“The deadline for individuals and families to enroll in a qualified health plan through NY State of Health is February 15, 2015. However, the Marketplace will provide additional assistance to those individuals who have taken steps to apply for coverage but have been unable to complete the enrollment process before the deadline. All applications and enrollments in health plans must be completed by the end of the day on February 28, 2015. Those who complete their enrollment after February 15, 2015 but on or before February 28, 2015 will have coverage starting on April 1, 2015.”

2/12/15

Last days for 2015 Individual Open Enrollment is ending this week. This deadline applies to both On and Off Exchange!

If you’re wondering about the penalty for not having insurance: yes, there is one, and no, you can’t really get out of paying for it. You’ll pay the penalty when you file your taxes for 2015. Even if you get coverage midway through the year, you’ll still need to pay a penalty for the months you weren’t insured. So get covered!

Think you might be eligible for a subsidy or aren’t sure?

You can check here at the New York State of Health Marketplace calculator. If you are eligible or think you might be eligible, you can contact the marketplace directly to purchase a plan or ask questions about financial assistance.

Please remember that during open enrollment you are permitted to switch carriers. Choose wisely because after February 15, one cannot switch plans until open enrollment 2015, unless you have a “qualifying event,” such as marriage, divorce, birth or adoption.

Individual Online Enrollment Resources for On and Off Exchange:

For NYS – To view Oscar’s plans, rates and simple online enrollment application, click here.

For more information on enrollment please contact our team at Millennium Medical Solutions Corp (855)667-4621. We have Spanish, Russian, and Hebrew speakers available.

Last week, the Georgetown University’s Center on Health Insurance Reforms, in conjunction with the Urban Institute, released a report about the role health insurance agents and brokers have played enrolling and supporting millions of new people in coverage over the past year. The study, which is favorable about the role of the broker in the new health insurance marketplace, makes six policy recommendations that the authors believe would help agents assist even more consumers in the years ahead.

This study provides valuable academic evidence to the continued and future role health insurance agents have in helping support both individual and business consumers with their coverage needs in a reformed health insurance marketplace. Many of the recommendations the authors make are reforms that SMB have called for to better support agents and brokers in both the federal and state-based exchanges since day one.

The conclusive outcome is that Brokers will be needed as a sustainable model to support future enrollment. “Consequently, many may seek to leverage insurance brokers to conduct consumer education and help people enroll in marketplace plans. As evidenced here, sources interviewed have many concrete suggestions for increasing broker sales of marketplace plans, potentially increasing enrollment under the ACA. The amount that increased broker sales can reduce the number of uninsured.”

Reminder: 2015 Open Enrollment ends this week by Feb 15th. For more information regarding both Exchanges – Individual Exchanges or SHOP please contact our team at Millennium Medical Solutions Corp (855)667-4621. We have Spanish, Russian, and Hebrew speakers available. Quotes can also be viewed on our site.

What to do with the 1095-A form you received in the mail?

Attached below is the link to the web page with information on Premium Tax Credits and Form 1095-A. The resources on this link provide information on Form 1095-A, including Frequently Asked Questions and the toll free numbers provided for assistance.The resources on this page provide information about your Form 1095-A from NY State of Health. The Form 1095-A is used to reconcile Advance Premium Tax Credits (APTC) and to claim Premium Tax Credits (PTC) on your federal tax returns.

I didn’t apply to NY State of Health for financial assistance. Can you tell me if I can claim the PTC on my tax returns for 2014?

Who is in my tax family? How do I figure out if someone is a dependent?

How do I report health care coverage on my tax return?

How do I report the information from Form 1095-A on my tax return?

Do I need to complete Form 8962?

How do I complete Form 8962 on my tax return? How do I use the Form 1095-A to complete my Form 8962. What counts as income? What is my FPL?

Do I owe money to the IRS? Will I get a refund from the IRS? How much tax credits will I have to repay to the IRS? How much extra in tax credits will I get from the IRS?

I am self-employed. Can I claim my NY State of Health premiums as a business expense on my tax returns?

I had to pay back tax credits or got extra tax credits. Should I estimate my income differently for 2015?

How do I claim an exemption from the Individual Responsibility requirement?

Do I owe an Individual Share Responsibility Payment?

What income needs to be considered when calculating the Individual Shared Responsibility Payment?

I enrolled in a health plan with financial assistance and my income is now less than 100% FPL. Am I still eligible for the PTC?

If you have questions about Form 1095-A, Minimum Essential Coverage, PTC or the SLCSP table, call Community Health Advocates’ Helpline at 1-888-614-5400.

If you think we made a mistake on your 1095-A, call NY State of Health at 1-855-766-7860.

If you have questions about Form 8962 or other tax-related questions, visit www.irs.gov.

Please take the time to review. For more information, please

单击此处,了解 简体中文 保费税收抵免和 Form 1095-A 的相关信息。

Cliquez ici pour accéder à des informations sur les crédits d’impôt pour cotisation d’assurance et sur le Form 1095-A en français.

Klike la a pou jwenn enfòmasyon sou Kredi nan Taks sou Prim ak Form 1095-A nan Kreyòl Ayisyen.

Per ricevere maggiori informazioni in italiano sul credito d’imposta sul premio (Premium Tax Credit, PTC) e sul Form 1095-A, cliccare qui.

한국어로 된 보험료 세금 공제(Premium Tax Credits, PTA) 및 Form 1095-A에 대한 정보가 필요하신 경우 여기를 클릭하십시오.

Нажмите здесь, чтобы получить информацию о налоговых вычетах за страховые взносы и форме Form 1095-A на русском языке.

Haga clic aquí para obtener información en español acerca de los Créditos tributarios para la prima y el formulario 1095-A.

WestMed Medical Group has now joined the North Shore LIJ’s insurance – CareConnect Network! This is not a purchase. This partnership expands their footprint and makes CareConnect a compelling fit for individuals and groups located in Westchester. In addition, CareConnect has just announced CareConnect’s Network Expansion! Yale-New Haven Health and all their facilities are now in-network with CareConnect. Tools are available to search for providers with updated expansion to be added shortly.

A combined Hospital Insurance system is an intriguing concept thats not all that new. Pittsburgh’s UPMC has been delivering the same model in Western PA successfully. In NYS an integrated medical approach is new on the other hand and challenging in an open competitive loop. A high quality smaller network that is priced affordably and can offer Patient Concierge like service may be what the market is asking for. They may also be in a better position to manage patient health and Preventative Medicine. For Jan 2015, NSLIJ CareConnect will have a 20% reduction in most regions such as Westchester and NYC. For new rates, benefits and provider listings click – CareConnect NSLIJ

For more information, please

Press Release#

Award-Winning WESTMED Joins CareConnect!

We’re pleased to announce our continued network expansion with the addition of WESTMED Medical Group. With this practice, CareConnect members now have more access in Westchester County:

• 289 physicians in eleven office locations • On-site laboratory and radiology services • Four urgent care centers • Three NCQA recognized programs including the patient-centered medical home and diabetes Stay tuned as we continue to add access for your groups around the CareConnect service area

Phelps Memorial Hospital and North Shore LIJ Health System have signed an acquisition agreement. The two organizations expect the signed agreement to receive all necessary regulatory approvals later this year.

Phelps was one of two hospitals who signed a Letter of Intent this Summer. Northern Westchester Hospital based in Mt. Kisko was the second one. Both potential hospitals would give the fast growing NSLIJ insurance company CareConnect a string foothold in Westchester. Additionally, CareConnect has an affiliate agreement with Montefiore Hospital who’s Bronx base has expanded into Westchester with acquisition of New Rochelle Hospitals – Montefiore Buying Sound Shore Hospital as well as a partnership with White Plains Hospital –Montefiore Health System and White Plains Hospital Sign Formal Agreement.

It will invest in infrastructure improvements and clinical program expansion at Phelps. The 238-bed Sleepy Hollow facility will become the system’s 18th hospital. With Phelps’ 1,700 employees, NS-LIJ has about 50,000 workers, which it said ranks it as the largest private employer in New York state. North Shore-LIJ expects to secure regulatory approvals for the acquisition later this Fall.

A combined Hospital Insurance system is an intriguing concept thats not all that new. Pittsburgh’s UPMC has been delivering the same model in Western PA successfully. In NYS an integrated medical approach is new on the other hand and challenging in an open competitive loop. A high quality smaller network that is priced affordably and can offer Patient Concierge like service may be what the market is asking for. They may also be in a better position to manage patient health and Preventative Medicine. For Jan 2015, NSLIJ CareConnect will have a 20% reduction in most regions such as Westchester and NYC. For new rates, benefits and provider listings click – CareConnect NSLIJ

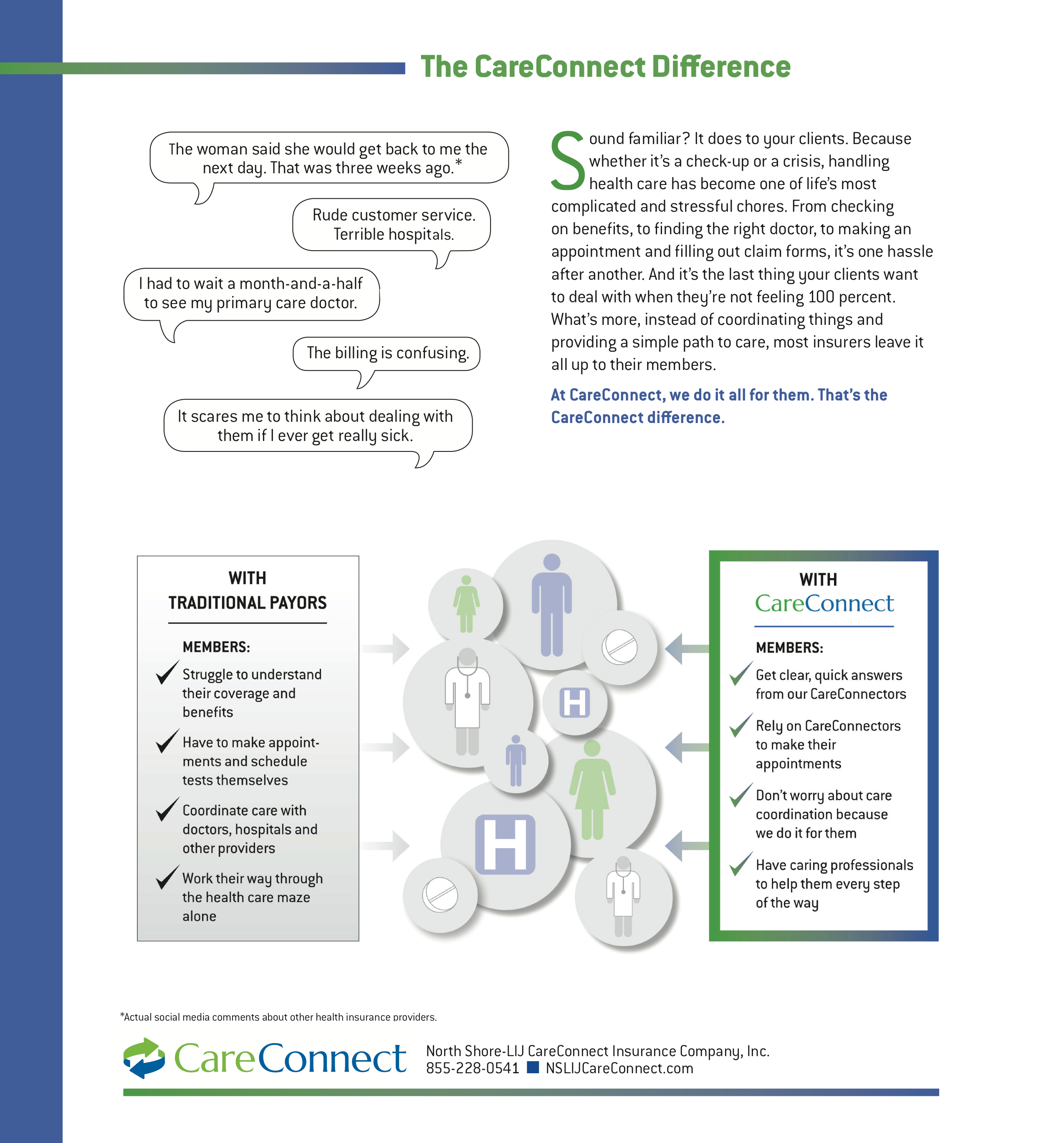

It’s not about a number … The North Shore-LIJ CareConnect network is built around the North Shore–LIJ Health System, its employed physicians and thousands of select affiliated community providers.

This network is designed to provide you access to the highest quality doctors, so choosing the right provider is worry free.

-17 hospitals, 8,000 providers, and an additional 12,000 contracted providers

-Future expansion includes network in northern NJ, Western CT, and Westchester.

-Partnership with CVS/MinuteClinic to provide basic care outside of the service area.

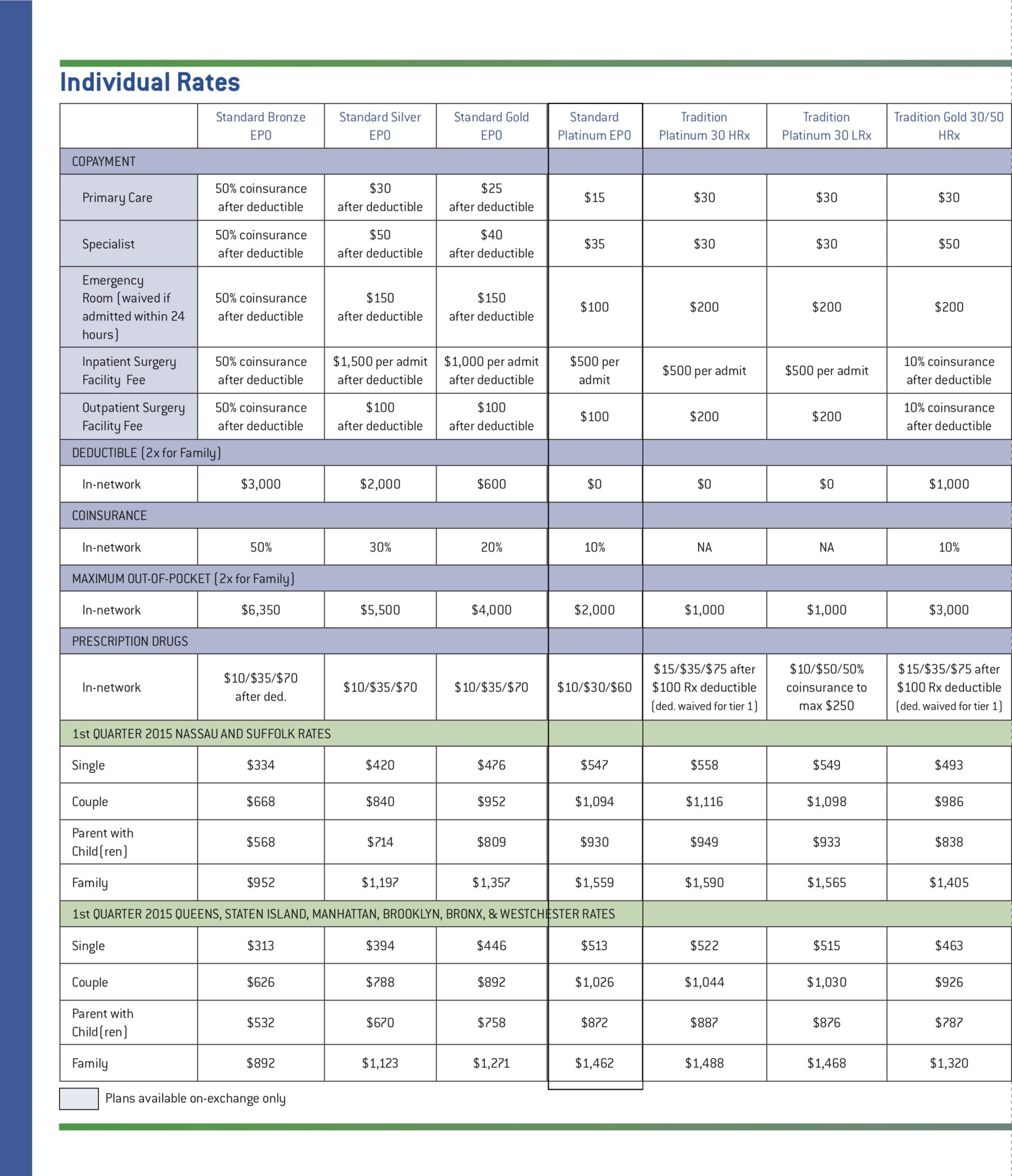

-New “Tradition” plans put the co-pay first, like we’re used to.

What makes CareConnect unique:

Concierge style service.

Call their customer support, speak with a real person empowered to help.

They’ll even find a doctor, and schedule an appointment, for a time that works for you.

Integrated care.

Low denial rate.

Integrated medical management.

Customer care centers for those who want to stop in and ask questions on their plan, their care, or even payment assistance.

OK so this may not be the catatonic movie of our favorite State starring Zach Braff and Natalie Portman but just the same Oxford couldn’t resist using the same logical name for the new network. Starting Sept 1, 2014 Oxford will be offering the Oxford Garden State Network on all size NJ group business. The 18,000 Doctor and 65 hospitals network will answer the call for a flexible lower cost plan option.

Judging by the #1 selling plan – Oxford Liberty HMO the market supports a smaller lower cost quality network. Taking the same playbook Oxford unveiled their plan last Friday. The plan will cover members outside NJ only on emergencies. Unlike the Liberty HMO some plans options are non-gated plans not needing referrals to for access to a Specialist Doctor.

The Garden State Network provides access to the 21 New Jersey counties only.The Garden State Network does not provide national access to the UnitedHealthcare Choice Plus network. For NJ 1-50, up to 4 plan options can be selected and the Garden State products can be paired with Liberty and Freedom network options. With this network, employers can select which of the 13, in-network only plan designs available will work best for their needs and for the needs of their employees.

Oxford/United has been purchasing Provider groups since 2011 , see our post UnitedHealthcare Buying Medical Groups? This strategy of late is by no means exclusive to this Insurer but it is worth pointing them out as they are a national leading health Provider and worth paying attention to.

Some highlights of the plan designs available with the Oxford Garden State Network are below:

∙ Routine, in-network preventive care covered at 100 percent

∙ In-network only coverage

∙ Choice between 11 non-gated and two gated plan designs (gated plan designs will require a referral)

∙ Plan designs with copayments, deductible and coinsurance, and Health Savings Accounts (HSA) are available.

Sign up for latest news updates. Please contact us for immediate information on how to implement these initiatives for your group-specific needs at info@medicalsolutionscorp.com or Call (855) 667-4621.

Under the Consolidated Omnibus Budget Reconciliation Act (COBRA), an individual who was covered by a group health plan on the day before the occurrence of a qualifying event (such as a termination of employment or a reduction in hours that causes loss of coverage under the plan) may be able to elect COBRA continuation coverage upon that qualifying event. Individuals with such a right are referred to as qualified beneficiaries.

Under COBRA, group health plans must provide covered employees and their families with certain notices explaining their COBRA rights. A group health plan must provide each covered employee and spouse (if any) with a written notice of COBRA rights “at the time of commencement of coverage” under the plan (general notice). A group health plan must also provide qualified beneficiaries with a notice which describes their rights to COBRA continuation coverage and how to make an election (election notice).

General Notice: The general notice must be furnished to each covered employee (and their spouse if covered under the plan) not later than the earlier of: (1) 90 days from the date on which the covered employee or spouse first becomes covered under the plan or, if later, the date on which the plan first becomes subject to the continuation coverage requirements; or (2) the date on which the administrator is required to furnish an election notice to the employee or to his or her spouse or dependent.

Election Notice: The election notice must be provided to the qualified beneficiaries within 14 days after the plan administrator receives notice that a qualifying event has occurred. Some qualified beneficiaries may want to consider and compare health coverage alternatives to COBRA continuation coverage, such as coverage that is available through the Health Insurance Marketplace (Exchange). Qualified beneficiaries may be eligible for a premium tax credit (a tax credit to help pay for some or all of the cost of coverage in plans offered through the Exchange) and cost-sharing reductions (amounts that lower out-of-pocket costs for deductibles, coinsurance, and copayments), and may find that Exchange coverage is more affordable than COBRA.

The Children’s Health Insurance Program Reauthorization Act of 2009 (CHIPRA) specifies that an employer that maintains a group health plan in a State that provides premium assistance for the purchase of coverage under a group health plan is required to notify each employee of potential opportunities currently available for premium assistance in the State in which the employee resides.

The Department of Labor has model notices that plans may use to satisfy the requirement to provide the general notice and election notice under COBRA, and the notice regarding premium assistance under CHIPRA. The COBRA model election notice was revised on May 8, 2013 to help make qualified beneficiaries aware of other coverage options that would soon become available in the Marketplace. Recently the DOL issued a Notice of Proposed Rulemaking, as well as updated versions of the model general notice and model election notice that reflect that the Exchange is now open and that better describes special enrollment rights in Exchange coverage. The DOL is also issuing a revised CHIPRA notice with similar updates related to Marketplace coverage.

Sign up for latest news updates. Please contact us for immediate information on how to implement these initiatives for your group-specific needs at info@medicalsolutionscorp.com or Call (855) 667-4621.

Adding a one-month orientation period may help an employer avoid complying with the new health benefits. Federal agencies are offering employers a benefits-free 30 day orientation period option in final regulations. There is also clarification on how employers must treat certain categories of new hires, as either FT , PT or Seasonal employees

The Final Regulations

These final regulations provide that the one month period would be determined by adding one calendar month and subtracting one calendar day, measured from an employee’s start date in a position that is otherwise eligible for coverage. For example, if an employee’s start date in an otherwise eligible position is May 3, the last permitted day of the orientation period is June 2. Similarly, if an employee’s start date in an otherwise eligible position is October 1, the last permitted day of the orientation period is October 31.

The new regulations implement part of the “employer shared responsibility mandate” provisions created by the Patient Protection and Affordable Care Act (PPACA). In all categories of new hire the e final regulations provide that one month is the maximum allowed length of an employment-based orientation period. For any period longer than one month that precedes a waiting period, the 90-day period begins after an individual is otherwise eligible to enroll under the terms of a group health plan.

When must an employer offer coverage:

The final regulations continue to provide that if a group health plan conditions eligibility on an employee’s having completed a reasonable and bona fide employment-based orientation period, the eligibility condition is not considered to be designed to avoid compliance with the 90-day waiting period limitation if the orientation period does not exceed one month and the maximum 90-day waiting period begins on the first day after the orientation period.

These final regulations apply to group health plans and health insurance issuers for plan years beginning on or after January 1, 2015.

When the Employer Might be Subject to a Penalty:

If at least one full-time employee of the employer buys health insurance in a public Exchange (Marketplace) and qualifies for a subsidy (either a premium tax credit or a cost-sharing reduction), the employer must pay a penalty.

There are two different types of penalties.

)The IRC section 4980H(a) penalty applies if a large employer offers coverage to less than 70% of its full-time employees in 2015 (or to less than 95% after the 2015 plan year). This penalty is $2000 annually or $166.67/month times the total number of “full-time” employees minus the first 80 (minus the first 30 after 2015). The penalty calculation does not include variable hour or seasonal employees who are in their measurement or administrative periods, even if they in fact worked on average at least 30 hours/week or 130/month during those periods. Nor does it include those who are in their stability periods but who did not qualify for coverage based on their hours worked during the associated measurement period.

IRC section 4980H(b) penalty. It applies if a large employer offers coverage to at least 70% of its full-time employees (95% after 2015), but for some full-time employees the coverage is either not “affordable” or does not provide minimum value. This penalty is $3,000 annually or $250/month for each full-time employee who buys health insurance in a public Exchange (Marketplace) and qualifies for a subsidy and for whom the employee cost for self-only coverage under the lowest-cost option available from the employer is more than 9.5% of the employee’s household income (or one of three safe harbors), or for whom the employer coverage offered does not provide at least minimum value. Again, the penalty calculation does not apply if the employee who qualified for a subsidy was a variable hour or seasonal employee who was in his/her measurement or administrative periods, nor does it include those employees who are in their stability periods but who did not qualify for coverage based on their hours worked during the associated measurement period. Additionally, the (b) penalty cannot be more than the (a) penalty would have been had it applied.

Summary and Employer Action Items

The bottom line is this:

If you hire a non-seasonal employee whom you reasonably expect (at date of hire) to work at least 30 hours/week or 130 hours/month, you must track hours each calendar month and offer benefits by the first day of the fourth month if the employee averages at least 130 hours/month for the first three months. This applies even if you hire this employee for a short-term position or a summer internship (unless you take the position, upon advice from your legal counsel, that a summer intern is a “seasonal” employee).

If you hire a non-seasonal employee and you cannot reasonably determine at date of hire if they will work on average at least 30 hours/week (130 hours/month), you can track their hours over their “initial measurement period” and not offer benefits until the associated “stability period,” if the employee averaged at least 130 hours/ month during the measurement period. The stability period might not begin until 13-14 months after the date of hire.

If you hire an employee who meets the new definition of a “seasonal employee,” you can track their hours over their “initial measurement period” and not offer benefits until the associated “stability period” if they averaged at least 130 hours/month during the initial measurement period. You do not have to offer benefits by the first day of the fourth month.

A copy of the final regulations can be obtained by clicking on the link below:

Sign up for latest news updates. Please contact us for immediate information on how to implement these initiatives for your group-specific needs at info@medicalsolutionscorp.com or Call (855) 667-4621.