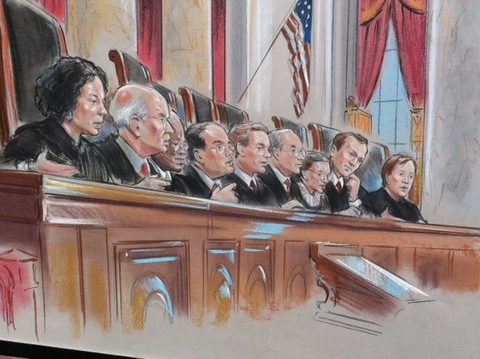

The U.S. Supreme Court ruled this morning that the Affordable Care Act may provide nationwide tax subsidies for people who purchase health insurance through an exchange. The Court considered a challenge to a provision of the ACA concerning whether subsidies were available only to those who purchased health insurance on an exchange “established by the state.” The Court, in King v. Burwell, ruled 6 to 3 in favor of upholding the eligibility for people to receive subsidies through either a state or federal health insurance exchange.

The opposite ruling would have had serious implications for the country due to the number of states relying on a federally-run exchange (37 states) and the number of customers who qualify for subsidies based on their income (about 85% of customers nationwide). The Government’s argument prevailing: defending the subsidies, the Government argued that if you look at the entire ACA and its history, it is clear that the subsidies are available to everyone who purchases insurance on an exchange, no matter who created it.

Please join us for upcoming Webinar on How to Prepare for Current and Future ACA Requirements.

Are you able to identify and address all of the ACA requirements? Have you developed a plan of action to help stay in compliance? This webinar will walk you through a three year case study and provide you with current and future solutions to help your group prepare for ACA challenges including the Cadillac Tax.

Some of the key webinar highlights include:

Will Federal subsidies stop in some states making residents unable to access subsidized Exchange coverage?

3 year case study providing a practical view

Will IRS information reporting still be required?

Could Congress step in and propose changes to the existing ACA law?

2015 – Section 125 changes including eligibility, PRAs, excepted benefits and FSA plans for higher OOP exposure

2016 – Renewal focus on HSA’s with a dollar for dollar matching contribution

2017 – Further conversation of reducing benefit costs utilizing post deductible HRA’s and consideration of Defined Contributions

Practical information you can use – a webinar you will not want to miss!

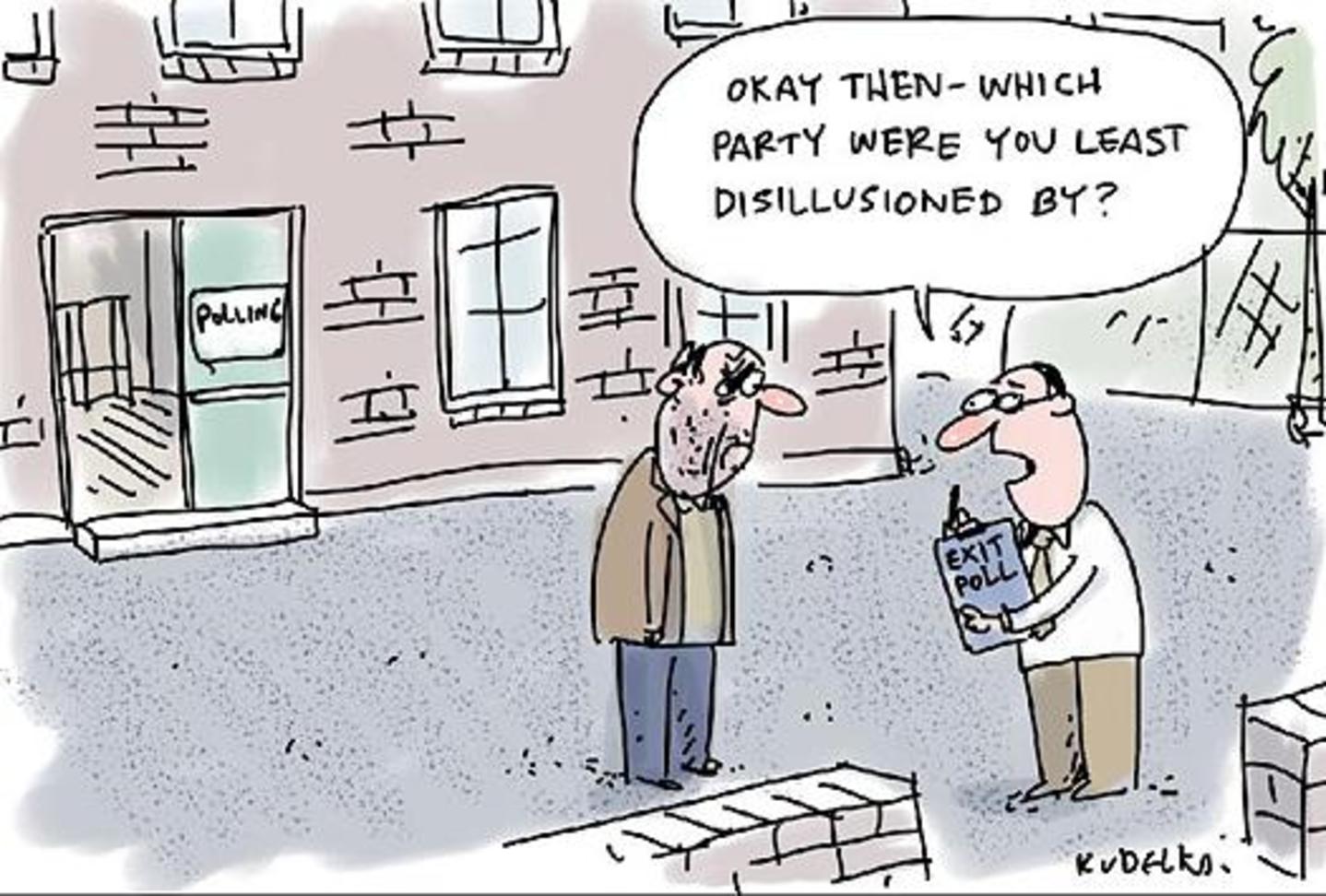

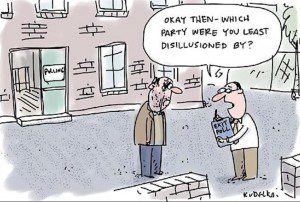

The people have spoken at least for now and they are saying they are unhappy. The storm clouds over Obmacare has ushered in GOP victories: +7 Senate + 13 House. 47% of those who cast ballots in the midterms said the 2010 health care law, which opened for enrollment a year ago, went too far. On the other hand, 26 percent said the law didn’t go far enough, CNN exit polls reported. Only 22 percent said Obamacare was just about right.

How will GOP use these powerful election gains on Obamacare?

GOP still will not have the needed 60 Senate Seats to repeal the Affordable Care Act. That said, they will now be able to pass budget rules on the legislation since the Courts ruled individual mandate penalty as a “tax”. Reinsurance funds such as Risk corridors could also be on the chopping block. Other examples would be the definition of “full-time” employee taxes on employer penalties (bipartisan support), medical devices & tanning salons etc.

According to Huffington Post article GOP-Controlled Congress Expected To Try To Repeal, Weaken ACA while Republicans have been “chomping at the bit to repeal Obamacare” since it was signed into law in 2010, even a GOP-controlled Congress is unlikely to undo the law. However, that won’t stop Republicans from forcing at least one vote on repeal. President Obama “would then swiftly veto it, but not before Democratic senators were forced to cast a vote very directly in support of Obamacare, which remains generally unpopular.” Additionally, the GOP might take aim at several provisions of the ACA, such as the individual mandate, the employer mandate, the Independent Payment Advisory Board, and the medical device tax. Some Senate Democrats would likely join them in eliminating or amending some of these measures.

A Democrat President governing with both Houses going GOP may not be so bad after all. The successful Clinton Presidency had to contend with the same balancing act. Two decades later, the key question is can both branches find a common ground and a productive working relationship?

For specific details on all available health plans in 2015, contact our team at Millennium Medical Solutions Corp (855)667-4621. We work in coordination with Navigators to assist with medicaid, CHIP Child Health Plus, Family Health Plus and Medicare Dual Eligibles. We have Spanish, Russian, and Hebrew speakers available. Quotes can also be viewed on our site.

Qualifying Events for Marketplace Special Enrollment Period

After March 31, 2014, what are considered qualifying events for individuals to buy coverage from the Exchange Marketplace outside of the annual enrollment period?

Please note that the open enrollment for Marketplace coverage ends March 31, 2014. See more at: Obamacare 2014 Deadline Nearing. The next proposed open enrollment period is November 15, 2014 – January 15, 2015. According to the Healthcare.gov site, most special enrollment periods last 60 days from the date of the qualifying life event.

Whats is a Qualifying Event?

A Special Enrollment Period (SEP) is the time outside of Open Enrollment that allows individuals and families facing special circumstances (Qualifying Life Events) to enroll in a Qualified Health Plan. Eligible individuals have 60 days to enroll after their Qualifying Life Event.

Individual or dependent loses minimum essential coverage due to: job loss; employer no longer offers coverage; divorce; death of a spouse; becoming ineligible for Medicaid or Child Health Plus; expiration of COBRA; or health plan is decertified

Marriage, birth, adoption, or placement for adoption

Gaining status as a citizen, national, or lawfully present individual

Consumer is newly eligible or ineligible for tax credits and/or cost sharing reductions

Permanent move to an area that has different health plan options

Marketplace staff or contractor enrollment error

Qualified Health Plan violated a provision of its contract

American Indians can enroll or change plans one time per month throughout the year

Other exceptional circumstances, as defined by HHS

Approximately 50% of all enrollments occur outside of Open Enrollment due to Qualifying Life Events. If you are uninsured do not miss your chance to enroll before March 31!

When do I need to complete my application to avoid a federal tax penalty?

You need to complete your application by 11:59pm on Monday, March 31, 2014 to avoid a federal tax penalty. However, if you give us your word that you tried to apply for health insurance and were not able to enroll through no fault of your own, you will have until 11:59pm on Tuesday, April 15, 2014 to complete your enrollment.

I forgot about the enrollment deadline. Can I still buy health insurance through the Marketplace this year?

No. Unless you are Medicaid eligible or you are buying insurance for a child, you must have a major life-changing event called a qualifying life event to be eligible to buy insurance through the Marketplace this year after the deadline. If you don’t have a qualifying life event, you must wait for the next open enrollment period that begins on November 15, 2014 for coverage that starts on January 1, 2015.

When is my next chance to buy insurance through the Marketplace if I am not eligible for Medicaid?

The next open enrollment period for individuals and families begins on November 15, 2014 for coverage that starts on January 1, 2015.

Are there any exceptions to the open enrollment period?

Enrollment in Medicaid, Child Health Plus and the Small Business Marketplace continues all year.

Have a Qualifying Event?

Enroll Now using our online shopping tool

where you can compare plans and prices and enroll

Find us on the Health Insurance Marketplace where you may qualify for help to pay for your health insurance. Qualifying Events for Exchange Marketplace. 76 percent of the uninsured are unaware of the looming March 31 sign-up deadline. Contact us at (855)667-4621.

A humorous take on Affordable Care Act by the site thelibertyactivist.com asks – What would it be like if buying coffee was handled just like Obamacare.

Breaking News President Announces Cancelled Policies Fix

Yesterday, the President announced that people with health care coverage that is not Affordable Care Act (ACA)-compliant may be able to keep their plans in 2014. Effectively “Grandfathering” of plans purchased after the original law has passed in 2010 There has been a great deal of concern being reported in the national media around the prospect of millions of people losing their health insurance coverage effective January 1, 2014 because of the Patient Protection and Affordable Care Act (“PPACA” aka “ObamaCare”).

We are awaiting how specifically your State’s Insurance Commissioner will react to this. Questions remain about how this new policy will work, including how insurance commissioners will react, whether insurance companies will choose to continue these policies, what the rates for the policies will be, and whether this grandfathering will extend past 2014.

To be clear, what’s being reported principally has to do with the individual health insurance market in the US which insures approximately 15 million people, or about 5% of the country’s population. Within that segment of the privately insured market, a large percentage, certainly more than half, of individual policies are not considered to be “grandfathered” under the law’s requirements for such status. As a result, to be in compliance with the law’s new mandates and coverage requirements, virtually all “non-grandfathered” policies are scheduled to be terminated January 1st, and it will be up to individuals to replace their existing coverage with new compliant policies after this date.

These recent developments have resulted in

1) President Obama issuing an apology to affected individuals on November 7th.

2) the President’s announcement earlier yesterday during a hastily called press conference at the White House that pursuant to an Executive Order, Americans may keep individual health insurance policies they were told will be canceled because these policies failed to meet requirements established by the new law.

President Obama has left it up to the states to independently determine how they will go about implementing this change which is being characterized as an “administrative fix”. However, since the insurance business is state-regulated, each state will need to determine whether or not they will implement this change, and if they choose to implement it, they will have control over defining some of the specific parameters. Insurance companies will also need to quickly make decisions on how to accommodate this new provision if the change is adapted in a state in which they operate.

In closing, if you should have any further questions or comments about the above or the attached, please let us know.We will continue to monitor this issue and all ACA implementation in an effort to keep you informed of new developments. In the meantime, please visit our https://360peo.com/about-us/blog to view past blogs and Legislative Alerts.

The New FSA Carry Over. U.S. loosens FSA rules and will allow a carry over of up to $500 to the next year. The use-it-or-lose-it rule scared off many workers, with just 25 percent of eligible workers participating in healthcare FSAs.

According to a WSJ article “Consumers Can Roll Over $500 in an FSA”, about 14 million families use FSA accounts and the new plan would be a welcome relief for them. That’s because until now any unused funds used to go the employer, so people were forced to use up the funds, especially toward the end of the year by spending on frivolous things. Moreover, many were fearful of signing up, lest they lose any unused amount.

The most recent prior change to FSA this year was a limit of $2,500 that a worker can set aside.

The health care Flexible Savings Account (FSA) can reimburse you or help you pay for eligible health care expenses not covered by your health plan. The portion of your paycheck you put into your FSA is taken out before you pay federal income taxes, Social Security taxes and most state taxes. It’s a great way to save money.

Generally, contributions you make to your FSA are not subject to federal income taxes or social security taxes. In most instances, there are no state taxes taken out either. The amount you may save depends upon:

The amount you put into your FSA

The tax percentage you would normally pay on that money (tax bracket)

Let’s say you want $2,000 taken out of your paycheck this year to put into your FSA. The money you direct to your FSA is taken out of your check before taxes are taken out. That reduces your taxable income by $2,000.

Let’s say you normally pay 30 percent in federal, social security and state taxes on your income. In this example, you would enjoy a tax savings of 30 percent of the $2,000. In other words, you could get a $600 tax savings on the $2,000 you directed to your FSA.

This example should not be taken as tax advice. See a tax advisor to seek the best advice for your situation. To see how much you may save, check out Aetna’s FSA Savings Calculator.

Is your FSA compliant? Which pre-tax qualified HSA, FSA, HRA spending card is right is right for you ? Please contact our team at Millennium Medical Solutions Corp (855)667-4621 for immediate answers.. Stay tuned for updates as more information gets released. Sign up for latest news updates.