The Health Exchange also known as The Health Marketplace or Obamacare Exchanges are set to open in less than 12 hours. Are you ready or aye you like most asking What is an Exchange? Starting Oct 1 you can enroll until March 31, 2014, though you’ll generally need to sign up by Dec. 15 of this year, to be covered as of Jan. 1. You can find your state’s marketplace at healthcare.gov. The prices for the marketplace plans are likely to be similar to those sold privately. A plan that is also available on the exchange may be eligible for subsidies. Heres an easy top 10 list of what you need to know.

10. Locate your State Exchange

Look up your state’s exchange here and Healthcare.gov. Some states are running their own exchange, others are running it through the federal government see www.healthcare.gov. For NY Tri-State the sites are:

NYS – http://info.nystateofhealth.ny.gov See rates here

CT – https://www.accesshealthct.com See rates here

9. Individual Mandate Penalty

For 2014, the annual penalty is $95 or 1% of your income, whichever is greater. The penalty will increase over the first three years. Coverage can include employer-provided insurance, individual health insurance, Medicare or Medicaid.

Health Insurance Individual Penalty for Not Having Insurance Pay the greater of the two amounts

Year

Percentage of Income

Set Dollar Amount

2014

1%

$95 & $285/family max

2015

2%

$325 & $975/family max

2016

2.5%

$695 & $2,085/family max

8. Individual Subsidies

Individuals who do not have affordable minimum essential coverage from their employer will be eligible for tax credit subsidies for their health insurance purchase on a state exchange if their income is below 400 percent of federal poverty level.

If you make under $45,960 or your family makes under $94,200, you could get a real break on health insurance costs More low-income people will also be eligible for free coverage under Medicaid For those eligible, the subsidies will cap the amount you pay for your exchange policy at between 2% and 9.5% of your income (on a sliding scale, based on your income). To find out how much you would pay, estimate your income for this year and plug it into any health subsidy calculator. You can also see estimate subsidies with these “health subsidy charts”.

7. Small Business Subsidy – SHOP Exchange

A key change is that the small business health care tax credits will only be available ONLY through the SHOP Exchange marketplace in 2014. Small businesses with 25 or fewer employees who receive less than $50,000 a year in wages may be eligible for tax credits if they purchase the plan through the SHOP marketplace. These credits will cover up to 50% of the employer’s cost (35% for non-profits) for the first two years of coverage. Click here to read more about the small business health care tax credits.

6. Your income

not your assets, such as your house, stocks or retirement accounts – will count toward determining whether you can get tax credits. When you buy your plan, you estimate your income for next year, and your tax credit is based on that estimate. The next year, your tax returns will be checked by the IRS and compared against your estimate.

5. Pre-Existing Conditions Eliminated

Your insurer generally can’t drop you, as long as you keep up with your insurance premiums and don’t lie on your application. Generally, people will be able to enroll in or change plans once a year during the annual open enrollment period. This first year, open enrollment on the exchanges will run for six months, from Oct. 1 through March of next year. But in subsequent years the time period will be shorter, running from October 15 to December 7.

4. Essential Health Benefits Covered

Each plan covers 10 “essential health benefits,” which include prescription drugs, emergency and hospital care, doctor visits, maternity and mental health services, rehabilitation and lab services, among others. In addition, recommended preventive services, such as mammograms, must be covered without any out-of-pocket costs to you. More info here.

3. Ninety-Day Maximum Waiting Period

Group health plans and health insurance issuers may not impose waiting periods of more than ninety days before coverage becomes effective. This also applies to grandfathered plans.

2. Annual or Lifetime Limits

Group health plans, including grandfathered plans, may no longer include more than restricted annual or any lifetime dollar limits on essential health benefits for participants. Limits may exist in and after 2014 for non-essential benefits.

1. Not Everyone is Eligible

Immigrants who are in the country illegally will be barred from buying insurance on the exchanges. However, legal immigrants are permitted to use the marketplaces and may qualify for subsidies if their income is no more than 400 percent of the federal poverty level (about $46,000 for an individual and $94,200 for a family of four).

members of certain religious groups and Native American tribes

incarcerated individuals

people whose incomes are so low they don’t have to file taxes (currently $9,500 for individuals and $19,000 for married couples)

Conclusion:

There has been a lot of news about individual Obamacare provisions getting delayed – Obamacare Employer mandate Delayed. Some people may assume that means the health law is being slowly dismantled, or put off for an additional several years. .The Affordable Care Act is an extremely complicated law with a lot of moving parts, but ultimately, the biggest provisions are still moving forward. There will likely be more hiccups along the way. As the enrollment period opens for Obamacare’s new exchanges, industry experts predict there will probably be other issues that need to be ironed out — but that doesn’t mean the whole law is collapsing

Still confused?

Don’t be. These are the common questions that we are working through with our clients daily. Am I better off going SHOP Exchange vs. Individual for my business? Am I better off going off Exchanges or onto Private Exchanges? Whats my minimum employer contribution? Do I have to cover employee and dependents? Is dental and vision included? What happens to my Healthy NY when it shuts down Jan 1, 2014? What employer notices must I be posting?

Please contact our team at Millennium Medical Solutions Corp if you have additional questions regarding how SHOP Exchanges and Individual Exchanges can benefit you Stay tuned to our site for updates as more information gets released. Sign up for latest news updates.

•Change in tax treatment for over-age dependent coverage •Accounting impact of change in Medicare retiree drug subsidy tax treatment •Early retiree medical reinsurance •Medicare prescription drug “donut hole” beneficiary rebate •Break time/private room for nursing moms

•No lifetime dollar limits on essential health benefits

•Restricted annual dollar limits on essentail health benefits, phased amounts until 2014

•No pre-existing condition limitations for enrollees up to age 19 and no rescissions

•No health FSA/HRA/HSA reimbursement for non-prescribed drugs

•Increased penalties for non-qualified HSA distributions

•Additional standards for new or “non-grandfathered” health plans, including preventive care in network with no cost-sharing appeal and external review, provider choice and non-discrimination provisions for insured plans

•Income-based Medicare Part D premiums Pharmaceutical importers and manufacturers’ fees start

•Medicare, Medicare Advantage benefit and payment reforms

•Insurers subject to medical loss ratio rules

•Employers to distribute uniform summary of benefits and coverage (SBC) to participants (deadlines vary with group of recipients)

•60-day advance notice of mid-year material modifications to SBC content

•Form W-2 reporting for health coverage (track in 2012 for W-2 form provided in early 2013)

•Coverage for additional women’s preventive care services

•$2,500 per plan year health FSA contribution cap (plan years on or after January 1, 2013)

•Comparative effectiveness group health plan fees first due

•Annual dollar limits on essential health benefits cannot be lower than $2 million

•Employers notify employees about exchanges •Medical device manufacturers’ fees start •Higher Medicare payroll tax on wages exceeding $200,000/individual; $250,000/couples

•Change in Medicare retiree drug subsidy tax treatment takes effect •Health Insurance exchanges initial open enrollment period

•Health insurance exchanges

•Individual coverage mandate

•Financial assistance for exchange coverage of lower-income individuals

•States Medicaid expansion (possibly only some states)

•Employer shared responsibility

•Dependent coverage to age 26 for any covered employee’s child

•No annual dollar limits on essential health benefits

•No pre-existing condition limits

•No waiting period over 90 days

•Wellness limit increase allowed

•Health insurance industry fees

•Additional standards for non-grandfathered health plans, including limits on out-of-pocket maximums, provider nondiscrimination, and coverage of routine medical costs of clinical trial participants

•Small market, non-grandfathered insured plans must cover essential health benefits with limited deductibles (initially $2,000/individual, $4,000/family), using a form of community rating

•Insurers must apply guaranteed issue and renewability to non-grandfathered plans of all sizes

•Auto enrollment sometime after 2014

•Temporary reinsurance fees first due in late 2014/early 2015

•Additional employee-specific reporting and disclosure of 2014 coverage

•40% excise tax on “high cost” or Cadillac coverage

[tab_item title=”Reminder PCORI Research Fees Due by July 231st”]

Posted on July 24 2013

Fees Apply to Employers Sponsoring Certain Self-Insured Plans

Effective for plan years ending on or after October 1, 2012, and before October 1, 2019, employers that sponsorcertain self-insured plans are responsible for new fees to fund the Patient-Centered Outcomes Research Institute (also known as PCORI). HRAs and health FSAs that are not treated as excepted benefits are generally subject to the fees.

Fees are due no later than July 31st of the year following the last day of the plan year. The IRS has revised Form 720for affected employers to report and pay the required fees.

Review our Health Care Reform Checklist for information on other requirements impacting employers and group health plans this year.

[/tab_item]

[tab_item title=”Affordable Care Act Weekly Webinar Series”]

Posted on July 23 2013

Free Series for Small Business Owners to Help Understand the Law

The U.S. Small Business Administration (SBA), together with the Small Business Majority (a national nonprofit advocacy organization), has launched the Affordable Care Act 101 Weekly Webinar Series. The webinars feature guidance on key pieces of the law for small business owners provided by SBA representatives, followed by a question and answer period.

Topics being discussed in the webinars include:

Small business tax credits—who is eligible and how to claim the credit;

Shared responsibility (also known as “pay or play”);

Cost containment; and

Tools and resources available for small businesses to learn more about the law.

The free series will take place every Thursday from now through the opening of the Health Insurance Exchanges (Marketplaces) in October. The first series of webinars will cover the same content; a second round of webinars featuring new content will be held later this fall.

The registration links for the first series of webinars can be found by clicking here. After registering, you will receive a confirmation email with all of the information needed to access the webinar either by telephone or online.

Visit our Health Care Reform Blog section to stay on top of the latest Affordable Care Act updates.

[/tab_item]

[tab_item title=”4 Things Employers Should Know About Providing the Health Insurance Exchange Notice”]

Posted on July 19 2013

Notice Must Be Distributed to Current Employees No Later Than October 1, 2013

Following a delay in the original effective date, employers will need to comply with the new requirement to provide each employee a written notice with information about a Health Insurance Exchange (also known as a Marketplace) beginning this fall. Below are four important reminders about the notice.

The notice requirement applies to employers covered by the federal Fair Labor Standards Act (FLSA). In general, the FLSA applies to employers that employ one or more employees who are engaged in, or produce goods for, interstate commerce. For most firms, a test of not less than $500,000 in annual dollar volume of business applies. The FLSA also specifically covers certain entities such as hospitals, educational institutions, and government agencies.

Employers must provide the notice to each employee, regardless of plan enrollment status (if applicable) or of part-time or full-time status. Employers are not required to provide a separate notice to dependents or other individuals who are or may become eligible for coverage under the plan but who are not employees.

The U.S. Department of Labor has provided two sample notices employers may use to comply with this requirement. The law requires that specific information be included in each notice. One model notice is available for employers that offer a health plan to some or all employees, and another model notice may be used by employers that do not offer a health plan.

Notices must be provided to each current employee no later than October 1, 2013, and to each new employee at the time of hiring beginning October 1, 2013. In general, a notice will be considered provided at the time of hiring if it is provided within 14 days of an employee’s start date. The notice is required to be provided automatically and free of charge. Employers may distribute the notice by first-class mail, or electronically if certain requirements are met.

Visit our section on Health Reform Resource for information on other notices required to be provided and to download additional model notices available for employers and group health plans.

[/tab_item][tab_item title=”5 Q and As on Individual Shared Responsibility”]

Posted on July 12 2013

Employer-Sponsored Coverage Considered “Minimum Essential Coverage”

The individual shared responsibility provision, which goes into effect on January 1, 2014, requires individuals of all ages (including children) to have minimum essential health coverage for each month, qualify for an exemption, or make a payment when filing his or her federal income tax return. Below are five questions and answers related to the mandate that may be of interest to employers and employees.

1. What counts as minimum essential coverage? Minimum essential coverage includes employer-sponsored coverage (including COBRA coverage and retiree coverage), coverage purchased in the individual market, Medicare Part A coverage and Medicare Advantage, Children’s Health Insurance Program (CHIP) coverage, and certain other types of coverage.

Minimum essential coverage does not include coverage providing only limited benefits, such as coverage only for vision care or dental care, workers’ compensation, or disability policies.

2. If an employee receives coverage from a spouse’s employer, will that employee have minimum essential coverage? Yes. Employer-sponsored coverage is generally minimum essential coverage. If an employee enrolls in employer-sponsored coverage for himself and his family, the employee and all of the covered family members have minimum essential coverage.

3. Does an employee’s spouse and dependent children have to be covered under the same policy or plan that covers the employee? No. An employee, his or her spouse, and dependent children do not have to be covered under the same policy or plan. However, the employee, spouse, and each dependent child for whom the employee may claim a personal exemption on his or her federal income tax return must have minimum essential coverage or qualify for an exemption, or a payment will be owed.

4. A company’s health plan is “grandfathered.” Does the employer’s plan provide minimum essential coverage? Yes. Grandfathered group health plans provide minimum essential coverage.

5. Is transition relief available in certain circumstances? Yes. Notice 2013-42 provides transition relief from the shared responsibility payment for individuals who are eligible to enroll in employer-sponsored health plans with a plan year other than a calendar year (non-calendar year plans) if the plan year begins in 2013 and ends in 2014. The transition relief applies to an employee, or an individual having a relationship to the employee, who is eligible to enroll in a non-calendar year eligible employer-sponsored plan with a 2013-2014 plan year. The transition relief begins in January 2014 and continues through the month in which the 2013-2014 plan year ends.

For More Information You may review additional questions and answers in their entirety on the IRS website.

[/tab_item][tab_item title=”IRS Guidance on Delay of Pay or Play Requirements”]

Posted on July 10 2013

No Penalties Will Be Assessed for 2014

Formal guidance released by the IRS provides additional details regarding the delay of the Health Care Reform “pay or play” requirements. Under those provisions, certain large employers (generally those with at least 50 full-time employees) who do not offer full-time employees affordable health insurance that provides a minimum level of coverage may be subject to a penalty tax.

According to the guidance, no penalties (also known as employer shared responsibility payments) will be assessed for 2014. The “pay or play” requirements will be fully effective for 2015 and employers are encouraged to maintain or expand health coverage in 2014 in preparation for compliance.

The delay is a result of transition relief being provided for 2014 with respect to certain employer and insurer reporting requirements. Such reporting will be necessary for the IRS to determine whether a penalty may be due, and, consequently, the transition relief makes it impractical to determine which employers owe shared responsibility payments for 2014. Once the information reporting rules are issued, employers are encouraged to voluntarily comply with the reporting requirements in 2014.

The delay does not affect the application or effective dates of other Health Care Reform provisions, including the individual shared responsibility requirements and employees’ access to premium tax credits for enrolling in qualified health plans through the Health Insurance Exchanges.

Change in tax treatment for over-age dependent coverage

Accounting impact of change in Medicare retiree drug subsidy tax treatment

Early retiree medical reinsurance

Medicare prescription drug “donut hole” beneficiary rebate

Break time/private room for nursing moms

[/tab_item]

[tab_item title=”2011″]

No lifetime dollar limits on essential health benefits

Restricted annual dollar limits on essentail health benefits, phased amounts until 2014

No pre-existing condition limitations for enrollees up to age 191 and no recissions

No health FSA/HRA/HSA reimbursement for non-prescribed drugs

Increased penalties for non-qualified HSA distributions

Additional standards for new or “non-grandfathered” health plans, including preventive care in network with no cost-sharing appeal and external review, provider choice and non-discrimination provisions for insured plans

Income-based Medicare Part D premiums

Pharmaceutical importers and manufacturers’ fees start

Medicare, Medicare Advantage benefit and payment reforms

Insurers subject to medical loss ratio rules

[/tab_item]

[tab_item title=”2012″]

Employers to distribute uniform summary of benefits and coverage (SBC) to participants (deadlines vary with group of recipients)

60-day advance notice of mid-year material modifications to SBC content

Form W-2 reporting for health coverage (track in 2012 for W-2 form provided in early 2013)

Coverage for additional women’s preventive care services5

[/tab_item]

[tab_item title=”2013″]

$2,500 per plan year health FSA contribution cap (plan years on or after January 1, 2013)

Comparative effectiveness group health plan fees first due

Annual dollar limits on essential health benefits cannot be lower than $2 million

Employers notify employees about exchanges

Medical device manufacturers’ fees start

Higher Medicare payroll tax on wages exceeding $200,000/individual; $250,000/couples

Change in Medicare retiree drug subsidy tax treatment takes effect

Health Insurance exchanges initial open enrollment period

[/tab_item]

[tab_item title=”2014″]

Health insurance exchanges

Individual coverage mandate

Financial assistance for exchange coverage of lower-income individuals

States Medicaid expansion (possibly only some states)

Employer shared responsibility

Dependent coverage to age 26 for any covered employee’s child

No annual dollar limits on essential health benefits

No pre-existing condition limits

No waiting period over 90 days

Wellness limit increase allowed

Health insurance industry fees

Additional standards for non-grandfathered health plans, including limits on out-of-pocket maximums,

provider nondiscrimination, and coverage of routine medical costs of clinical trial participants

Small market, non-grandfathered insured plans must cover essential health benefits with limited deductibles (initially $2,000/individual, $4,000/family), using a form of community rating

Insurers must apply guaranteed issue and renewability to non-grandfathered plans of all sizes

Auto enrollment sometime after 2014

[/tab_item]

[tab_item title=”2015″]

Temporary reinsurance fees first due in late 2014/early 2015

Additional employee-specific reporting and disclosure of 2014 coverage

[/tab_item]

[tab_item title=”2018″]

40% excise tax on “high cost” or Cadillac coverage

Jan 1 Deadline is Today. Attention last minute health insurance shoppers you have until midnight to purchase a policy on the Health Exchange.

NYS Health Exchange is down again. Not surprisingly a large volume of late comers trying to beat t0morrows deadline for Jan 1, 2014. Last week a 34% enrollment spike in 1 week alone. Despite the 1 week extension the enrollments are still falling short of the original 600,000 projection. A significant percentage have instead been qualified under expanded Medicaid in NYS. At the same time many New Yorkers have had sole prop and husband/wife groups shut out of the small group market place. In addition, popular programs such as Healthy NY have been increased by 25-35% and new $600/single or $1200/family deductibles.

Facts:

Some people mistakenly believe they have until Dec. 31 to enroll in a plan that takes effect on Jan. 1. Others don’t realize they could pay a federal tax penalty if they don’t have health insurance in place by March 31.

Under the Affordable Care Act, most adults will pay a $95 penalty — or 1 percent of income — in 2014 if they don’t have health insurance coverage. The penalty rises to $695 — or 2 percent of income — by 2016.

To avoid the penalty, people must enroll in a plan by Feb. 15 or qualify for an exemption from the penalty.

Consumers who sign up by Dec. 23 and pay the first month’s premium by Jan. 10 will have coverage on Jan. 1, the industry group America’s Health Insurance Plans announced Wednesday.

If you make under $45,960 or your family makes under $94,200, you could get a real break on health insurance costs More low-income people will also be eligible for free coverage under Medicaid For those eligible, the subsidies will cap the amount you pay for your exchange policy at between 2% and 9.5% of your income (on a sliding scale, based on your income). To find out how much you would pay, estimate your income for this year and plug it into any health subsidy calculator. You can also see estimate subsidies with these ”health subsidy charts”.

Important: If the web site is down we can sign up via paper application to avoid the penalty. A surge of 34% enrollments in one week caused some technical delays last week.

For more information regarding both Exchanges – Individual Exchanges or SHOP please contact our team at Millennium Medical Solutions Corp (855)667-4621. We have Spanish, Russian, and Hebrew speakers available. Quotes can also be viewed on our site.

360PEO is an award-winning Independent PEO Brokerage representing SMB. We work with top 100 PEOs and customize personalized HR Solutions, competitive benefits, payroll services, Workman’s Comp, risk and compliance services. Helping people with productivity and large buying group perks.

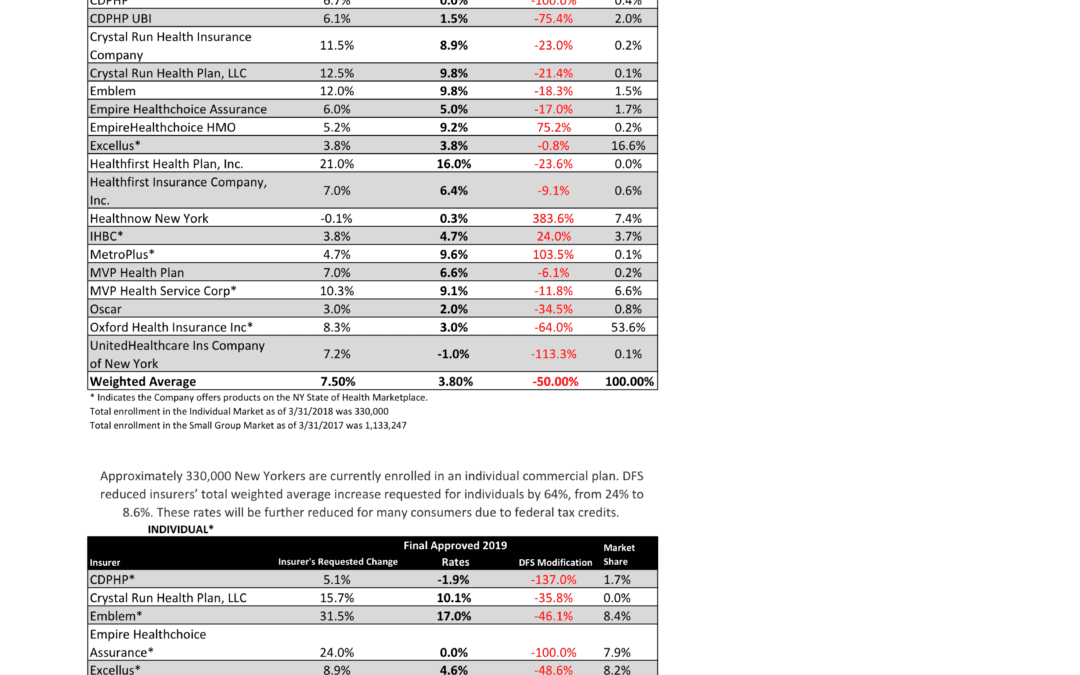

NYS has approved 2019 Final Rates last Friday. Small group rates will increase 3.8% and 8.6% for individuals.

As per NY State Law, Health Insurers are required to send out early notices of rate request filings to groups and subscribers see original –NYS 2019 Rate Requests. Despite only 3 months of mature claims data experience for 2018 health insurers’ original requests were noticeably below average 7.5% for small group and 24% for individuals. Ultimately NYS reduced this request substantially by approximately 50%.

Experts are concerned over the long term effects. Example, the Individual mandate was removed last December by Presidential order. Without the Mandate anyone can drop insurance without penalty. A comparable take away for similar auto insurance industry would be something like this -Drivers ought not be mandated to buy auto insurance as its a profit scheme by Insurers. While a popular decision this will hardly bend the curve long term and reduce competition. Furthermore, the new order of Selling Across State lines makes NYS most unwelcoming.

OTHER STATES

Insurers have been filing to sell Obamacare plans that will go into effect in 2019, and in some states they appear to be pricing in for the fact that the mandate is going away next year. Other states are seeing mild increases, but that is in part because they saw significant hikes for the previous year.

Insurers have concluded that fewer people will enroll without the mandate than otherwise, so in some places they are pricing their plans higher based on the assumption that sicker people will be left behind, which will increase medical costs for those left. It is well worth pointing out that in recent years the loss federal risk reinsurance corridor funds account for 5.5 percent of the rate increase.

How are neighboring States doing?

In NJ, not that bad. Last year the average increase were 5.5% for small groups and some popular plans such as Horizon Blue Cross Blue Shield’s OMINA increasing only 4.8% increase. This year the increase is only 5.2. Other insurers offering EPO and HMO plans in the individual market for 2019 include Oscar Health and Oxford Health Plans.

With individual mandate repeal fewer people will buy health insurance raising the prices for those who do. NJ Banking and Insurance Department officials said premium prices would have increased, on average, by 12.6 percent.

For CT market, on the other hand, things are much worse at least for the individual marketplace with average 25% rate increases last year. The 2019 proposed rate increases for both the individual and small group market are, on average lower, than last year: The proposed average small group rate increase request is a 10.22 percent and ranges from -5.0 percent to 21.1 percent. This compares to the average increase request of 18.06 percent requested last year.The proposed average individual rate increase request is 12.3 percent and ranges from -10.9 percent to 31.0 percent. This compares to the average increase request of 25.51 percent requested last year.

Final plan rates in New Jersey & CT will be finalized and released in the fall, state officials said. ACA open enrollment begins Nov. 1

Trend: Trend is a factor that accounts for rising health care costs, including the cost of prescription drugs, and the increased demand for medical services.

Uncertainty in Washington:

Removal of penalty for individual mandate: The elimination of the penalty means that individuals who are typically younger and healthier would have no inducement to participate in the insurance pool, which could further destabilize the market. Lack of participation shrinks the pool and increases the cost of insurance to the remaining members.

Short-duration health plans and Association Health Plans: Still pending are final federal regulations on non-ACA compliant short-duration plans, which may have implications for the ACA risk pool. Also, Connecticut along with other state insurance regulators, are awaiting clarification from the federal government on new federal regulations allowing association health plans, which could further shrink the ACA risk pool.

A bipartisan group of congressional representatives has discussed an agreement to extend and guarantee the payments, but it’s unclear whether they could do so by the new filing deadline of Sept. 5. A lawsuit filed by Congress against the Obama administration to challenge the payments is still pending. In addition, Trump has repeatedly threatened to withhold payments to insurers that reduce cost-sharing – deductibles, copays and coinsurance – paid by low-income customers. More than half of New Jersey’s marketplace customers receive that assistance, and without it, most would be unable to afford coverage.

Finally, a tax on health insurance premiums has been reinstated in 2018 after a one-year “tax holiday” approved by Congress for 2017. That contributed 2.3 percent to the rate hikes that insurers requested for 2019 and for 2019

SMALL GROUP MARKET VS. INDIVIDUAL MARKET

Importantly, small group market is still more advantageous than individual markets unless one gets a sizable low-income tax credit. Overall, about 350,000 individual plan consumers will be affected by the price hike, while more than a million users will be hit by higher small group fees. Last year, Blue Cross Blue Shield released a study showing Obamacare user costs were 22 percent higher than people with employer-sponsored health plans, while UnitedHealthplans to exit most Exchanges see – Breaking: Oxford Exits Metro Indiv & Oxford Liberty HMO 2017.

The correct approach for a small business in keeping with simplicity is a Private Exchange and with our large buying group PEO partnerships. This is a true defined contribution empowering employees with a choice of leading insurers offering paperless technologies integrating HRIS/Benefits/Payroll. Both employee and employers still gain tax advantage benefits under the business. Also, the benefits, rates and network size are superior under a group plan as the risk are lower for small group plans than individual markets.

Learn how a PEO Partnership can help your group please contact us at info@360PEO.com or (855)667-4621.

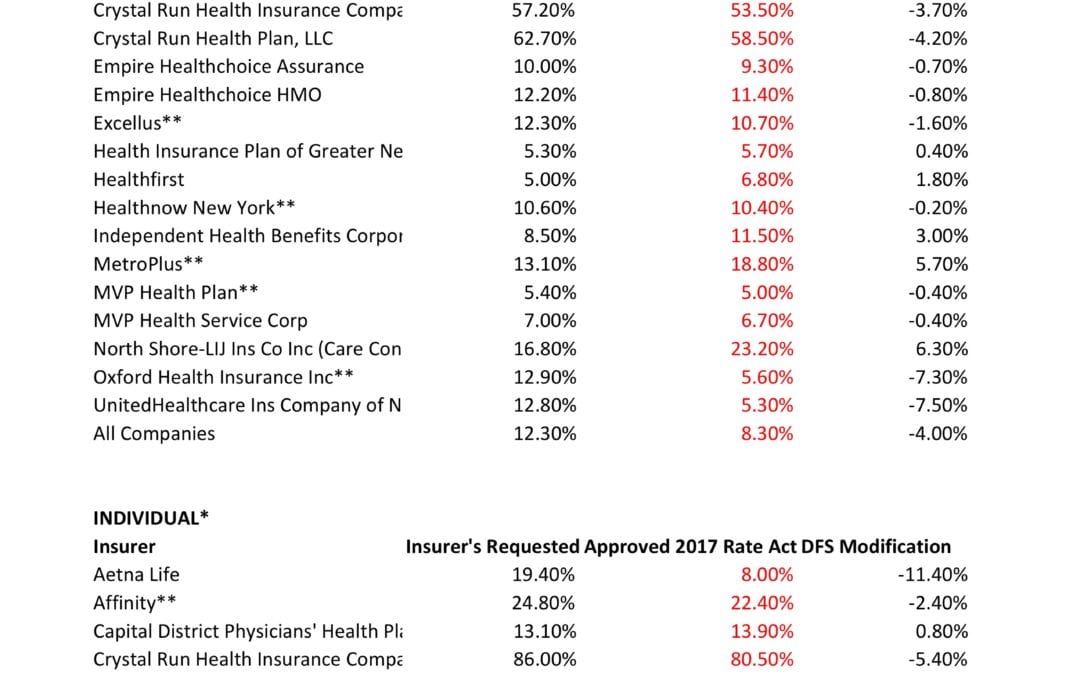

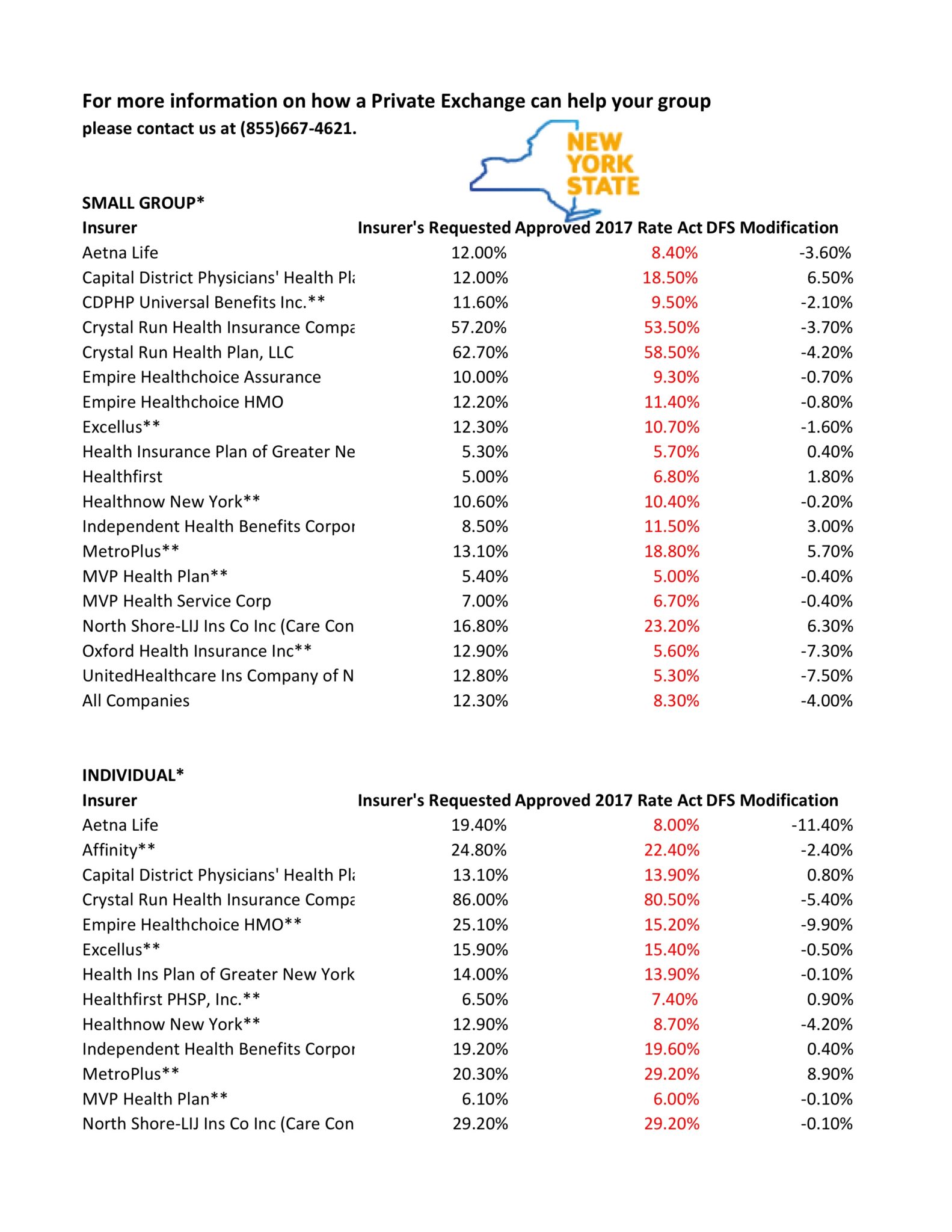

NYS has approved 2017 Final Rates. Small group rates will increase 8.3%, a reduction from the 12.3% average originally requested. In the individual market, the average increase will be 16.6%, a reduction from the originally requested 19.3%.

As per NY State Law carriers are required to send out early notices of rate request filings to groups and subscribers see original –NYS 2017 Rate Requests. With only 3 months of mature claims experience for 2016 health insurers’ requests are historically above average. Ultimately the State reduces this request substantially. This year, however, NYS acknowledged that medical costs increased, citing a 7-percent average increase on the individual market and an 8.5-percent increase on the small group market. The administration also acknowledged drug prices have impacted insurers, pointing specifically to blockbuster drugs for Hepatitis C.

OTHER STATES

The national rate trend, however, has been much higher than in past years due to higher health care costs Like other states throughout the nation, the 2017 rate of increase for individuals in New York is higher than in past years partly due to the termination of the federal reinsurance program. The lost of the program’s aka federal risk reinsurance corridor funds accounts for 5.5 percent of the rate increase.

How are neighboring States doing? In NJ, not that bad. According to a review of filings made public last week the expected rate increase will be likley ve half. Example: Horizon Blue Cross Blue Shield requested a 4.8% increase on their OMINA Plans. For CT market, on the other hand, things are much worse at least for individual marketplace with average 25% rate increases.

SMALL GROUP MARKET VS. INDIVIDUAL MARKET

The new premium hikes ranged from as little as 5.6 percent for Oxford Small group to a whopping 58.5% percent increase for Crystal Run Health Insurance Company, an insurer that covers parts of the Hudson Valley and Catskills. Importantly, small group market are still more advantageous than individual markets unless one gets a sizable low income tax credit.

Overall, about 350,000 individual plan consumers will be affected by the price hike, while more than a million users will be hit by higher small group fees.Earlier this year, Blue Cross Blue Shield released a study showing Obamacare user costs were 22 percent higher than people with employer-sponsored health plans, while UnitedHealthplans to exit most Exchanges see – Breaking: Oxford Exits Metro Indiv & Oxford Liberty HMO 2017.

The correct approach for a small business in keeping with simplicity is a Private Exchange. This is a true defined contribution empowering employees with choice of leading insurers offering paperless technologies integrating HRIS/Benefits/Payroll. Both employee and employers still gain tax advantage benefits under the business. Also, the benefits, rates and network size are superior under a group plan as the risk are lower for small group plans than individual markets.

* All amounts are rounded to the nearest 1/10.

**Indicates that the company makes products available on the “New York State of Health” marketplace.

***After rate applications were filed on 5/9/2016, additional information, including the final results of the federal risk adjustment program, prompted several insurers to update their initially filed rates.

For more information on how a Private Exchange can help your group please contact us at (855)667-4621.

“The deadline for individuals and families to enroll in a qualified health plan through NY State of Health is February 15, 2015. However, the Marketplace will provide additional assistance to those individuals who have taken steps to apply for coverage but have been unable to complete the enrollment process before the deadline. All applications and enrollments in health plans must be completed by the end of the day on February 28, 2015. Those who complete their enrollment after February 15, 2015 but on or before February 28, 2015 will have coverage starting on April 1, 2015.”

2/12/15

Last days for 2015 Individual Open Enrollment is ending this week. This deadline applies to both On and Off Exchange!

If you’re wondering about the penalty for not having insurance: yes, there is one, and no, you can’t really get out of paying for it. You’ll pay the penalty when you file your taxes for 2015. Even if you get coverage midway through the year, you’ll still need to pay a penalty for the months you weren’t insured. So get covered!

Think you might be eligible for a subsidy or aren’t sure?

You can check here at the New York State of Health Marketplace calculator. If you are eligible or think you might be eligible, you can contact the marketplace directly to purchase a plan or ask questions about financial assistance.

Please remember that during open enrollment you are permitted to switch carriers. Choose wisely because after February 15, one cannot switch plans until open enrollment 2015, unless you have a “qualifying event,” such as marriage, divorce, birth or adoption.

Individual Online Enrollment Resources for On and Off Exchange:

For NYS – To view Oscar’s plans, rates and simple online enrollment application, click here.

For more information on enrollment please contact our team at Millennium Medical Solutions Corp (855)667-4621. We have Spanish, Russian, and Hebrew speakers available.

The NCQA believes its own health plan accreditation program and program data could useful to exchange programs, the NCQA says. With so much more individual choice on both, the Marketplace Health Exchange and off-Exchange along with new Health Insurers this is an important consumer tool.

About NCQA

NCQA is a private, non-profit organization dedicated to improving health care quality. NCQA’s Healthcare Effectiveness Data and Information Set (HEDIS®) is the most widely used performance measurement tool in health care. NCQA accredits and certifies a wide range of health care organizations and recognizes physicians in key clinical areas. NCQA is committed to providing health care quality information through the Web, media and data licensing agreements in order to help consumers, employers and others make more informed health care choices.

NCQA accreditation ratings are based on three sets of measurements HEDIS®, CAHPS® and NCQA accreditation standards. Health plans in every state, the District of Columbia and Puerto Rico are NCQA Accredited. These plans cover 109 million Americans or 70.5 percent of all Americans enrolled in health plans.

HEDIS is a set of standardized performance measures designed to ensure that purchasers and consumers have the information they need to reliably compare health care quality. The Consumer Assessment of Healthcare Providers and System (CAHPS) is a survey mailed to select members asking them to rate their experience with the care given by their doctors and the services provided by their plans.

How the Results of HEDIS and CAHPS Help Consumers Results from HEDIS and CAHPS enable consumers to understand how well Insurers are fulfilling our clinical agenda to help members stay healthy, get better quickly or live effectively with chronic illness. In addition, the scores facilitate our ability to identify areas of care and service where we can continue to improve. The results also enable us to compare our companies’ performance with other local and national health plans.

The “Excellent” ratings our plans received demonstrate that members continue to receive high-quality health care and that they are satisfied with the service that their physicians, health care practitioners and health plans provide.

HEDIS® (Healthcare Effectiveness Data and Information Set) is a registered trademark of the National Committee for Quality Assurance (NCQA).

CAHPS® (Consumer Assessment of Healthcare Providers and Systems) is a registered trademark of the Agency for Healthcare Research and Quality (AHRQ).

For more information about these plans and the full range of offerings available through MMS Inc. contact us today at (855) 667-4621.

Your plans NCQA 2014 Rating

NCQA Health Insurance Plan Rankings 2014-2015

Click on any Plan Name for details.

Methodology and other information about the rankings is here