Yesterday, NYS 2018 Health Insurance Rate Filing were released. The total weighted average increases were 11.5% small groups and 16.6% individual market. This early filing request deadline request requirement is not an Obamacare requirement. As per NY State Law carriers are required to send out notices of rate increase filings to groups and subscribers.

These are simply requests and the state’s Department of Financial Services has authority to modify the final rates. But they are the first indication of what New Yorkers can expect when shopping for health insurance on the individual marketplace at the end of this year. The news comes as insurance companies across the country brace consumers for another year of large rate hikes, owing in part to the composition of the individual market, and in part to the uncertainty over the future of the law under the Trump administration.

Background:

By comparison last year NYS 2017 Rate Request early filings were higher at 12.3% small group and 19.3% for individuals. The final filing rates were lower NYS 2017 Final Rates were 8.3% small group and 16.6% for individuals. The NYS 2016 Rates final rates were 9.8% small group and 7.1% for individuals. Using these past figures one projects a 2018 Final Rates of 7% small groups and 14% individuals.

With only 3 months of mature claims in 2017 to work of off Insurance Actuaries have little experience to predict accurate projections. Simply put the less credible information presented to actuarial the higher the uncertainly and higher than expected rate increase. The national rate trend, however, has been much higher than in past years due to higher health care costs and the loss of Federal reinsurance fund known as risk reinsurance corridor.

Individuals:

Individual rates are expected to be higher than small group. The national rate trend, however, has been much higher than in past years due to higher health care costs Like other states throughout the nation, the 2018 rate of increase for individuals in New York is higher than in past years partly due to the termination of the federal reinsurance program. The lost of the program’s aka federal risk reinsurance corridor funds accounts for 5.5 percent of the rate increase.

This is one of the reasons why the individual market is significantly more costly to operate than small group as per recent Aetna and United Healthcare pull out of most State Individual Exchanges. Another local example was last year’s Oscar Health Insurance which had lost $105 million and is asking for up to 30% rate increase. The 3 year old company said the increase was necessary because medical costs have risen, government programs that helped cover costs are ending, and its members needed more care than expected. For 2018, with successful pivotal changes Oscar is asking below average 11% individual increase and a decrease of 3.2% small group next year.

Small Groups:

While small group rates are better risk and naturally lower rates. There is some rate shock with notably Careconnect. CareConnect, the financially struggling health insurance arm of Northwell Health, has asked the Cuomo administration to allow an average 30 percent premium hike on the individual market in 2018. The company, which lost $157 million in 2016, is asking for small group increases that range between 9 and 24 percent.

THE THREE R – RISK CORRIDOR, RISK ADJUSTMENT & REINSURANCE designed to mitigate the adverse selection and risk selection. The problem, according to many insurance companies, is that the formula is flawed, and CareConnect executives have consistently complained that they are at an unfair disadvantage. The Cuomo administration has taken steps to ameliorate some of those problems, giving the DFS the authority to essentially overrule the federal numbers. In its first-quarter financial report, executives made clear that the risk adjustment penalty was a threat to its business.

Instead, the correct approach for a small business in keeping with simplicity is a Private Exchange. This is a true defined contribution empowering employees with choice of leading insurers offering paperless technologies integrating HRIS/Benefits/Payroll. Both employee and employers still gain tax advantage benefits under the business. Also, the benefits, rates and network size are superior under a group plan as THE RISK OUTLINED ABOVE ARE HIGHER FOR INDIVIDUAL MARKETS THAN SMALL GROUP PLANS.

You may view the NYS 2018 Rate Requests DFS press release, which includes a recap of the increases requested and approved by clicking here.

For a custom analysis comparing PEO with YOUR upcoming 2017-2018 renewal please contact our team at 36PEO (855)667-4621. We work in coordination with Navigators to assist with Medicaid, CHIP Child Health Plus, Family Health Plus and Medicare Dual Eligibles. We have Spanish, Russian, and Hebrew speakers available. Quotes can also be viewed onour site.

Summary of 2018 Requested Rate Actions

INDIVIDUAL MARKET

Company Name

2018 Requested Rate Action

Affinity

23.5%

Care Connect

29.7%

CDPHP

15.2%

Crystal Run Health Plan, LLC

8.7%

Emblem (HIP)

24.9%

Empire **

N/A

Excellus

4.4%

Fidelis

8.5%

Healthfirst Insurance Company, Inc.

13.0%

Healthfirst PHSP, Inc.

22.1%

HealthNow New York

47.3%

IHBC

25.9%

MetroPlus

7.9%

MVP Health Plan

13.5%

Oscar

11.1%

UnitedHealthcare of New York Inc

38.5%

Total Weighted Average

16.6%

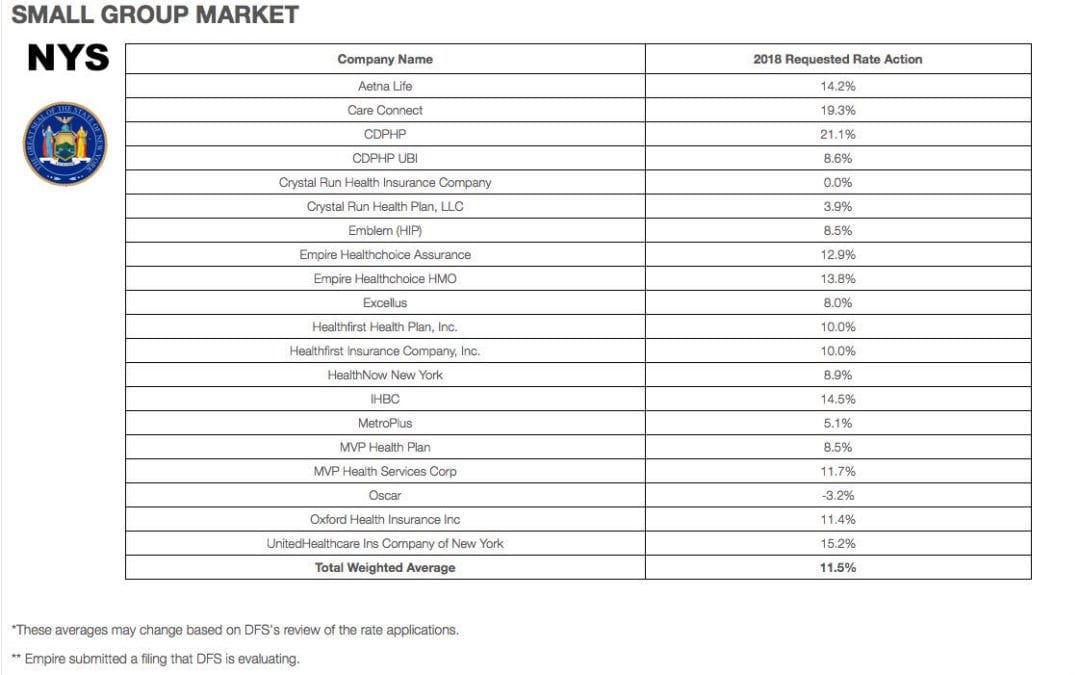

SMALL GROUP MARKET

Company Name

2018 Requested Rate Action

Aetna Life

14.2%

Care Connect

19.3%

CDPHP

21.1%

CDPHP UBI

8.6%

Crystal Run Health Insurance Company

0.0%

Crystal Run Health Plan, LLC

3.9%

Emblem (HIP)

8.5%

Empire Healthchoice Assurance

12.9%

Empire Healthchoice HMO

13.8%

Excellus

8.0%

Healthfirst Health Plan, Inc.

10.0%

Healthfirst Insurance Company, Inc.

10.0%

HealthNow New York

8.9%

IHBC

14.5%

MetroPlus

5.1%

MVP Health Plan

8.5%

MVP Health Services Corp

11.7%

Oscar

-3.2%

Oxford Health Insurance Inc

11.4%

UnitedHealthcare Ins Company of New York

15.2%

Total Weighted Average

11.5%

*These averages may change based on DFS’s review of the rate applications.

** Empire submitted a filing that DFS is evaluating.

Everything you need to know ahead of tomorrow’s 2017 Individual Open Enrollment. This Open Enrollment marks the 4th anniversary of Obamacare a.ka. The Affordable Care Act. As a helpful resource, the new NY and NJ rates with important deadlines are listed below. 33 States such as NJ use the healthcare.gov website or at https://medicalsolutionscorp.demo.hcinternal.net/individual/individual/homePage. States such as NY and CT use their own Marketplace – NYS of Health and AccessHealth CT. Importantly, individuals not expecting a subsidy may also apply Off-Exchange which in many case has more options and Insurers.

2017 NY Individual Health Plans

These rates are for New York City unless otherwise indicated, and for a single person. For a family premium, multiply by 2.85, Husband/Wife multiply by 2.0 and Parent/Children multiply by 1.70. The non single deductibles are out of pocket maximums are doubled. These are for standard plans, which two-thirds of customers enrolled in during 2016.

While deductibles for platinum, gold and silver plans have stayed the same, many bronze plan deductibles have increased 33 percent. That means consumers who purchase a bronze plan — presumably for its lower monthly premium — are paying more out of pocket for their medical costs before their insurance company kicks in a dime. A family of four that purchased a bronze plan will have an $8,000 deductible in 2017, up from $6,000 in 2015. For someone young and relatively healthy, that might be OK, but that person is vulnerable to a very large bill if he or she needs expensive medical care. It’s the platinum plans where New York State really shows itself to be a national outlier. Roughly 18 percent of New Yorkers chose a platinum plan in 2016, compared to 2 percent across the nation, according to the Kaiser Family Foundation.

NJ Dept of Banking and Insurance posted the 2017 NJ individual health plans Monday. Only two carriers will offer plans on the state’s Obamacare marketplace next year: Horizon Blue Cross Blue Shield of New Jersey and AmeriHealth.

Additional insurers are participating off-exchange or outside the Marketplace. Examples: Aetna, CIGNA and Oxford. There are additional 20 plan options available off exchange. A notable new entrant, Health Republic of NJ, will no longer be available for 2017. See – Health Republic NJ Shutting Down.

November 1, 2016: Open Enrollment starts — first day you can enroll in a 2017 insurance plan through the Health Insurance Marketplace. Coverage can start as soon as January 1, 2016.

December 15, 2016: Last day to enroll in or change plans for new coverage to start January 1, 2017.

January 1, 2017: 2017 coverage starts for those who enroll or change plans by December 15.

January 15, 2017: Last day to enroll in or change plans for new coverage to start February 1, 2017

January 31, 2017: 2016 Open Enrollment ends. Enrollments or changes between January 16 and January 31 take effect March 1, 2017.

If you don’t enroll in a 2016 health insurance plan by January 31, 2017, you can’t enroll in a health insurance plan for 2016 unless you qualify for a Marketplace Special Enrollment Period.

Penalty: The uninsured penalty rises to $695 or 2.5% of your income, whichever is higher.

Coverage start dates

If you enroll before the 15th of any month, your coverage starts the first day of the next month. If you enroll after the 15th of the month, you’ll have to wait until the month after that for your coverage to start. So, for example, if you enroll on January 16, your coverage would start on March 1.

Enroll using our online comparison shopping tool for both on and off-Exchange Marketplace to be released next week. Email us or Contact us at (855)667-4621.

“The deadline for individuals and families to enroll in a qualified health plan through NY State of Health is February 15, 2015. However, the Marketplace will provide additional assistance to those individuals who have taken steps to apply for coverage but have been unable to complete the enrollment process before the deadline. All applications and enrollments in health plans must be completed by the end of the day on February 28, 2015. Those who complete their enrollment after February 15, 2015 but on or before February 28, 2015 will have coverage starting on April 1, 2015.”

2/12/15

Last days for 2015 Individual Open Enrollment is ending this week. This deadline applies to both On and Off Exchange!

If you’re wondering about the penalty for not having insurance: yes, there is one, and no, you can’t really get out of paying for it. You’ll pay the penalty when you file your taxes for 2015. Even if you get coverage midway through the year, you’ll still need to pay a penalty for the months you weren’t insured. So get covered!

Think you might be eligible for a subsidy or aren’t sure?

You can check here at the New York State of Health Marketplace calculator. If you are eligible or think you might be eligible, you can contact the marketplace directly to purchase a plan or ask questions about financial assistance.

Please remember that during open enrollment you are permitted to switch carriers. Choose wisely because after February 15, one cannot switch plans until open enrollment 2015, unless you have a “qualifying event,” such as marriage, divorce, birth or adoption.

Individual Online Enrollment Resources for On and Off Exchange:

For NYS – To view Oscar’s plans, rates and simple online enrollment application, click here.

For more information on enrollment please contact our team at Millennium Medical Solutions Corp (855)667-4621. We have Spanish, Russian, and Hebrew speakers available.

Open enrollment for the 2015 New York individual market season is right around the corner. Below are answers to commonly asked questions pertaining to individual market coverage for residents of New York State:

Q: What is the New York State of Health (NYSOH) exchange website? A:NYSOH provides NYS residents living between 139%-400% of the Federal Poverty Level, access to lower cost health insurance by supplying them with tax credit premium subsidies. Additional Cost Sharing subsidies are available to those living between 139%-250% of the FPL. All subsidy programs are subject to eligibility requirements. Additionally, NYSOH is where individuals can enroll in Medicaid (for those living below 139% of the FPL).

Q: Is the NYSOH government health insurance? Is that what “Obamacare” means? A: No. Individual health insurance is a relationship between a consumer, and a private health insurance company. NYOSH slips in between this relationship by forwarding tax credit money to the carrier on behalf of the subsidy-eligible consumer, and then the carrier bills the consumer for the difference in premium owed. “Obamacare” is simply the nickname of the new health insurance law, which (in part) assists individuals in obtaining health insurance.

Q: Do I have to have health insurance? A: Yes. As part of the individual mandate, all US citizens must enroll in Affordable Care Act-compliant health insurance…be it through your employer, the individual market, Medicare, or Medicaid. Citizens not enrolled in coverage will be fined by the IRS (less those who qualify for exemptions).

Q: What is the fine for not having health insurance? A: In 2015, the fine is 2% of household income per uninsured month. In 2016, this increases to 2.5% of household income per uninsured month.

Q: Do I have to enroll in individual coverage through NYSOH? A: No. Only people in need of tax credit subsidy assistance must enroll through the NYSOH exchange website.

Q: What if I don’t earn enough income to qualify for subsidy assistance for on-exchange health plans? A: People in NY living below 139% of the FPL will be eligible for Medicaid. Medicaid enrollments are conducted on the NYSOH website.

Q: If I am over the subsidy income limit threshold, how do I apply for coverage outside of the NYSOH website? A: You can enroll directly with a carrier, or, by contacting a licensed insurance broker for assistance. Off-exchange carrier applications are extremely simplified, requiring only a 1-2 page paper/PDF application to be completed in most cases, and with no government intervention.

Q: Can brokers assist me with my individual coverage written through the NYSOH website as well? A: Yes. Licensed brokers, who are also certified to write health plans on the exchange, can be found in the Broker directory on the NYSOH website. You can search using a specific broker’s first and last name, by selecting a specific Agency from the drop down list, or you can enter your ZIP Code to find one in your region.

Q: Do brokers charge fees for helping me secure an individual health plan? A: Brokers are not allowed to charge fees for assisting individuals with writing their health insurance.

Q: How do brokers get paid? A: Every time you pay your health insurance bill, a portion of your payment is allocated towards compensating a broker (just like with your auto or homeowners insurance). Most carriers pay broker commissions on the back end, which is completely transparent to the consumer. If no broker is utilized by the consumer, the carrier retains the commission. This means that whether you use a broker or not, you’ll be paying for one anyway.

Q: Don’t Navigators already provide these broker services? A: No. Sometimes referred to as “in person assistors” or “experts” by the NYSOH, Navigators are not licensed to write health insurance. They are trained employees or contracted agencies of the NYS government (funded by Federal grant money) to help individuals navigate the enrollment process on the NYSOH website only. They are not required by federal law to undergo criminal background checks, nor are they licensed by the NYS Department of Financial Services, which means they cannot make plan recommendations to health insurance consumers.

Q: Can a certified broker process my NYSOH enrollment for me? A: Yes. Brokers that are certified to write business on the NYSOH exchange website can drive the entire online enrollment process for the consumer. You just need to authorize a broker through your NYSOH account by logging in, and then clicking “Find a Navigator/Broker” towards the bottom left side of your NYSOH account home page. Once authorized, the broker you have selected will receive an email from the NYSOH that you are in need of assistance, and can now enroll you on your behalf.

Q: When can I enroll in individual health insurance? A: Like Medicare, the individual health insurance market is setup to have an open enrollment season. The individual market open enrollment window is from 11/15/14 through 2/15/15.

Q. Are there any exceptions to the open enrollment period?

A. Enrollment in Medicaid, Child Health Plus and the Small Business Marketplace continues all year.

Have a Qualifying Event?

Enroll Now using our online shopping tool where you can compare plans and prices and enroll

Find us on the Health Insurance Marketplace where you may qualify for help to pay for your health insurance. Qualifying Events for Exchange Marketplace. 76 percent of the uninsured are unaware of the looming March 31 sign-up deadline. Contact us at (855)667-4621.

Q: Can I enroll in coverage outside of the open enrollment season? A: Consumers can enroll in individual coverage outside the open enrollment season so long as a “Qualifying Life Event” exists. Examples of such events include the loss of a job, marriage, divorce, birth of a child, a change in subsidy eligibility, and others. Written proof of the QLE will be required when enrolling outside of the open enrollment season as established by the US Department of Health and Human Services.

Q: If I am subsidy eligible, and my income changes, what do I do? A: Consumers enrolled through the exchange who receive tax credits must notify the NYSOH Marketplace whenever a change of income is experienced. You can contact the marketplace call center at 855-355-5777 to update your income information.

Q: Am I limited to certain insurance companies if I am subsidy-eligible? A: No. Consumers who are subsidy-eligible may pick any plan they wish that is available on the NYSOH exchange website. However, subsidy-eligible individuals may not apply those tax credits towards health plans written outside of the NYSOH website (for example, Oxford Liberty plans, which are only available outside of the NYSOH Marketplace).

Q: I have completed the income portion of my on-exchange application, and I’m now ready to pick a plan. How can I find out more specific information pertaining to the available options in the market? A: A licensed insurance broker can help you understand the available health plans in the market, and can make plan recommendations specific to your needs and financial situation.

Q: I started my current individual plan in July 2014. Do I have to renew my plan on January 1st 2015? A: Yes. All individual market plans have calendar year deductible and maximum out of pocket accumulation periods, which resets on January 1st of any given year. So for example, if you lost your job (and your health insurance) effective 12/1/14, and then you enroll for individual coverage effective 12/1/14, you must renew your individual plan the following month (for 1/1/15) at the new carrier plan structures and rates.

Q: I already have individual market based health insurance. Can I change plans during the open enrollment season? A: Yes. Existing individual health insurance policyholders may change their plan during the open enrollment season. You may also change carriers should you wish to find a better solution for your needs. Talk to your licensed insurance broker about the available plan options in the market for 2015.

Q: My employer is offering me a health plan that I am not interested in. Can I waive my employer health plan and replace it with an individual plan, and receive tax credit subsidy assistance? A: The answer to the first part of the question is yes. Employees can choose to opt out of employer-sponsored health insurance, and can replace their coverage in the individual market.

With regards to receiving tax credit subsidies in these situations, yes, an individual can receive tax credit subsidies to help pay the cost of individual health insurance. However, in addition to the employee needing to meet tax credit eligibility requirements as discussed earlier, one of two additional conditions must be met to be eligible to receive subsidy assistance: 1) The employer’s health plan does not meet the minimum actuarial value of 60%, or 2) The employee’s single rate cost (self-only coverage, no dependents) for employer-sponsored coverage exceeds 9.5% of their household adjusted gross income (defined as “unaffordable” under the health care law).

Q: I’m applying for a tax credit subsidy. How do I determine my adjusted gross income? A: Your adjusted gross income can be found on line 37 of your 1040 tax return. Subsidy applicants who have a steady income can use this figure as a guide when determining tax credit eligibility for the upcoming tax year.

Those that do not have a steady income (e.g. sole proprietors, freelancers, single-person businesses, etc.) should speak with their accountants to determine their estimated adjusted gross income for the upcoming tax year.

Q: I was determined Medicaid eligible after applying for tax credit subsidy on the NYSOH website. However, my doctors do not take Medicaid. Can I opt out of medicaid and get a subsidized individual health plan instead? A: You may choose to opt out of Medicaid if you wish. However, those who are Medicaid eligible will not qualify for tax credit subsidies for individual health plans. You can enroll in a health plan, but you must pay the full price of the plan.

Q: I was determined subsidy eligible, and I want to pick a plan to enroll in through the NYSOH website. Can I put my children on my health plan with my spouse and I? A: No. Those who are subsidy eligible must insure their dependent children through a Child Health Plus plan. CHP (or “chip”) plans are selected during the plan check out process at the end of the NYSOH application. Only the applicant and spouse will qualify for a private health plan with subsidy assistance. If you choose to opt your children out of CHP, you and your spouse will lose subsidy eligibility for your private health plan.

Q: How can I find out if my doctors take a particular health plan? A: Your licensed insurance broker can provide you with carrier-specific tools to look up providers in particular networks.

Q: How can I get a copy of the full benefit summary for a particular health plan I’m interested in? A: Your licensed insurance broker can provide you with electronic benefit summaries for most health plans upon request.

Q: How can I find a licensed broker to assist me? A: Licensed insurance brokers, and who are also certified to write on-exchange plans, can be found in the Broker directory on the NYSOH website. You can search using a specific broker’s first and last name, by selecting a specific Agency from the drop down list, or you can enter your ZIP Code to find one in your region.

For more information regarding both Exchanges – Individual Exchanges or SHOP please contact our team at Millennium Medical Solutions Corp (855)667-4621. We have Spanish, Russian, and Hebrew speakers available. Quotes can also be viewed on our site.

New Proposed Rules for Wellness ProgramsIn another step forward to ncentivize wellness new proposal can give discounts for managing good health much like good drivers with auto insurance.Newproposed rules issued under Health Care Reform address certain amendments to the nondiscrimination requirements for group health plans offering a wellness program to comply with the federal Health Insurance Portability and Accountability Act(HIPAA).Specifically, the proposed rules would increase the maximum permissible reward under a wellness program that requires an individual to satisfy a standard based on a health factor in order to obtain a reward, from 20% to 30% of the cost of coverage (and to 50% for programs designed to prevent or reduce tobacco use). The rules also include other proposed clarifications regarding the requirements for such wellness programs to avoid prohibited discrimination, including reasonable design and reasonable alternatives that must be offered for individuals to obtain the reward.Other Proposed Rules Released Under Health Care Reform Separately, new proposed rules have been issued for health insurance companies regarding the law’s requirements related to guaranteed availability of coverage and essential health benefits.

Under one set of proposed rules, issuers offering non-grandfathered health insurance coverage in the individual or group market would be required to accept every individual and employer that applies for coverage, with limited exceptions. Issuers in the individual and small group markets would be allowed to vary premiums within limits, only based on age, tobacco use, family size, and geography.

Another set of proposed rules outline issuer standards related to coverage of “essential health benefits.” Essential health benefits are a core set of items and services that must be covered by non-grandfathered plans in the individual and small group markets beginning in 2014.

While its always been known a healthy livingfor employees makes a productive employee. Large businesses have benefited from a healthy work force as they can better afford programs and have a direct rate reduction in rates.

Although employers continue to use cost shifting to control health insurance expenses, many companies are also making wellness programs part of the overall strategy to keep costs down by keeping staff members healthy.“Our entire health care system is organized around treating diseases after they occur, not preventing them before they occur. We need a paradigm shift that places prevention at the center of our health priorities.” – Lynn C. Swann, Chairman, President’s Council on Physical Fitness and Sports

The new proposed rules would apply for plan years beginning on or after January 1, 2014. An overview of the proposed rules is available on Healthcare.gov. Our Summary by Year offers updates on other requirements related to Health Care Reform.

Anti Mandatory Mail Order Victory. A little noticed NYS Healthcare Law has gone under the radar amidst fast changes in Affordable Care Act tumult. AMMO – Anti-Mandatory Mail Order passed late Dec 2011 effective for groups renewing after Jan 11, 2012. A significant signal by Governor Cuomo to stand up to the billion dollar industry no doubt.

According to trade group Pharmacists United for Truth the PBM (pharmaceutical benefits managemnt) claim that mandatory mail order lowers costs proves otherwisee. Plan sponsors are routinely charged far more than retail price in mandatory mail order plans, and their lack of transparency keeps plan sponsors to detecting the unreasonable prices.

After spending a good part of a day in early March helping a NYS client faced with mandatory mail order I learned of this change. For certain medications the insurer limits retail pharmacy coverage. While the incentivisation of 90 day supply at 2 copays was attractive this has now declined to 2.5 copay. With few exceptions such as specialty pharmaceuticals retail pharmacists are given the same advantages and evening the playing field.

The National Community Pharmacists Association’s blog post below offers a helpful FAQ. Additionally with the steady decline of the local independent pharmacist a quality of personalized care has been eroded. The price paid in patient compliance and safety has received little attention. Independent Pharmacists have been the canary in the mine for fellow small businesses competing with large copra big box chain stores. At least now NYS is finally listening.

Community pharmacists in New York scored a significant win for their patients, communities and pharmacy choice in late 2011 with the enactment of the Anti-Mandatory Mail Order or AMMO with overwhelming, bipartisan backing. What lessons might the campaign in support of the AMMO law hold for community pharmacists across the country?

To find out, NCPA recently asked one of the legislation’s staunchest supporters and advocates to share his observations on the effort to enact the AMMO law. Craig Burridge, M.S., is Executive Director of the Pharmacists Society of the State of New York (PSSNY). Mr. Burridge credits PSSNY members as most instrumental to enacting AMMO over the fierce opposition of mandatory mail order proponents, principally large pharmacy benefit managers (PBMs). He notes people including Ray Macioci, Charles Catalano, Vinny Chiffy and literally hundreds of pharmacy owners helped win a hard fought battle by gathering tens of thousands of signatures on petitions from their patients and coordinating tens of thousands of phone calls, emails and letters.

What follows is a Q&A with Mr. Burridge, in hopes that his advice would benefit patients and independent community pharmacists in other states advocating for patient choice.

NCPA: When it comes to the forced or mandated use of mail order pharmacies, many of the concerns expressed by patients and the community pharmacists who care for them are not new and have, in fact, been voiced for a number of years. What made 2011 different in New York?

Mr. Burridge: In New York, consumers by the tens of thousands signed petitions at their local pharmacy against mandatory mail order. Patients wrote dozens of letters to the editor of many regional newspapers telling about their horror stories with mail order. Finally, pharmacy owners had had enough of losing their patients to self-dealing PBMs. Tens of thousands of phone calls to the Governor’s Office and to Legislators were made by pharmacy owners, their staffs and their patients in support of passage of the no mandatory mail order bill.

NCPA: One obstacle to ensuring patient choice of pharmacy is the myth of mail order savings. This persists in some minds despite what appears to be rampant mail order waste and studies demonstrating how health plan sponsors that incent or require the use of mail order can end up paying more for drugs. Did you encounter such misperceptions and, if so, what did you do to alter or overcome them?

Mr. Burridge: We did in New York. The PBMs came at us with ads stating that costs would go up and that it was a ‘prescription drug tax’ or that it would ‘prohibit mail order.’ We responded with evidence that exposed the ‘spreads’ being used at mail for generics and the fact that the legislation requires participating pharmacies to agree to the same reimbursement and the same co-pays.

NCPA: The health care benefits of a patient’s face-to-face consultation with a community pharmacist and the preference of most patients for going to a local pharmacy are both well-established. But how did you chronicle and reinforce the economic and tax benefits of buying local when it comes to pharmacies?

Mr. Burridge: According to national data (IMS Health) for 2009, the last year we had data before introducing legislation, 22.8 percent of the national drug spend was for mail order prescriptions. Using New York’s percentage of total drug spend (11 percent), we removed hospital expenditures and Medicaid (which had less than one percent mail order) and came up with a mail order drug spend in NY in access of $5.8 billion annually. New York State has no major mail order facilities so this represents thousands of lost pharmacy jobs.

NCPA: Like PSSNY, NCPA continually stresses to its members the importance of grassroots activism, whether it is at the federal or state levels or with local employers and leaders. Did you find that your memberships became more engaged than usual in 2011 and, if so, what did you do to encourage their further involvement?

Mr. Burridge: It helped to have the PBM industry fly in colleagues from around the country and host their own Lobby Day. They told legislators that New York’s pharmacies could survive on acute medications only. This only caused yet another round of thousands of phone calls from our pharmacists, their staffs and patients. Our grass roots turned into a raging grass fire. Livelihoods were at stake and our opponents showed their hand. They wanted ALL maintenance medications going to their wholly-owned out-of-state mail order facilities. Our legislators saw that too.

NCPA: What surprised you the most about your 2011 campaign against mandatory mail order?

Mr. Burridge: I’ve been doing this too long to be surprised. We expected the worst from our opponents and they did not disappoint us.

NCPA: What were some of your opponents’ most challenging arguments and how did you address them?

Mr. Burridge: That depends if you consider outright lies as a challenge. Their ads said that it was a “Prescription Tax” or, when that flopped, they said our bill “would prohibit mail order.” These were easily swept aside and only upset legislators who felt the PBM industry was accusing them of passing a tax on prescription drugs.

NCPA: Do you have any other words of wisdom that you would like to share with concerned patients or your colleagues in community pharmacy?

Mr. Burridge: Choosing one’s pharmacy should be a basic right. If the playing field is level, it only makes sense to buy local. Watch out for PBMs calling all maintenance medications so-called ‘specialty drugs’ as a way of getting around no mandatory mail order laws. We’ll have a lot more to say on that in the near future.

These rates are for New York City unless otherwise indicated, and for a single person. For a family premium, multiply by 2.85, Husband/Wife

These rates are for New York City unless otherwise indicated, and for a single person. For a family premium, multiply by 2.85, Husband/Wife