Recently, UHC/Oxford and Mt Sinai Health System had split effective January 1, 2024. Since that time there have been a state-required cooling-off period and ongoing talks on resolution but that has not yielded a positive outcome yet. The Mount Sinai Hospital, Mount Sinai Queens, and their related hospital outpatient locations will remain in-network for all patients until at least Friday, March 1.

According to UnitedHealthcare/Oxford:

People enrolled in UnitedHealthcare fully insured commercial plans have continued network access to all of Mount Sinai’s hospitals through Feb. 29, 2024, due to New York cooling-off requirements.

Unless they obtain admitting privileges to another in-network hospital, the majority of Mount Sinai’s physicians will no longer participate in our network for employer-sponsored and individual plans, including the Oxford Health Plan, effective March 22, 2024.

This negotiation only impacts our relationship with Mount Sinai for employer-sponsored and individual commercial plans, including Oxford. All other active contracts, including Medicare Advantage and the Empire Plan, remain in place with no change.

The two organizations had a three-year agreement that took effect on Jan. 1, 2022, which was canceled before it was supposed to expire amid a dispute over payment rates. Both institutions are blaming one another for the standoff.

Mount Sinai claims UnitedHealthcare compensates it an average of 30% less for care than other health systems in New York. The insurer pays New York-Presbyterian $25,911 for a normal vaginal birth, and Mount Sinai $15,989, Mount Sinai said.

“Mount Sinai must be paid fairly,” spokeswoman Lucia Lee said in a statement. “As Mount Sinai costs substantially less than our peers, UHC/Oxford will actually end up paying more for patients to get care at other systems in New York. This cost — estimated to be at least $140 million more over the course of a year — will be passed on to employers and patients.”

UnitedHealthcare says Mount Sinai sought “outlandish price hikes” that would increase costs for services an average of 50% over three years or $600 million — an estimate disputed by Mount Sinai. For example, a regular, outpatient colonoscopy at South Nassau costs about $6,000 and would be about $8,700 in three years under Mount Sinai’s proposal, according to UnitedHealthcare.

Mt Sinai Hospitals & Health System

Facility Name

County

Mount Sinai Beth Israel

NYC

The Mount Sinai Hospital

NYC

Mount Sinai Morningside

NYC

The Mount Sinai West

NYC

Mount Sinai-Union Square

NYC

Mount Sinai Kravis Children’s Hospital

NYC

Mount Sinai-Behavioral Health Center (MSBHC)

NYC

Blavatnik Center, Medical Center

NYC

New York Eye and Ear Infirmary of Mount Sinai

NYC

Mount Sinai Brooklyn

Brooklyn

Mount Sinai Queens

Queens

Mount Sinai South Nassau

Long Island

Neighboring Hospitals

Bellevue Hospital Center

NYC

New York Presbyterian Queens

Queens

Elmhurst Hospital Center

Queens

New York Presbyterian Weill Cornell

NYC

Flushing Hospital Medical Center

Queens

North Shore University Hospital Manhasset

Long Island

Lenox Hill Hospital

NYC

NYU Langone Hospital Brooklyn

Brooklyn

Long Island Jewish Medical Center

Brooklyn

NYU Langone Hospital Long Island

Long Island

Maimonides Medical Center

Brooklyn

St. Francis Hospital

Long Island

Mercy Medical Center

Long Island

St. Johns Episcopal Hospital

Queens

New York Presbyterian Columbia

NYC

St. Joseph Hospital

Queens

New York Presbyterian Lower Manhattan Hospital

NYC

Wyckoff Heights Medical Center

Brooklyn

Both sides need each other as both are market leaders in their fields. It is our hope and most of our clients that they get this resolved soon. In the meantime, please bookmark our site for the latest updates. And do reach out to us and learn the steps that you can take to smoothen this temporary roadblock.

This Compliance Overview is not intended to be exhaustive nor should any discussion or opinions be construed as legal advice. Readers should contact legal counsel for legal advice.

In preparation for open enrollment, Employers should review their plan documents in light of changes for the plan year beginning Jan 1, 2024. Below is an Employer 2024 Open Enrollment Checklist including some administrative items to prepare for in 2024.

Change has been constant for employer plans in the last few years. Unfortunately, 2023 was no exception. As they prepare for 2024 open enrollment, employers must incorporate new requirements affecting the design and administration of their health plans for plan years beginning on or after Jan. 1, 2024. Those changes include items that are adjusted for cost of living changes each year, – e.g., the cost-sharing limits for high deductible health plans (HDHPs), contribution limits to health savings accounts (HSAs), as well as new requirements due to legislative and regulatory updates, such as the expiration of COVID-19 mandates, to name a few.

Employers should ensure their health plan is updated and communicate benefit changes to participants through an updated summary plan description (SPD) or a summary of material modifications (SMM) for the 2024 plan year.

As a general best practice, employers should confirm that their open enrollment materials contain certain required participant notices and consider including some periodic notices, such as the Medicare Part D creditable/non-creditable coverage notice, in their open enrollment materials.

PLAN DESIGN CHANGES

ACA Mandates

Affordability Requirements

Under the ACA’s employer shared responsibility rules (the “pay or play” rules), applicable large employers (ALEs) (those with 50 or more full-time employees or the equivalent) are required to offer affordable, minimum value health coverage to their full-time employees (and dependent children) or risk paying a penalty.

Under the ACA, an ALE’s health coverage is considered affordable if the employee’s required contribution to the plan does not exceed 9.5% of the employee’s household income for the taxable year (as adjusted each year). The adjusted percentage is 9.12% for 2023.

The affordability percentage for plan years that begin on or after Jan. 1, 2024, will be 8.39%. That is another reduction demonstrating the need for ALEs to monitor the affordability percentage each year so they can confirm that at least one of the health plans offered to full-time employees satisfies the ACA’s affordability standard (typically by the use of one of the optional safe harbors – federal poverty level, W-2 or rate of pay).

Out-of-pocket Maximum

Under the ACA, non-grandfathered health plans (which apply to almost all employer plans) are subject to limits on cost sharing for essential health benefits. Confirm that out-of-pocket maximum limits for your health plan comply with the ACA’s limits for the 2024 plan year.

Plan years beginning on or after Jan. 1, 2024:

$9,450for self-only coverage

$18,900for family coverage

Note, the out-of-pocket maximum limits for HDHPs compatible with HSAs must be lower than the ACA’s limits. For the 2024 plan year, the out-of-pocket maximum limits for HDHPs are $8,050 for self-only coverage and $16,100 for family coverage.

Preventive Care Benefits

The ACA requires non-grandfathered health plans to cover certain preventive health services without imposing cost-sharing requirements (e.g., deductibles, copayments, or coinsurance) when in-network healthcare providers supply the services. The preventive care services covered by the requirements are based on the following:

Evidence-based items or services that have a rating of A or B in the current recommendations of the United States Preventive Services Task Force (USPSTF).

Immunizations for routine use in children, adolescents, and adults that are currently recommended by the Centers for Disease Control and Prevention.

Evidence-informed preventive care and screenings are included in the Health Resources and Services Administration (HRSA) guidelines for infants, children, and adolescents.

Evidence-informed preventive care and screenings are included in HRSA-supported guidelines for women.

There needs to be some clarity. An ongoing court case has raised some uncertainty about using the USPSTF recommendations. However, guidance from federal agencies will permit employers to use those factors without the risk of penalties for the time being. Therefore, employers should monitor future developments regarding the ACA’s preventive care mandate, which is expected by the end of 2023.

Coverage For COVID-19 Vaccines, Testing And Treatment

Because the COVID-19 public health emergency has ended (seeAlert here), health plans are no longer required to cover COVID-19 diagnostic tests and related services without cost sharing or other medical management requirements. Health plans are still required to cover recommended preventive services (under the ACA requirements), including COVID-19 immunizations, without cost sharing, but this coverage requirement can now be limited to in-network providers.

For plan years ending after Dec. 31, 2024, an HSA-compatible HDHP is no longer permitted to provide COVID-19 testing and treatment benefits without a deductible (or with a deductible below the minimum deductible for an HDHP). Therefore, employers should

Determine whether health plans will impose cost-sharing requirements, prior authorization, or other medical management requirements on COVID-19 testing for the upcoming plan year.

Determine whether health plans will continue covering COVID-19 immunizations without cost sharing from all healthcare providers or whether this first-dollar coverage will be limited to in-network providers.

Confirm that HDHPs that do not have a calendar year as the plan year will not pay benefits for COVID-19 testing and treatment before the annual minimum deductible has been met for plan years ending after Dec. 31, 2024.

Notify plan participants of any changes for the 2024 plan year regarding COVID-19 testing and vaccines through an updated SPD or SMM.

The IRS issued a memorandum on claims substantiation (see Article here) for health FSAs. The memorandum clarifies that health FSA expenses are not considered properly substantiated if employees self-certify expenses, if the plan uses sampling, if only amounts over a certain level are substantiated, or if charges from favored providers are not substantiated. Employers should, therefore, review the health FSA substantiation procedures to make sure they comply with IRS rules.

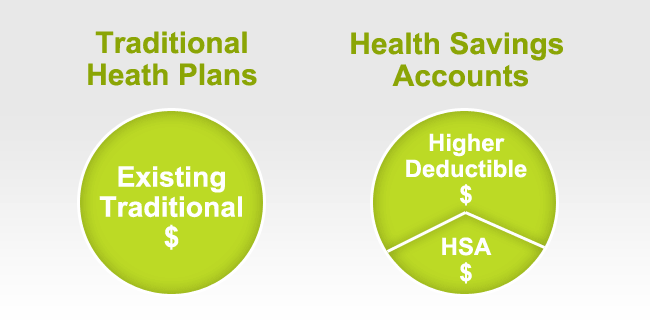

If you offer an HDHP to your employees that is compatible with an HSA, you should confirm that the HDHP’s minimum deductible and out-of-pocket maximum comply with the 2020 limits. The IRS limits for HSA contributions and HDHP cost-sharing increase for 2024. The HSA contribution limits will increase effective Jan. 1, 2024, while the HDHP limits will increase effective for plan years beginning on or after Jan. 1, 2024.

Check whether your HDHP’s cost-sharing limits need to be adjusted for the 2024 limits.

If you communicate the HSA contribution limits to employees as part of the enrollment process, these enrollment materials should be updated to reflect the increased limits that apply for 2024.

The following table contains the HDHP and HSA limits for 2024 as compared to 2023. It also includes the catch-up contribution limit that applies to HSA-eligible individuals who are age 55 or older, which is not adjusted for inflation and stays the same from year to year.

Type of Limit

2024

2023

Change

HSA Contribution Limit

Self-only

$4,150

$3,850

Up $300

Family

$8,300

$7,750

Up $550

HSA Catch-up Contributions (not subject to adjustment for inflation)

Age 55 or older

$1,000

$1,000

No change

HDHP Minimum Deductible

Self-only

$1,600

$1,500

Up $100

Family

$3,200

$3,000

Up $200

HDHP Maximum Out-of-pocket Expense Limit (deductibles, copayments and other amounts, but not premiums)

Self-only

$8,050

$7,500

Up $550

Family

$16,100

$15,000

Up $1,100

HDHP Design Option – Telehealth

At the beginning of the COVID-19 pandemic, Congress temporarily relaxed the rules for HDHPs to allow them to provide benefits for telehealth or other remote care services before plan deductibles were met without jeopardizing HSA eligibility. That relaxed rule currently applies for plan years beginning before Jan. 1, 2025.

Determine whether HDHPs will waive the deductible for telehealth services for the plan year beginning in 2024

Communicate plan changes for the upcoming year to participants through an updated SPD or SMM

Mental Health Parity – Required Comparative Analysis For NQTLs

The Mental Health Parity and Addiction Equity Act (MHPAEA) requires parity between a group health plan’s medical/surgical benefits and its mental health or substance use disorder (MH/SUD) benefits. These parity requirements apply to financial requirements and treatment limits for MH/SUD benefits. In addition, any nonquantitative treatment limitations (NQTLs) placed on MH/SUD benefits must comply with MHPAEA’s parity requirements. For example, NQTLs include prior authorization, step therapy protocols, network adequacy, and medical necessity criteria.

MHPAEA requires health plans and issuers to conduct comparative analyses of the NQTLs used for medical/surgical benefits compared to MH/SUD benefits. This analysis must contain a detailed, written, and reasoned explanation of the specific plan terms and practices and include the basis for the plan or issuer’s conclusion that the NQTLs comply with MHPAEA. Plans and issuers must make their comparative analyses available to specific federal agencies or applicable state authorities upon request.

Employers should request that health plan issuers (or third-party administrators) confirm that comparative analyses of NQTLs will be updated, if necessary, for the plan year beginning in 2024 and make the analysis available to the employee.

Open Enrollment Notices

Employers who sponsor group health plans should provide certain benefits notices in connection with their open enrollment periods. Some of these notices must be provided at open enrollment time, such as the Summary of Benefit and Coverage (SBC). Other notices, such as the WHCRA notice, must be distributed annually. Although these annual notices may be provided at different times throughout the year, employers often include them in their open enrollment materials for administrative convenience.

In addition, employers should review their open enrollment materials to confirm that they accurately reflect the terms and cost of coverage. In general, any plan design changes for 2024 should be communicated to plan participants through an updated SPD or an SMM.

Summary Of Benefits And Coverage

The ACA requires health plans and health insurance issuers to provide an SBC to applicants and enrollees each year at open enrollment or renewal. Federal agencies have provided atemplatefor the SBC, which health plans must use.

Note that for self-funded plans, the plan administrator is responsible for providing the SBC. For insured plans, the issuer usually prepares the SBC. If the issuer prepares the SBC, an employer is not required to also prepare an SBC for the health plan, although the employer may need to distribute the SBC prepared by the issuer.

Medicare Part D Notices

Group health plan sponsors must provide a notice of creditable or non-creditable prescription drug coverage to Medicare Part D-eligible individuals covered by, or who apply for, prescription drug coverage under the health plan. The notice alerts the individuals about whether their prescription drug coverage is at least as good as Medicare Part D coverage. The notice generally must be provided at various times that cannot always be anticipated, including when an individual enrolls in the plan and each year before Oct. 15 (when the Medicare annual open enrollment period begins). Therefore, the best practice is to provide it annually at open enrollment, as that will ensure timely compliance. Model notices are available on the Centers for Medicare and Medicaid Services’website.

Annual CHIP Notices

Group health plans covering residents in a state that provides a premium subsidy to low-income children and their families to help pay for employer-sponsored coverage must send an annual Children’s Health Insurance Program (CHIP) notice about the available assistance to all employees in that state. The U.S. Department of Labor (DOL) has provideda model notice.

Initial COBRA Notices

COBRA applies to employers with 20 or more employees who sponsor group health plans. Group health plan administrators must provide an initial COBRA notice to new participants and certain dependents within 90 days after plan coverage begins. The initial COBRA notice may be incorporated into the plan’s SPD. Because the COBRA election-period will not start until this notice is provided, it is helpful to many employers to include a copy in the open enrollment materials as a backup.

Notices Of Patient Protections

Under the ACA, group health plans and issuers that require the designation of a participating primary care provider must permit each participant, beneficiary, and enrollee to designate any available participating primary care provider (including a pediatrician for children). Additionally, plans and issuers that provide obstetrical/gynecological care and require a designation of a participating primary care provider may not require preauthorization or referral for such care. If a health plan requires participants to designate a participating primary care provider, the plan or issuer must provide a notice of these patient protections whenever the SPD or similar description of benefits is provided to a participant. If an employer’s plan is subject to this notice requirement, they should confirm that it is included in the plan’s open enrollment materials. This notice may be included in the plan’s SPD.Model languageis available from the DOL.

Grandfathered Plan Notices

If an employer has a grandfathered plan, they should include information about its grandfathered status in plan materials describing the coverage under the plan, such as SPDs and open enrollment materials. Model language is available from the DOL.

Notices Of HIPAA Special Enrollment Rights

At or before enrollment, an employer’s group health plan must provide each eligible employee with a notice of their special enrollment rights under HIPAA. This notice may be included in the plan’s SPD.

HIPAA Privacy Notices

The HIPAA Privacy Rule requires covered entities (including group health plans and issuers) to provide a Notice of Privacy Practices (or Privacy Notice) to everyone who is the subject of protected health information (PHI). Health plans are required to send the Privacy Notice at certain times, including to new enrollees at the time of enrollment. Also, at least once every three years, health plans must either redistribute the Privacy Notice or notify participants that the Privacy Notice is available and explain how to obtain a copy. Self-insured health plans are required to maintain and provide their own Privacy Notices. However, special rules apply for fully insured plans, where the health insurance issuer, not the plan itself, is primarily responsible for the Privacy Notice.

Special Rules for Fully Insured Plans

The plan sponsor of a fully insured health plan has limited responsibilities with respect to the Privacy Notice, including the following:

If the sponsor of a fully insured plan has access to PHI for plan administrative functions, they are required to maintain a Privacy Notice and to provide the notice upon request.

If the sponsor of a fully insured plan does not have access to PHI for plan administrative functions, they are not required to maintain or provide a Privacy Notice.

A plan sponsor’s access to enrollment information, summary health information, and PHI that is released pursuant to a HIPAA authorization does not qualify as having access to PHI for plan administration purposes.

Model Privacy Notices are available through the Department of Health and Human Services.

WHCRA Notices

Plans and issuers must provide notice of participants’ rights to mastectomy-related benefits under the WHCRA at the time of enrollment and annually. The DOL’s compliance assistance guide includes model language for this disclosure.

SARs

Plan administrators required to file Form 5500 must provide participants with a narrative summary of the information in Form 5500, called a summary annual report (SAR). Amodel noticeis available from the DOL.

Group health plans that are unfunded (that is, benefits are payable from the employer’s general assets and not through an insurance policy or trust) are not subject to the SAR requirement. The plan administrator generally must provide the SAR within nine months of the close of the plan year. If an extension of time to file Form 5500 is obtained, the plan administrator must furnish the SAR within two months after the close of the extension period.

Wellness Program Notices

Group health plans that include wellness programs may be required to provide certain notices regarding the program’s design. As a general rule, these notices should be provided when the wellness program is communicated to employees and before employees provide any health-related information or undergo medical examinations. These notices are required in the following situations:

HIPAA Wellness Program Notice—HIPAA imposes a notice requirement on health-contingent wellness programs offered under group health plans. Health-contingent wellness plans require individuals to satisfy standards related to health factors (e.g., not smoking) to obtain rewards. The notice must disclose the availability of a reasonable alternative standard to qualify for the reward (and, if applicable, the possibility of waiver of the otherwise applicable standard) in all plan materials describing the terms of a health-contingent wellness program. The DOL’scompliance assistance guideincludes a model notice that can be used to satisfy this requirement.

ADA Wellness Program Notice—Employers with 15 or more employees are subject to the Americans with Disabilities Act (ADA). Wellness programs that include health-related questions or medical exams must comply with the ADA’s requirements, including an employee notice requirement. Employers must give participating employees a notice that tells them what information will be collected as part of the wellness program, with whom it will be shared, and for what purpose, as well as the limits on disclosure and the way information will be kept confidential. The U.S. Equal Employment Opportunity Commission (EEOC) has provided asample noticeto help employers comply with this ADA requirement.

ICHRA Notices

Employers may use individual coverage HRAs (ICHRAs) to reimburse their eligible employees for insurance policies purchased in the individual market or Medicare premiums. Employers with ICHRAs must notify eligible participants about the ICHRA and its interaction with the ACA’s premium tax credit. In general, this notice must be provided at least 90 days before the start of each plan year. Employers may provide this notice at open enrollment time if it is at least 90 days before the beginning of the plan year. A model notice is available for employers to use to satisfy this notice requirement.

________________________________

Enhance Your Employee Benefits Package. A competitive benefits package is key to keeping and attracting top talent.Assess your current benefits package and consider making necessary adjustments to include options, such as expanded mental health support, for example.

GENERAL HR

Review Employee Records. The fourth quarter is a good time to review your employee records and check record retention guidelines. Don’t forget to dispose of outdated termination and outdated job applications properly. With W2s around the corner, make sure all addresses and information are updated.

Develop and Distribute Your 2024 Calendar. Create and distribute a calendar outlining important dates, vacation time, pay dates, and company-observed holidays for 2024.

Review and Update Employee Handbook. Review your employee handbook to make sure it is up-to-date and addresses areas, such as employment law mandates, new COVID-related policies, guidelines for remote working, privacy policies, compensation and performance reviews, social media policies, attendance, and time-off, break periods, benefits, and procedures for termination, discipline, workplace safety, and emergency procedures.

PLEASE NOTE: This Checklist is not intended to be exhaustive nor should any discussion or opinions be construed as legal advice. Readers should contact legal counsel for legal advice. This information is for general reference purposes only. Because laws, regulations, and filing deadlines are likely to change, please check with the appropriate organizations or government agencies for the latest information and consult your employment attorney and/or benefits advisor regarding your responsibilities. In addition, your business may be exempt from certain requirements and/or be subject to different requirements under the laws of your state. (Updated Sept 3, 2023)

Contact us at (855) 667-4621 or email us at info@360peo.com

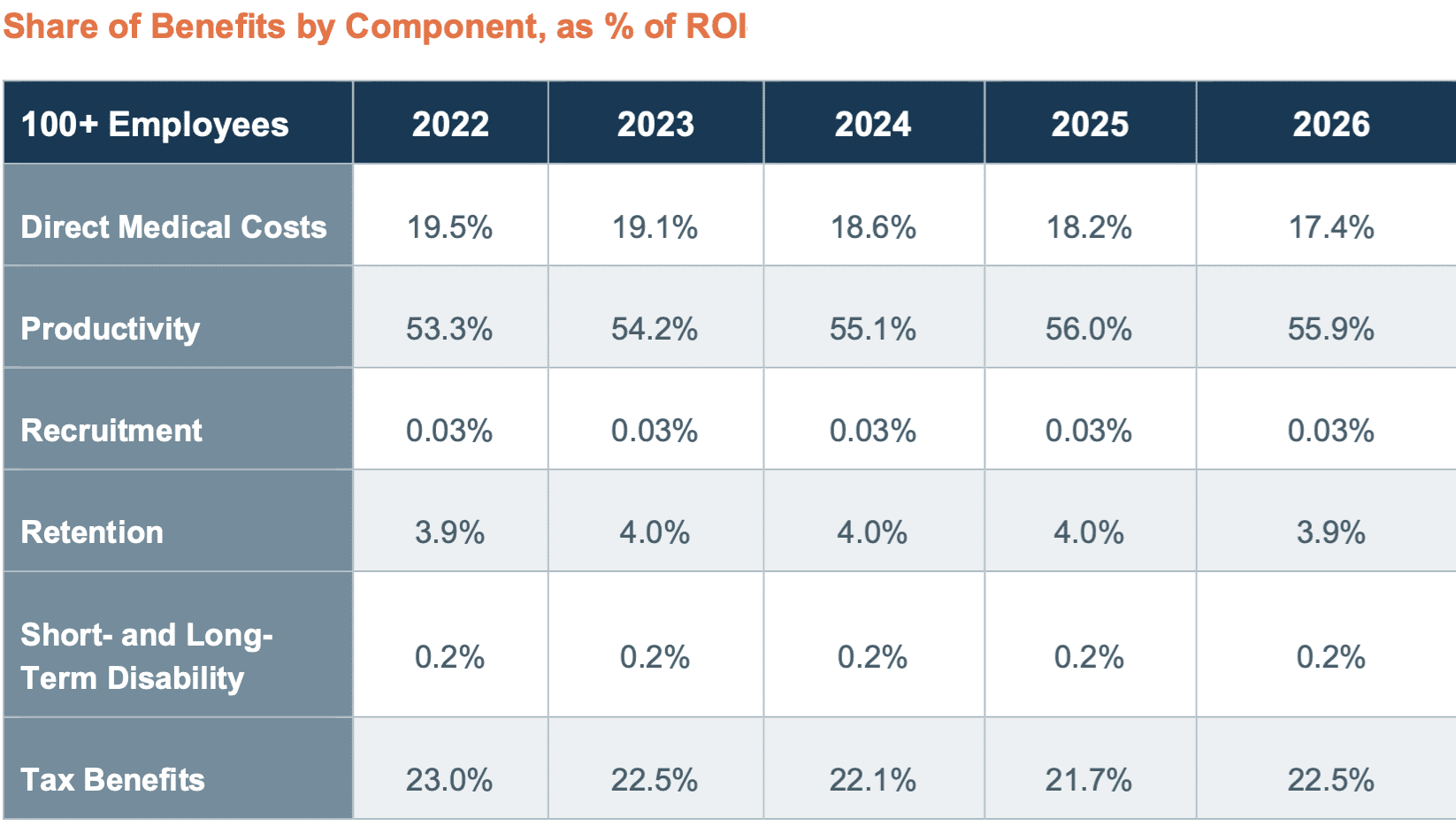

Health insurance is expensive, and we’ve all asked ourselves, “Is it really worth what I am paying?”. For employer-sponsored health insurance, the answer is a resounding YES it is. For every dollar employers spent on health insurance-related costs, they get back $1.47 according to a newstudy from Avalere Health. This figure in fact is expected to grow to 52% by 2026 from 47%.

The U.S. Chamber of Commerce commissioned the Avalere Health employer study that used publicly available data from the Bureau of Labor Statistics and the Congressional Budget Office to estimate the return on investment employer-sponsored health insurance provides employers with 100 or more employees. Improved employee productivity, reduced direct medical costs, and tax benefits were the primary aspects that generated benefits for employer-sponsored health plans. Employers who offered employer-sponsored health coverage and wellness programs had healthier employees and spent less on direct medical costs, Avalare found.

The Numbers

Employee productivity reflects the reductions in absenteeism and lost productivity after receiving employer-sponsored coverage. These productivity increases contributed an estimated $275.6 billion in employer benefits in 2022, or 53.3% of all benefits. By 2026, this is expected to rise to $346.6 billion or 55.9 percent of total ROI.

ROI of some of these key components includes $275.6 billion from improved productivity in 2022 and $346.6 billion in 2026, $101 billion from a reduction in direct medical costs in 2022 and $108 billion in 2026, and $119.2 billion or a 23% ROI from tax benefits in 2022 and $139.7 billion in 2026.

Employer-Sponsored Insurance(ESI) offerings can positively influence prospective employees’ decisions to join firms, reducing employer recruitment and vacancy costs. The study’s model assumes that 9% of individuals decide to accept a certain position based on ESI. The analysis estimates that firms with 100 or more employees derived $141M in employer benefits in 2022, growing to $167M in 2026.

Similarly, ESI positively affects the retention of employees. Avalere’s analysis estimates $20.3B in employer benefits from improved retention in 2022 and $24.3B in 2026.

Conclusion

The study finds that industries where firms generally made greater investments in ESI tended to result in larger ROI. Also, since costs associated with turnover and recruitment are positively associated with wages, Avalere estimates higher ROI in higher-wage industries. On the flip side of that same coin, lower ROI was associated with industries that typically have a lower investment in ESI and wellness programs, lower wages, and lower employee participation in ESI and wellness programs.

The full report including the methodology can be found here.

For more information on how Employer-Sponsored Insurance and a PEO can make difference for your small business please contact us at info@360peo.com or 855-667-4621.

A little-known requirement but most important under Affordable Care Act (ACA) is for Health Insurers must waive their minimum employer-contribution and employee-participation rules once a year. ACA requires a one-month Special Open Enrollment Window for January 1st coverage.

The special open enrollment period occurs November 15th through December 15th of each year, allowing eligible small group employers to enroll for coverage effective January 1st of the following year.

Background

The ACA has a section in it called the “guaranteed issuance of coverage in the individual and group market.” It stipulates that “each health insurer that offers health insurance coverage in the individual or group market in the state must accept every employer and individual in the state that applies for such coverage.” The section also states that this guaranteed issuance of coverage can only be offered during (special) open enrollment periods, and that plans can only be offered to applicants that live in, work in, or reside in the plans’ service area(s).

Participation and Contribution Requirements

In many states (including California and Nevada), carriers can decline to issue group health coverage if fewer than 70% of employees elect to enroll in coverage. Some carriers may have even tighter participation requirements.

Generally speaking, employees with other coverage (Medicare, other group coverage, individual coverage through the Exchange, etc.) are removed from the participation requirement calculation – though it varies by insurance carrier.

Furthermore, employer contribution rules require employers to contribute a certain percentage of premium costs for all employees in order to attain group health coverage. Some businesses struggle to meet these contribution requirements for a variety of financial reasons.

Problem Solved: Special Open Enrollment Period

Many employers want to offer coverage to their employees, but are denied because they struggle to meet participation and/or contribution requirements. Employers cannot force employees to enroll in coverage unless the employer pays for 100% of the employees’ premiums, which many employers cannot afford. Even with moderate to generous employer contributions, many employers still find young and lower-income employees waiving coverage. This was even more evident in 2019 with the ACA’s federal Individual Mandate non-compliance penalty reduced to $0.00.

The U.S. Department of Health & Human Services provides final guidance on this in regulation 147.104(b)(1): “In the case of health insurance coverage offered in the small group market, a health insurance issuer may limit the availability of coverage to an annual enrollment period that begins November 15 and extends through December 15 of each year in the case of a plan sponsor that is unable to comply with a material plan provision relating to employer contribution or group participation rules.”

If your employer groups are struggling with participation and/or contribution, the Special Open Enrollment Window is the time to enroll them in coverage.

A little-known requirement but most important under Affordable Care Act (ACA) is for Health Insurers must waive their minimum employer-contribution and employee-participation rules once a year. ACA requires a one-month Special Open Enrollment Window for January 1st coverage.

The special open enrollment period occurs November 15th through December 15th of each year, allowing eligible small group employers to enroll for coverage effective January 1st of the following year.

Background

The ACA has a section in it called the “guaranteed issuance of coverage in the individual and group market.” It stipulates that “each health insurer that offers health insurance coverage in the individual or group market in the state must accept every employer and individual in the state that applies for such coverage.” The section also states that this guaranteed issuance of coverage can only be offered during (special) open enrollment periods, and that plans can only be offered to applicants that live in, work in, or reside in the plans’ service area(s).

Participation and Contribution Requirements

In many states (including California and Nevada), carriers can decline to issue group health coverage if fewer than 70% of employees elect to enroll in coverage. Some carriers may have even tighter participation requirements.

Generally speaking, employees with other coverage (Medicare, other group coverage, individual coverage through the Exchange, etc.) are removed from the participation requirement calculation – though it varies by insurance carrier.

Furthermore, employer contribution rules require employers to contribute a certain percentage of premium costs for all employees in order to attain group health coverage. Some businesses struggle to meet these contribution requirements for a variety of financial reasons.

Problem Solved: Special Open Enrollment Period

Many employers want to offer coverage to their employees, but are denied because they struggle to meet participation and/or contribution requirements. Employers cannot force employees to enroll in coverage unless the employer pays for 100% of the employees’ premiums, which many employers cannot afford. Even with moderate to generous employer contributions, many employers still find young and lower-income employees waiving coverage. This was even more evident in 2019 with the ACA’s federal Individual Mandate non-compliance penalty reduced to $0.00.

The U.S. Department of Health & Human Services provides final guidance on this in regulation 147.104(b)(1): “In the case of health insurance coverage offered in the small group market, a health insurance issuer may limit the availability of coverage to an annual enrollment period that begins November 15 and extends through December 15 of each year in the case of a plan sponsor that is unable to comply with a material plan provision relating to employer contribution or group participation rules.”

If your employer groups are struggling with participation and/or contribution, the Special Open Enrollment Window is the time to enroll them in coverage.

As COVID-19 unfolds, the importance of a PEO for a Small Business becomes evident. How can you protect your employees while also managing costs? Here are examples of how our PEO clients have benefited.

1. Rapid Law Changes

With recent CARES Act and FFCRA(Families First Coronavirus Response Act) to help struggling businesses, overwhelming info and regulations have mounted for the small business owner. Who is eligible for benefits? Tax credits? Furloughs and COBRA? Is their business Essential? Paid Sick Leave eligibility and additional tax credit entitlement?

PEOs provide a full team of experts who anxiously awaited the legislation, final rulings, and updates on all the Acts. They spend countless hours diving into legal jargon to answer business owners’ questions. Then, PEOs work alongside organizations to implement processes that assist in keeping the business compliant. They also help employees through the difficult time, with the livelihood of the business always in mind.

2. PEOs help with Paycheck Protection Program (PPP) loans through the CARES Act

Lenders are asking for historical payroll data and tax reports quickly produced by a PEO’s HRIS System. Many small businesses without HR help find these systems financially draining. Example: Needed 940/941 reporting is issued which can be sent to SBA Lender. Also, several leading PEO’s have supported clients with NYS Shared Loans Program.

Working with clients to understand options.

3. Payroll Burden

Payroll administration is now a nightmare. Tracking the FFCRA emergency sick leave and expanded FMLA separately from regular sick and FMLA leave has thrown a wrench in many payroll processors’ systems. Add on any furloughed or terminated employee reporting and tracking, and now the job has doubled.

Instead, our PEO Clientsy are spending their time on mission-critical work that could make or break the business. Additionally, their payroll is processed by professionals who have the time and expertise to know the nuances of payroll and payroll tax laws with back up teams of professionals in place.

4. Staffing Needs – On-Boarding and Terminations

A minimum 75% of PPP loans must be spent on staffing costs. Companies that had previously furloughed or terminated employees find they need to hire employees back. This comes with additional paperwork and many employee questions, such as whether benefits wait periods start over.

Conversely, when businesses do need to furlough or terminate employees, the PEO is a great guide for compliance. The layoff process, COBRA, paperwork including givernement reporting are supported.

5. HR Excellence

Partnering with a PEO is much like gaining access to a full-service HR division, with a team of HR experts who are up-to-date with new and changing employment laws and able to identify ways to streamline your HR.

According to a report conducted by the National Association of Professional Employer Organizations (NAPEO), PEOs provide access to more HR services at a cost that is close to $450 lower per employee, compared to companies that manage their HR services in-house.

Studies show that businesses in a PEO arrangement grow 7-9 percent faster, have 10-14 percent lower turnover, and are 50 percent less likely to go out of business.

6. Affordable and Better Benefits

By joining a large group risk-pool a a PEO can help employers gain access to high quality employee benefits, such as health insurance options with stable and affordable rates. Due to costs, small businesses often find high-quality employee benefits out of reach. The savings on health insurance alone can pay for the PEO itself.

If you’re interested in hearing more about the advantages of partnering with a PEO, we’d love to talk to you. Fill out the form below or email info@medicalsolutionscorp.com for a FREE Consultation Today!

The information provided on this website is intended for informational purposes only. Millennium Medical Solutions Corp. does not offer legal or medical guidance. Those with legal or medical questions should seek appropriate assistance from a licensed professional. Stay up to date by signing up for Newsletter and Coronavirus Dashboard below.