learn more about the NYC Transit Mandate, please visit the official website of the City of New York.

To start a Transit benefit within 24 hours contact us today (855) 667-4621 or info@medicalsolutionscorp.com. Ask us about our enterprise payroll.

MMS, Inc. in partnership with BenefitMall adds allCheck ACA compliance tool! Want to know how to easily calculate your FTE’s ( Full Time Equivalents)? Not sure if you need to provide the Notice of Exchange? Unsure about your Health Care Tax Credit Eligibility? Want to get an idea what your overall ACA compliance obligations might be?

Let MMS inc. and allCheck do the work. How? Its simple. Download the input sheet, complete and we will crunch the numbers and send you a customized report just like the sample! Please call us 855-667-4621.

This law is new and constantly evolving. We (and everyone else) are still processing the thousands of complex provisions. The calculations here will change based upon your input, and is meant to be an educational tool for you to use in understanding how healthcare reform may impact your business. We recommend you work closely with your broker and local counsel to receive the most accurate and up-to-date information.

The rate requests for 2016 marked the first year in which insurers could rely on actual data from exchange enrollees. In many cases, insurers participating in exchanges in other states requested double-digit rate increases. New York is the second-largest state to receive final approval of its rate requests. Earlier this week, California insurance regulators approving an average rate increase of just 4 percent.

To the relief of customers of industry leader Oxford/UnitedHealthcare the rate increase for groups will be 3.9 to 6.5%. Importantly, the rates are a collective average and may range depending on one’s particular health plan. Additionally, Helath Insurers can opt to tweak or remove plans. Reminder: be sure to check back again our site in 30-60 days. Rates will be posted upon Health Insurer’s release. Also 2016 Individual Exchange Marketplace opens Nov 15th.

Individual Market

On average, insurers requested a 10.4 percent increase in health insurance rates for 2016 in the individual market. DFS reduced that average increase more than 30 percent to 7.1 percent – which is below the approximately 8 percent average increase in health care costs.

Starting on January 1, 2016, New York will add a new Basic Health Plan a.k.a ” Essential Health Plan” to the plans that can be purchased by lower income New Yorkers through NY State of Health. Households at or below 150 percent of the federal poverty level ($17,655 for a household of one; $36,375 for a household of four) will have no monthly premium for the Basic Health Plan. Those with slightly higher incomes at 200 percent of the federal poverty level ($23,540 for a household of one; $48,500 for a household of four) will have a low monthly premium of $20 for each adult.

The Basic Health Plan will provide the same covered services as other plans offered on the Marketplace. The Basic Health Plan has no annual deductible and lower copayments, making health care even more affordable for hundreds of thousands of New Yorkers. For example, a person who earns about $20,000 a year and uses moderate health care services including an inpatient hospital stay, prescription drugs and doctor’s visits, will pay about $730 a year for premiums and out-of-pocket costs under the Basic Health Plan in 2016 as compared to about $1,830 in 2015 if they were enrolled in a Qualified Health Plan.

Small Group Market

On average, insurers requested a 14.4 percent increase in health insurance rates for 2015 in the small group market. DFS reduced that average increase by 32 percent to 9.8 percent. A number of small businesses will also be eligible for tax credits that would lower those premium costs even further.

2016 Small Group Rate Actions – Overall Summary

Company

Requested

Approved

Reduction

Aetna Life

23.87%

21.47%

-2.40%

CDPHP HMO*

-19.84%

-19.84%

0.00%

CDPHP UBI*

16.56%

16.56%

0.00%

Emblem HIP*

29.74%

29.74%

0.00%

Empire Assurance

8.70%

3.40%

-5.30%

Empire HMO

9.21%

4.37%

-4.84%

Excellus*

13.90%

10.00%

-3.90%

Health Republic*

20.00%

20.00%

0.00%

HealthNow*

8.06%

0.66%

-7.40%

Independent IHA*

-15.60%

-15.60%

0.00%

Independent IHBC

-6.19%

-6.19%

0.00%

Managed Health

5.60%

3.94%

-1.66%

Metro Plus*

-0.81%

-0.81%

0.00%

MVP Health Plan*

7.28%

6.36%

-0.92%

MVP Services*

16.71%

15.90%

-0.81%

North Shore LIJ*

3.27%

3.27%

0.00%

Oxford OHI

13.61%

6.75%

-6.86%

Oxford OHP

10.58%

3.90%

-6.68%

United UHIC

18.79%

11.61%

-7.18%

All Companies Combined

14.41%

9.80%

-4.61%

You may view the DFS press release, which includes a recap of the increases requested and approved by clicking here.

For specific details on all available health plans in 2015, contact our team at Millennium Medical Solutions Corp (855)667-4621. We work in coordination with Navigators to assist with Medicaid, CHIP Child Health Plus, Family Health Plus and Medicare Dual Eligibles. We have Spanish, Russian, and Hebrew speakers available. Quotes can also be viewed on our site.

NYC become the 3rd U.S. City to require Employer Transit Benefits following SF and Washington, DC. Beginning in 2016, the ordinance will require employers (not including government employers) with 20 or more full-time employees in New York City to provide full-time employees a pre-tax qualified transportation benefit program (excluding parking subsidies). It would mean that an estimated 450,000 more New York City-based employees will have access to the commuter tax break. That’s in addition to the 700,000 who already get the break.

“The ordinance will require private employers with 20 or more full-time employees in New York City to provide a pretax qualified transportation benefit program for their full-time employees.” For purposes of the ordinance, a full-time employee is one who works 30 or more hours per week.

Penalties:

While the new ordinance goes into effect January 1, 2016, it provides a six-month grace period, so penalties will not begin until July 1, 2016. Penalties for a first violation will range from $100 to $250. If an employer corrects the violation within 90 days of being notified, then penalties will be waived. If correction (the steps for which have not yet been described) does not occur, penalties for the first violation will apply and an additional penalty will apply, equal to $250 for each 30-day period in which the employer continues to fail to offer the required benefits.

Tax Savings:

The way the pretax commuter tax break works is employees exclude their transit commuting costs from their taxable wages up to the $130 monthly limit (there’s a separate $250 monthly limit for parking). If you’re in the 40% combined federal and state bracket and you put away $130 a month pretax salary to use for transit, you save $624 a year. This also saves the employer money because the employer doesn’t pay payroll taxes of 7.65% on every dollar set aside by employees pre-tax.

$130 transit maximum NEW $255 transit maximum for 2016

EE Savings @ 40% tax bracket = $1200/year

ER Savings (FICA) = $230/year

$255 parking maximum

EE Savings @ 40% tax bracket = $1,200/year

ER Savings (FICA) = $230/year

Next Step:

If you want your employer to add commuter benefits—so you’re eligible for the tax break–petition your HR department, and specifically ask for the pretax commuter benefits program (why wait until 2016?). To learn more about the NYC Transit Mandate, please visit the official website of the City of New York. To start a Transit benefit within 24 hours contact us today (855) 667-4621 or info@medicalsolutionscorp.com.

The U.S. Supreme Court ruled this morning that the Affordable Care Act may provide nationwide tax subsidies for people who purchase health insurance through an exchange. The Court considered a challenge to a provision of the ACA concerning whether subsidies were available only to those who purchased health insurance on an exchange “established by the state.” The Court, in King v. Burwell, ruled 6 to 3 in favor of upholding the eligibility for people to receive subsidies through either a state or federal health insurance exchange.

The opposite ruling would have had serious implications for the country due to the number of states relying on a federally-run exchange (37 states) and the number of customers who qualify for subsidies based on their income (about 85% of customers nationwide). The Government’s argument prevailing: defending the subsidies, the Government argued that if you look at the entire ACA and its history, it is clear that the subsidies are available to everyone who purchases insurance on an exchange, no matter who created it.

Please join us for upcoming Webinar on How to Prepare for Current and Future ACA Requirements.

Are you able to identify and address all of the ACA requirements? Have you developed a plan of action to help stay in compliance? This webinar will walk you through a three year case study and provide you with current and future solutions to help your group prepare for ACA challenges including the Cadillac Tax.

Some of the key webinar highlights include:

Will Federal subsidies stop in some states making residents unable to access subsidized Exchange coverage?

3 year case study providing a practical view

Will IRS information reporting still be required?

Could Congress step in and propose changes to the existing ACA law?

2015 – Section 125 changes including eligibility, PRAs, excepted benefits and FSA plans for higher OOP exposure

2016 – Renewal focus on HSA’s with a dollar for dollar matching contribution

2017 – Further conversation of reducing benefit costs utilizing post deductible HRA’s and consideration of Defined Contributions

Practical information you can use – a webinar you will not want to miss!

The King Ruling awaits As Supreme Court schedules more decision days. The decision is expected to be possibly on Thursday on the legality of the Health care subsidies. ISSUE RECAP: At issue is whether subsidies that 8.7 million people receive to help pay for their insurance are available in all 50 states, or only those that set up their own health insurance exchanges. (more…)

Great news for families with HSA and high deductible plans. Individual out of pocket maximums will apply EVEN UNDER A FAMILY POLICY. New federal health care reform law regulatory guidance ends lingering uncertainty on how much in out-of-pocket costs employers with high-deductible plans can require employees to pick up.

The guidance, leaves intact the maximum out-of-pocket expenses employers can require employees to pay before health plan coverage kicks in: $6,850 for single coverage and $13,700 for family coverage when the rules go into effect in 2016.

An example illustrates how the HHS-imposed “EMBEDDED” limit on out-of-pocket expenses will work:

An employee and his or her spouse enroll in family coverage with an annual cost sharing limit of $13,000, and during the 2016 plan year, $10,000 of cost sharing payments are attributable to the spouse and $3,000 of cost sharing payments are attributable to the employee. Prior to the HHS’s clarification, the full $13,000 would be payable by the covered individuals because the $13,000 plan limit had not been reached on an aggregate basis. However, with the new EMBEDDED self-only limitation, the cost sharing payments attributable to the spouse must be capped at the self-only limit of $6,850, with the remaining $3,150 being covered 100% by the group health plan. The employee would still be subject to cost sharing, however, until the $13,000 plan limit is reached.

The biggest impact on the new cost-sharing rules will be on employers with high-deductible plans.

For the FAQs, visit: http://www.dol.gov/ebsa/pdf/faq-aca27.pdf

For more information and a free renewal evaluation please

HDHP Minimum Annual Deductible (No change from calendar year 2011):

Single – $1,300 (NONE, $1,300 in 2015)

Family – $2,600 (+$100, $2,500 in 2015)

HDHP Out-of-Pocket Maximum:

Single – $6,550 (+$100, $6,450 in 2015)

Family – $13,100 (+$200, $12,900 in 2015)

Age 55 Catch Up Contribution

As in 401k and IRA contributions, you are allowed to contribute extra if you are above a certain age. If you are age 55 or older by the end of year, you can contribute additional $1,000 to your HSA. If you are married, and both of you are age 55, each of you can contribute additional $1,000.

HSA/HDHP Market Growth

HSA holders own the assets in the accounts and can build up substantial sums over time. Enrollment in HSA-compatible insurance plans has increased to 10 million earlier this year, from 1 million in March 2005, according to, America’s Health Insurance Plans (AHIP), a trade group.

HSAs were authorized starting in January 2004. Since then, AHIP has conducted a periodic census of health plans participating in the HSA/HDHP market.

The number of people with HSA/HDHP coverage rose to more than 11.4 in January 2011, up from 10.0 million in January 2010, 8.0 million in January 2009, and 6.1 million in January 2008.

30 percent of individuals covered by an HSA plan were in the small group market, 50 percent were in the large-group market, and the remaining 20 percent were in the individual market.

14% of all workers in the private sector that have access to a Health Savings Account acc. to Bureau of Labor Statistics.

States with the highest levels of HSA/HDHP enrollment were California, Ohio, Florida, Texas, Illinois and Minnesota.

HSA Advantages:

Opportunity to build savings – Unused money stays in your account from year to year and earns tax-free interest. The HSA also gives you an investment opportunity.

Tax-free contributions and earnings – You don’t pay taxes on contributions or earnings.

Tax Free Money allowed for non traditional Medical coverage– As per IRS Publication 502, unused moneys can be used for dental,vision, lasik eye surgery, acupuncture, yoga, infertility etc. Popular Examples

Portability – The funds belong to you, so you keep the funds if you change jobs or retire.

Our overall experience with HSAs have been positive when employer funding is at minimum 50% using either the HSA or an HRA (Health Reimbursement Account-employer keeps unspent money). Traditional plans trend of higher copays and new in network deductibles has also led to the popularity of an HSA.

(Note that a health plan will not fail to qualify as a high deductible health plan merely because it provides certain preventive health services without a deductible, as required under Health Care Reform.)

Is your HSA compliant? Which pre-tax qualified HSA, FSA, HRA spending card is right for you? Please contact our team at Millennium Medical Solutions Corp (855)667-4621 for immediate answers.. Stay tuned for updates as more information gets released. Sign up for latest news updates.

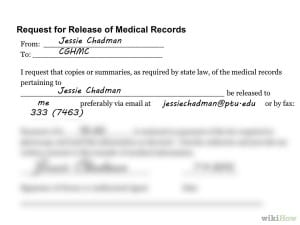

Anyone who has moved has been confronted with the question “How to Order Your Medical Records?”. Requesting your medical records may seem complex at first its simpler than one thinks.

1. Get a HIPAA release form. The federal law known as HIPAA entitles every person the right to access his or her medical records, receive copies of them, and request amendments to them.

2, Select your records. I would make this at least one month no more than 2 months This will give the office plenty of time to get you the records together. Specify the effective date, medical providers name, address, your name, address, medical record number ( you can get this from the staff) any identification numbers; i.e., Social Security Number or insurance ID number.

3. Submit forms. Fill out an authorization form giving one medical provider permission to share your records with another.Mark on that form which types of records you want included. Pay any fees that result.

4. Wait. The turnaround time under HIPAA can be 30 days. Most facilities, however, do not require that much time—many can fulfill a request in five to 10 days. Individual state laws may also dictate how quickly a facility must fulfill a request.

5. Follow up. In an imperfect world things can go wrong. What to do?

If your doctor has moved, you should be able to find your records at the practice she left. If that practice was affiliated with a hospital, the records may be housed within the hospital’s records system.

If your old provider says the records have been sent, but your new doctor’s office hasn’t received them, ask that they be re-sent. Doublecheck to make sure the old provider has the right contact information for your new one. You may find getting someone from your new doctor’s office involved could help. Having a nurse advocate for you, for instance, could put you in a better position.

If you’ve tried everything and are getting nowhere, offer to pick up the records yourself (but be aware that this may cost you), ask to speak with a manager or your doctor directly, or, as a final resort, contact your state medical board to file a complaint. This step is rarely necessary, but even suggesting you’ll have to go this route could get things moving on your request.

The Value of Requesting Your Records

There are many good reasons to request a copy of your medical records. Physicians don’t always share complete patient information or exchange a patient’s health records, so if a patient is seeing a new provider it is beneficial to ensure a copy of their record is sent to the new physician.. Also, it is beneficial for patients or caregivers dealing with multiple doctors and facilities to have all medical records in one place, which can then be used by providers to ensure thorough care.

Reviewing your record is an important way to ensure your provider has complete, correct, and up-to-date information, such as your known allergies. If you find information in your record that is incorrect or that you disagree with, contact the provider’s Health Info Management department.

Finally, it can be good for your health to keep a copy of your medical records, . Keeping an up-to-date copy of your health information will prevent redundant care, like repeat tests, and give all your physicians essential information about your health.

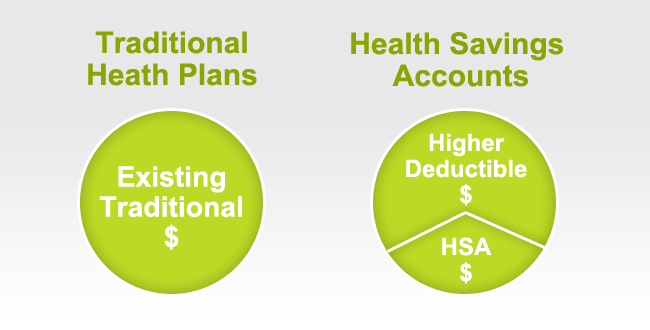

HSA-FSA-HRA: Whats the Difference? Health reimbursement arrangements (HRAs), health savings accounts (HSAs) and health care flexible spending accounts (HFSAs) are generally referred to as account-based plans. That is because each participant has their own account, at least for bookkeeping purposes. Under the tax rules, amounts may be contributed to these accounts (with certain restrictions) and used for health care on a tax-favored basis.

The Patient Protection and Affordable Care Act (PPACA) has added new requirements that affect HRAs and HFSAs. Most HFSAs and HRAs will need to be amended to meet the new PPACA requirements. HSAs generally are not affected by PPACA.

The chart below describes the main characteristics of these types of accounts, and should help you decide which is the best option for your particular situation.

Any employee who is also eligible to participate in a group medical plan sponsored by the employer; retired employees are eligible if most participants are active employees.

Any employee who is covered by a group medical plan sponsored by the employer (or if the employer chooses, by the spouse’s employer); retired employees are eligible (a retiree-only plan does not have to meet the medical coverage requirement).

Any employee who is covered by a high deductible health plan (HDHP), not covered by a plan that is not an HDHP, and not covered by any part of Medicare or eligible to be claimed as a tax dependent; individuals who are receiving Medicare may not contribute to an HSA.

May the employer impose additional eligibility requirements?

Yes, the employer may design the plan to cover whom it wishes as long as it meets the non-discrimination requirements.

Yes, the employer may design the plan to cover whom it wishes as long as it meets the non-discrimination requirements.

An employer may not limit the ability of an eligible employee to contribute to an HSA, but the employer may limit its contributions to employees participating in the HSA designated by the employer.

May an employee contribute to the account?

Yes, up to the lesser of $2,500 (indexed to $2,550 for 2015) or the maximum set by the plan (any carryover does not apply toward the $2,500 cap).

No.

Yes, up to the total contribution limit ($3,350 in 2015 for self-only coverage and $6,650 in 2015 for family coverage); individuals aged 55 or greater may contribute an additional $1,000.

May an employer contribute to the account?

Yes, up to two times the employee’s contribution plus $500.

Yes.

Yes, up to the total contribution limit described above.

May another person or entity contribute to the account?

No.

No.

Yes – anyone may contribute to an HSA, up to the total contribution limit.

Does the spouse’s coverage matter?

No.

An employer may – but is not required to — integrate the HRA with coverage through the spouse’s employer.

Yes. If the employee is covered by a non-HDHP through the spouse (which may include an HFSA or an HRA), the employee will not be eligible to contribute to an HSA.

Is a formal account required?

No, a notational/ bookkeeping account is allowed.

No, a notational/ bookkeeping account is allowed.

Yes, a trust or custodial account is required. Generally this is done at a bank or credit union.

Should a Section 125 cafeteria plan be used?

Yes – the HFSA must be part of a Section 125 plan.

No – an HRA may not be part of a Section 125 plan.

An HSA may, but need not be, part of a Section 125 plan. Including in a Section 125 plan will allow the employee to contribute with pre-tax dollars and allow the employer to meet the Section 125 non-discrimination rules instead of the comparable contribution rules.

What health expenses may be reimbursed?

All medical expenses allowed by Code Section 213 (which includes dental and vision expenses), except long term care services, may be reimbursed. Premiums may not be reimbursed.

All medical expenses allowed by Code Section 213 (which includes dental and vision expenses), may be reimbursed. Health premiums may be reimbursed for group coverage if not reimbursing (directly or indirectly) employee’s pre-tax premium. The cost of premiums for individual policies may not be reimbursed.

All medical expenses allowed by Code Section 213, except premiums (unless for COBRA, long-term care insurance or Medicare supplemental, which may be reimbursed).

May non-health expenses be reimbursed?

No.

No.

Yes, but income taxes and a 20% excise tax will apply.

Are limits on reimbursable expenses allowed?

Yes. An employer may exclude specific expenses if it wishes. It also may design the plan to be a “limited purpose” FSA to interface with an HSA option. Limited purpose FSAs typically only reimburse dental, vision and/or preventive care expenses, retiree expenses, or expenses in excess of the IRS high deductible.

Yes. An employer may exclude specific expenses if it wishes. It also may design the plan to be a “limited purpose” HRA to interface with an HSA option. Limited purpose HRAs typically only reimburse dental, vision and/or preventive care expenses, retiree expenses, or expenses in excess of the IRS high deductible.

No.

Whose expenses may be reimbursed?

The employee, spouse, children under age 27 and tax dependents, if the expense was incurred during the coverage period.

The employee, spouse, children under age 27 and tax dependents, if the expense was incurred while coverage is in effect.

The employee, spouse, children under age 27 and tax dependents – even if the person is not eligible to set up their own HSA – if the expense was incurred after the HSA is established.

How are expenses reimbursed?

Employee submits substantiated expense to claims administrator. May be paper or debit card.

Employee submits substantiated expense to claims administrator. May be paper or debit card.

Employee pays expense from HSA. May be paper or debit card. Employee is responsible for maintaining record to substantiate expense.

May expenses be reimbursed after employment terminates?

COBRA may be elected, generally until the end of the plan year in which termination occurred.

COBRA may be elected. Employer may design plan to allow reimbursement after termination, but employee must be given option to decline that extended coverage.

Yes.

May unused contributions be carried over from year to year?

Generally no; however, plan may be designed to allow carryover of up to $500 into next year or a grace period to incur claims attributable to prior year for up to 2-1/2 months.

Yes, if plan allows.

Yes (the account is the individual’s).

May an employee access funds before they have been contributed?

Yes – under the HFSA rules the employee must have access to the full planned contribution for the year on the first day of the coverage period.

Not required, but plan may be written to allow full access at start of year.

Generally no, although in certain situations the employer may advance contributions.

May planned contributions be changed mid-year?

Generally no. An employee may make a mid-year change only if allowed under the Section 125 change in status rules.

Yes (may require plan amendment and participant communications).

Yes – even if employee is contributing to the HSA through a Section 125 plan.

Do non-discrimination rules apply?

Yes, the Section 125 and the Section 105(h) rules apply.

Yes, the Section 105(h) rules apply.

Yes, either the Section 125 or the comparability rules apply.

May an employee participate in multiple accounts?

May participate in an HSA if HFSA is limited purpose; pays after HRA unless plan provides differently.

May participate in an HSA if HFSA is limited purpose; pays before HFSA unless plan provides differently.

Could also participate in a limited purpose HFSA or HRA.

Are a plan document and SPD required?

Yes (unless a government or church plan).

Yes (unless a government or church plan).

Not for HSA; will need for related HDHP.

Is a 5500 required?

If 100+ participants in the HFSA unless a government or church plan.

If 100+ participants in the HFSA unless a government or church plan.

No.

Is W-2 reporting required?

No, provided the HFSA is an “excepted benefit.”

No (reporting is currently optional).

Employer contributions are reported in Box 12 with code W; do not include in “cost of coverage” reporting under code DD.

Does the PCORI fee apply?

Not if an excepted benefit (if owed, fee is only due on employees, not dependents).

Yes, if HRA is the only self-funded plan using that plan year (fee is only due on employees, not dependents).

No.

Does the health insurance provider fee apply?

No.

No.

No.

Does the TRF apply?

No.

No.

No.

Do contributions apply to Cadillac tax?

Yes (both employer and employee).

Yes.

Yes (employer; probably employee if made through a Section 125 plan).

Do contributions apply toward minimum value determinations?

No.

Yes, if may only be used for cost-sharing (deductible, coinsurance, copays).

Yes.

Do employer contributions apply to affordability determinations?

No.

Yes, if may be used for premiums and/or cost-sharing.

No.

Qualifies as “minimum essential coverage”?

No.

Yes (if provides any medical benefits).

No.

Do HIPAA privacy requirements apply?

Yes.

Yes.

Not to HSA; may apply to related HDHP.

Is a Medicare Part D notice required?

No.

Yes, unless integrated with the Rx coverage.

Not for HSA; will need for related HDHP.

To qualify as an excepted benefit, an HFSA must be offered in conjunction with a group medical plan and the employer’s contribution cannot exceed two times the employee’s pre-tax contribution to the HFSA plus $500.

Beginning in 2014, HRAs must be available only to individuals actually covered by the group medical plan (or the spouse’s group medical plan if the plan provides). Participants must be given the option to decline further HRA reimbursement annually and when their employment terminates.

——————————————————————————

4/15/15

This information is general and is provided for educational purposes only and is subject to change. It is not intended to provide legal advice.

You should not act on this information without consulting legal counsel or other knowledgeable advisors.

With first new star rankings released yesterday by CMS (Center for Medicare & Medicaid Services) this will be a little easier for consumers. The role of Government in medical transparency have long been touted as a qualitative and cost factor. The patient experience Star Ratings will make it easier for consumers to use the information on the Hospital Compare website and spotlight excellence in health care quality.

The Hospital Compare star ratings relate to patients’ experience of care at almost 3,500 Medicare-certified acute care hospitals. The ratings are based on data from the Hospital Consumer Assessment of Healthcare Providers and Systems Survey (HCAHPS) measures that are included in Hospital Compare. HCAHPS has been in use since 2006 to measure patients’ perspectives of hospital care, and includes topics like:

• How well nurses and doctors communicated with patients

• How responsive hospital staff were to patient needs

• How clean and quiet hospital environments were

• How well patients were prepared for post-hospital settings

Only 251 hospitals–or 7 percent of those ranked–received a five-star rating under the new system, Kaiser Health Newsreported. The largest share of hospitals (40 percent) received three stars, including highly respected institutions such as Cedars-Sinai Medical Center in Los Angeles, NewYork-Presbyterian Hospital in Manhattan and Northwestern Memorial Hospital in Chicago. Only 3 percent of hospitals netted one star.

Consumers will now see 12 HCAHPS Star Ratings on Hospital Compare, one for each of the 11 publicly reported HCAHPS measures, plus a summary star rating that combines or rolls up all the HCAHPS Star Ratings. These star ratings will be updated each quarter. Also, the Nursing Home Compare site already uses star ratings to help consumers compare nursing homes and choose one based on quality.

Dark, Milk or White – Which Chocolate Is Best for Your Heart? (Infographic)

From our wellness partner, Cleveland Clinic

Chocolate is good for blood flow, which means it’s good for your heart. But not all chocolate is created equal. Find out about the healthy antioxidants and what else is inside so you can make the best choice of chocolate for your heart health.

Consumer complaints about receiving inadequate reimbursement from their insurers for medical services that they received outside of a provider network have been answered by New York’s “Emergency Medical Services and Surprise Bills” law. As of March 31, 2015, consumers will have protection from “surprise” medical bills for emergency medical services and certain out-of-network medical services.

The state of affairs today for small business plans offering both in and out of network is an exception with only 2 insurers in Downstate covering out of network at catastrophic high deductible levels. For Individual Marketplace it is even more dire with NO OUT OF NETWORK coverage at all.

The Problem. This has been a pattern in recent years and posted in Out of Control Out of Network Charges (March 2012). According to an investigation report commissioned by Governor Cuomo recognizing the unexpected out-of-network claim problem. Officials say that this is now “an overwhelming amount of consumer complaints.” Some examples cited in the report An Unwelcome Surprise – “a neurosurgeon charged $159,000 for an emergency procedure for which Medicare would have paid only $8,493.” Another example: ” a consumer went to an in-network hospital for gallbladder surgery with a participating surgeon. The consumer was not informed that a non-participating anesthesiologist would be used, and was stuck with a $1,800 bill. Providers are not currently required to disclose before they provide services whether they are in-network.” The average out-of-network radiology bill was 33 times what Medicare pays, officials say.

The blog post goes on to say “Today, 90% of SMB members have in network only benefits but the few remaining consumers are paying for eroding out of network benefits with little transparencies and necessary protection from new out of network billing practices. The NY Dept of Financial services is calling for providers in non-emergency situations to disclose whether or not all services are in-network, what out-of-network charges will be and how much insurers will cover.”

Balance Bill Protection. The long awaited bill passed last April protects patients from out-of-network providers from “balance-billing” consumers for emergency care or when patients can’t choose their doctors. Balance-billing occurs when health workers who don’t accept a patient’s insurance try to collect the difference between their charge and the insurer’s reimbursement.

Provider Disclosure Requirements. Hospitals will now be required to disclose anticipated charges. Patients most often receive these surprise bills in emergency cases, when they can’t choose the doctors who treat them. Its not unusual for a Provider to come into the picture who may read your tests or touch you thats not in network. Under the new law all medical providers will have to notify patients before treatment if they don’t take their insurance. If not, patients will be required to pay only a regular co-pay as if the provider was in network.

Providers will need to provide patients with disclosures of the health plans with which they participate and the names of the providers that may be billing them. They are also required to disclose procedures to follow with the an independent dispute-resolution entity (IDRE) which will be the arbiter of disputes under the law if a patient feels that a bill is inappropriate.

Network Adequacy. While the Affordable Care Act didn’t address surprise bills, the government has imposed network adequacy requirements that prevent health plans from having too few providers, which may reduce the number of cases where patients find themselves inadvertently out-of-network. New York will now require doctors and hospitals to disclose their network status before treatment in non-emergency procedures. Insurers will have to update online provider directories within 15 days of a change.

Prior to the Surprise Bill Law, these network adequacy rules only applied to health maintenance organizations (HMOs) and other “managed care” plans. HMO’s normally have more Provider/Insurer responsibility shifting form the patient. As with most non-HMO plans, however, the responsibility rests with patient to make sure everything is pre-authorized and in network is possible. Starting next month Health plans that are also based on more comprehensive PPO and EPO are also required to be certified as having provider networks that can meet the health needs of their members without having to rely on more expensive out-of network services.

A patient protection law is a welcome respite form the unfair unwelcome surprises out of one’s control. Common sense finally prevails!

“The deadline for individuals and families to enroll in a qualified health plan through NY State of Health is February 15, 2015. However, the Marketplace will provide additional assistance to those individuals who have taken steps to apply for coverage but have been unable to complete the enrollment process before the deadline. All applications and enrollments in health plans must be completed by the end of the day on February 28, 2015. Those who complete their enrollment after February 15, 2015 but on or before February 28, 2015 will have coverage starting on April 1, 2015.”

2/12/15

Last days for 2015 Individual Open Enrollment is ending this week. This deadline applies to both On and Off Exchange!

If you’re wondering about the penalty for not having insurance: yes, there is one, and no, you can’t really get out of paying for it. You’ll pay the penalty when you file your taxes for 2015. Even if you get coverage midway through the year, you’ll still need to pay a penalty for the months you weren’t insured. So get covered!

Think you might be eligible for a subsidy or aren’t sure?

You can check here at the New York State of Health Marketplace calculator. If you are eligible or think you might be eligible, you can contact the marketplace directly to purchase a plan or ask questions about financial assistance.

Please remember that during open enrollment you are permitted to switch carriers. Choose wisely because after February 15, one cannot switch plans until open enrollment 2015, unless you have a “qualifying event,” such as marriage, divorce, birth or adoption.

Individual Online Enrollment Resources for On and Off Exchange:

For NYS – To view Oscar’s plans, rates and simple online enrollment application, click here.

For more information on enrollment please contact our team at Millennium Medical Solutions Corp (855)667-4621. We have Spanish, Russian, and Hebrew speakers available.

Last week, the Georgetown University’s Center on Health Insurance Reforms, in conjunction with the Urban Institute, released a report about the role health insurance agents and brokers have played enrolling and supporting millions of new people in coverage over the past year. The study, which is favorable about the role of the broker in the new health insurance marketplace, makes six policy recommendations that the authors believe would help agents assist even more consumers in the years ahead.

This study provides valuable academic evidence to the continued and future role health insurance agents have in helping support both individual and business consumers with their coverage needs in a reformed health insurance marketplace. Many of the recommendations the authors make are reforms that SMB have called for to better support agents and brokers in both the federal and state-based exchanges since day one.

The conclusive outcome is that Brokers will be needed as a sustainable model to support future enrollment. “Consequently, many may seek to leverage insurance brokers to conduct consumer education and help people enroll in marketplace plans. As evidenced here, sources interviewed have many concrete suggestions for increasing broker sales of marketplace plans, potentially increasing enrollment under the ACA. The amount that increased broker sales can reduce the number of uninsured.”

Reminder: 2015 Open Enrollment ends this week by Feb 15th. For more information regarding both Exchanges – Individual Exchanges or SHOP please contact our team at Millennium Medical Solutions Corp (855)667-4621. We have Spanish, Russian, and Hebrew speakers available. Quotes can also be viewed on our site.

What to do with the 1095-A form you received in the mail?

Attached below is the link to the web page with information on Premium Tax Credits and Form 1095-A. The resources on this link provide information on Form 1095-A, including Frequently Asked Questions and the toll free numbers provided for assistance.The resources on this page provide information about your Form 1095-A from NY State of Health. The Form 1095-A is used to reconcile Advance Premium Tax Credits (APTC) and to claim Premium Tax Credits (PTC) on your federal tax returns.

I didn’t apply to NY State of Health for financial assistance. Can you tell me if I can claim the PTC on my tax returns for 2014?

Who is in my tax family? How do I figure out if someone is a dependent?

How do I report health care coverage on my tax return?

How do I report the information from Form 1095-A on my tax return?

Do I need to complete Form 8962?

How do I complete Form 8962 on my tax return? How do I use the Form 1095-A to complete my Form 8962. What counts as income? What is my FPL?

Do I owe money to the IRS? Will I get a refund from the IRS? How much tax credits will I have to repay to the IRS? How much extra in tax credits will I get from the IRS?

I am self-employed. Can I claim my NY State of Health premiums as a business expense on my tax returns?

I had to pay back tax credits or got extra tax credits. Should I estimate my income differently for 2015?

How do I claim an exemption from the Individual Responsibility requirement?

Do I owe an Individual Share Responsibility Payment?

What income needs to be considered when calculating the Individual Shared Responsibility Payment?

I enrolled in a health plan with financial assistance and my income is now less than 100% FPL. Am I still eligible for the PTC?

If you have questions about Form 1095-A, Minimum Essential Coverage, PTC or the SLCSP table, call Community Health Advocates’ Helpline at 1-888-614-5400.

If you think we made a mistake on your 1095-A, call NY State of Health at 1-855-766-7860.

If you have questions about Form 8962 or other tax-related questions, visit www.irs.gov.

Please take the time to review. For more information, please

单击此处,了解 简体中文 保费税收抵免和 Form 1095-A 的相关信息。

Cliquez ici pour accéder à des informations sur les crédits d’impôt pour cotisation d’assurance et sur le Form 1095-A en français.

Klike la a pou jwenn enfòmasyon sou Kredi nan Taks sou Prim ak Form 1095-A nan Kreyòl Ayisyen.

Per ricevere maggiori informazioni in italiano sul credito d’imposta sul premio (Premium Tax Credit, PTC) e sul Form 1095-A, cliccare qui.

한국어로 된 보험료 세금 공제(Premium Tax Credits, PTA) 및 Form 1095-A에 대한 정보가 필요하신 경우 여기를 클릭하십시오.

Нажмите здесь, чтобы получить информацию о налоговых вычетах за страховые взносы и форме Form 1095-A на русском языке.

Haga clic aquí para obtener información en español acerca de los Créditos tributarios para la prima y el formulario 1095-A.

WestMed Medical Group has now joined the North Shore LIJ’s insurance – CareConnect Network! This is not a purchase. This partnership expands their footprint and makes CareConnect a compelling fit for individuals and groups located in Westchester. In addition, CareConnect has just announced CareConnect’s Network Expansion! Yale-New Haven Health and all their facilities are now in-network with CareConnect. Tools are available to search for providers with updated expansion to be added shortly.

A combined Hospital Insurance system is an intriguing concept thats not all that new. Pittsburgh’s UPMC has been delivering the same model in Western PA successfully. In NYS an integrated medical approach is new on the other hand and challenging in an open competitive loop. A high quality smaller network that is priced affordably and can offer Patient Concierge like service may be what the market is asking for. They may also be in a better position to manage patient health and Preventative Medicine. For Jan 2015, NSLIJ CareConnect will have a 20% reduction in most regions such as Westchester and NYC. For new rates, benefits and provider listings click – CareConnect NSLIJ

For more information, please

Press Release#

Award-Winning WESTMED Joins CareConnect!

We’re pleased to announce our continued network expansion with the addition of WESTMED Medical Group. With this practice, CareConnect members now have more access in Westchester County:

• 289 physicians in eleven office locations • On-site laboratory and radiology services • Four urgent care centers • Three NCQA recognized programs including the patient-centered medical home and diabetes Stay tuned as we continue to add access for your groups around the CareConnect service area

Open enrollment for the 2015 New York individual market season is right around the corner. Below are answers to commonly asked questions pertaining to individual market coverage for residents of New York State:

Q: What is the New York State of Health (NYSOH) exchange website? A:NYSOH provides NYS residents living between 139%-400% of the Federal Poverty Level, access to lower cost health insurance by supplying them with tax credit premium subsidies. Additional Cost Sharing subsidies are available to those living between 139%-250% of the FPL. All subsidy programs are subject to eligibility requirements. Additionally, NYSOH is where individuals can enroll in Medicaid (for those living below 139% of the FPL).

Q: Is the NYSOH government health insurance? Is that what “Obamacare” means? A: No. Individual health insurance is a relationship between a consumer, and a private health insurance company. NYOSH slips in between this relationship by forwarding tax credit money to the carrier on behalf of the subsidy-eligible consumer, and then the carrier bills the consumer for the difference in premium owed. “Obamacare” is simply the nickname of the new health insurance law, which (in part) assists individuals in obtaining health insurance.

Q: Do I have to have health insurance? A: Yes. As part of the individual mandate, all US citizens must enroll in Affordable Care Act-compliant health insurance…be it through your employer, the individual market, Medicare, or Medicaid. Citizens not enrolled in coverage will be fined by the IRS (less those who qualify for exemptions).

Q: What is the fine for not having health insurance? A: In 2015, the fine is 2% of household income per uninsured month. In 2016, this increases to 2.5% of household income per uninsured month.

Q: Do I have to enroll in individual coverage through NYSOH? A: No. Only people in need of tax credit subsidy assistance must enroll through the NYSOH exchange website.

Q: What if I don’t earn enough income to qualify for subsidy assistance for on-exchange health plans? A: People in NY living below 139% of the FPL will be eligible for Medicaid. Medicaid enrollments are conducted on the NYSOH website.

Q: If I am over the subsidy income limit threshold, how do I apply for coverage outside of the NYSOH website? A: You can enroll directly with a carrier, or, by contacting a licensed insurance broker for assistance. Off-exchange carrier applications are extremely simplified, requiring only a 1-2 page paper/PDF application to be completed in most cases, and with no government intervention.

Q: Can brokers assist me with my individual coverage written through the NYSOH website as well? A: Yes. Licensed brokers, who are also certified to write health plans on the exchange, can be found in the Broker directory on the NYSOH website. You can search using a specific broker’s first and last name, by selecting a specific Agency from the drop down list, or you can enter your ZIP Code to find one in your region.

Q: Do brokers charge fees for helping me secure an individual health plan? A: Brokers are not allowed to charge fees for assisting individuals with writing their health insurance.

Q: How do brokers get paid? A: Every time you pay your health insurance bill, a portion of your payment is allocated towards compensating a broker (just like with your auto or homeowners insurance). Most carriers pay broker commissions on the back end, which is completely transparent to the consumer. If no broker is utilized by the consumer, the carrier retains the commission. This means that whether you use a broker or not, you’ll be paying for one anyway.

Q: Don’t Navigators already provide these broker services? A: No. Sometimes referred to as “in person assistors” or “experts” by the NYSOH, Navigators are not licensed to write health insurance. They are trained employees or contracted agencies of the NYS government (funded by Federal grant money) to help individuals navigate the enrollment process on the NYSOH website only. They are not required by federal law to undergo criminal background checks, nor are they licensed by the NYS Department of Financial Services, which means they cannot make plan recommendations to health insurance consumers.

Q: Can a certified broker process my NYSOH enrollment for me? A: Yes. Brokers that are certified to write business on the NYSOH exchange website can drive the entire online enrollment process for the consumer. You just need to authorize a broker through your NYSOH account by logging in, and then clicking “Find a Navigator/Broker” towards the bottom left side of your NYSOH account home page. Once authorized, the broker you have selected will receive an email from the NYSOH that you are in need of assistance, and can now enroll you on your behalf.

Q: When can I enroll in individual health insurance? A: Like Medicare, the individual health insurance market is setup to have an open enrollment season. The individual market open enrollment window is from 11/15/14 through 2/15/15.

Q. Are there any exceptions to the open enrollment period?

A. Enrollment in Medicaid, Child Health Plus and the Small Business Marketplace continues all year.

Have a Qualifying Event?

Enroll Now using our online shopping tool where you can compare plans and prices and enroll

Find us on the Health Insurance Marketplace where you may qualify for help to pay for your health insurance. Qualifying Events for Exchange Marketplace. 76 percent of the uninsured are unaware of the looming March 31 sign-up deadline. Contact us at (855)667-4621.

Q: Can I enroll in coverage outside of the open enrollment season? A: Consumers can enroll in individual coverage outside the open enrollment season so long as a “Qualifying Life Event” exists. Examples of such events include the loss of a job, marriage, divorce, birth of a child, a change in subsidy eligibility, and others. Written proof of the QLE will be required when enrolling outside of the open enrollment season as established by the US Department of Health and Human Services.

Q: If I am subsidy eligible, and my income changes, what do I do? A: Consumers enrolled through the exchange who receive tax credits must notify the NYSOH Marketplace whenever a change of income is experienced. You can contact the marketplace call center at 855-355-5777 to update your income information.

Q: Am I limited to certain insurance companies if I am subsidy-eligible? A: No. Consumers who are subsidy-eligible may pick any plan they wish that is available on the NYSOH exchange website. However, subsidy-eligible individuals may not apply those tax credits towards health plans written outside of the NYSOH website (for example, Oxford Liberty plans, which are only available outside of the NYSOH Marketplace).

Q: I have completed the income portion of my on-exchange application, and I’m now ready to pick a plan. How can I find out more specific information pertaining to the available options in the market? A: A licensed insurance broker can help you understand the available health plans in the market, and can make plan recommendations specific to your needs and financial situation.

Q: I started my current individual plan in July 2014. Do I have to renew my plan on January 1st 2015? A: Yes. All individual market plans have calendar year deductible and maximum out of pocket accumulation periods, which resets on January 1st of any given year. So for example, if you lost your job (and your health insurance) effective 12/1/14, and then you enroll for individual coverage effective 12/1/14, you must renew your individual plan the following month (for 1/1/15) at the new carrier plan structures and rates.

Q: I already have individual market based health insurance. Can I change plans during the open enrollment season? A: Yes. Existing individual health insurance policyholders may change their plan during the open enrollment season. You may also change carriers should you wish to find a better solution for your needs. Talk to your licensed insurance broker about the available plan options in the market for 2015.

Q: My employer is offering me a health plan that I am not interested in. Can I waive my employer health plan and replace it with an individual plan, and receive tax credit subsidy assistance? A: The answer to the first part of the question is yes. Employees can choose to opt out of employer-sponsored health insurance, and can replace their coverage in the individual market.

With regards to receiving tax credit subsidies in these situations, yes, an individual can receive tax credit subsidies to help pay the cost of individual health insurance. However, in addition to the employee needing to meet tax credit eligibility requirements as discussed earlier, one of two additional conditions must be met to be eligible to receive subsidy assistance: 1) The employer’s health plan does not meet the minimum actuarial value of 60%, or 2) The employee’s single rate cost (self-only coverage, no dependents) for employer-sponsored coverage exceeds 9.5% of their household adjusted gross income (defined as “unaffordable” under the health care law).

Q: I’m applying for a tax credit subsidy. How do I determine my adjusted gross income? A: Your adjusted gross income can be found on line 37 of your 1040 tax return. Subsidy applicants who have a steady income can use this figure as a guide when determining tax credit eligibility for the upcoming tax year.

Those that do not have a steady income (e.g. sole proprietors, freelancers, single-person businesses, etc.) should speak with their accountants to determine their estimated adjusted gross income for the upcoming tax year.

Q: I was determined Medicaid eligible after applying for tax credit subsidy on the NYSOH website. However, my doctors do not take Medicaid. Can I opt out of medicaid and get a subsidized individual health plan instead? A: You may choose to opt out of Medicaid if you wish. However, those who are Medicaid eligible will not qualify for tax credit subsidies for individual health plans. You can enroll in a health plan, but you must pay the full price of the plan.

Q: I was determined subsidy eligible, and I want to pick a plan to enroll in through the NYSOH website. Can I put my children on my health plan with my spouse and I? A: No. Those who are subsidy eligible must insure their dependent children through a Child Health Plus plan. CHP (or “chip”) plans are selected during the plan check out process at the end of the NYSOH application. Only the applicant and spouse will qualify for a private health plan with subsidy assistance. If you choose to opt your children out of CHP, you and your spouse will lose subsidy eligibility for your private health plan.

Q: How can I find out if my doctors take a particular health plan? A: Your licensed insurance broker can provide you with carrier-specific tools to look up providers in particular networks.

Q: How can I get a copy of the full benefit summary for a particular health plan I’m interested in? A: Your licensed insurance broker can provide you with electronic benefit summaries for most health plans upon request.

Q: How can I find a licensed broker to assist me? A: Licensed insurance brokers, and who are also certified to write on-exchange plans, can be found in the Broker directory on the NYSOH website. You can search using a specific broker’s first and last name, by selecting a specific Agency from the drop down list, or you can enter your ZIP Code to find one in your region.

For more information regarding both Exchanges – Individual Exchanges or SHOP please contact our team at Millennium Medical Solutions Corp (855)667-4621. We have Spanish, Russian, and Hebrew speakers available. Quotes can also be viewed on our site.

Phelps Memorial Hospital and North Shore LIJ Health System have signed an acquisition agreement. The two organizations expect the signed agreement to receive all necessary regulatory approvals later this year.

Phelps was one of two hospitals who signed a Letter of Intent this Summer. Northern Westchester Hospital based in Mt. Kisko was the second one. Both potential hospitals would give the fast growing NSLIJ insurance company CareConnect a string foothold in Westchester. Additionally, CareConnect has an affiliate agreement with Montefiore Hospital who’s Bronx base has expanded into Westchester with acquisition of New Rochelle Hospitals – Montefiore Buying Sound Shore Hospital as well as a partnership with White Plains Hospital –Montefiore Health System and White Plains Hospital Sign Formal Agreement.

It will invest in infrastructure improvements and clinical program expansion at Phelps. The 238-bed Sleepy Hollow facility will become the system’s 18th hospital. With Phelps’ 1,700 employees, NS-LIJ has about 50,000 workers, which it said ranks it as the largest private employer in New York state. North Shore-LIJ expects to secure regulatory approvals for the acquisition later this Fall.

A combined Hospital Insurance system is an intriguing concept thats not all that new. Pittsburgh’s UPMC has been delivering the same model in Western PA successfully. In NYS an integrated medical approach is new on the other hand and challenging in an open competitive loop. A high quality smaller network that is priced affordably and can offer Patient Concierge like service may be what the market is asking for. They may also be in a better position to manage patient health and Preventative Medicine. For Jan 2015, NSLIJ CareConnect will have a 20% reduction in most regions such as Westchester and NYC. For new rates, benefits and provider listings click – CareConnect NSLIJ

The people have spoken at least for now and they are saying they are unhappy. The storm clouds over Obmacare has ushered in GOP victories: +7 Senate + 13 House. 47% of those who cast ballots in the midterms said the 2010 health care law, which opened for enrollment a year ago, went too far. On the other hand, 26 percent said the law didn’t go far enough, CNN exit polls reported. Only 22 percent said Obamacare was just about right.

How will GOP use these powerful election gains on Obamacare?

GOP still will not have the needed 60 Senate Seats to repeal the Affordable Care Act. That said, they will now be able to pass budget rules on the legislation since the Courts ruled individual mandate penalty as a “tax”. Reinsurance funds such as Risk corridors could also be on the chopping block. Other examples would be the definition of “full-time” employee taxes on employer penalties (bipartisan support), medical devices & tanning salons etc.

According to Huffington Post article GOP-Controlled Congress Expected To Try To Repeal, Weaken ACA while Republicans have been “chomping at the bit to repeal Obamacare” since it was signed into law in 2010, even a GOP-controlled Congress is unlikely to undo the law. However, that won’t stop Republicans from forcing at least one vote on repeal. President Obama “would then swiftly veto it, but not before Democratic senators were forced to cast a vote very directly in support of Obamacare, which remains generally unpopular.” Additionally, the GOP might take aim at several provisions of the ACA, such as the individual mandate, the employer mandate, the Independent Payment Advisory Board, and the medical device tax. Some Senate Democrats would likely join them in eliminating or amending some of these measures.

A Democrat President governing with both Houses going GOP may not be so bad after all. The successful Clinton Presidency had to contend with the same balancing act. Two decades later, the key question is can both branches find a common ground and a productive working relationship?

For specific details on all available health plans in 2015, contact our team at Millennium Medical Solutions Corp (855)667-4621. We work in coordination with Navigators to assist with medicaid, CHIP Child Health Plus, Family Health Plus and Medicare Dual Eligibles. We have Spanish, Russian, and Hebrew speakers available. Quotes can also be viewed on our site.

The NCQA believes its own health plan accreditation program and program data could useful to exchange programs, the NCQA says. With so much more individual choice on both, the Marketplace Health Exchange and off-Exchange along with new Health Insurers this is an important consumer tool.

About NCQA

NCQA is a private, non-profit organization dedicated to improving health care quality. NCQA’s Healthcare Effectiveness Data and Information Set (HEDIS®) is the most widely used performance measurement tool in health care. NCQA accredits and certifies a wide range of health care organizations and recognizes physicians in key clinical areas. NCQA is committed to providing health care quality information through the Web, media and data licensing agreements in order to help consumers, employers and others make more informed health care choices.

NCQA accreditation ratings are based on three sets of measurements HEDIS®, CAHPS® and NCQA accreditation standards. Health plans in every state, the District of Columbia and Puerto Rico are NCQA Accredited. These plans cover 109 million Americans or 70.5 percent of all Americans enrolled in health plans.