OK so this may not be the catatonic movie of our favorite State starring Zach Braff and Natalie Portman but just the same Oxford couldn’t resist using the same logical name for the new network. Starting Sept 1, 2014 Oxford will be offering the Oxford Garden State Network on all size NJ group business. The 18,000 Doctor and 65 hospitals network will answer the call for a flexible lower cost plan option.

Judging by the #1 selling plan – Oxford Liberty HMO the market supports a smaller lower cost quality network. Taking the same playbook Oxford unveiled their plan last Friday. The plan will cover members outside NJ only on emergencies. Unlike the Liberty HMO some plans options are non-gated plans not needing referrals to for access to a Specialist Doctor.

The Garden State Network provides access to the 21 New Jersey counties only.The Garden State Network does not provide national access to the UnitedHealthcare Choice Plus network. For NJ 1-50, up to 4 plan options can be selected and the Garden State products can be paired with Liberty and Freedom network options. With this network, employers can select which of the 13, in-network only plan designs available will work best for their needs and for the needs of their employees.

Oxford/United has been purchasing Provider groups since 2011 , see our post UnitedHealthcare Buying Medical Groups? This strategy of late is by no means exclusive to this Insurer but it is worth pointing them out as they are a national leading health Provider and worth paying attention to.

Some highlights of the plan designs available with the Oxford Garden State Network are below:

∙ Routine, in-network preventive care covered at 100 percent

∙ In-network only coverage

∙ Choice between 11 non-gated and two gated plan designs (gated plan designs will require a referral)

∙ Plan designs with copayments, deductible and coinsurance, and Health Savings Accounts (HSA) are available.

Sign up for latest news updates. Please contact us for immediate information on how to implement these initiatives for your group-specific needs at info@medicalsolutionscorp.com or Call (855) 667-4621.

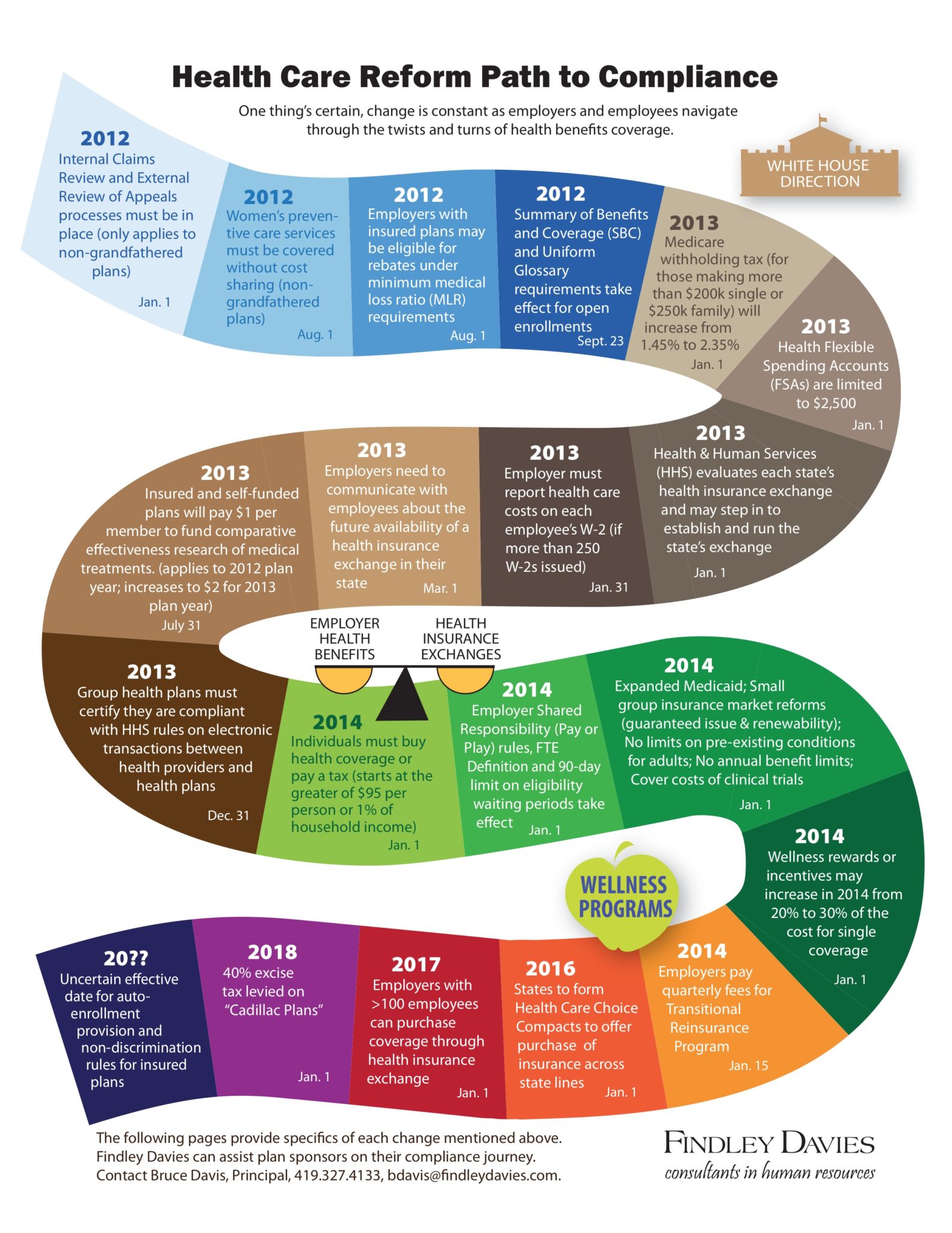

IRS Releases Draft of Employer Reporting Form for Health Reform Law Compliance

Business Insurance Story by Matt Dunning

Click Above

July 28, 2014

The Internal Revenue Service has issued draft versions of the reporting forms most employers will begin using next year to show that their group health insurance plans comply with the health care reform law.

The long-awaited draft forms, posted late Thursday afternoon to the IRS’ website, are the first practical application of employers’ health care coverage and enrollment reporting obligations under the Patient Protection and Affordable Care Act since the regulations were finalized in March.

The forms are the primary mechanism through which the government intends to enforce the health care reform law’s minimum essential coverage and shared responsibility requirements for employers.

Beginning in 2015, employers with at least 100 full-time employees will be required to certify that benefits-eligible employees and their dependents have been offered minimum essential coverage and that their employees’ contributions to their premiums comply with cost-sharing limits established under the reform law. Smaller employers with 50-99 full-time employees are required to begin reporting in 2016.

Additionally, self-insured employers will be required to submit documentation to ensure compliance with minimum essential coverage requirements under the reform law’s individual coverage mandate.

“In accordance with the IRS’ normal process, these draft forms are being provided to help stakeholders, including employers, tax professionals and software providers, prepare for these new reporting provisions and to invite comments from them,” the IRS said in a statement released Thursday.

The IRS said it expects to publish draft instructions for completing the reporting forms by late August and that both the forms and the instructions would be finalized later this year.

Last year, the Obama administration announced it would postpone implementation of employers’ minimum essential coverage and shared responsibility obligations under the reform law for one year, largely due to widespread complaints about the complexity of the reporting requirements.

Though several months have passed since the administration issued a simplified set of information reporting rules, many employers have delayed preparations for meeting the requirements until the forms and instructions are available for review, said Richard Stover, a principal with Buck Consultants at Xerox in Secaucus, New Jersey.

“A lot of employers really haven’t been doing anything about reporting requirements, even with the final regulations in place, because they were waiting for these forms,” Mr. Stover said. “This is something they’ve been anxious to see.”

Under the Consolidated Omnibus Budget Reconciliation Act (COBRA), an individual who was covered by a group health plan on the day before the occurrence of a qualifying event (such as a termination of employment or a reduction in hours that causes loss of coverage under the plan) may be able to elect COBRA continuation coverage upon that qualifying event. Individuals with such a right are referred to as qualified beneficiaries.

Under COBRA, group health plans must provide covered employees and their families with certain notices explaining their COBRA rights. A group health plan must provide each covered employee and spouse (if any) with a written notice of COBRA rights “at the time of commencement of coverage” under the plan (general notice). A group health plan must also provide qualified beneficiaries with a notice which describes their rights to COBRA continuation coverage and how to make an election (election notice).

General Notice: The general notice must be furnished to each covered employee (and their spouse if covered under the plan) not later than the earlier of: (1) 90 days from the date on which the covered employee or spouse first becomes covered under the plan or, if later, the date on which the plan first becomes subject to the continuation coverage requirements; or (2) the date on which the administrator is required to furnish an election notice to the employee or to his or her spouse or dependent.

Election Notice: The election notice must be provided to the qualified beneficiaries within 14 days after the plan administrator receives notice that a qualifying event has occurred. Some qualified beneficiaries may want to consider and compare health coverage alternatives to COBRA continuation coverage, such as coverage that is available through the Health Insurance Marketplace (Exchange). Qualified beneficiaries may be eligible for a premium tax credit (a tax credit to help pay for some or all of the cost of coverage in plans offered through the Exchange) and cost-sharing reductions (amounts that lower out-of-pocket costs for deductibles, coinsurance, and copayments), and may find that Exchange coverage is more affordable than COBRA.

The Children’s Health Insurance Program Reauthorization Act of 2009 (CHIPRA) specifies that an employer that maintains a group health plan in a State that provides premium assistance for the purchase of coverage under a group health plan is required to notify each employee of potential opportunities currently available for premium assistance in the State in which the employee resides.

The Department of Labor has model notices that plans may use to satisfy the requirement to provide the general notice and election notice under COBRA, and the notice regarding premium assistance under CHIPRA. The COBRA model election notice was revised on May 8, 2013 to help make qualified beneficiaries aware of other coverage options that would soon become available in the Marketplace. Recently the DOL issued a Notice of Proposed Rulemaking, as well as updated versions of the model general notice and model election notice that reflect that the Exchange is now open and that better describes special enrollment rights in Exchange coverage. The DOL is also issuing a revised CHIPRA notice with similar updates related to Marketplace coverage.

Sign up for latest news updates. Please contact us for immediate information on how to implement these initiatives for your group-specific needs at info@medicalsolutionscorp.com or Call (855) 667-4621.

Adding a one-month orientation period may help an employer avoid complying with the new health benefits. Federal agencies are offering employers a benefits-free 30 day orientation period option in final regulations. There is also clarification on how employers must treat certain categories of new hires, as either FT , PT or Seasonal employees

The Final Regulations

These final regulations provide that the one month period would be determined by adding one calendar month and subtracting one calendar day, measured from an employee’s start date in a position that is otherwise eligible for coverage. For example, if an employee’s start date in an otherwise eligible position is May 3, the last permitted day of the orientation period is June 2. Similarly, if an employee’s start date in an otherwise eligible position is October 1, the last permitted day of the orientation period is October 31.

The new regulations implement part of the “employer shared responsibility mandate” provisions created by the Patient Protection and Affordable Care Act (PPACA). In all categories of new hire the e final regulations provide that one month is the maximum allowed length of an employment-based orientation period. For any period longer than one month that precedes a waiting period, the 90-day period begins after an individual is otherwise eligible to enroll under the terms of a group health plan.

When must an employer offer coverage:

The final regulations continue to provide that if a group health plan conditions eligibility on an employee’s having completed a reasonable and bona fide employment-based orientation period, the eligibility condition is not considered to be designed to avoid compliance with the 90-day waiting period limitation if the orientation period does not exceed one month and the maximum 90-day waiting period begins on the first day after the orientation period.

These final regulations apply to group health plans and health insurance issuers for plan years beginning on or after January 1, 2015.

When the Employer Might be Subject to a Penalty:

If at least one full-time employee of the employer buys health insurance in a public Exchange (Marketplace) and qualifies for a subsidy (either a premium tax credit or a cost-sharing reduction), the employer must pay a penalty.

There are two different types of penalties.

)The IRC section 4980H(a) penalty applies if a large employer offers coverage to less than 70% of its full-time employees in 2015 (or to less than 95% after the 2015 plan year). This penalty is $2000 annually or $166.67/month times the total number of “full-time” employees minus the first 80 (minus the first 30 after 2015). The penalty calculation does not include variable hour or seasonal employees who are in their measurement or administrative periods, even if they in fact worked on average at least 30 hours/week or 130/month during those periods. Nor does it include those who are in their stability periods but who did not qualify for coverage based on their hours worked during the associated measurement period.

IRC section 4980H(b) penalty. It applies if a large employer offers coverage to at least 70% of its full-time employees (95% after 2015), but for some full-time employees the coverage is either not “affordable” or does not provide minimum value. This penalty is $3,000 annually or $250/month for each full-time employee who buys health insurance in a public Exchange (Marketplace) and qualifies for a subsidy and for whom the employee cost for self-only coverage under the lowest-cost option available from the employer is more than 9.5% of the employee’s household income (or one of three safe harbors), or for whom the employer coverage offered does not provide at least minimum value. Again, the penalty calculation does not apply if the employee who qualified for a subsidy was a variable hour or seasonal employee who was in his/her measurement or administrative periods, nor does it include those employees who are in their stability periods but who did not qualify for coverage based on their hours worked during the associated measurement period. Additionally, the (b) penalty cannot be more than the (a) penalty would have been had it applied.

Summary and Employer Action Items

The bottom line is this:

If you hire a non-seasonal employee whom you reasonably expect (at date of hire) to work at least 30 hours/week or 130 hours/month, you must track hours each calendar month and offer benefits by the first day of the fourth month if the employee averages at least 130 hours/month for the first three months. This applies even if you hire this employee for a short-term position or a summer internship (unless you take the position, upon advice from your legal counsel, that a summer intern is a “seasonal” employee).

If you hire a non-seasonal employee and you cannot reasonably determine at date of hire if they will work on average at least 30 hours/week (130 hours/month), you can track their hours over their “initial measurement period” and not offer benefits until the associated “stability period,” if the employee averaged at least 130 hours/ month during the measurement period. The stability period might not begin until 13-14 months after the date of hire.

If you hire an employee who meets the new definition of a “seasonal employee,” you can track their hours over their “initial measurement period” and not offer benefits until the associated “stability period” if they averaged at least 130 hours/month during the initial measurement period. You do not have to offer benefits by the first day of the fourth month.

A copy of the final regulations can be obtained by clicking on the link below:

Sign up for latest news updates. Please contact us for immediate information on how to implement these initiatives for your group-specific needs at info@medicalsolutionscorp.com or Call (855) 667-4621.

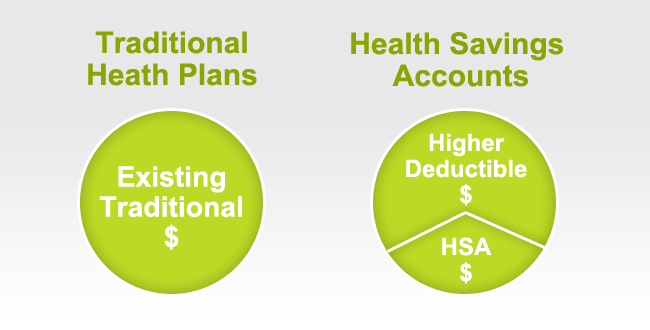

HDHP Minimum Annual Deductible (No change from calendar year 2011):

Single – $1,300 (up from $1,250 in 2014)

Family – $2,600 (up from $2,500 in 2014)

HDHP Out-of-Pocket Maximum:

Single – $6,450 (up from $6,350 in 2014)

Family – $12,900 (up from $12,900 in 2014)

HSA/HDHP Market Growth

HSA holders own the assets in the accounts and can build up substantial sums over time. Enrollment in HSA-compatible insurance plans has increased to 10 million earlier this year, from 1 million in March 2005, according to, America’s Health Insurance Plans (AHIP), a trade group.

HSAs were authorized starting in January 2004. Since then, AHIP has conducted a periodic census of health plans participating in the HSA/HDHP market.

The number of people with HSA/HDHP coverage rose to more than 11.4 in January 2011, up from 10.0 million in January 2010, 8.0 million in January 2009, and 6.1 million in January 2008.

30 percent of individuals covered by an HSA plan were in the small group market, 50 percent were in the large-group market, and the remaining 20 percent were in the individual market.

14% of all workers in the private sector that have access to a Health Savings Account acc. to Bureau of Labor Statistics.

States with the highest levels of HSA/HDHP enrollment were California, Ohio, Florida, Texas, Illinois and Minnesota.

HSA Advantages:

Opportunity to build savings – Unused money stays in your account from year to year and earns tax-free interest. The HSA also gives you an investment opportunity.

Tax-free contributions and earnings – You don’t pay taxes on contributions or earnings.

Tax Free Money allowed for non traditional Medical coverage– As per IRS Publication 502, unused moneys can be used for dental,vision, lasik eye surgery, acupuncture, yoga, infertility etc. Popular Examples

Portability – The funds belong to you, so you keep the funds if you change jobs or retire.

Our overall experience with HSAs have been positive when employer funding is at minimum 50% using either the HSA or an HRA (Health Reimbursement Account-employer keeps unspent money). Traditional plans trend of higher copays and new in network deductibles has also led to the popularity of an HSA.

Is your HSA compliant? Which pre-tax qualified HSA, FSA, HRA spending card is right is right for you? Please contact our team at Millennium Medical Solutions Corp (855)667-4621 for immediate answers.. Stay tuned for updates as more information gets released. Sign up for latest news updates.

(Note that a health plan will not fail to qualify as a high deductible health plan merely because it provides certain preventive health services without a deductible, as required under Health Care Reform.)

Congratulations – you just signed up successfully for Obamacare! You made it right before the March 31st deadline and avoided the individual penalty and getting blocked out for 2014. Don’t relax just yet. If you’re one of the many people who applied on the first open enrollment it’s smart to expect some bumps over the next few weeks. Shifting deadlines and technical glitches have left many insurance companies scrambling to catch up to the flood of requests. To make sure you start things right, here are some easy ways to stay vigilant:

Pay the premium –Until you pay for the plan you do not truly have a plan just yet. Some states and insurance companies have extended the deadline to pay, but its best to do this as soon as possible. For maximum peace of mind, get written confirmation from your new insurance company. If you go to the doctor before you pay your premium, you may end up footing that medical bill if the insurance company doesn’t have a record of your premium payment.

Member ID Cards –in about 1–2 weeks after you receive your first bill you will receive your Member ID card from your carrier after you’ve made your first premium payment. This is the card you’ll share with medical providers and pharmacies when you receive service. Your carrier may allow you to print a temporary ID card if you need care prior to receiving your Member ID card(s). Your insurance card will (hopefully) arrive in your mailbox in early January. You’ll present it wherever you need services: at the pharmacy, doctor’s office or hospital. Since insurance companies had a very short turnaround time to process new members, you may see a delay. Don’t panic! Go to the insurance company’s website to see if you can print a temporary ID card. (This is a lifesaver!) If you turn up empty, call the company’s customer service number to confirm that you are in their system as an enrolled member.

Don’t rush to the doctors – If you have an immediate need for a prescription or an appointment, by all means take care of it asap. But if you can, wait a few weeks before scheduling your doctor’s visit. This will give time for the insurance companies and doctors to update their systems with all the new plans and enrollees. This way, you help ensure that the medical claim for your doctor’s visit will be processed accurately – and that you dodge some of the early-stage craziness.

Double check – that your doctor is in your new plan’s network . Most of the new insurance plans also came with new provider networks. Its smart to double check that your favorite doctor is in the network for the exact plan you just enrolled in. There are specific networks for different insurance products, so make sure you are checking the right one. If your doctor is not in the network, keep in mind that you may have to pay significantly more money to see an out-of-network doctor, so you may consider switching. See States Pushing Back Against Smaller Networks

Keep records – Keep a record of your payments, calls, emails with your insurance company and physicians. Just in case of a technical glitch in the insurance or doctor’s computer systems, you can show evidence of your payment or confirmations from your insurance company.

Obamacare 2014 Deadline Nearing. You are now more knowledgable than most after reading this article. Given all the new changes thanks to the new insurance plans, new enrollees, and changing deadlines, being aware of these simple tips will help you avoid unnecessary headaches. And remember, if you are still shopping for insurance, you only have until March 31st to enroll in a plan.

For enrollment help before the deadline information please contact our team at Millennium Medical Solutions Corp (855)667-4621. We have Spanish, Russian, and Hebrew speakers available. Quotes can also be viewed on our site.

HSA holders own the assets in the accounts and can build up substantial sums over time. Enrollment in HSA-compatible insurance plans has increased to 10 million earlier this year, from 1 million in March 2005, according to, America’s Health Insurance Plans (AHIP), a trade group.

HSAs were authorized starting in January 2004. Since then, AHIP has conducted a periodic census of health plans participating in the HSA/HDHP market.

The number of people with HSA/HDHP coverage rose to more than 11.4 in January 2011, up from 10.0 million in January 2010, 8.0 million in January 2009, and 6.1 million in January 2008.

30 percent of individuals covered by an HSA plan were in the small group market, 50 percent were in the large-group market, and the remaining 20 percent were in the individual market.

14% of all workers in the private sector that have access to a Health Savings Account acc. to Bureau of Labor Statistics.

States with the highest levels of HSA/HDHP enrollment were California, Ohio, Florida, Texas, Illinois and Minnesota.

HSA Advantages:

Opportunity to build savings – Unused money stays in your account from year to year and earns tax-free interest. The HSA also gives you an investment opportunity.

Tax-free contributions and earnings – You don’t pay taxes on contributions or earnings.

Tax Free Money allowed for non traditional Medical coverage– As per IRS Publication 502, unused moneys can be used for dental,vision, lasik eye surgery, acupuncture, yoga, infertility etc. Popular Examples

Portability – The funds belong to you, so you keep the funds if you change jobs or retire.

Our overall experience with HSAs have been positive when employer funding is at minimum 50% using either the HSA or an HRA (Health Reimbursement Account-employer keeps unspent money). Traditional plans trend of higher copays and new in network deductibles has also led to the popularity of an HSA.

Is your HSA compliant? Which pre-tax qualified HSA, FSA, HRA spending card is right is right for you ? Please contact our team at Millennium Medical Solutions Corp (855)667-4621 for immediate answers.. Stay tuned for updates as more information gets released. Sign up for latest news updates.

The New FSA Carry Over. U.S. loosens FSA rules and will allow a carry over of up to $500 to the next year. The use-it-or-lose-it rule scared off many workers, with just 25 percent of eligible workers participating in healthcare FSAs.

According to a WSJ article “Consumers Can Roll Over $500 in an FSA”, about 14 million families use FSA accounts and the new plan would be a welcome relief for them. That’s because until now any unused funds used to go the employer, so people were forced to use up the funds, especially toward the end of the year by spending on frivolous things. Moreover, many were fearful of signing up, lest they lose any unused amount.

The most recent prior change to FSA this year was a limit of $2,500 that a worker can set aside.

The health care Flexible Savings Account (FSA) can reimburse you or help you pay for eligible health care expenses not covered by your health plan. The portion of your paycheck you put into your FSA is taken out before you pay federal income taxes, Social Security taxes and most state taxes. It’s a great way to save money.

Generally, contributions you make to your FSA are not subject to federal income taxes or social security taxes. In most instances, there are no state taxes taken out either. The amount you may save depends upon:

The amount you put into your FSA

The tax percentage you would normally pay on that money (tax bracket)

Let’s say you want $2,000 taken out of your paycheck this year to put into your FSA. The money you direct to your FSA is taken out of your check before taxes are taken out. That reduces your taxable income by $2,000.

Let’s say you normally pay 30 percent in federal, social security and state taxes on your income. In this example, you would enjoy a tax savings of 30 percent of the $2,000. In other words, you could get a $600 tax savings on the $2,000 you directed to your FSA.

This example should not be taken as tax advice. See a tax advisor to seek the best advice for your situation. To see how much you may save, check out Aetna’s FSA Savings Calculator.

Is your FSA compliant? Which pre-tax qualified HSA, FSA, HRA spending card is right is right for you ? Please contact our team at Millennium Medical Solutions Corp (855)667-4621 for immediate answers.. Stay tuned for updates as more information gets released. Sign up for latest news updates.

Obamacare Simplified Using Youtoon by Kaiser is just what the Doctor ordered. With less than 60 days to go to the October 1, 2013 Health Exchanges Open Enrollment Period what better way to ease the confusion than a 7 minute cartoon?

CMS maintains the HealthCare.gov website, and this is where individuals can find more information on health insurance exchanges, the enrollment for which begins on October 1, 2013. Depending on which state individuals reside in, one may be able to enroll in an exchange plan, or may be directed to their state’s own exchange enrollment site. Employers can also use this site to learn about the Small Business Health Options Program (SHOP) which can help them provide coverage for employees.

Several resources have been made available to help people weed through the information and to make you aware of what requirements and deadlines apply to you. The Kaiser Family Foundation (KFF) brought some levity to the topic by creating an animated video explaining the upcoming changes in health coverage under the ACA. Narrated by Charlie Gibson, “The YouToons Get Ready for Obamacare,” explains what is and isn’t changing under the law and is posted on the KFF site, along with other resources on the topic. KFF President, Drew Altman, was quoted as saying, ’[t]his cartoon is meant to demystify a complex law and explain what it means for you, whether you support or oppose Obamacare.”

For a comparison and additional questions on which Exchange – Individual or SHOP Exchanges is right for you please contact our team at Millennium Medical Solutions Corp. Stay tuned for updates as more information gets released. We’re inside of 45 days until exchanges open, and information will be coming quickly in the next few months. Sign up for latest news updates.

Breaking Westchester Health Care News: As reported in The Journal News earlier. A Stellaris Hospitals Break Up is planned; Phelps, Lawrence, Northern Westchester and White Plains may form new alliances. Stellaris had been in the news in recent years with down to the wite negotiations with Empire Blue Cross Empire & Stellaris Reach Pact effective 8/1/10.

A Stellaris Hospitals Break Up is not surprising. This is viewed as possible strategic move for acquisition form larger local hospitals or even national chains such as Cardinal Health or HCA. Insurers have also purchaszed recenlty medical groups,see UnitedHealthcare Buying Medical Groups? Will it our market allow an Insurer to purchase a Hospital?

4 hospitals seek to cut Stellaris ties

By Jane Lerner

Four hospitals in Westchester County want to cut ties with their parent organization — a move that could signal their interest in forming new consolidations and alliances with other health-care facilities.

Phelps Memorial Hospital Center in Sleepy Hollow, Lawrence Hospital Center in Bronxville, Northern Westchester Hospital in Mount Kisco and White Plains Hospital are seeking to leave the Stellaris Health Network.

“Stellaris and its member hospitals made this decision after a lengthy strategic review that evaluated a variety of alternatives to respond to a dynamic and ever more challenging health-care environment,” Stellaris said in a statement.

The state Department of Health has to approve any change in ownership of a hospital. Requests from the four hospitals to “dis-establish” Stellaris as “active parent and co-operator” were filed with the state last week.

Leaving Stellaris will enable each hospital to seek new partners.

“By becoming independent, each hospital can move forward in the direction that each feels is best for its community,” said Arthur Nizza, who is on his way out as president and chief executive officer of Stellaris.

All four hospitals declined to comment.

As the parent organization of the four hospitals, Armonk-based Stellaris handled their negotiations with commercial insurance companies, purchasing and information technologies.

Stellaris will continue to provide IT support and some other services to the hospitals. But once they leave the network, they will be able to seek new partners to increase their bargaining power and share services and expenses.

Numerous hospital consolidations and mergers are taking place nationwide.

“I think in time — not immediately — the idea of a freestanding community hospital is going to be passe,” said Kevin Dahill, president of the Northern Metropolitan Hospital Association, an industry group.

Sound Shore Medical Center in New Rochelle and its Mount Vernon Hospital are seeking to merge with Montefiore Medical Center in the Bronx once the Westchester County institutions emerge from Bankruptcy Court. In New York City, Mount Sinai Medical Center and Continuum Health Partners, a network that includes Beth Israel and two St. Luke’s-Roosevelt campuses, agreed last week to merge.

“Hospitals are doing what they have to do to position their organizations,” Dahill said.

Stellaris was formed in 1996 as an alliance between White Plains and Northern Westchester hospitals. In 1997, Phelps and Lawrence joined and, in 2000, the company formed an emergency medical service to provide paramedic service to part of Westchester.

Nizza will become CEO of St. Francis Hospital and Health Centers in Poughkeepsie next month. Sharon Lucian, who has been with Stellaris since 1999 and is vice president and chief financial officer, will replace him.