Obamacare Simplified Using Youtoon by Kaiser is just what the Doctor ordered. With less than 60 days to go to the October 1, 2013 Health Exchanges Open Enrollment Period what better way to ease the confusion than a 7 minute cartoon?

CMS maintains the HealthCare.gov website, and this is where individuals can find more information on health insurance exchanges, the enrollment for which begins on October 1, 2013. Depending on which state individuals reside in, one may be able to enroll in an exchange plan, or may be directed to their state’s own exchange enrollment site. Employers can also use this site to learn about the Small Business Health Options Program (SHOP) which can help them provide coverage for employees.

Several resources have been made available to help people weed through the information and to make you aware of what requirements and deadlines apply to you. The Kaiser Family Foundation (KFF) brought some levity to the topic by creating an animated video explaining the upcoming changes in health coverage under the ACA. Narrated by Charlie Gibson, “The YouToons Get Ready for Obamacare,” explains what is and isn’t changing under the law and is posted on the KFF site, along with other resources on the topic. KFF President, Drew Altman, was quoted as saying, ’[t]his cartoon is meant to demystify a complex law and explain what it means for you, whether you support or oppose Obamacare.”

For a comparison and additional questions on which Exchange – Individual or SHOP Exchanges is right for you please contact our team at Millennium Medical Solutions Corp. Stay tuned for updates as more information gets released. We’re inside of 45 days until exchanges open, and information will be coming quickly in the next few months. Sign up for latest news updates.

Governor Cuomo announced yesterday that New York’s Health Benefits Exchange have been approved . Additionally, the New York Times yesterday published an article highlighting that the rates in the individual market that will be offered in 2014 are at least 50 percent lower than they are now. The article link and Governor’s office press release are included below.

5 things we now know about the NYS Exchanges:

Importantly, Insurers must still confirm that they will be in either the individual exchange and/ or shop exchange

The rates approved yesterday are subject to final certification of the insurers’ participation in the exchange.

Many of the networks used on the Exchange appear to be smaller than the group rated.

Some new insurers have eneter the marketplace such as OSCAR and Freelancers. While a few such as EmblemHealth have taken a wait and see approach.

Additionally, NYS individual market rate will drop significantly in 2014 but they have been historically always the highest. An individual/Direct Pay HMO is approximately $1,000-$1,200/month. They are still approximately 18% highest.

The Department of Financial Services (DFS) has approved New York’s Health Health Insurance Exchange rates for 17 insurers seeking to offer coverage including eight new entrants into the market that do not currently offer commercial health insurance plans. Please click the following links for the Governor’s Press Release and the Individual and Small Group rates.

The following companies had health insurance plan rates for the health benefits exchange approved today by DFS. The rates approved today are subject to final certification of the insurers’ participation in the exchange.

Aetna

Affinity Health Plan, Inc.

The cheapest you’ll pay for individual health insurance in NY

American Progressive Life & Health Insurance Company of New York

Capital District Physicians Health Plan, Inc.

Health Insurance Plan of Greater New York

Empire BlueCross BlueShield

Excellus

Fidelis Care

Freelancers Co-Op

Healthfirst New York

HealthNow New York, Inc.

Independent Health

MetroPlus Health Plan

MVP Health Plan, Inc.

North Shore LIJ

Oscar Health Insurance Co.

United Healthcare

If you have additional questions regarding how SHOP Exchanges and Individual Exchanges can benefit you please contact our team at Millennium Medical Solutions Corp. Stay tuned for updates as more information gets released. We’re inside of 75 days until exchanges open, and information will be coming quickly in the next few months. Sign up for latest news updates.

With only 6 month away from full implementation of 2014 Patient Protection Affordability Care Act (PPACA) employers are understandably uncertain. Below are Health Care reform – five things employers can do now to prepare and take action.

UPDATE JULY 2nd: Since blog posting the President Administration has delayed 1 year Employed Shared Responsibility Mandate i.e. Pay or Play to Jan 2015.

1. Employee Communications

Employers must notify employees of the online insurance marketplace known as a Healthcare Exchange. Recently released federal guidelines require employers to notify their workers of eligibility requirements for their state exchange starting Oct. 1, 2013 Open Enrollments for Jan 2014 effective date. To the relief of many, the U.S. Labor Department also provided model notices that employers can give to their workers, which eliminates the need to develop their own notifications.

Additionally, Employers sponsoring a health plan must give employees a Summary of Benefits and Coverage (SBC). The purpose of the Summary of Benefits and Coverage, or SBC, is to present benefits and coverage information in clear language and in a consistent format. Inspired by the Nutrition Facts Label on packaged food, theSBC (pdf) includes two medical scenarios: having a baby and managing Type II diabetes. It estimates how much a patient would pay for medical care in each scenario with specific insurance plans.

It’s the employer’s responsibility to distribute the SBCs to employees.

This requirement applies to health plan renewals after Sept. 23, 2012.

Department of Labor will NOT impose penalties for non-compliance with the SBC notice during the first year as long as employers show a “good faith” effort to comply. Read the FAQ on SBC and ACA pdf here.

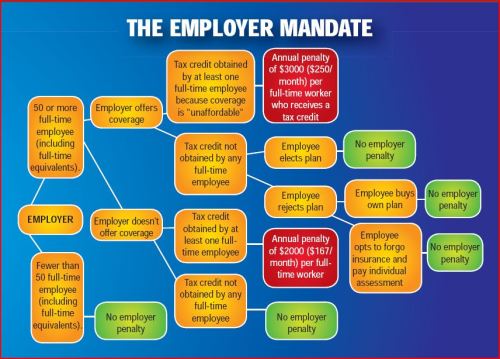

2. Determining which Employers must offer health care.

Because employers with 50 full-time equivalents face penalties for not providing affordable, minimum value insurance an employer should know whether it is subject to these requirements or not. Common law employees of the employer and any commonly controlled company must be counted. Employers with temporary or leased employees will want to discuss with their advisors whether these employees will be considered “common law employees” for purposes of determining how many FTEs an employer has. Employers with employees who are paid based on unique payment models (stipends, work product, etc) will want to discuss how to calculate these employee hours with their benefits advisors.

Employers with 50 or more employees will incur penalties of up to $2,000 per employee if they cancel their existing health care program (which up until 2014 would be considered an optional benefit to provide). They will also incur penalties if their plan is too costly, and they do not meet the affordability standards.

Employers with less than 50 employees will not incur penalties if they cancel their health care plan, and that decision will need to be made on a business by business basis. They can also choose to offer partial coverage and contribute up to the minimum 50% of single coverage not to exceed 9.5% employee

The good news is Employers can subtract 30 FT employees. This portion is known as the Employer “play or pay” option. Specific case example and details are found at Pay or Play Employer Guide.

To encourage businesses to offer health benefits to their employees, the federal government is offering tax credits to small businesses. These credits are available to an estimated 4 million small businesses, including nonprofits.The IRS has set up a web page with information: Small Business Health Care Tax Credit for Small Employers. The maximum “credit” (which offsets taxes dollar for dollar and is better than a “deduction” which reduces taxable income) is 35 percent of the amount an employer pays towards employee health insurance.

Who’s eligible?

To qualify, small employers must:

Have fewer than the equivalent of 25 full-time workers

Pay average annual wages below $50,000

Cover at least 50% of the cost of health care coverage for their workers

Because of the high wages paid in most industries in NY/NJ/CT Tri State, few small employers that provide coverage pay such a low average wage. Note, however, that the calculation of average wages and number of employees excludes the wages of an owner and his or her family members.

medicalsolutionscorp.com help clients gather the appropriate information and do a preliminary estimate of the credit amount. This information will help you and your accountant determine whether applying for the credit makes financial sense. Find out what the new tax credit could mean for your coverage. Call us at 855-667-4621.

4. Determine affordability

Beginning Jan. 1, 2014, an employer with 50 or more employees must pay a tax penalty if they either: a) Do not provide health insurance with minimum benefits or 60 percent of healthcare expenses; b) Require employees to contribute more than 9.5 percent of an employee’s household income for the health insurance and those employees obtain a government subsidy for coverage.

Companies will be required to pay $3,000 per employee without affordable coverage. (Note: there are a number of caveats that might affect the actual penalty paid, so consult your tax advisor.)

It is crucial to Understand the difference between FT and Full Time Equivalent. To determine the FTE (Full Time Equivalent) you must count FT and PT employees. Full Time Employees are those working 30 hours+/week.* The number of full-time employees excludes those full-time seasonal employees who work for less than 120 days during the year.4 The hours worked by part-time employees (i.e., those working less than 30 hours per week) are included in the calculation of a large employer, on a monthly basis, by taking their total number of monthly hours worked divided by 120.

For example, a firm has 35 full-time employees (30+ hours). In addition, the firm has 20 part time employees who all work 24 hours per week (96 hours per month). These part-time employees’ hours would be treated as equivalent to 16 full-time employees, based on the following calculation:

20 employees x 96 hours / 120 = 1920 / 120 = 16

Thus, in this example, the firm would be considered a “large employer,” based on a total full-time equivalent count of 51—that is, 35 full-time employees plus 16 full-time equivalents based on part-time hours.

In the coming months, Millennium Medical Solutions Inc will host seminars and will share information you’ll need to know as the countdown continues to October 1st.

Error: Contact form not found.

This blog is not intended to represent legal advise and one should consult with a tax and/or legal expert.

* IRC 4980H(c)(4)

Disclaimer: This blog is not intended to represent legal advise and one should consult with a tax and/or legal expert.

In Time magazine’s March issue Bitter Pill: Why Medical Bills Are Killing Us Steven Brill gets to work on answering the ever elusive Why are Medical Costs So High? The 21,000 word article is longest article in Time Magazine history that can boiled down to simply there is no free marketplace in health care. We think everything in this country is a free market but is there a free market when one needs to got to an emergency room or a free market when one must take a cancer pill? According to Howard Dean the singular reason is to get away form the current fee for service system where providers get paid per procedure and not per patient.

Here’s an eye opener: “Insurance Companies are not really the problem they run pretty terribly. They process claims, a lot of us think they process claims and fairly consistently but they are increasingly at the mercy of hospitals which are consolidating buying a doctors practices. We should tax profits on so-called nonprofit hospitals and put that money back into the system. We should control all the prices for prescription drugs because if I have a monopoly a cancer wonder drug I can charge anything I want for them that’s obviously not a free market and it’s completely two different uses you see this article once you follow the money.”

Transcript of the video:

“This is not a free-market. You don’t get health care because you want it. You don’t wake up in the morning and gee I love to go down to the emergency room today. You enter that market and will you know nothing about the products of you being asked by no choice of those products. Hi I am Steve Brill I’ve got the cover story this week in TIME Magazine looking at the health care debate from a very different perspective. Everybody focuses on who should pay for the exorbitant cost of health care and that I decided to do was ask for more fundamental question which is why does health care cost so much.

I look behind the bills and trace the bills all the way back to who’s getting what money is making what profits and the results are really surprised one of the things I found that everybody in the healthcare industry knows about that that nobody else knows his something called the charge-master. The charge master is a internal listing each hospital of the thousands of different items that they charge and nobody could explain it to me. Indeed would be hard to explain for example why would you charge $77 for a box of gauze pads? You can buy for a dollar at the drugstore. why would you charge thousands of dollars for CAT scan it really isn’t cost you anything?

It’s emblematic if you will, of the irrationality of the higher healthcare system because no one can explain the cost no one tries to and the only people who are guaranteed surefire to pay to be asked to pay the charge-master prices are the poorest people who don’t have health insurance.

Real profit makers are way hospitals markup very expensive drugs that you get. If you have cancer to have pneumonia but they’re making thousands of dollars on these drugs and drug companies in turn making still more thousands of dollars.

Obamacare does very little to solve any of these problems and just probably why you got to Congress I’m it doesn’t do anything to control the prices of prescription drugs or medical devices CAT scan. In fact if anything it will increase the profitable the players in the market by making equal insurance and therefore more people are in the marketplace with the funds from insurance companies to buy all these products.

Insurance Companies are not really the problem they run pretty terribly. They process claims, a lot of us think they process claims and fairly consistently but they are increasingly at the mercy of hospitals which are consolidating buying a doctors practices. See Provider Consolidation Info-graph– “The proliferation of hospital mergers and hospitals’ appetite for buying doctors’ practices—in part to assure a steady stream of patients to fill hospital beds—could create local monopolies that raise prices without increasing efficiency. ‘Historically,’ says Deloitte’s Mr. Keckley, ‘hospital consolidation hasn’t reduced costs.’”

We should tax profits on so-called nonprofit hospitals and put that money back into the system. We should control all the prices for prescription drugs because if I have a monopoly a cancer wonder drug I can charge anything I want for them that’s obviously not a free market and it’s completely two different uses you see this article once you follow the money.”

The ACO (Accountable Care Organization) referenced in our post NYU Beth Israel Merger and ACOs are models encouraged in Obamacare in fact as examples of Provider capitated reimbursement that Howard Dean is in favor of. An ACOI cordiantes patient care and provide the full range of health care services for patients. The health reform law provides incentives for providers who join together to form such organizations and who agree to be accountable for the quality, cost, and overall care of Medicarebeneficiaries who are enrolled in the traditional fee-for-service program who are assigned to the ACO.

The fee-for-service system has evidentially driven costs by incentivizing volumes of added procedures. The ACO model is built on par excellence hospitals such as Mayo Clinic where there is team of providers are financially incentivized for patient care coordination outcomes and high quality of care. The ACO’s payment would be tied to achieving goals that improve health care and save money. Members of the ACO would divvy up that payment. Today’s payment system, investments in providing better care are doubly penalized. If a hospital hires a nurse to follow up with patients after they are discharged in order to reduce readmissions — for example, to help patients with diabetes improve blood sugar control — it must pay for the nurse, which is typically not reimbursed by insurance companies or Medicare, and it loses revenue by preventing the readmission.

Congress included ACOs in the health care law as a way to rein in Medicare spending. That federal program pays for health care for people 65 and older and the disabled. The federal government estimates ACOs could save the Medicare program up to $940 million over four years. Medicare recently began testing this system with 32 pilot ACOs in 18 states, including one in the New York City area – Bronx Accountable Healthcare Network.

Some have pointed to ACO Model just as a pro-merger supporting argument with the FTC. These significant mergers create market dominance and therefore limit competition and drive up health care dollars. And yet Hospitals operate on thin profit margins and cannot afford to lose market share therein lies is the conundrum.

Note: At time of this article MVP and Hudson Valley Health Plans announced a merger –Hudson Health Plans joins MVP. Hudson Health Plan, the Medicaid managed care organization based in Tarrytown, will join the MVP Health Care group of companies, the two nonprofit health plans jointly announced today.

“Size and diversity of offerings are important for health plans in the new world of the health insurance marketplaces. A 55-year-old person would like to join a health plan that can continue to cover him when he turns 65. Likewise, if someone is no longer eligible for Medicaid, she might prefer to buy a commercial product from that same insurer. Together, MVP and Hudson now can cover people through all of life’s stages and changing needs.

In the coming months, Millennium Medical Solutions Inc will host seminars and will share information you’ll need to know as the countdown continues to October 1st. Please contact us for immediate information on how to implement these initiatives for your group-specific needs at info@medicalsolutionscorp.com or Call (855) 667-4621.

Fiscal Cliff Deal: Doc Cuts Spared. Happy 2013 Fiscal Cliff averted! At least for another year the dreaded 27% Medicare reimbursement have been spared. The so-called “doc fix” would boost the deficit by $31 billion. The President stood firm against any proposed Republican cuts to the Affordable Care Act.

The fear in provider cuts is grounded. According to The Lewin Report Patient Protection and Affordable Care Act (PPACA): Long Term Costs for Governments, Employers, Families and Providers “About half of program costs will be funded with reductions in payments to providers and health plans under the Medicare and Medicaid programs, which the CBO estimates will amount to $498 billion over the ten year period“. The new cost estimate has been updated to $1.4445 trillion from original estimate $938 billion over 10 years.

With millions of new uninsured patients slated to enter the system this would help providers recover reimbursement losses. Additionally, the President was firmly against any Provider cuts in 2013.

The Lewin Report predicts in fact that Provider Reimbursement will recover losses long term and in fact increase gross payments to $129.8 billion under the Act.

“..estimate that utilization of physician services will increase by about $102.7 billion under the Act. This estimate reflects Medicaid the payment levels for the portion of newly insured people covered under that program and commercial payment levels for those who become covered under private insurance. As discussed above, our key assumption is that utilization of services for newly insured people adjusts to the levels reported by insured individuals with similar age, gender, health status and income characteristics. Physicians also will be paid for services formerly provided free to uninsured people resulting in revenues of $8.4 billion. There will be an increase in reimbursement for people who shift from Medicaid to private coverage, and payment rates for Medicare primary care services will be increased for a three year period under the Act. These factors will add 18.7 billion in revenues for physicians.

While there was large Senate consensus 89-8 approval for the American Taxpayer Relief Act the health care debate is far from over. With rising health care costs, combined with the aging of the baby boomers, means the entitlement programs will remain at the heart of the tax-and-spending battles to come.

Ever Wonder why in a Metropolis of 25 Million there are maybe 5 insurers left?

New York Taxes – As published with the NYS Insurance Dept.

New York adds more insurance taxes than any other state in the country. These consist of both direct taxes and a number of “hidden” taxes amounting to a total of over $4.1 billion in taxes passed on to our customers in the form of higher premiums. These taxes include:

• NYS Premium Tax- this 1.75% tax is on all HMO and insurance contracts and is projected to raise $353 million for the State in 2010. Empire alone pays $103.9 million to the State in premium taxes (this amount includes a special surcharge for customers in the MTA service area).

• Covered Lives Assessment- this “hidden tax” is a charge on all fully and self insured “covered lives” and raises, statewide, projected to raise $1.16 billion for the State in 2010. Empire alone will pay about $296.2 million in covered lives assessments in 2010. The purpose of the Covered Lives Assessment is raise funds for a variety of state programs and for the state Budget. The Assessment is included in claims costs for purposes of calculating the MLR.

• HCRA Surcharge- this is a 9.63% surcharge on all hospital discharges projected to raise $2.33 billion in 2010. Empire alone will pay approximately $379.4 million to the State in HCRA surcharges in 2010. The purpose of the HCRA Surcharge is to raise funds for a variety of state programs and for the state Budget. The Assessment is included in claims costs for purposes of calculating the MLR. NYS Insurance Department “332” Assessment- while this assessment is legitimately intended to fund the cost of the Insurance Department’s regulatory activities there is a “hidden tax” whereby a large portion of the revenue generated by the assessment is used to fund other programs funded not directly related to insurance regulation and is projected to raise $270 million from New York’s health insurers and HMO’s in 2010. Empire will pay the state $57.9 million in 332 assessments for 2010.

Each of these taxes is increased regularly by the State and contributes significantly to annual increases in rates. The competition in the health insurance industry is already at a dangerous low level. Negotiating with insurers has become an overwhelming challenge in the large group market.