ACA Marketplace and Employer Health Plan Cost Comparison

Are you ready for 2016 Individual Open Enrollment? The #1 question we get form individuals is am I better off staying on the individual plan or joining my small employer group plan?

Starting Nov 1, 2015, the 3rd anniversary of Obamacare’s ACA Marketplace begins. Continuing through 2018, several new parts of the Affordable Care Act that affect costs and benefits will be rolled out. The remaining provisions will take effect against a backdrop of new patterns in health care spending and trends.

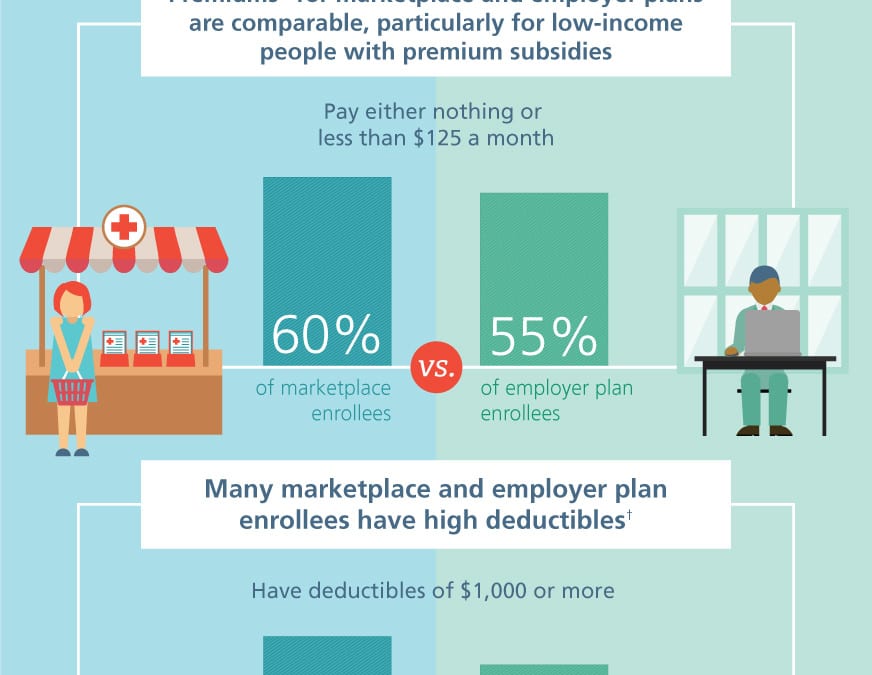

A frequent Employer question is how do costs compare on the ACA Marektplace vs. Employer Health Plans. The infographic from the Commonwealth Fund point out that the premiums are more favorable when factoring low income premium subsidies. In order to even the scales, an individual must earn $23,500 for a net subsidized premium of $125/month (click Kaiser calculator). This number represents 60% of marketplace enrollees. The same $125/month contribution amount represents 55% of employer health plans.

One positive point is that U.S. health care spending has slowed in the past few years. In a recent 16-month period, nearly 23 million Americans have enrolled in the Affordable Care Act, while almost 6 million people lost coverage. Research from Rand Corp. finds that of the newly insured:

42 percent are covered through employer-sponsored plans.

29 percent are enrolled in Medicaid.

18 percent have health coverage in individual marketplaces.

Take a look at the infographic:

2016 Open Enrollment Deadlines:

November 1, 2015: Open Enrollment starts — first day you can enroll in a 2016 insurance plan through the Health Insurance Marketplace. Coverage can start as soon as January 1, 2016.

FYI2016 plans and prices will be available for preview the third week of October, 2015.

December 15, 2015: Last day to enroll in or change plans for new coverage to start January 1, 2016.

January 1, 2016: 2016 coverage starts for those who enroll or change plans by December 15.

January 15, 2016: Last day to enroll in or change plans for new coverage to start February 1, 2016

January 31, 2016: 2016 Open Enrollment ends. Enrollments or changes between January 16 and January 31 take effect March 1, 2016.

If you don’t enroll in a 2016 health insurance plan by January 31, 2016, you can’t enroll in a health insurance plan for 2016 unless you qualify for a Marketplace Special Enrollment Period.

Penalty: The uninsured penalty rises to $695 or 2.5% of your income, whichever is higher.

Coverage start dates

If you enroll before the 15th of any month, your coverage starts the first day of the next month. If you enroll after the 15th of the month, you’ll have to wait until the month after that for your coverage to start. So, for example, if you enroll on January 16, your coverage would start on March 1.

Enroll using our online comparison shopping tool for both on and off-Exchange Marketplace to be released next week. Email us or Contact us at (855)667-4621.

Breaking News: NSLIJ, and Brooklyn’s Maimonides Announce Strategic Partnership on Wednesday. Both side shave been in talks since February.

Eventually North Shore-LIJ and Maimonides will fully integrate, “in a phased approach that will begin immediately,” the two jointly announced Wednesday. In the meantime, both institutions maintain their independence and separate governance structures. Lynam said there was no specific time frame for full integration.

Maimonides gets much-needed cash — tens of millions of dollars — for capital and operational investments. That will help it compete with Presbyterian-backed Methodist and Langone-backed Lutheran. North Shore-LIJ gets its first real foothold in #Brooklyn, one of the most competitive health care markets in the nation. But it does so without the commitment that a full-scale merger would entail. An affiliation agreement also protects North Shore-LIJ from unknown liabilities related to the Federation of Jewish Philanthropies, a malpractice insurer that covers Maimonides and several other hospitals

North Shore-LIJ has made strategic partnerships and acquisitions before. For North Shore-LIJ, the relationship means it has a hospital or hospitals in every borough as well as blanketing Westchester and Long Island. North Shore-LIJ, the country’s 14th largest health care system, owns 19 hospitals. In the city that includes Lenox Hill Hospital in Manhattan, Staten Island University Hospital, and, in Queens, Forest Hills Hospital, Long Island Jewish Medical Center, Cohen Children’s Medical Center and Zucker Hillside Hospital, a behavioral health center.

They are also actively insuring members today in the Downstate NY area under the CareConnect NSLIJ holding company. With important advantages under ACA and mindful of delivering value the insurance arm is priced affordably. In fact they had lowered their rates 15-20% for 2015 and and industry low 3.3% for 2016.

MMS, Inc. in partnership with BenefitMall adds allCheck ACA compliance tool! Want to know how to easily calculate your FTE’s ( Full Time Equivalents)? Not sure if you need to provide the Notice of Exchange? Unsure about your Health Care Tax Credit Eligibility? Want to get an idea what your overall ACA compliance obligations might be?

Let MMS inc. and allCheck do the work. How? Its simple. Download the input sheet, complete and we will crunch the numbers and send you a customized report just like the sample! Please call us 855-667-4621.

This law is new and constantly evolving. We (and everyone else) are still processing the thousands of complex provisions. The calculations here will change based upon your input, and is meant to be an educational tool for you to use in understanding how healthcare reform may impact your business. We recommend you work closely with your broker and local counsel to receive the most accurate and up-to-date information.

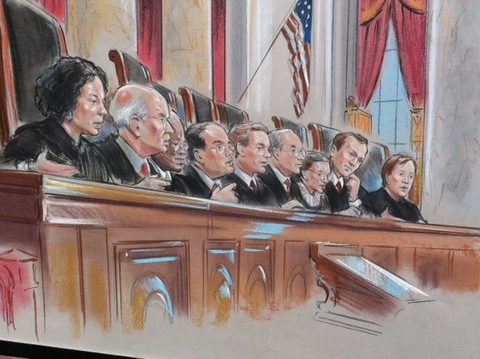

The U.S. Supreme Court ruled this morning that the Affordable Care Act may provide nationwide tax subsidies for people who purchase health insurance through an exchange. The Court considered a challenge to a provision of the ACA concerning whether subsidies were available only to those who purchased health insurance on an exchange “established by the state.” The Court, in King v. Burwell, ruled 6 to 3 in favor of upholding the eligibility for people to receive subsidies through either a state or federal health insurance exchange.

The opposite ruling would have had serious implications for the country due to the number of states relying on a federally-run exchange (37 states) and the number of customers who qualify for subsidies based on their income (about 85% of customers nationwide). The Government’s argument prevailing: defending the subsidies, the Government argued that if you look at the entire ACA and its history, it is clear that the subsidies are available to everyone who purchases insurance on an exchange, no matter who created it.

Please join us for upcoming Webinar on How to Prepare for Current and Future ACA Requirements.

Are you able to identify and address all of the ACA requirements? Have you developed a plan of action to help stay in compliance? This webinar will walk you through a three year case study and provide you with current and future solutions to help your group prepare for ACA challenges including the Cadillac Tax.

Some of the key webinar highlights include:

Will Federal subsidies stop in some states making residents unable to access subsidized Exchange coverage?

3 year case study providing a practical view

Will IRS information reporting still be required?

Could Congress step in and propose changes to the existing ACA law?

2015 – Section 125 changes including eligibility, PRAs, excepted benefits and FSA plans for higher OOP exposure

2016 – Renewal focus on HSA’s with a dollar for dollar matching contribution

2017 – Further conversation of reducing benefit costs utilizing post deductible HRA’s and consideration of Defined Contributions

Practical information you can use – a webinar you will not want to miss!

The King Ruling awaits As Supreme Court schedules more decision days. The decision is expected to be possibly on Thursday on the legality of the Health care subsidies. ISSUE RECAP: At issue is whether subsidies that 8.7 million people receive to help pay for their insurance are available in all 50 states, or only those that set up their own health insurance exchanges. (more…)

Great news for families with HSA and high deductible plans. Individual out of pocket maximums will apply EVEN UNDER A FAMILY POLICY. New federal health care reform law regulatory guidance ends lingering uncertainty on how much in out-of-pocket costs employers with high-deductible plans can require employees to pick up.

The guidance, leaves intact the maximum out-of-pocket expenses employers can require employees to pay before health plan coverage kicks in: $6,850 for single coverage and $13,700 for family coverage when the rules go into effect in 2016.

An example illustrates how the HHS-imposed “EMBEDDED” limit on out-of-pocket expenses will work:

An employee and his or her spouse enroll in family coverage with an annual cost sharing limit of $13,000, and during the 2016 plan year, $10,000 of cost sharing payments are attributable to the spouse and $3,000 of cost sharing payments are attributable to the employee. Prior to the HHS’s clarification, the full $13,000 would be payable by the covered individuals because the $13,000 plan limit had not been reached on an aggregate basis. However, with the new EMBEDDED self-only limitation, the cost sharing payments attributable to the spouse must be capped at the self-only limit of $6,850, with the remaining $3,150 being covered 100% by the group health plan. The employee would still be subject to cost sharing, however, until the $13,000 plan limit is reached.

The biggest impact on the new cost-sharing rules will be on employers with high-deductible plans.

For the FAQs, visit: http://www.dol.gov/ebsa/pdf/faq-aca27.pdf

For more information and a free renewal evaluation please