Obamacare Midsize Employer Mandate Delayed Till 2016.

For small businesses employing 50-99 the Treasury Dept is not requiring compliance of the Employer Mandate until 2016. Companies with 100 workers or more could avoid penalties in 2015 if they showed they were offering coverage to at least 70 percent of their full-time workers, the Treasury said.

The large group employer mandate had been originally delayed until 2015 in July 2013 see- Obamacare Employer Mandate Delayed, More Guidance. Employers with the equivalent of 50 full-time workers or more had to originally offer coverage or pay a penalty starting at $2,000 per worker beginning in 2014.

Employers with 100 or more full-time employers will have to comply with the Internal Revenue Code Section 4980H “play or pay” provision Jan. 1, 2015. Companies with 100 workers or more could avoid penalties in 2015 if they showed they were offering coverage to at least 70 percent of their full-time workers, the Treasury said.

Under the new rules, companies would be allowed during the phasing-in year to offer coverage specifically to a subset of employees, such as those working 35 hours or more a week, the Treasury said.

Treasury also set new rules for how the requirement would apply to workers such as volunteers and seasonal employees, saying that employers wouldn’t be penalized for failing to offer those people coverage, regardless of the number of hours they were working. Teachers, however, wouldn’t be considered part-time workers even if they were away over the summer, and adjunct faculty would have a special arrangement for how their classroom hours should be counted.

The penalty the employer pays would be based on the number of full-time workers that the employer employs. For purposes of calculating the penalty, the employer would not have to include part-time and seasonal workers in the calculations. Under PPACA, only workers who are not offered group health coverage are eligible to apply for exchange coverage.

The coverage must encompass a core set of benefits and be affordable – which the law defines as premiums costing no more than 9.5 percent of an employee’s income – and the employer must pay for the equivalent of 60 percent of the cost of coverage for workers but not their dependents.

As reported in Washington Post: “Administration officials said that organizations with a large number of volunteer employees – such as firefighters and first responders – would not have to provide coverage, along with those hiring seasonal employers who work six months or less in a given year. Teachers will not be considered part-time just because they do not work for three months during the summer, officials added, while the status of adjunct faculty will be calculated on a formula where they would receive credit for 2¼ hours of service per week for each hour they spent teaching or in the classroom.”

Many Employers are asking for flexibilities of defining FT as higher than 30 hours. The law has already had unintended consequences with shift in employment hours especially in industries such as dining, entertainment, services and construction.

Other transitional relief contained in the regulations include:

For employers with between 50 and 99 employees, the employer mandate is delayed until 2016. Note that an employer must provide a certification to take advantage of this relief.

Employees in positions for which the customary annual employment is six months or less generally will be considered seasonal employees and not full-time employees.

When employers are first subject to the employer mandate, they can determine whether they had at least 100 full-time employees in the previous year by referencing a period of six consecutive months, rather than an entire year.

For purposes of determining coverage in 2015 only, employers may use a measurement period (the period used to determine whether a variable-hour employee is a full-time employee) of six months, with respect to a stability period (the period following the measurement period, during which the variable-hour employee must be offered coverage) of up to 12 months.

Employers with non-calendar year plans must comply with the employer mandate at the start of their 2015 plan year, rather than on January 1, 2015.

For more information regarding both Exchanges – Individual Exchanges or SHOP please contact our team at Millennium Medical Solutions Corp (855)667-4621. We work in coordination with Navigators to assist with medicaid, CHIP Child Health Plus, Family Health Plus and Medicare Dual Eligibles. We have Spanish, Russian, and Hebrew speakers available. Quotes can also be viewed on our site.

In an unexpected announcement pre-July 4th the big news was Obamacare Employer Mandate Delayed with penalties under the Affordable Care Act (ACA) until 2015. The mandate also known as the “Employer Shared Responsibility” requires employers with 50 or more FTEs to offer affordable health insurance coverage to their workers or face financial penalties for not doing so. Those penalties would originally have been applied beginning in 2014.

There has been a follow up guidance issued last week July 9th by the IRS. According to the IRS, the delay will give employers more time to prepare for the change in how health insurance is provided and will also give the Obama Administration time to simplify the insurance-related reporting requirements that employers face. This transition relief appears to come with “no strings attached.” Although the IRS guidance encourages employers to voluntarily comply with the employer mandate and maintain or expand health care coverage in 2014, the IRS will not impose penalties for a failure to do so.

Although the IRS guidance encourages employers to voluntarily comply with the employer mandate and maintain or expand health care coverage in 2014, the IRS will not impose penalties for a failure to do so.Notably, the guidance issued on July 9th also does not require employers to make “good faith” efforts to comply. As a result of this transition year, employers will have the option of deciding to what extent (if any) they will continue efforts to comply with the employer mandate during 2014.

Employers who intended to rely on one of the transition rules previously announced for 2014 should keep in mind that the latest IRS guidance does not provide special transition rules for 2015. Other group health plan requuirements still apply as discussed in our prior blog Essential Health Benefits Not Delayed.

This means that for plan years beginning on and after January 1, 2014, all group health plans must:

Eliminate all pre-existing condition exclusions (regardless of age);

Maximum Cost Sharing Deductible to $2,000/individual ($4,000/family); limit in-network out-of-pocket maximums to $6,350/individual ($12,700/family)

Individual Mandate Still Applies. individuals will still be required to obtain health care coverage or pay a penalty for each month they do not have coverage, beginning January 1, 2014

Exchanges (Marketplaces) Open for Enrollment October 1, 2013.

The IRS notice makes it clear that individuals who enroll in coverage on the marketplaces will continue to be eligible for a premium tax credit if their household income is within a specified range and they are not eligible for other minimum essential coverage.

Employers Must Send Notice of Exchanges (Marketplaces) Before October 1, 2013. These notices must be sent to current employees by October 1, 2013. Then, beginning October 1, 2013, employers must send this notice to new hires within 14 days of their start date.

New taxes still apply – Patient Centered Outcomes Research Institute (PCORI) excise taxes and transitional reinsurance program fees;HRA/HSA/FSA clients also pay a monthly $1/employee tax.

We will continue to monitor ACA developments and will provide you relevant updated information when available. In the meantime, please visit to view past blogs and Legislative Alerts at https://360peo.com/feed.

Obama administration announced that the employer shared responsibility mandate also known as “Pay or Play” aspect of the Patient Protection and Affordable Care Act (PPACA) will be delayed by one year.

This mandate requires businesses with 50 or more workers to provide health insurance coverage to employees. As a result, the administration will start enforcing the mandate in 2015, rather than January 1, 2014, in an effort to give businesses more time to prepare.

There will be additional changes tied to this delay, and the administration has stated that they will provide formal guidance within the next week.

More details will be available for our July 11th WebMeeting. Medical Solutions Corp is working with the various regulatory agencies to understand the specifics surrounding this ruling, and will continue to provide updates through Legislative Alerts and on our blog.

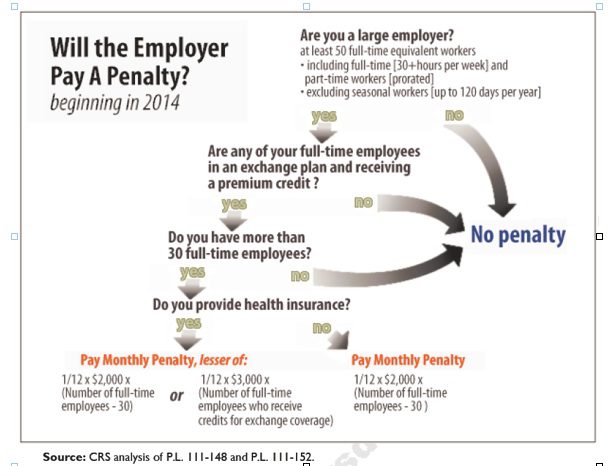

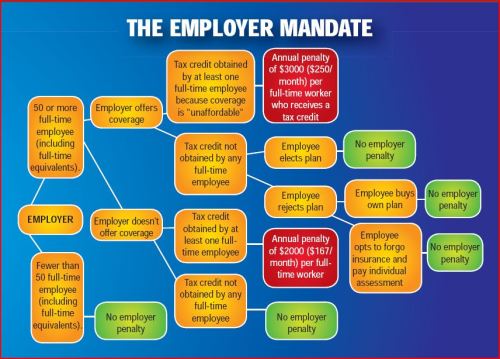

Larger employers that don’t offer minimum essential health coverage to full-time workers may face penalties under health care reform if any full-time employees receive a government premium credit or subsidy to buy their own insurance through an exchange.

The so-called employer mandate and the health insurance exchanges both go into effect in 2014 under the Patient Protection and Affordable Care Act.

The penalties generally apply to all employers with 50 or more full-time equivalent employees. An employer with at least 50 FTEs that provides access to coverage but fails to meet certain requirements, outlined below, may also be subject to a penalty.

To determine the FTE (Full Time Equivalent) you must count FT and PT employees. Full Time Employees are those working 30 hours+/week. See blog post “What does FTE mean?”

Affordability of the employer plan remains a consideration, however, since just one employee qualifying for federal premium assistance for exchange coverage will trigger a penalty for employers with 50 or more employees

Minimum essential coverage generally includes any coverage offered in the small or large group markets. Excepted benefits, such as limited-scope dental or vision offered under a separate policy, certificate or contract of insurance and Medicare supplemental plans, do not qualify.

Penalties explained

Starting in 2014, large employers that don’t offer coverage face a penalty of $2,000 per full-time employee (excluding the first 30) if at least one FTE receives a government subsidy to buy coverage on an exchange. This is sometimes referred to as the “play or pay” penalty.

Employers that offer coverage to employees may still face a “free rider” penalty if the coverage offered is deemed unaffordable or low in value.

If an employer offers coverage, but a full-time employee receives a premium credit subsidy through an exchange, the employer must pay an assessment equal to the lesser of:

$3,000 for each employee that receives a subsidy

$2,000 for each full-time employee after the first 30

The monetary penalties listed above are annual figures and may be pro-rated to the number of months for which the penalty applies.

Who’s eligible for a subsidy?

Employees who are offered coverage from their employer could be eligible for subsidies on the exchange if they don’t qualify for Medicaid or other programs, are not enrolled in their employer’s coverage and meet either of the following conditions:

The employee’s share of the premium exceeds 9.5 percent of their household income

The plan pays for less than 60 percent on average of covered health care expenses (e.g. coverage offered does not have at least a 60-percent actuarial value).

After 2014, penalty amounts are indexed by a premium adjustment percentage for the calendar year.

The Congressional Budget Office expects the penalties to generate $52 billion toward the overall cost of health reform by 2019. The Department of Health and Human Services estimates that fewer than 2 percent of large American employers will have to pay the assessments.

Disclaimer: This blog is not intended to represent legal advise and one should consult with a tax and/or legal expert.

By the end of January every year, employers must provide their employees with form 1005-B or 1095-C as applicable. Employees will need them while validating to the IRS and health exchanges of the type and cost of coverage they were offered and maintained. If employers miss the deadline by less than 30 days late on their delivery, the penalty is $50 per form. After the 30 days, employers will be penalized $250 per formthat was not distributed to the employees.

3. Form filing to the IRS

By the end of Marchevery year, employers must submit forms 1094 and 1095 to the IRS. If employers miss the deadline to file, they will be penalized $250 per form.

4. ‘A’ Penalties

If the employer fails to offer compliant coverage they must indicate so on the 1094-C forms. The IRS will automatically calculate ‘A’ penalties due by the employer of $2,160 per employee per year(adjusts annually for inflation). The IRS will make their calculations from the information submitted in Section III of form and issue penalty letters to employers due for immediate payment.

5. ‘B’ Penalties

Employers will be receiving letters from the federal and state health insurance exchanges in regards to employees of theirs who went to these various exchanges, purchased coverage and received a premium subsidy. The combination of an employee purchasing coverage from an exchange and receiving a subsidy is the necessary element to trigger a ‘B’ penalty of $3,240(adjusts annually for inflation).

For more information on compliance please contact our team at Millennium Medical Solutions Corp (855)667-4621.

NYC become the 3rd U.S. City to require Employer Transit Benefits following SF and Washington, DC. Beginning in 2016, the ordinance will require employers (not including government employers) with 20 or more full-time employees in New York City to provide full-time employees a pre-tax qualified transportation benefit program (excluding parking subsidies). It would mean that an estimated 450,000 more New York City-based employees will have access to the commuter tax break. That’s in addition to the 700,000 who already get the break.

“The ordinance will require private employers with 20 or more full-time employees in New York City to provide a pretax qualified transportation benefit program for their full-time employees.” For purposes of the ordinance, a full-time employee is one who works 30 or more hours per week.

Penalties:

While the new ordinance goes into effect January 1, 2016, it provides a six-month grace period, so penalties will not begin until July 1, 2016. Penalties for a first violation will range from $100 to $250. If an employer corrects the violation within 90 days of being notified, then penalties will be waived. If correction (the steps for which have not yet been described) does not occur, penalties for the first violation will apply and an additional penalty will apply, equal to $250 for each 30-day period in which the employer continues to fail to offer the required benefits.

Tax Savings:

The way the pretax commuter tax break works is employees exclude their transit commuting costs from their taxable wages up to the $130 monthly limit (there’s a separate $250 monthly limit for parking). If you’re in the 40% combined federal and state bracket and you put away $130 a month pretax salary to use for transit, you save $624 a year. This also saves the employer money because the employer doesn’t pay payroll taxes of 7.65% on every dollar set aside by employees pre-tax.

$130 transit maximum NEW $255 transit maximum for 2016

EE Savings @ 40% tax bracket = $1200/year

ER Savings (FICA) = $230/year

$255 parking maximum

EE Savings @ 40% tax bracket = $1,200/year

ER Savings (FICA) = $230/year

Next Step:

If you want your employer to add commuter benefits—so you’re eligible for the tax break–petition your HR department, and specifically ask for the pretax commuter benefits program (why wait until 2016?). To learn more about the NYC Transit Mandate, please visit the official website of the City of New York. To start a Transit benefit within 24 hours contact us today (855) 667-4621 or info@medicalsolutionscorp.com.

No discrimination in favor of highly compensated individuals – awaiting further guidance and definitions

Health plan claim and appeals protections

Patient protections, including the selection of primary care provider, coverage of emergency services, and access to pediatric, obstetrical and gynecological care providers

Importantly, the excise tax will not be assessed if an employer can demonstrate that it did not know, and exercising reasonable diligence would not have known, of a violation. Further, the excise tax will not be assessed if the failure is due to reasonable cause and not willful neglect and it is corrected within the 30-day period beginning on the first date an employer knows, or exercising reasonable diligence would have known, that the failure existed. This limited correction window makes identifying and promptly correcting any potential errors of utmost importance.

For more information on compliance please contact our team at Millennium Medical Solutions Corp (855)667-4621.

With only 6 month away from full implementation of 2014 Patient Protection Affordability Care Act (PPACA) employers are understandably uncertain. Below are Health Care reform – five things employers can do now to prepare and take action.

UPDATE JULY 2nd: Since blog posting the President Administration has delayed 1 year Employed Shared Responsibility Mandate i.e. Pay or Play to Jan 2015.

1. Employee Communications

Employers must notify employees of the online insurance marketplace known as a Healthcare Exchange. Recently released federal guidelines require employers to notify their workers of eligibility requirements for their state exchange starting Oct. 1, 2013 Open Enrollments for Jan 2014 effective date. To the relief of many, the U.S. Labor Department also provided model notices that employers can give to their workers, which eliminates the need to develop their own notifications.

Additionally, Employers sponsoring a health plan must give employees a Summary of Benefits and Coverage (SBC). The purpose of the Summary of Benefits and Coverage, or SBC, is to present benefits and coverage information in clear language and in a consistent format. Inspired by the Nutrition Facts Label on packaged food, theSBC (pdf) includes two medical scenarios: having a baby and managing Type II diabetes. It estimates how much a patient would pay for medical care in each scenario with specific insurance plans.

It’s the employer’s responsibility to distribute the SBCs to employees.

This requirement applies to health plan renewals after Sept. 23, 2012.

Department of Labor will NOT impose penalties for non-compliance with the SBC notice during the first year as long as employers show a “good faith” effort to comply. Read the FAQ on SBC and ACA pdf here.

2. Determining which Employers must offer health care.

Because employers with 50 full-time equivalents face penalties for not providing affordable, minimum value insurance an employer should know whether it is subject to these requirements or not. Common law employees of the employer and any commonly controlled company must be counted. Employers with temporary or leased employees will want to discuss with their advisors whether these employees will be considered “common law employees” for purposes of determining how many FTEs an employer has. Employers with employees who are paid based on unique payment models (stipends, work product, etc) will want to discuss how to calculate these employee hours with their benefits advisors.

Employers with 50 or more employees will incur penalties of up to $2,000 per employee if they cancel their existing health care program (which up until 2014 would be considered an optional benefit to provide). They will also incur penalties if their plan is too costly, and they do not meet the affordability standards.

Employers with less than 50 employees will not incur penalties if they cancel their health care plan, and that decision will need to be made on a business by business basis. They can also choose to offer partial coverage and contribute up to the minimum 50% of single coverage not to exceed 9.5% employee

The good news is Employers can subtract 30 FT employees. This portion is known as the Employer “play or pay” option. Specific case example and details are found at Pay or Play Employer Guide.

To encourage businesses to offer health benefits to their employees, the federal government is offering tax credits to small businesses. These credits are available to an estimated 4 million small businesses, including nonprofits.The IRS has set up a web page with information: Small Business Health Care Tax Credit for Small Employers. The maximum “credit” (which offsets taxes dollar for dollar and is better than a “deduction” which reduces taxable income) is 35 percent of the amount an employer pays towards employee health insurance.

Who’s eligible?

To qualify, small employers must:

Have fewer than the equivalent of 25 full-time workers

Pay average annual wages below $50,000

Cover at least 50% of the cost of health care coverage for their workers

Because of the high wages paid in most industries in NY/NJ/CT Tri State, few small employers that provide coverage pay such a low average wage. Note, however, that the calculation of average wages and number of employees excludes the wages of an owner and his or her family members.

medicalsolutionscorp.com help clients gather the appropriate information and do a preliminary estimate of the credit amount. This information will help you and your accountant determine whether applying for the credit makes financial sense. Find out what the new tax credit could mean for your coverage. Call us at 855-667-4621.

4. Determine affordability

Beginning Jan. 1, 2014, an employer with 50 or more employees must pay a tax penalty if they either: a) Do not provide health insurance with minimum benefits or 60 percent of healthcare expenses; b) Require employees to contribute more than 9.5 percent of an employee’s household income for the health insurance and those employees obtain a government subsidy for coverage.

Companies will be required to pay $3,000 per employee without affordable coverage. (Note: there are a number of caveats that might affect the actual penalty paid, so consult your tax advisor.)

It is crucial to Understand the difference between FT and Full Time Equivalent. To determine the FTE (Full Time Equivalent) you must count FT and PT employees. Full Time Employees are those working 30 hours+/week.* The number of full-time employees excludes those full-time seasonal employees who work for less than 120 days during the year.4 The hours worked by part-time employees (i.e., those working less than 30 hours per week) are included in the calculation of a large employer, on a monthly basis, by taking their total number of monthly hours worked divided by 120.

For example, a firm has 35 full-time employees (30+ hours). In addition, the firm has 20 part time employees who all work 24 hours per week (96 hours per month). These part-time employees’ hours would be treated as equivalent to 16 full-time employees, based on the following calculation:

20 employees x 96 hours / 120 = 1920 / 120 = 16

Thus, in this example, the firm would be considered a “large employer,” based on a total full-time equivalent count of 51—that is, 35 full-time employees plus 16 full-time equivalents based on part-time hours.

In the coming months, Millennium Medical Solutions Inc will host seminars and will share information you’ll need to know as the countdown continues to October 1st.

Error: Contact form not found.

This blog is not intended to represent legal advise and one should consult with a tax and/or legal expert.

* IRC 4980H(c)(4)

Disclaimer: This blog is not intended to represent legal advise and one should consult with a tax and/or legal expert.

Health Insurance Mandates 2012. The Councel for Affordable Health Insurance in VA released their annual “Health Insurance Mandates in the States” for 2012 last week. While NYS did not crack the top 5 they did come close at number 7 this year.

NYS Mandates were discussed in our posting Empire Leaving Small Groups Nov 2011. ” Today, we have so many State mandates that many of the mandates(overage dependents coverage, preventive care, pre-existing for kids) in PPACA didnt even affect NY since they were already in place. Mandates account for approx 17% of the costs of which Small Businesses pay more than fair share. Large corporations and Unions can self insure and avoid some mandates as they are governed by ERISA and not State. To the relief of of our struggling clients on subsidized Healthy NYthe State doesn’t play by their own rules and instead opts out of its very own mandates.”

According to the study CAHI Identifies 2,271 State Health Insurance Mandates “The sheer number of state mandates will make it difficult for states to deliver on one of the key promises repeatedly made by supporters of Obamacare: it would provide all Americans with affordable health coverage. The essential health benefit plan design was supposed to give states the flexibility to craft benefit packages which would be suitable and affordable for their unique populations. But HHS shackled the states to the full load of mandated benefits on their books, and the prices of next year’s offerings in the health insurance exchanges are going to bear witness to the free-wheeling mandate craze of the last twenty years. Recent studies have predicted double digit increases in health insurance premiums next year — the mandates are coming home to roost,” said Roy Ramthun, CAHI’s Director of Federal Affairs.”

The United Hospital Fun estimates that approximately 2.2 million New Yorkers lacked insurance coverage in 2009, (Health Insurance Coverage in New York 2009.)

The collective cost of paying for New York’s health insurance mandates equates to 12.2% of overall premium cost. Based on 2008 premiums, this translates into $1,538 expense per year for an average family policy and $566 per year for a single person policy. (Employer Alliance, NYS Mandated Health Insurance Benefits, 2003)

Higher health care costs increase the number of uninsured. In New York, it is estimated that for every 1% increase in premiums, 30,000 New Yorkers lose health insurance. (Barents Group, 1999)

Mandates have a cumulative impact on premium costs. It is estimated that the cost of the 12 most common mandates can increase the cost of health insurance by as much as 30%. (Milliman and Robertson 1996)

Rising health care costs have the biggest impact on the small business sector. For every 1% increase in premium costs, small business sponsorship of health insurance drops by 2.6%. (Morrisey et al., 1994)

The percentage of US small business workers receiving insurance through their employer declined 5% between 1996 and 1998 – from 52% in 1996 to 47% in 1998. (KPMG Peat Marwick, 1999)

Nearly one of every four uninsured Americans has no health care coverage as the direct result of state mandates. (Jensen, Morrisey, 1999)

Health insurance premiums for New York’s working families skyrocketed between 2000 & 2007 increasing by 80.7 percent. (Families versus Paychecks, Families USA 2008)

Since 1999, family premiums for employer-sponsored health coverage have increased by 131 percent, placing increasing cost burdens on employers and workers. (Kaiser Family Foundation and Health Research and Educational Trust. Employer Health Benefits 2009 Annual Survey. September 2009).

the HIT is actually a hidden tax on small business. PPACA assesses a tax on all health insurance companies based on their “net premiums” written. The tax will raise $8 billion starting in 2014, $14.3 billion in 2018 and more in later years. This is [aid for by fully insured health plans which are comprised mostly by small businesses.

Tick! tick! tick! As the 2014 Employer Mandate to either pay or play gets closer the nation’s employers move a step closer to having to make a decision: Do I play or pay? This Employer mandate under Patient Protection and Affordable Care Act (PPACA) does not apply to smaller groups under 50 FTE (full time equivalent) employees. Many small groups such as food service industry, retailers, construction etc. in fact have many FTE and while they may work minimal hours can trigger the “pay or play” mandate.

The IRS has released recently guidance published in the form of a Notice of Proposed Rulemaking (NPRM), addresses a number of issues tightly linked to an array of practical considerations related to the employer mandate. These include defining a “large employer,” determining “full-time” status for employees, clarifying the meaning of “dependents,” and determining what constitutes “affordable” coverage.

The guidance also tackles several stickier questions such as how and whether to count foreign or seasonal workers, as well as how to calculate the full-time status of employees who work unusual hours, such as teachers or airline pilots.

Three safe harbors relating to the provision of “affordable” coverage to employees in order to avoid exposure to the mandate penalties are also included in the guidance. Transition relief is offered in recognition of certain employers’ needing time to bring their plans into compliance.

Still, there are several regs that the IRS is awaiting commentary and resolution on due on March 18, 2013.

A Q&A summary of the rule has been released by the IRS and is available by clickinghere.

Some employers assert that the play-or-pay mandate will raise their costs and force them to make workforce cutbacks. As a result, a number are considering eliminating their health care coverage altogether and instead paying the penalty on their full-time employees. While the “pay” option might be worth considering, there are strong reasons why employers should look carefully at all of their options and do their best to calculate the actual outcomes of each.

Other Key Issues Addressed in the Proposed Rules Additional issues addressed in the proposed regulations include:

Determining which employers are subject to the “pay or play” requirements;

Determining who is a full-time employee, including approaches that can be used for employees who work variable hour schedules, seasonal employees, and teachers who have time off between school years;

Determining whether coverage is affordable and provides minimum value; and

Calculating the amount of the penalty due and how the penalty will be assessed.

When conducting a cost-benefit analysis, the key tax issues the employer should consider are:

Employer Tax Penalty for Not Offering “Qualified” Group Health

Not applicable for employers with less than 50 FTEs

$2,000 penalty per full-time employee (minus 30 employee credit)****

Employer Tax Penalty for Offering “Qualified” Health That is Not “Affordable”

Not applicable for employers with less than 50 FTEs

$3000 per employee receiving subsidy

Example:

Jungle Corp. has 100 full-time employees and is a leader in its market, using a talent differentiation strategy. Jungle’s family coverage costs $15,000, of which employees pay $3,000. Bob Smith, a highly skilled worker with a strong performance record, earns $50,000 and has family coverage through Jungle’s plan.

On Jan. 1, 2014, Jungle Corp. announces it is dropping its group health plan coverage and will instead pay the $2,000-per-full-time-employee penalty. On Jan. 2, Bob walks into HR and asks about receiving replacement compensation for the $12,000 that the business had been paying toward his family coverage.

Wanting to retain Bob in accordance with its strategy of maintaining market leadership with an experienced workforce, Jungle offers him another $12,000. But clever Bob points out that his share of Social Security and Medicare payroll (FICA) taxes will take a bite out of that $12,000, as will federal and state income taxes, so the HR manager agrees to make good on those amounts as well. Of course, the company will also have to pay its share of FICA taxes on Bob’s additional compensation. As a result, instead of paying $12,000 toward Bob’s family coverage using pre-tax dollars, Jungle Corp. now finds itself paying an additional:

Bob’s salary adjustment: $14,500

Employer’s share of FICA taxes: $1,109

Excise tax (penalty): $2,000 ———————————-

Total: $17,609 (versus $12,000 currently)

Similar per-employee costs will be reflected across the company’s workforce. A move that seemed like a no-brainer, the consequences could make you look silly.

For More Information Due to the complexity of the law in this area, and the absence of finalized guidance, employers are strongly advised to review their benefit plans to prepare for the changes ahead. Additional information regarding the penalty is featured on our Employer Shared Responsibilitypage.

In the coming months, Millennium Medical Solutions Inc will host seminars and will share information you’ll need to know as the countdown continues to October 1st. Please contact us for immediate information on how to implement these initiatives for your group-specific needs at info@medicalsolutionscorp.comor Call (855) 667-4621.