[tab_item title=”Reminder PCORI Research Fees Due by July 231st”]

Posted on July 24 2013

Fees Apply to Employers Sponsoring Certain Self-Insured Plans

Effective for plan years ending on or after October 1, 2012, and before October 1, 2019, employers that sponsorcertain self-insured plans are responsible for new fees to fund the Patient-Centered Outcomes Research Institute (also known as PCORI). HRAs and health FSAs that are not treated as excepted benefits are generally subject to the fees.

Fees are due no later than July 31st of the year following the last day of the plan year. The IRS has revised Form 720for affected employers to report and pay the required fees.

Review our Health Care Reform Checklist for information on other requirements impacting employers and group health plans this year.

[/tab_item]

[tab_item title=”Affordable Care Act Weekly Webinar Series”]

Posted on July 23 2013

Free Series for Small Business Owners to Help Understand the Law

The U.S. Small Business Administration (SBA), together with the Small Business Majority (a national nonprofit advocacy organization), has launched the Affordable Care Act 101 Weekly Webinar Series. The webinars feature guidance on key pieces of the law for small business owners provided by SBA representatives, followed by a question and answer period.

Topics being discussed in the webinars include:

Small business tax credits—who is eligible and how to claim the credit;

Shared responsibility (also known as “pay or play”);

Cost containment; and

Tools and resources available for small businesses to learn more about the law.

The free series will take place every Thursday from now through the opening of the Health Insurance Exchanges (Marketplaces) in October. The first series of webinars will cover the same content; a second round of webinars featuring new content will be held later this fall.

The registration links for the first series of webinars can be found by clicking here. After registering, you will receive a confirmation email with all of the information needed to access the webinar either by telephone or online.

Visit our Health Care Reform Blog section to stay on top of the latest Affordable Care Act updates.

[/tab_item]

[tab_item title=”4 Things Employers Should Know About Providing the Health Insurance Exchange Notice”]

Posted on July 19 2013

Notice Must Be Distributed to Current Employees No Later Than October 1, 2013

Following a delay in the original effective date, employers will need to comply with the new requirement to provide each employee a written notice with information about a Health Insurance Exchange (also known as a Marketplace) beginning this fall. Below are four important reminders about the notice.

The notice requirement applies to employers covered by the federal Fair Labor Standards Act (FLSA). In general, the FLSA applies to employers that employ one or more employees who are engaged in, or produce goods for, interstate commerce. For most firms, a test of not less than $500,000 in annual dollar volume of business applies. The FLSA also specifically covers certain entities such as hospitals, educational institutions, and government agencies.

Employers must provide the notice to each employee, regardless of plan enrollment status (if applicable) or of part-time or full-time status. Employers are not required to provide a separate notice to dependents or other individuals who are or may become eligible for coverage under the plan but who are not employees.

The U.S. Department of Labor has provided two sample notices employers may use to comply with this requirement. The law requires that specific information be included in each notice. One model notice is available for employers that offer a health plan to some or all employees, and another model notice may be used by employers that do not offer a health plan.

Notices must be provided to each current employee no later than October 1, 2013, and to each new employee at the time of hiring beginning October 1, 2013. In general, a notice will be considered provided at the time of hiring if it is provided within 14 days of an employee’s start date. The notice is required to be provided automatically and free of charge. Employers may distribute the notice by first-class mail, or electronically if certain requirements are met.

Visit our section on Health Reform Resource for information on other notices required to be provided and to download additional model notices available for employers and group health plans.

[/tab_item][tab_item title=”5 Q and As on Individual Shared Responsibility”]

Posted on July 12 2013

Employer-Sponsored Coverage Considered “Minimum Essential Coverage”

The individual shared responsibility provision, which goes into effect on January 1, 2014, requires individuals of all ages (including children) to have minimum essential health coverage for each month, qualify for an exemption, or make a payment when filing his or her federal income tax return. Below are five questions and answers related to the mandate that may be of interest to employers and employees.

1. What counts as minimum essential coverage? Minimum essential coverage includes employer-sponsored coverage (including COBRA coverage and retiree coverage), coverage purchased in the individual market, Medicare Part A coverage and Medicare Advantage, Children’s Health Insurance Program (CHIP) coverage, and certain other types of coverage.

Minimum essential coverage does not include coverage providing only limited benefits, such as coverage only for vision care or dental care, workers’ compensation, or disability policies.

2. If an employee receives coverage from a spouse’s employer, will that employee have minimum essential coverage? Yes. Employer-sponsored coverage is generally minimum essential coverage. If an employee enrolls in employer-sponsored coverage for himself and his family, the employee and all of the covered family members have minimum essential coverage.

3. Does an employee’s spouse and dependent children have to be covered under the same policy or plan that covers the employee? No. An employee, his or her spouse, and dependent children do not have to be covered under the same policy or plan. However, the employee, spouse, and each dependent child for whom the employee may claim a personal exemption on his or her federal income tax return must have minimum essential coverage or qualify for an exemption, or a payment will be owed.

4. A company’s health plan is “grandfathered.” Does the employer’s plan provide minimum essential coverage? Yes. Grandfathered group health plans provide minimum essential coverage.

5. Is transition relief available in certain circumstances? Yes. Notice 2013-42 provides transition relief from the shared responsibility payment for individuals who are eligible to enroll in employer-sponsored health plans with a plan year other than a calendar year (non-calendar year plans) if the plan year begins in 2013 and ends in 2014. The transition relief applies to an employee, or an individual having a relationship to the employee, who is eligible to enroll in a non-calendar year eligible employer-sponsored plan with a 2013-2014 plan year. The transition relief begins in January 2014 and continues through the month in which the 2013-2014 plan year ends.

For More Information You may review additional questions and answers in their entirety on the IRS website.

[/tab_item][tab_item title=”IRS Guidance on Delay of Pay or Play Requirements”]

Posted on July 10 2013

No Penalties Will Be Assessed for 2014

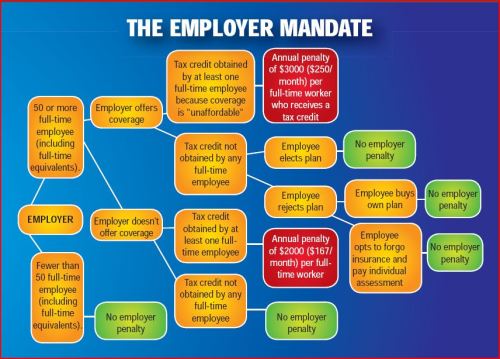

Formal guidance released by the IRS provides additional details regarding the delay of the Health Care Reform “pay or play” requirements. Under those provisions, certain large employers (generally those with at least 50 full-time employees) who do not offer full-time employees affordable health insurance that provides a minimum level of coverage may be subject to a penalty tax.

According to the guidance, no penalties (also known as employer shared responsibility payments) will be assessed for 2014. The “pay or play” requirements will be fully effective for 2015 and employers are encouraged to maintain or expand health coverage in 2014 in preparation for compliance.

The delay is a result of transition relief being provided for 2014 with respect to certain employer and insurer reporting requirements. Such reporting will be necessary for the IRS to determine whether a penalty may be due, and, consequently, the transition relief makes it impractical to determine which employers owe shared responsibility payments for 2014. Once the information reporting rules are issued, employers are encouraged to voluntarily comply with the reporting requirements in 2014.

The delay does not affect the application or effective dates of other Health Care Reform provisions, including the individual shared responsibility requirements and employees’ access to premium tax credits for enrolling in qualified health plans through the Health Insurance Exchanges.

In an unexpected announcement pre-July 4th the big news was Obamacare Employer Mandate Delayed with penalties under the Affordable Care Act (ACA) until 2015. The mandate also known as the “Employer Shared Responsibility” requires employers with 50 or more FTEs to offer affordable health insurance coverage to their workers or face financial penalties for not doing so. Those penalties would originally have been applied beginning in 2014.

There has been a follow up guidance issued last week July 9th by the IRS. According to the IRS, the delay will give employers more time to prepare for the change in how health insurance is provided and will also give the Obama Administration time to simplify the insurance-related reporting requirements that employers face. This transition relief appears to come with “no strings attached.” Although the IRS guidance encourages employers to voluntarily comply with the employer mandate and maintain or expand health care coverage in 2014, the IRS will not impose penalties for a failure to do so.

Although the IRS guidance encourages employers to voluntarily comply with the employer mandate and maintain or expand health care coverage in 2014, the IRS will not impose penalties for a failure to do so.Notably, the guidance issued on July 9th also does not require employers to make “good faith” efforts to comply. As a result of this transition year, employers will have the option of deciding to what extent (if any) they will continue efforts to comply with the employer mandate during 2014.

Employers who intended to rely on one of the transition rules previously announced for 2014 should keep in mind that the latest IRS guidance does not provide special transition rules for 2015. Other group health plan requuirements still apply as discussed in our prior blog Essential Health Benefits Not Delayed.

This means that for plan years beginning on and after January 1, 2014, all group health plans must:

Eliminate all pre-existing condition exclusions (regardless of age);

Maximum Cost Sharing Deductible to $2,000/individual ($4,000/family); limit in-network out-of-pocket maximums to $6,350/individual ($12,700/family)

Individual Mandate Still Applies. individuals will still be required to obtain health care coverage or pay a penalty for each month they do not have coverage, beginning January 1, 2014

Exchanges (Marketplaces) Open for Enrollment October 1, 2013.

The IRS notice makes it clear that individuals who enroll in coverage on the marketplaces will continue to be eligible for a premium tax credit if their household income is within a specified range and they are not eligible for other minimum essential coverage.

Employers Must Send Notice of Exchanges (Marketplaces) Before October 1, 2013. These notices must be sent to current employees by October 1, 2013. Then, beginning October 1, 2013, employers must send this notice to new hires within 14 days of their start date.

New taxes still apply – Patient Centered Outcomes Research Institute (PCORI) excise taxes and transitional reinsurance program fees;HRA/HSA/FSA clients also pay a monthly $1/employee tax.

We will continue to monitor ACA developments and will provide you relevant updated information when available. In the meantime, please visit to view past blogs and Legislative Alerts at https://360peo.com/feed.

With only 6 month away from full implementation of 2014 Patient Protection Affordability Care Act (PPACA) employers are understandably uncertain. Below are Health Care reform – five things employers can do now to prepare and take action.

UPDATE JULY 2nd: Since blog posting the President Administration has delayed 1 year Employed Shared Responsibility Mandate i.e. Pay or Play to Jan 2015.

1. Employee Communications

Employers must notify employees of the online insurance marketplace known as a Healthcare Exchange. Recently released federal guidelines require employers to notify their workers of eligibility requirements for their state exchange starting Oct. 1, 2013 Open Enrollments for Jan 2014 effective date. To the relief of many, the U.S. Labor Department also provided model notices that employers can give to their workers, which eliminates the need to develop their own notifications.

Additionally, Employers sponsoring a health plan must give employees a Summary of Benefits and Coverage (SBC). The purpose of the Summary of Benefits and Coverage, or SBC, is to present benefits and coverage information in clear language and in a consistent format. Inspired by the Nutrition Facts Label on packaged food, theSBC (pdf) includes two medical scenarios: having a baby and managing Type II diabetes. It estimates how much a patient would pay for medical care in each scenario with specific insurance plans.

It’s the employer’s responsibility to distribute the SBCs to employees.

This requirement applies to health plan renewals after Sept. 23, 2012.

Department of Labor will NOT impose penalties for non-compliance with the SBC notice during the first year as long as employers show a “good faith” effort to comply. Read the FAQ on SBC and ACA pdf here.

2. Determining which Employers must offer health care.

Because employers with 50 full-time equivalents face penalties for not providing affordable, minimum value insurance an employer should know whether it is subject to these requirements or not. Common law employees of the employer and any commonly controlled company must be counted. Employers with temporary or leased employees will want to discuss with their advisors whether these employees will be considered “common law employees” for purposes of determining how many FTEs an employer has. Employers with employees who are paid based on unique payment models (stipends, work product, etc) will want to discuss how to calculate these employee hours with their benefits advisors.

Employers with 50 or more employees will incur penalties of up to $2,000 per employee if they cancel their existing health care program (which up until 2014 would be considered an optional benefit to provide). They will also incur penalties if their plan is too costly, and they do not meet the affordability standards.

Employers with less than 50 employees will not incur penalties if they cancel their health care plan, and that decision will need to be made on a business by business basis. They can also choose to offer partial coverage and contribute up to the minimum 50% of single coverage not to exceed 9.5% employee

The good news is Employers can subtract 30 FT employees. This portion is known as the Employer “play or pay” option. Specific case example and details are found at Pay or Play Employer Guide.

To encourage businesses to offer health benefits to their employees, the federal government is offering tax credits to small businesses. These credits are available to an estimated 4 million small businesses, including nonprofits.The IRS has set up a web page with information: Small Business Health Care Tax Credit for Small Employers. The maximum “credit” (which offsets taxes dollar for dollar and is better than a “deduction” which reduces taxable income) is 35 percent of the amount an employer pays towards employee health insurance.

Who’s eligible?

To qualify, small employers must:

Have fewer than the equivalent of 25 full-time workers

Pay average annual wages below $50,000

Cover at least 50% of the cost of health care coverage for their workers

Because of the high wages paid in most industries in NY/NJ/CT Tri State, few small employers that provide coverage pay such a low average wage. Note, however, that the calculation of average wages and number of employees excludes the wages of an owner and his or her family members.

medicalsolutionscorp.com help clients gather the appropriate information and do a preliminary estimate of the credit amount. This information will help you and your accountant determine whether applying for the credit makes financial sense. Find out what the new tax credit could mean for your coverage. Call us at 855-667-4621.

4. Determine affordability

Beginning Jan. 1, 2014, an employer with 50 or more employees must pay a tax penalty if they either: a) Do not provide health insurance with minimum benefits or 60 percent of healthcare expenses; b) Require employees to contribute more than 9.5 percent of an employee’s household income for the health insurance and those employees obtain a government subsidy for coverage.

Companies will be required to pay $3,000 per employee without affordable coverage. (Note: there are a number of caveats that might affect the actual penalty paid, so consult your tax advisor.)

It is crucial to Understand the difference between FT and Full Time Equivalent. To determine the FTE (Full Time Equivalent) you must count FT and PT employees. Full Time Employees are those working 30 hours+/week.* The number of full-time employees excludes those full-time seasonal employees who work for less than 120 days during the year.4 The hours worked by part-time employees (i.e., those working less than 30 hours per week) are included in the calculation of a large employer, on a monthly basis, by taking their total number of monthly hours worked divided by 120.

For example, a firm has 35 full-time employees (30+ hours). In addition, the firm has 20 part time employees who all work 24 hours per week (96 hours per month). These part-time employees’ hours would be treated as equivalent to 16 full-time employees, based on the following calculation:

20 employees x 96 hours / 120 = 1920 / 120 = 16

Thus, in this example, the firm would be considered a “large employer,” based on a total full-time equivalent count of 51—that is, 35 full-time employees plus 16 full-time equivalents based on part-time hours.

In the coming months, Millennium Medical Solutions Inc will host seminars and will share information you’ll need to know as the countdown continues to October 1st.

Error: Contact form not found.

This blog is not intended to represent legal advise and one should consult with a tax and/or legal expert.

* IRC 4980H(c)(4)

Disclaimer: This blog is not intended to represent legal advise and one should consult with a tax and/or legal expert.

Many follow up questions on the postPay or Play Employer Guide have been raised. A Pay or Play FAQ hopefully adds some clarification.

Will I be required to offer health insurance coverage to my employees?

No. However, if you have at least 50 full-time employees, and you don’t offer coverage, you will owe a penalty starting in 2014 if any full time employee is eligible for and purchases subsidized coverage through an exchange. This penalty is called the “free rider” penalty.

We employ about 40 full-time employees working 30 or more hours per week and about 25 part-time or seasonal employees. So we are not subject to the employer mandate penalties, right?

You may be. The health reform law does not require you to provide coverage for employees working on average less than 30 hours per week (“part-time”). However, the hours worked by part time employees are counted to determine whether you have at least 50 full-time employee equivalents and therefore are subject to the employer mandate. This is done by taking the total number of monthly hours worked by part time employees (but not to exceed 120 hours for any one part-time employee) and dividing by 120 to get the number of “full time equivalent” employees. You would then add those “full-time equivalent” employees to your 40 full-time employees.

The hours worked by seasonal employees are also counted to determine whether you have at least 50 full-time employee equivalents and therefore are subject to the employer mandate. For purposes of determining whether you are a large employer, seasonal employees are workers who perform labor or services on a seasonal basis (i.e. exclusively performed at certain seasons or periods of the year and which, from its nature, may not be continuous or carried on throughout the year) for no more than 120 days during the taxable year and retail workers employed exclusively during holiday seasons. There is an exemption from the employer mandate that says you would not be considered to employ more than 50 full-time employees if:

Your workforce only exceeds 50 full-time employees for 120 days, or fewer, during the calendar year; and

The employees in excess of 50 who were employed during that 120-day (or fewer) period were seasonal workers.

Our workforce numbers go up and down during the year. How do we determine if we had at least 50 full-time employees on business days during the preceding calendar year?

For purposes of determining if you are a large employer, the formula requires the following steps:

1.Determine the total number of full-time employees (including any full-time seasonal workers) for each calendar month in the preceding calendar year;

2.Determine the total number of full-time equivalents (including non-full-time seasonal employees) for each calendar month in the preceding calendar year;

3.Add the number of full-time employees and full-time equivalents described in Steps 1 and 2 above for each month of the calendar year;

4.Add up the 12 monthly numbers;

5.Divide by 12. If the average per month is 50 or more, you are a large employer.

So if we offer coverage to our full-time employees, we will not have to pay a penalty?

Not necessarily. If you have at least 50 full-time employees and you offer coverage to at least 95% of your full-time employees, you are still subject to a penalty starting in 2014 if:

1.A full-time employee’s contribution for employee-only coverage exceeds 9.5% of the employee’s household income (Note: see below regarding a proposed affordability “safe harbor”) or the plan’s value is less than 60%; and

2.The employee’s household income is less than 400% of the federal poverty level; and

3.The employee waives your coverage and purchases coverage on an exchange with premium tax credits.

The penalty will be calculated separately for each month in which the above applies. The amount of the penalty for a given month equals the number of full- time employees who receive a premium tax credit for that month multiplied by 1/12 of $3,000.

We have more than 50 full-time employees so we are subject to the employer mandate penalties. How do we know which of our employees is considered “full-time” requiring us to pay a penalty if they qualify for premium tax credits at an exchange (if the employee has a variable work schedule or is seasonal)?

Through the end of 2014, for purposes of the employer mandate penalties, the guidance permits you to use a “look-back measurement period/stability period” safe harbor to determine which of your employees are considered full-time employees. You may use a standard measurement/stability period for ongoing employees, while using a different initial measurement/stability period for new variable and seasonal employees

How do the full-time employee safe harbors work for new hires?

They are generally based on the employee’s hours worked, or, the amount of hours the employee is reasonably expected to work as of their hire date.

New employee reasonably expected to work full-time (i.e. 30 or more hours per week)– If you reasonably expect an employee to work full-time when you hire them, and coverage is offered to the employee before the end of the employee’s initial 90 days of employment, you will not be subject to the employer mandate payment for that employee, if the coverage is affordable and meets the minimum required value.

New employee reasonably expected to work part-time (i.e. less than 30 hours per week)-– If you reasonably expect an employee to work part-time and the employee’s number of hours do not vary, you will not be subject to the employer mandate penalty for that employee if you don’t offer them coverage.

New variable hour and seasonal employees – If based on the facts and circumstances at the date the employee begins working (the start date), you cannot determine that the employee is reasonably expected to work on average at least 30 hours per week, then that employee is a variable hour employee. Because the term “seasonal employee” is not defined for purposes of the employer responsibility penalty, through 2014, you are permitted to use a reasonable, good faith interpretation of the term “seasonal employee”. The IRS has indicated that any interpretation of the term “seasonal” probably would not be reasonable if it included a working period of more than six months. Once hired, you have the option to determine whether a new variable hour or seasonal employee is a full-time employee using an “initial measurement period” of between three and 12 months (as selected by you).You would measure the hours of service completed by the new employee during the initial measurement period to determine whether the employee worked an average of 30 hours per week or more during this period. If the employee did work at least 30 hours per week during the measurement period, then the employee would be treated as a full-time employee during a subsequent “stability period,” regardless of the employee’s number of hours of service during the stability period, so long as he or she remained an employee. The stability period must be for at least six consecutive calendar months and cannot be shorter than the initial measurement period. If the employee then didn’t work on average at least 30 hours per week during the measurement period, you would not have to treat the employee as a full-time employee during the stability period that followed the measurement period, but the stability period could not be more than one month longer than the initial measurement period.

Example – Facts: For new variable hour employees, you use a 12-month initial measurement period that begins on the start date and apply an administrative period from the end of the initial measurement period through the end of the first calendar month beginning on or after the end of the initial measurement period.

Situation: Dianna is hired on May 10, 2014. Dianna’s initial measurement period runs from May 10, 2014, through May 9, 2015. Dianna works an average of 30 hours per week during this initial measurement period. You offer affordable coverage to Dianna for a stability period that runs from July 1, 2015 through June 30, 2016.

Conclusion: Dianna worked an average of 30 hours per week during her initial measurement period and you had (1) an initial measurement period that does not exceed 12 months; (2) an administrative period totaling not more than 90 days; and (3) a combined initial measurement period and administrative period that does not last beyond the final day of the first calendar month beginning on or after the one-year anniversary of Dianna’s start date. Accordingly, from Dianna’s start date through June 30, 2016, you are not subject to an employer mandate penalty with respect to Dianna because you complied with the standards for the initial measurement period and stability periods for a new variable hour employee. However, you must test Dianna again based on the period from October 15, 2014 through October 14, 2015 (your first standard measurement period that begins after Dianna’s start date) to see if she qualifies to continue coverage beyond the initial stability period.

Employee FT Testing Period Chart

As you can tell, there are many things to consider as you map out your plans for how your business is going to proceed with health care reform. Millennium Medical Solutions Corp hopes to be a valuable resource in the weeks and months ahead as you make these decisions. What about you? Do you have any glaring questions that we could answer for you about health care reform compliance?

For a FREE Affordable Care Act Guide leave your questions in the comments below or click the “Contact Us” button and we’ll do our best to answer your questions.

Please refer to the IRS Notice in the links below for more details and examples:

DISCLAIMER: We share this information with our clients and friends for general informational purposes only. It does not necessarily address all of your specific issues. It should not be construed as, nor is it intended to provide, legal advice. Questions regarding specific issues and application of these rules to your plans should be addressed by your legal counsel.

Tick! tick! tick! As the 2014 Employer Mandate to either pay or play gets closer the nation’s employers move a step closer to having to make a decision: Do I play or pay? This Employer mandate under Patient Protection and Affordable Care Act (PPACA) does not apply to smaller groups under 50 FTE (full time equivalent) employees. Many small groups such as food service industry, retailers, construction etc. in fact have many FTE and while they may work minimal hours can trigger the “pay or play” mandate.

The IRS has released recently guidance published in the form of a Notice of Proposed Rulemaking (NPRM), addresses a number of issues tightly linked to an array of practical considerations related to the employer mandate. These include defining a “large employer,” determining “full-time” status for employees, clarifying the meaning of “dependents,” and determining what constitutes “affordable” coverage.

The guidance also tackles several stickier questions such as how and whether to count foreign or seasonal workers, as well as how to calculate the full-time status of employees who work unusual hours, such as teachers or airline pilots.

Three safe harbors relating to the provision of “affordable” coverage to employees in order to avoid exposure to the mandate penalties are also included in the guidance. Transition relief is offered in recognition of certain employers’ needing time to bring their plans into compliance.

Still, there are several regs that the IRS is awaiting commentary and resolution on due on March 18, 2013.

A Q&A summary of the rule has been released by the IRS and is available by clickinghere.

Some employers assert that the play-or-pay mandate will raise their costs and force them to make workforce cutbacks. As a result, a number are considering eliminating their health care coverage altogether and instead paying the penalty on their full-time employees. While the “pay” option might be worth considering, there are strong reasons why employers should look carefully at all of their options and do their best to calculate the actual outcomes of each.

Other Key Issues Addressed in the Proposed Rules Additional issues addressed in the proposed regulations include:

Determining which employers are subject to the “pay or play” requirements;

Determining who is a full-time employee, including approaches that can be used for employees who work variable hour schedules, seasonal employees, and teachers who have time off between school years;

Determining whether coverage is affordable and provides minimum value; and

Calculating the amount of the penalty due and how the penalty will be assessed.

When conducting a cost-benefit analysis, the key tax issues the employer should consider are:

Employer Tax Penalty for Not Offering “Qualified” Group Health

Not applicable for employers with less than 50 FTEs

$2,000 penalty per full-time employee (minus 30 employee credit)****

Employer Tax Penalty for Offering “Qualified” Health That is Not “Affordable”

Not applicable for employers with less than 50 FTEs

$3000 per employee receiving subsidy

Example:

Jungle Corp. has 100 full-time employees and is a leader in its market, using a talent differentiation strategy. Jungle’s family coverage costs $15,000, of which employees pay $3,000. Bob Smith, a highly skilled worker with a strong performance record, earns $50,000 and has family coverage through Jungle’s plan.

On Jan. 1, 2014, Jungle Corp. announces it is dropping its group health plan coverage and will instead pay the $2,000-per-full-time-employee penalty. On Jan. 2, Bob walks into HR and asks about receiving replacement compensation for the $12,000 that the business had been paying toward his family coverage.

Wanting to retain Bob in accordance with its strategy of maintaining market leadership with an experienced workforce, Jungle offers him another $12,000. But clever Bob points out that his share of Social Security and Medicare payroll (FICA) taxes will take a bite out of that $12,000, as will federal and state income taxes, so the HR manager agrees to make good on those amounts as well. Of course, the company will also have to pay its share of FICA taxes on Bob’s additional compensation. As a result, instead of paying $12,000 toward Bob’s family coverage using pre-tax dollars, Jungle Corp. now finds itself paying an additional:

Bob’s salary adjustment: $14,500

Employer’s share of FICA taxes: $1,109

Excise tax (penalty): $2,000 ———————————-

Total: $17,609 (versus $12,000 currently)

Similar per-employee costs will be reflected across the company’s workforce. A move that seemed like a no-brainer, the consequences could make you look silly.

For More Information Due to the complexity of the law in this area, and the absence of finalized guidance, employers are strongly advised to review their benefit plans to prepare for the changes ahead. Additional information regarding the penalty is featured on our Employer Shared Responsibilitypage.

In the coming months, Millennium Medical Solutions Inc will host seminars and will share information you’ll need to know as the countdown continues to October 1st. Please contact us for immediate information on how to implement these initiatives for your group-specific needs at info@medicalsolutionscorp.comor Call (855) 667-4621.

Crains Brokers’ Commissions Face Uncertain Future. A quick comment on our quote in Crains “Crains Brokers’ Commissions Face Uncertain Future” today. Insurers are indeed cutting back on services resulting in cost containement measures such as layoffs, outsourcing and significant broker commissions cuts.

A significant negative development is the NYS decision to not allow licensed Agents/Brokers in the Individual Exchange. Many States such as Massachusettes, the inspiration for Health Care Reform, use a Connectorwhich is an Exchange or an independent state agency that helps Massachusetts residents find health insurance coverage and avoid tax penalties. Instead NYS will allow Agents/Brokers to only work in the Commercial Exchange known as SHOP. HealthPass is a good pre-cursor of the SHOP Exchange offering Small Businesses a Defined Contribution Health Planof full options form Health Insurance, Dental, Vision to Term Life Insurance and Disability.

The Individual Exchange will work with an “Assitor” or “Navigator”. In NYS Government and Non-Profit Agencies will comprise the “Navigator” which will only be allowed to operate in the Individual Exchange. By design an income subsidy will only pass through this Individual Exchange an not on the SHOP Exchange. Example: a $50,000 Family Household of 4 can get approximately 80% credited.

The Federal Gov has already spent $2.2 Billion on State Exchanges. And this figures does not include remaining States as there are only 19 States working on an Exchange for 2014. The Exchanges will be built up for 2 years and then must be fully independent by 2016. If 88% of small groups coverage purchased by Brokers acc. to Bostons Wakely Report in research study- Role of Producers and Other Third Party Assisters in New York’s Individual and SHOP Exchanges the distribution infrastructure is already there. Access to care is not the difficulty in finding a plan its the very cost of the plan! Why then does NYS decide to spend on building up new infrastructures? AgentsBrokers can easily outreach and council to uninsured as well. In fact many small businesses such as construction, consulting services and dining have many uninsured that an Agent/Broker already has a relationship with.

Despite all this and the rapid changes in reshaping health care we remain optimistic and look forward to taking on a greater role in health care reform.

With more choice, our groups and their employees will need more direction, allowing brokers to take on more of a consultative role. Healthcare plans are not a simple purchase and one plan doesn’t fit all. By delivering the latest cutting-edge benefits technologies, continued consumer focus approach and leveraging our long time relationships with Benefits/HR/Payroll partners our role will be pivotal in being part of the solution.

What is an Exchange? One of the centerpieces of the recently passed Patient Protection and Affordable Care Act

(PPACA) is the establishment of state based health insurance exchanges by the year 2014.

An “Exchange” is a mechanism for organizing the health insurance marketplace to help consumers and small businesses shop for coverage in a way that permits easy comparison of available plan options based on price, benefits, service and quality. By pooling individuals and small groups together, transaction costs can be reduced and transparency can be increased. Exchanges can create more efficient and competitive markets for individuals and small employers.

Historically, the individual and small group health insurance markets have suffered from adverse selection and high administrative costs, resulting in low value for consumers. “Exchanges” will allow individuals and small businesses to benefit from the pooling of risk, market leverage, and economies of scale that large businesses currently enjoy.

Beginning with an open enrollment period in 2013, Insurance agents and Benefits professionals will help individuals and small employers shop, select, and enroll in high-quality, affordable private health plans in these “Exchanges” to fit their specific needs at competitive prices. Individuals in these “Exchanges” may also be eligible to receive premium subsidies through the Federal or State government. By providing one-stop shopping, we will make purchasing health insurance easier and more understandable through these “Exchanges” and provide the same level of service that you have become accustomed to.

Middle-class people will be able to pick from a range of private insurance plans, and most people will be eligible for help from the government to pay their premiums.

Low-income people will be steered to safety-net programs for which they might qualify. This could be a problem in states that choose not to expand their Medicaid programs under a separate part of the health care law. In that case, many low-income residents in those states would remain uninsured.

Q: How will I know if I can get help with my health insurance premiums?

A: You’ll disclose your income to the exchange at the time you apply for coverage and they’ll let you know. Only legal residents of the United States can get financial assistance.

The health care law offers sliding-scale subsidies based on income for individuals and families making up to four times the federal poverty level, about $44,700 for singles, $92,200 for a family of four.

But do yourself a favor and read the fine print because the government’s help gets skimpier as household income increases.

For example, a family of four headed by a 40-year-old making $35,000 will get a $10,742 tax credit toward an annual premium of $12,130. They’d have to pay $1,388, about 4 percent of their income, or about $115 a month.

A similar hypothetical family making $90,000 will get a much smaller tax credit, $3,580, meaning they’d have to pay $8,550 of the same $12,130 policy. That works out to more than 9 percent of their income, or about $710 a month.

The estimates were made using the nonpartisan Kaiser Family Foundation’s online calculator. Some people will also be eligible for help with their copayments.

Final note: Though it’s called a “tax credit” the government assistance goes directly to the insurer. You won’t see a check.

Q: What will the benefits look like?

A: The coverage will be more comprehensive than what’s now typically available in the individual health insurance market, dominated by bare-bones plans. It will be more like what an established, successful small business offers its employees. Premiums are likely to be higher for some people, but government assistance should mostly compensate for that.

All plans in the exchange will have to cover a standard set of “essential health benefits,” including hospitalization, doctor visits, prescriptions, emergency room treatment, maternal and newborn care, and prevention. Insurers cannot turn away the sick or charge them more. Middle-aged and older adults can’t be charged more than three times what young people pay. Insurers can impose penalties on smokers.

Because the benefits will be similar, the biggest difference among plans will be something called “actuarial value.” A new term for consumers, it’s the share of expected health care costs that the plan will cover.

There will be four levels of coverage, from “bronze,” which will cover 60 percent of expected costs, to “platinum,” which will cover 90 percent. “Silver” and “gold” are in between. Bronze plans will charge the lowest premiums, but they’ll have the highest annual deductibles. Platinum plans will have the highest premiums and the lowest out-of-pocket cost sharing.

This part is insurance nerdy but an important point – The government’s subsidy will be tied to the premium for the second-lowest-cost plan at the silver coverage level that’s available in your area. You could take it and buy a lower cost bronze plan, saving money on premiums. But you’d have to be prepared for the higher annual deductible and copayments.

If you have additional questions regarding how SHOP Exchanges and Individual Exchanges can benefit you please contact our team at Millennium Medical Solutions Corp. Stay tuned for updates as more information gets released. We’re inside of 75 days until exchanges open, and information will be coming quickly in the next few months. Sign up for latest news updates.

After a six-month delay in the original effective date, group health plans (including grandfathered plans) will soon need to comply with a new requirement under Health Care Reform to provide a summary of benefits and coverage (SBC) so that employees can more easily compare insurance options.

The new SBC notice requirements are effective for plan years and open enrollment periods beginning on or after Sept. 23, 2012. If you need a refresher, the following are some key points for group health plans:

An SBC must be provided to plan enrollees at specific times, such as upon application for coverage and at renewal, as well as upon request.

Insured group health plans can satisfy the requirement if the issuer provides a timely and complete SBC to the participant or beneficiary.

Combining information for different coverage tiers, different cost-sharing selections (such as levels of deductibles and copayments), and different add-ons to major medical coverage (such as FSAs, HRAs, HSAs, or wellness programs) into one SBC is permissible, provided the appearance is understandable.

SBCs may be provided either as a stand-alone document or in combination with other summary materials (for example, an SPD), if the SBC information is intact and prominently displayed at the beginning of the materials and in accordance with the SBC timing requirements.

The SBC must comply with certain appearance and format requirements and must use terminology understandable by the average plan enrollee; an SBC template along with instructions and related materials that may be used to satisfy the notice requirements, is available online.

The U.S. Department of Labor has released three sets of Frequently Asked Questions (FAQs) which address a number of issues relating to the SBC notice requirements. The FAQs also make clear that, during the first year of applicability of the new SBC rules, penalties will not be imposed on plans that are working diligently and in good faith to provide the required content in an appearance that is consistent with the final regulations.

Hello. It’s been awhile, hope you’re all well. To all who have inquired, my thanks for your concern, but all’s good. Hectic, but good. Lot’s going on and an awful lot of travel. I’ve had a chance to meet and talk with with insurance carriers, Health Human Services, Trade Groups, Broker panels and most importantly customers with spirited opinions such as yourselves. It’s been a great time to learn, recharge and stay a bit too busy to write any meaningful posts. While staying busy appears to be the new constant, I’ll try to find something worthy to share on a more regular basis. Before I get into it some news at MMS Corp:

Check our new 360peo.com this summer. We began the redesign and update of our web site to make it more user friendly and features packed with the following:

1-Quoting Module – The quoting engine will offer cross leading plans based on your location, income and employee total. Not all plans and carriers will participate and it is recommended that you get in touch with us. 2-Health Care Reform Section-this tab is dedicated to the new PPACA law. 3 Instant Chat – Scheduled Fall 2011 4. Social 2.0- Find us on Facebook, Linkedin and Twitter. 5. HR Log In- For clients only. Some of you have already begun using this online HR Kiosk. We’ve deployed this in partnership with HR Connect Technologies to offer employers tools for common HR tasks such as Benefit Plan Admin, Forms for new hires, terminations, work-site postings and employee record keeping. HR-Connect is a secure, HIPAA-compliant, Internet driven system designed to simplify your human resource department. Employees can review their own personal information, but not other employee’s data. Click Video Demo here and just ask us to set it up for your business at no charge!

Lastly, we have been appointed earlier in 2011 to the Empire Broker Advisory Council which consists of top 10 of 5000 brokers that meets throughout the year to discuss relevant topics such as market insights, health reform changes and input on future plan designs. We take this opportunity seriously in giving voice to our clients and shaping a more consumer friendly plan. To Empire’s credit, they have been indeed listening and have taken suggestions seriously. New plan options released in the Fall will be examples of this.

For now, however, let’s play some catch-up:

Latest new is that US Court of Appeals has ruled that the Affordable Care Act is constitutional. The ruling is online here. The ruling stated that this is in synch with the commerce clause of interstate commerce. Furthermore, since Congress can force someone to buy health insurance because even if they don’t need insurance today they will at some point in their life. While this ruling is impactful and could influence future rulings, this is expected by many to go to Supreme Court. They have been loudly silent on this touchy topic thus far.

Regardless, this Individual Mandate has little teeth with penalties @ $95 or 1% for 2014, $325 or 2% in 2015 and $695 or 2.5% in 2016. In other words if one can still buy health insurance, face little penalties and no pre-existing condition whats stopping someone form buying insurance when they’re in the hospital?!

To date, many key provisions have already been enacted. Some of those are:

Extending the age of adult children eligible for coverage under their parents’ health care plan to age 26

Prohibiting individual and group health plans from placing lifetime limits on the dollar value of coverage

Preventing health insurers from rescinding coverage (except in cases of fraud)

Prohibiting health insurers from imposing pre-existing condition exclusions for children

Mandating coverage for recommended immunizations and preventive care

PPACA items that died in 2011.

1. The non-discrimination provision for Group Health Plans have been delayed. The short answer is that IRS needs more funding to enforce this as well as additional guidance. See blog here

3. W2 Reporting delayed- the IRS said employers who file fewer than 250 Forms W-2 in 2011 will not be required to report the cost of health care coverage prior to January 2014

Items that have funding delays:

1. Free Choice Voucher Program Takes a Hit- The program would have provided funding of vouchers for lower income employees to subsidize the employer contribution. Under this provision, plan sponsors of employer-based plans (including self-funded benefit plans) would have been required to offer vouchers to employees who fall below a pre-defined income threshold, while the state-based exchanges would credit the employee the amount of the voucher that exceeded their monthly premium.

2. No Health Co-Ops- The goal of the program was to spur the creation of qualified nonprofit health insurance issuers that could offer health plans for individuals and small businesses in states where insurance issuers are licensed to offer them. The program also would have provided loans and grants to fund start-up and maintenance costs for these plans.

This is a bit disappointing as we looked to the highly rated Seattle-based Group Health Cooperative program as a successful at managing costs and offering consumer centric care, click here for more info.

3. Wellness Funding for Small groups- no updates as of yet on the $750 Million funding. This was forward thinking incentives for small groups to afford a a Wellness Program for smoking cessation, diet/nutrition, gym etc. Typically large groups have had these programs as their rates are directly linked to “experience” of their members. In small market the rates are spread over thousands of other small groups. This is a first come first serve funding that we are closely monitoring to help our groups.

We are partnering with Wellness Companies and Health Insurers on establishing a program for small groups. The ROI on this is typically 1.6 :1. If you think your group could benefit please drop us a note at info@medicalsolutionscor.com.

The biggest news really will be the Health Exchanges schedule to open by 2014. NYS in particular than most states has enjoyed 2 rounds of Federal seed capital with almost $30 million for this effort. Each state has to set up an exchange, or marketplace, where small employers and individuals whose employers don’t provide coverage, or who can’t afford the employer plans, can purchase insurance. About 2.7 million New Yorkers are uninsured.

Sponsors say it should also result in one statewide, online, streamlined system for enrolling and renewing enrollment in government-supported Medicaid, Child Health Plus and Family Health Plus programs.

Each state can implement their own version. Several states have rejected funding and do not want to participate in the exchange. By discounting health plan rates based on income its unclear of how much will fall as a state burden?

Florida is one state that has decided not to implement a state health insurance exchange altogether. That state is seeking to shift virtually all of its Medicaid population from government coverage into private plans starting in July 2012.

Two states, Massachusetts and Utah, each have existing state exchanges that differ fundamentally. The Massachusetts exchange is considered an “active purchaser” model, has a large organization and a sizeable budget. The state’s model does not allow all licensed insurers to participate in the exchange. The Utah model, on the other hand, is an “all-comer” model that allows any licensed health insurer to participate. Utah’s exchange initiative is much smaller in scope with only two full-time employees and a limited budget. Currently, the Massachusetts state exchange is suffering major cost overruns.

Rebecca Vesely, writing in Business Insurance, makes this clear in her article describing how two states, Vermont and Florida, are taking strikingly different paths in addressing health care reform. Vermont has taken the first step toward creating a single payer system by 2017. Legislation to set up a five member board to move the state in this direction has already been enacted. And while many details need to be worked out (funding, to name one) and Vermont will need to obtain a waiver from the Centers for Medicare and Medicaid Services to put the package together, the state is further down the road to single payer than any other.

With healthcare becoming a hot issue for 2012 both parties are entrenched. Democrats are promoting Medicare as an effective low cost plan that provides insurance for millions of people. The fact that it is imploding is seemingly lost. Republicans, on the other hand, are touting touting free enterprise system but the Medicare Part D law enacted by Bush in 2003 had been under estimated by half! Along with Medicare Advantage plans that have cost the Gov in excess of what was expected.

Rita Redberg, UCF professor of medicine writes an amazing editorial in NYT “Squandering Medicare Money”. While this war of words by both parties goes on no one is really minding the issues. There are things that can be done right now while Washington tries to get its own house in order. An honest appraisal of Medicare Advantage shows that the program doesn’t deserve a fatter payday; it demands a serious crackdown.

Limitations on funding both at the federal and state levels will need to be addressed to avoid a rise in government deficit levels. In the short term, PPACA will continue to face significant political and legal hurdles. Nonetheless, implementation will continue, with more provisions and offices becoming established under the law.

* * * * *

As more information becomes available, MMS Corp is committed to keeping you up-to-date in a timely manner. Coming soon 360peo.com to view past Legislative Alerts in the “Newsroom” section. Or, you may visit alexmiller.wordpress.com for blog posts, polls, surveys and numerous resources. If you have any questions, please contact us. Thank you for taking the time to read through this important notification.

Change in tax treatment for over-age dependent coverage

Accounting impact of change in Medicare retiree drug subsidy tax treatment

Early retiree medical reinsurance

Medicare prescription drug “donut hole” beneficiary rebate

Break time/private room for nursing moms

[/tab_item]

[tab_item title=”2011″]

No lifetime dollar limits on essential health benefits

Restricted annual dollar limits on essentail health benefits, phased amounts until 2014

No pre-existing condition limitations for enrollees up to age 191 and no recissions

No health FSA/HRA/HSA reimbursement for non-prescribed drugs

Increased penalties for non-qualified HSA distributions

Additional standards for new or “non-grandfathered” health plans, including preventive care in network with no cost-sharing appeal and external review, provider choice and non-discrimination provisions for insured plans

Income-based Medicare Part D premiums

Pharmaceutical importers and manufacturers’ fees start

Medicare, Medicare Advantage benefit and payment reforms

Insurers subject to medical loss ratio rules

[/tab_item]

[tab_item title=”2012″]

Employers to distribute uniform summary of benefits and coverage (SBC) to participants (deadlines vary with group of recipients)

60-day advance notice of mid-year material modifications to SBC content

Form W-2 reporting for health coverage (track in 2012 for W-2 form provided in early 2013)

Coverage for additional women’s preventive care services5

[/tab_item]

[tab_item title=”2013″]

$2,500 per plan year health FSA contribution cap (plan years on or after January 1, 2013)

Comparative effectiveness group health plan fees first due

Annual dollar limits on essential health benefits cannot be lower than $2 million

Employers notify employees about exchanges

Medical device manufacturers’ fees start

Higher Medicare payroll tax on wages exceeding $200,000/individual; $250,000/couples

Change in Medicare retiree drug subsidy tax treatment takes effect

Health Insurance exchanges initial open enrollment period

[/tab_item]

[tab_item title=”2014″]

Health insurance exchanges

Individual coverage mandate

Financial assistance for exchange coverage of lower-income individuals

States Medicaid expansion (possibly only some states)

Employer shared responsibility

Dependent coverage to age 26 for any covered employee’s child

No annual dollar limits on essential health benefits

No pre-existing condition limits

No waiting period over 90 days

Wellness limit increase allowed

Health insurance industry fees

Additional standards for non-grandfathered health plans, including limits on out-of-pocket maximums,

provider nondiscrimination, and coverage of routine medical costs of clinical trial participants

Small market, non-grandfathered insured plans must cover essential health benefits with limited deductibles (initially $2,000/individual, $4,000/family), using a form of community rating

Insurers must apply guaranteed issue and renewability to non-grandfathered plans of all sizes

Auto enrollment sometime after 2014

[/tab_item]

[tab_item title=”2015″]

Temporary reinsurance fees first due in late 2014/early 2015

Additional employee-specific reporting and disclosure of 2014 coverage

[/tab_item]

[tab_item title=”2018″]

40% excise tax on “high cost” or Cadillac coverage