Governor Cuomo announced yesterday that New York’s Health Benefits Exchange have been approved . Additionally, the New York Times yesterday published an article highlighting that the rates in the individual market that will be offered in 2014 are at least 50 percent lower than they are now. The article link and Governor’s office press release are included below.

5 things we now know about the NYS Exchanges:

Importantly, Insurers must still confirm that they will be in either the individual exchange and/ or shop exchange

The rates approved yesterday are subject to final certification of the insurers’ participation in the exchange.

Many of the networks used on the Exchange appear to be smaller than the group rated.

Some new insurers have eneter the marketplace such as OSCAR and Freelancers. While a few such as EmblemHealth have taken a wait and see approach.

Additionally, NYS individual market rate will drop significantly in 2014 but they have been historically always the highest. An individual/Direct Pay HMO is approximately $1,000-$1,200/month. They are still approximately 18% highest.

The Department of Financial Services (DFS) has approved New York’s Health Health Insurance Exchange rates for 17 insurers seeking to offer coverage including eight new entrants into the market that do not currently offer commercial health insurance plans. Please click the following links for the Governor’s Press Release and the Individual and Small Group rates.

The following companies had health insurance plan rates for the health benefits exchange approved today by DFS. The rates approved today are subject to final certification of the insurers’ participation in the exchange.

Aetna

Affinity Health Plan, Inc.

The cheapest you’ll pay for individual health insurance in NY

American Progressive Life & Health Insurance Company of New York

Capital District Physicians Health Plan, Inc.

Health Insurance Plan of Greater New York

Empire BlueCross BlueShield

Excellus

Fidelis Care

Freelancers Co-Op

Healthfirst New York

HealthNow New York, Inc.

Independent Health

MetroPlus Health Plan

MVP Health Plan, Inc.

North Shore LIJ

Oscar Health Insurance Co.

United Healthcare

If you have additional questions regarding how SHOP Exchanges and Individual Exchanges can benefit you please contact our team at Millennium Medical Solutions Corp. Stay tuned for updates as more information gets released. We’re inside of 75 days until exchanges open, and information will be coming quickly in the next few months. Sign up for latest news updates.

Yoga initiatives improves health and reduces costs according to Aetna studies. A yoga and meditation initiative for stressed employees helped them reduce their heart rates and helped Aetna increase productivity and lower health benefit costs 7%, CEO Mark Bertolini told the Third Metric conference.

Ezekiel Emanuel of the University of Pennsylvania said while data on the efficacy of wellness programs overall is mixed, prevention efforts, including traditional wellness programs, are important for saving money and improving health.

In Huffington Post article Company Wellness Programs May Boost Bottom Lines, Aetna CEO Mark Bertolini Says when Aetna determined in 2010 that its workers with the highest levels of stress were costing the company $2,000 more each year than co-workers, the company created an initiative to promote yoga and meditation. Bertolini said at the Third Metric conference co-sponsored by The Huffington Post in New York Thursday. The results include improvements in heart rates and increased productivity.

“Stress can have a significant impact on physical and mental health, so there is a strong need for programs that help people reduce stress as part of achieving their best health,” said Aetna Chairman and CEO Mark T. Bertolini. “The results from the mind-body study provide evidence that these mind-body approaches can be an effective complement to conventional medicine and may help people improve their health, something that I have experienced personally.”

Yoga and Stretching

The study participants included 239 Aetna employees in California and Connecticut who volunteered for the two mind-body stress reduction programs. As part of the studies, 96 employees were randomly assigned to mindfulness-based classes, 90 were randomly assigned to therapeutic yoga classes and 53 were randomly assigned to the control group.

The Affordable Care Act recognizes the benefits of wellness which also includes alternative medicines such as yoga, massage therapy, acupuncture etc. Long awaited guidance on how employers can institute a wellness program using financial incentives and discounts were released recently – Final Wellness Incentive Rule Released.

Does your company offer a wellness program? For more information, you may review the final rulesin their entirety. For MMS Corp previous blogs on wellness, clickhere. we will keep you posted on future PPACA wellness program opportunities. Ask us for more info on Aetna Wellness, Yoga, and how we can help you implement a healthy program for your staff.

Error: Contact form not found.

The views expressed in this post do not necessarily reflect the official policy, position, or opinions of MMS Corp. This update is provided for informational purposes. Please consult with a licensed accountant or attorney regarding any legal and tax matters discussed herein.

With only 6 month away from full implementation of 2014 Patient Protection Affordability Care Act (PPACA) employers are understandably uncertain. Below are Health Care reform – five things employers can do now to prepare and take action.

UPDATE JULY 2nd: Since blog posting the President Administration has delayed 1 year Employed Shared Responsibility Mandate i.e. Pay or Play to Jan 2015.

1. Employee Communications

Employers must notify employees of the online insurance marketplace known as a Healthcare Exchange. Recently released federal guidelines require employers to notify their workers of eligibility requirements for their state exchange starting Oct. 1, 2013 Open Enrollments for Jan 2014 effective date. To the relief of many, the U.S. Labor Department also provided model notices that employers can give to their workers, which eliminates the need to develop their own notifications.

Additionally, Employers sponsoring a health plan must give employees a Summary of Benefits and Coverage (SBC). The purpose of the Summary of Benefits and Coverage, or SBC, is to present benefits and coverage information in clear language and in a consistent format. Inspired by the Nutrition Facts Label on packaged food, theSBC (pdf) includes two medical scenarios: having a baby and managing Type II diabetes. It estimates how much a patient would pay for medical care in each scenario with specific insurance plans.

It’s the employer’s responsibility to distribute the SBCs to employees.

This requirement applies to health plan renewals after Sept. 23, 2012.

Department of Labor will NOT impose penalties for non-compliance with the SBC notice during the first year as long as employers show a “good faith” effort to comply. Read the FAQ on SBC and ACA pdf here.

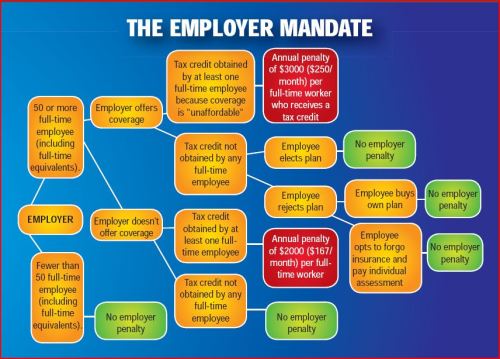

2. Determining which Employers must offer health care.

Because employers with 50 full-time equivalents face penalties for not providing affordable, minimum value insurance an employer should know whether it is subject to these requirements or not. Common law employees of the employer and any commonly controlled company must be counted. Employers with temporary or leased employees will want to discuss with their advisors whether these employees will be considered “common law employees” for purposes of determining how many FTEs an employer has. Employers with employees who are paid based on unique payment models (stipends, work product, etc) will want to discuss how to calculate these employee hours with their benefits advisors.

Employers with 50 or more employees will incur penalties of up to $2,000 per employee if they cancel their existing health care program (which up until 2014 would be considered an optional benefit to provide). They will also incur penalties if their plan is too costly, and they do not meet the affordability standards.

Employers with less than 50 employees will not incur penalties if they cancel their health care plan, and that decision will need to be made on a business by business basis. They can also choose to offer partial coverage and contribute up to the minimum 50% of single coverage not to exceed 9.5% employee

The good news is Employers can subtract 30 FT employees. This portion is known as the Employer “play or pay” option. Specific case example and details are found at Pay or Play Employer Guide.

To encourage businesses to offer health benefits to their employees, the federal government is offering tax credits to small businesses. These credits are available to an estimated 4 million small businesses, including nonprofits.The IRS has set up a web page with information: Small Business Health Care Tax Credit for Small Employers. The maximum “credit” (which offsets taxes dollar for dollar and is better than a “deduction” which reduces taxable income) is 35 percent of the amount an employer pays towards employee health insurance.

Who’s eligible?

To qualify, small employers must:

Have fewer than the equivalent of 25 full-time workers

Pay average annual wages below $50,000

Cover at least 50% of the cost of health care coverage for their workers

Because of the high wages paid in most industries in NY/NJ/CT Tri State, few small employers that provide coverage pay such a low average wage. Note, however, that the calculation of average wages and number of employees excludes the wages of an owner and his or her family members.

medicalsolutionscorp.com help clients gather the appropriate information and do a preliminary estimate of the credit amount. This information will help you and your accountant determine whether applying for the credit makes financial sense. Find out what the new tax credit could mean for your coverage. Call us at 855-667-4621.

4. Determine affordability

Beginning Jan. 1, 2014, an employer with 50 or more employees must pay a tax penalty if they either: a) Do not provide health insurance with minimum benefits or 60 percent of healthcare expenses; b) Require employees to contribute more than 9.5 percent of an employee’s household income for the health insurance and those employees obtain a government subsidy for coverage.

Companies will be required to pay $3,000 per employee without affordable coverage. (Note: there are a number of caveats that might affect the actual penalty paid, so consult your tax advisor.)

It is crucial to Understand the difference between FT and Full Time Equivalent. To determine the FTE (Full Time Equivalent) you must count FT and PT employees. Full Time Employees are those working 30 hours+/week.* The number of full-time employees excludes those full-time seasonal employees who work for less than 120 days during the year.4 The hours worked by part-time employees (i.e., those working less than 30 hours per week) are included in the calculation of a large employer, on a monthly basis, by taking their total number of monthly hours worked divided by 120.

For example, a firm has 35 full-time employees (30+ hours). In addition, the firm has 20 part time employees who all work 24 hours per week (96 hours per month). These part-time employees’ hours would be treated as equivalent to 16 full-time employees, based on the following calculation:

20 employees x 96 hours / 120 = 1920 / 120 = 16

Thus, in this example, the firm would be considered a “large employer,” based on a total full-time equivalent count of 51—that is, 35 full-time employees plus 16 full-time equivalents based on part-time hours.

In the coming months, Millennium Medical Solutions Inc will host seminars and will share information you’ll need to know as the countdown continues to October 1st.

Error: Contact form not found.

This blog is not intended to represent legal advise and one should consult with a tax and/or legal expert.

* IRC 4980H(c)(4)

Disclaimer: This blog is not intended to represent legal advise and one should consult with a tax and/or legal expert.

An interesting NYT article today “Slower Growth of Health Costs Eases U.S. Deficit” describes the good news that actual spending has been reduced by 15% or $200 Billion than projected 3 years ago. New data also show overall health care spending growth continuing at the lowest rate in decades for a fourth consecutive year.

Its any ones guess to the exact cause of this good news I will venture to say a good part of is the severe escalating out of pocket costs. With average office copays $50 and $200 for ER and many replacing these plans with high deductibles is it any wonder there is lower utilization? One might argue are poor health plans the cause for middle class leading to lower usage? To get an updated picture of todays NY Small Business rates once can get instant quote on our site and implement strategies in “How to Reduce My Health Care Costs“. In some instances people are turning to self insured Health Savings Accounts carrying deductibles as high as $5000 Individual and $10,000 Family.

In 2014 Individual Health Exchanges will offer a subsidized rate for lower income. For example, a $25,000 Individual filer would get approximate 80% subsidized rate and pay approx. $100/month. However salaries are not geo-sensitive and the average NY Middle Class Household will not see this subsidy. There are a number of questions outstanding such as the quality of the network. Also some Governors such as Christy Has Rejected Exchange is capable of running this Exchange version.

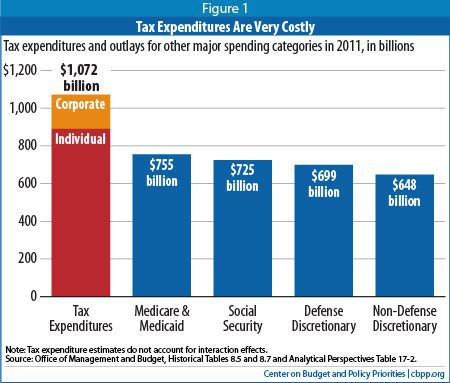

On the higher end according to CBO “tax expenditures disproportionately benefit the most well-off. As Figure 2 shows, the most affluent 20 percent of Americans receive 66 percent of all tax expenditure benefits (the richest 1 percent alone getting 24 percent of the benefits), while the middle 60 percent of households received just 31 percent of the benefits. In contrast, the middle 60 percent of households receive a proportionate share (58 percent) of the benefits of entitlement programs on the spending side of the budget (see Figure 3). The poorest fifth of households receive 32 percent of these benefits.”

But the greatest looming concern are costs. is behavior changing? Are people initiating preventive care more readily? Are they enrolled in wellness programs, managing chronic conditions, seeking Urgent Care vs. ER, using generics vs brands? Is technology playing a greater role such as mobile devices in managing care? Are modern medicine efficiencies such as avoiding testing redundancies and EMR helping?

No one argues that medical costs are a drag on the economy and are directly linked to our prosperity. “Slower cost growth would have ramifications far beyond the deficit. According to calculations by White House economists, slowing the annual growth rate of health care costs by 1.5 percentage points might increase economic output by 2 percent in 2020 and 8 percent in 2030. It might also lead to higher wages for workers and more room for productive investments in the budget.”

The hope is medical care is becoming more efficient. Whether or not the rate is subsidized it is still being paid for by someone. With this new finding it does offer hope but unless there are added incentives such a preventive medications under an Health Savings Account card covered without a deductible the concerns are Middle Class families will be reluctant to access care and we all end up paying for this.

You can self quoteon our site. Contact us at 1-855-667-4621 for more customized information.

First, and most importantly, we hope that you and your families are safe and sound.

An office status for Health Insurance Carrier post Hurricane Sandy for your information. Millennium medical Solutions Corp is up and running and the offices are open until 2:00 PM today, Friday November 2nd.

Our building has power but we are having on and off phone/internet trouble but some calls are able to come through so you can call if you have any issues.

Carrier Update

• EmblemHealth still closed • Horizon still closed • AmeriHealth still had no power as of yesterday • Oxford Update – see below

A few changes to business as usual in response to the storm:

1. The deadline for payment of October premiums has been extended. We’ve extended the deposit date for payments to November 9th. Customers should make their payments online, however, as we cannot guarantee that our overnight mailing facilities will be open and available to accept mail.

https://www.payerexpress.com/billmail/EBPP/Sites/Oxford/ 2. The deadline for November renewals has been extended from the 1st to the 6th. This includes renewals run through our IDEA portal. As we get any additionalupdates, we will reach out to you.

Change in tax treatment for over-age dependent coverage

Accounting impact of change in Medicare retiree drug subsidy tax treatment

Early retiree medical reinsurance

Medicare prescription drug “donut hole” beneficiary rebate

Break time/private room for nursing moms

[/tab_item]

[tab_item title=”2011″]

No lifetime dollar limits on essential health benefits

Restricted annual dollar limits on essentail health benefits, phased amounts until 2014

No pre-existing condition limitations for enrollees up to age 191 and no recissions

No health FSA/HRA/HSA reimbursement for non-prescribed drugs

Increased penalties for non-qualified HSA distributions

Additional standards for new or “non-grandfathered” health plans, including preventive care in network with no cost-sharing appeal and external review, provider choice and non-discrimination provisions for insured plans

Income-based Medicare Part D premiums

Pharmaceutical importers and manufacturers’ fees start

Medicare, Medicare Advantage benefit and payment reforms

Insurers subject to medical loss ratio rules

[/tab_item]

[tab_item title=”2012″]

Employers to distribute uniform summary of benefits and coverage (SBC) to participants (deadlines vary with group of recipients)

60-day advance notice of mid-year material modifications to SBC content

Form W-2 reporting for health coverage (track in 2012 for W-2 form provided in early 2013)

Coverage for additional women’s preventive care services5

[/tab_item]

[tab_item title=”2013″]

$2,500 per plan year health FSA contribution cap (plan years on or after January 1, 2013)

Comparative effectiveness group health plan fees first due

Annual dollar limits on essential health benefits cannot be lower than $2 million

Employers notify employees about exchanges

Medical device manufacturers’ fees start

Higher Medicare payroll tax on wages exceeding $200,000/individual; $250,000/couples

Change in Medicare retiree drug subsidy tax treatment takes effect

Health Insurance exchanges initial open enrollment period

[/tab_item]

[tab_item title=”2014″]

Health insurance exchanges

Individual coverage mandate

Financial assistance for exchange coverage of lower-income individuals

States Medicaid expansion (possibly only some states)

Employer shared responsibility

Dependent coverage to age 26 for any covered employee’s child

No annual dollar limits on essential health benefits

No pre-existing condition limits

No waiting period over 90 days

Wellness limit increase allowed

Health insurance industry fees

Additional standards for non-grandfathered health plans, including limits on out-of-pocket maximums,

provider nondiscrimination, and coverage of routine medical costs of clinical trial participants

Small market, non-grandfathered insured plans must cover essential health benefits with limited deductibles (initially $2,000/individual, $4,000/family), using a form of community rating

Insurers must apply guaranteed issue and renewability to non-grandfathered plans of all sizes

Auto enrollment sometime after 2014

[/tab_item]

[tab_item title=”2015″]

Temporary reinsurance fees first due in late 2014/early 2015

Additional employee-specific reporting and disclosure of 2014 coverage

[/tab_item]

[tab_item title=”2018″]

40% excise tax on “high cost” or Cadillac coverage

Today, health care costs are high, and getting higher. Who will pay your bills if you have a serious accident or a major illness? You buy health insurance for the same reason you buy other kinds of insurance, to protect yourself financially. With health insurance, you protect yourself and your family in case you need medical care that could be very expensive. You can’t predict what your medical bills will be. In a good year, your costs may be low. But if you become ill, your bills could be very high. If you have insurance, many of your costs are covered by a third-party payer, not by you. A third-party payer can be an insurance company or, in some cases, it can be your employer.

Sign up for latest news updates. Please contact us for immediate information on how to implement these initiatives for your group-specific needs at info@medicalsolutionscorp.com or Call (855) 667-4621.

Group Health Insurance Quote Request

Please complete the following information and Census Form if you would like to obtain a group health insurance quote. Please understand this is not an application for insurance. An application will be sent to you if coverage is desired. All information provided on this information sheet is confidential and will be used solely for the purpose of developing a quote for you. If you have more than 50 employees, just submit the form twice. You only need to enter the company name and your email address on the second form, along with the employee information.

Today, health care costs are high, and getting higher. Who will pay your bills if you have a serious accident or a major illness? You buy health insurance for the same reason you buy other kinds of insurance, to protect yourself financially. With health insurance, you protect yourself and your family in case you need medical care that could be very expensive. You can’t predict what your medical bills will be. In a good year, your costs may be low. But if you become ill, your bills could be very high. If you have insurance, many of your costs are covered by a third-party payer, not by you. A third-party payer can be an insurance company or, in some cases, it can be your employer.

Sign up for latest news updates. Please contact us for immediate information on how to implement these initiatives for your group-specific needs at info@medicalsolutionscorp.com or Call (855) 667-4621.

Get NY/NJ Individual Insurance:

National:

Please complete the following information if you would like to obtain an individual health insurance quote. Please understand this is not an application for insurance. An application will be sent to you if coverage is desired. All information provided on this information sheet is confidential and will be used solely for the purpose of developing a quote for you.

Highlights of the new dependent coverage legislation The legislation has two dependent coverage features, the “make available option” and the “young adult option” (also called “NY DU30 option”). Under the make available option, Insurers offer customers the option to provide dependent coverage to age 30. This option is similar to adding a rider to a benefits plan.

Under the NY DU30 option, dependents who reach the maximum age can elect extended coverage to age 30.

For either option, a dependent must meet these requirements:

Is a child of an employee or other group member insured under a group.

Is under age 30.

Is unmarried.

Is not insured by or eligible for coverage through the young adult’s own employer-sponsored group policy or contract, whether insured or self-funded, provided the policy or contract includes both hospital and medical benefits.

Lives or works in New York State or in the service area of the insurer’s network-based policy or contract (as set forth and defined by the policy or contract).

The American Resources and Recovery and Reinvestment Act of 2009 was signed into law by President Obama February 17th. Under the Act, certain individuals who are eligible for COBRA continuation health coverage, or similar coverage under State law, may receive a subsidy for 65 percent of the premiums for themselves and their families for up to nine months.

Click on the link below for detailed information on the American Recovery and Reinvestment Act of 2009 which went into effect February 17, 2009

These individuals are required to pay only 35 percent of the premium.

The employer may recover the subsidy provided to assistance-eligible individuals by taking the subsidy amount as a credit on its quarterly employment tax return. The employer may provide the subsidy – and take the credit on its employment tax return – only after it has received the 35 percent premium payment from the individual.

To qualify, a worker must have been involuntarily separated between Sept. 1, 2008, and Dec. 31, 2009. Workers who lost their jobs between Sept. 1, 2008, and enactment, but failed to initially elect COBRA because it was unaffordable, get an additional 60 days to elect COBRA and receive the subsidy.

This subsidy phases out for individuals whose modified adjusted gross income exceeds $125,000, or $250,000 for those filing joint returns. Taxpayers with modified adjusted gross income exceeding $145,000, or $290,000 for those filing joint returns, do not qualify for the subsidy.

On February 26, the Internal Revenue Service released its first round of information for employers to use in administering the new subsidy program. Included are the subsidy reporting form, instructions and a very detailed questions-and-answers piece. The Department of Labor is still working on model notices and other guidance for release by March 17.

The American Resources and Recovery and Reinvestment Act of 2009 was signed into law by President Obama February 17th. Under the Act, certain individuals who are eligible for COBRA continuation health coverage, or similar coverage under State law, may receive a subsidy for 65 percent of the premiums for themselves and their families for up to nine months.

The American Resources and Recovery and Reinvestment Act of 2009 was signed into law by President Obama February 17th. Under the Act, certain individuals who are eligible for COBRA continuation health coverage, or similar coverage under State law, may receive a subsidy for 65 percent of the premiums for themselves and their families for up to nine months.