ACA Marketplace and Employer Health Plan Cost Comparison

Are you ready for 2016 Individual Open Enrollment? The #1 question we get form individuals is am I better off staying on the individual plan or joining my small employer group plan?

Starting Nov 1, 2015, the 3rd anniversary of Obamacare’s ACA Marketplace begins. Continuing through 2018, several new parts of the Affordable Care Act that affect costs and benefits will be rolled out. The remaining provisions will take effect against a backdrop of new patterns in health care spending and trends.

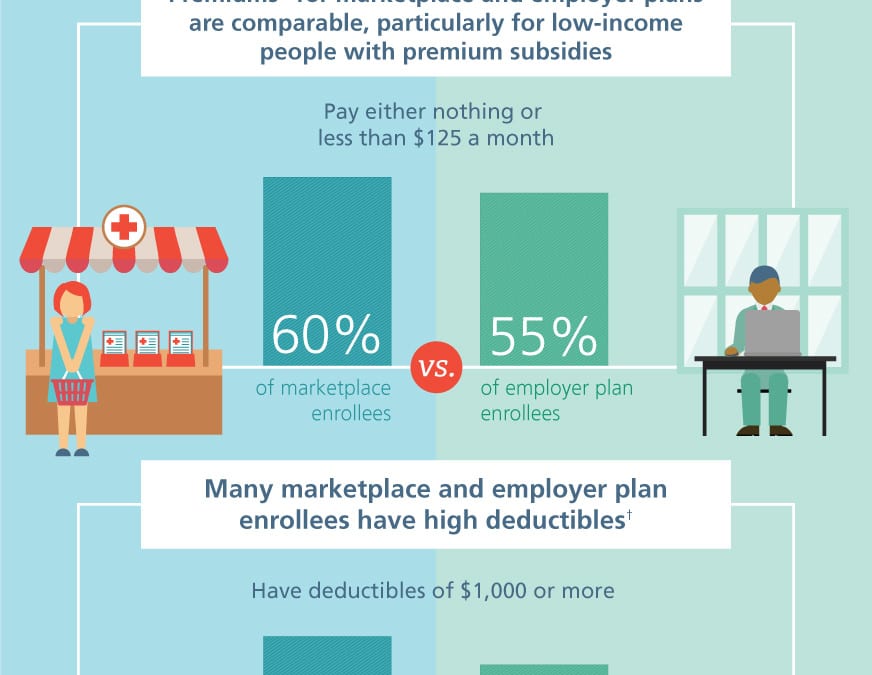

A frequent Employer question is how do costs compare on the ACA Marektplace vs. Employer Health Plans. The infographic from the Commonwealth Fund point out that the premiums are more favorable when factoring low income premium subsidies. In order to even the scales, an individual must earn $23,500 for a net subsidized premium of $125/month (click Kaiser calculator). This number represents 60% of marketplace enrollees. The same $125/month contribution amount represents 55% of employer health plans.

One positive point is that U.S. health care spending has slowed in the past few years. In a recent 16-month period, nearly 23 million Americans have enrolled in the Affordable Care Act, while almost 6 million people lost coverage. Research from Rand Corp. finds that of the newly insured:

42 percent are covered through employer-sponsored plans.

29 percent are enrolled in Medicaid.

18 percent have health coverage in individual marketplaces.

Take a look at the infographic:

2016 Open Enrollment Deadlines:

November 1, 2015: Open Enrollment starts — first day you can enroll in a 2016 insurance plan through the Health Insurance Marketplace. Coverage can start as soon as January 1, 2016.

FYI2016 plans and prices will be available for preview the third week of October, 2015.

December 15, 2015: Last day to enroll in or change plans for new coverage to start January 1, 2016.

January 1, 2016: 2016 coverage starts for those who enroll or change plans by December 15.

January 15, 2016: Last day to enroll in or change plans for new coverage to start February 1, 2016

January 31, 2016: 2016 Open Enrollment ends. Enrollments or changes between January 16 and January 31 take effect March 1, 2016.

If you don’t enroll in a 2016 health insurance plan by January 31, 2016, you can’t enroll in a health insurance plan for 2016 unless you qualify for a Marketplace Special Enrollment Period.

Penalty: The uninsured penalty rises to $695 or 2.5% of your income, whichever is higher.

Coverage start dates

If you enroll before the 15th of any month, your coverage starts the first day of the next month. If you enroll after the 15th of the month, you’ll have to wait until the month after that for your coverage to start. So, for example, if you enroll on January 16, your coverage would start on March 1.

Enroll using our online comparison shopping tool for both on and off-Exchange Marketplace to be released next week. Email us or Contact us at (855)667-4621.

BREAKING: The young Co-Op start up of 2014 will be shutting down Dec 31, 2015. With membership totals approx. 200,000+ the early exit comes as a shocking surprise despite their recent losses and 15-20% rate increase approved for 2016.

On Friday, a joint announcement came from the state Department of Financial Services, the Department of Health and the federal Centers for Medicare and Medicaid Services (CMS), with DFS directing Health Republic to cease writing new health insurance policies and begin an orderly wind-down of business.

“Given Health Republic’s financial situation, commencing an orderly wind down process before the upcoming open enrollment period is the best course of action to protect consumers,” said Anthony Albanese, acting superintendent at DFS. “Moving forward, we will work closely with New York State of Health and federal regulators to help ensure continuity of coverage for Health Republic’s customers.”CMS officials said decision was made after state and federal agencies determined it was likely Health Republic would become financially insolvent.

According to recent announcements Health Republic of NY was exiting the small group and individual markets for Mid-Hudson, Albany, and Utica/Watertown regions. These counties include: Albany, Columbia, Delaware, Dutchess, Essex, Greene, Hamilton, Oneida, Orange, Oswego, Putnam, Rensselaer, Saratoga, Schenectady, Sullivan, Ulster, Warren, and Washington. The reasoning was the high delivery costs driven by Provider consolidation, see https://healthrepublicny.org/media/2563/faqs-service-area-reductions.pdf.

With recent exits for Insurers such Atlantis, Emblem Health/GHI and Empire blue Cross the transitions were handled differently. Some allowed groups to see their plan through renewal anniversary date or end of year. Further announcements are expected on transition of coverage.

Our Agency as in the past will be out and early in front positioning our clients for best options. For more information on this or to schedule a call please contact us info@medicalsolutionscorp.com today.

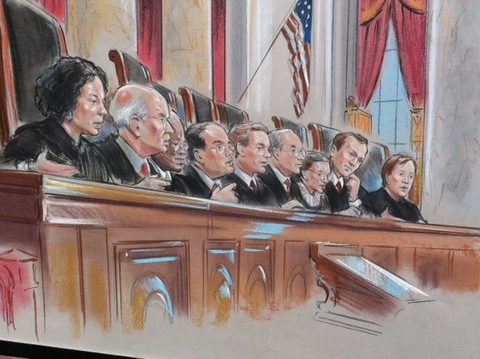

The U.S. Supreme Court ruled this morning that the Affordable Care Act may provide nationwide tax subsidies for people who purchase health insurance through an exchange. The Court considered a challenge to a provision of the ACA concerning whether subsidies were available only to those who purchased health insurance on an exchange “established by the state.” The Court, in King v. Burwell, ruled 6 to 3 in favor of upholding the eligibility for people to receive subsidies through either a state or federal health insurance exchange.

The opposite ruling would have had serious implications for the country due to the number of states relying on a federally-run exchange (37 states) and the number of customers who qualify for subsidies based on their income (about 85% of customers nationwide). The Government’s argument prevailing: defending the subsidies, the Government argued that if you look at the entire ACA and its history, it is clear that the subsidies are available to everyone who purchases insurance on an exchange, no matter who created it.

Please join us for upcoming Webinar on How to Prepare for Current and Future ACA Requirements.

Are you able to identify and address all of the ACA requirements? Have you developed a plan of action to help stay in compliance? This webinar will walk you through a three year case study and provide you with current and future solutions to help your group prepare for ACA challenges including the Cadillac Tax.

Some of the key webinar highlights include:

Will Federal subsidies stop in some states making residents unable to access subsidized Exchange coverage?

3 year case study providing a practical view

Will IRS information reporting still be required?

Could Congress step in and propose changes to the existing ACA law?

2015 – Section 125 changes including eligibility, PRAs, excepted benefits and FSA plans for higher OOP exposure

2016 – Renewal focus on HSA’s with a dollar for dollar matching contribution

2017 – Further conversation of reducing benefit costs utilizing post deductible HRA’s and consideration of Defined Contributions

Practical information you can use – a webinar you will not want to miss!

“The deadline for individuals and families to enroll in a qualified health plan through NY State of Health is February 15, 2015. However, the Marketplace will provide additional assistance to those individuals who have taken steps to apply for coverage but have been unable to complete the enrollment process before the deadline. All applications and enrollments in health plans must be completed by the end of the day on February 28, 2015. Those who complete their enrollment after February 15, 2015 but on or before February 28, 2015 will have coverage starting on April 1, 2015.”

2/12/15

Last days for 2015 Individual Open Enrollment is ending this week. This deadline applies to both On and Off Exchange!

If you’re wondering about the penalty for not having insurance: yes, there is one, and no, you can’t really get out of paying for it. You’ll pay the penalty when you file your taxes for 2015. Even if you get coverage midway through the year, you’ll still need to pay a penalty for the months you weren’t insured. So get covered!

Think you might be eligible for a subsidy or aren’t sure?

You can check here at the New York State of Health Marketplace calculator. If you are eligible or think you might be eligible, you can contact the marketplace directly to purchase a plan or ask questions about financial assistance.

Please remember that during open enrollment you are permitted to switch carriers. Choose wisely because after February 15, one cannot switch plans until open enrollment 2015, unless you have a “qualifying event,” such as marriage, divorce, birth or adoption.

Individual Online Enrollment Resources for On and Off Exchange:

For NYS – To view Oscar’s plans, rates and simple online enrollment application, click here.

For more information on enrollment please contact our team at Millennium Medical Solutions Corp (855)667-4621. We have Spanish, Russian, and Hebrew speakers available.

What to do with the 1095-A form you received in the mail?

Attached below is the link to the web page with information on Premium Tax Credits and Form 1095-A. The resources on this link provide information on Form 1095-A, including Frequently Asked Questions and the toll free numbers provided for assistance.The resources on this page provide information about your Form 1095-A from NY State of Health. The Form 1095-A is used to reconcile Advance Premium Tax Credits (APTC) and to claim Premium Tax Credits (PTC) on your federal tax returns.

I didn’t apply to NY State of Health for financial assistance. Can you tell me if I can claim the PTC on my tax returns for 2014?

Who is in my tax family? How do I figure out if someone is a dependent?

How do I report health care coverage on my tax return?

How do I report the information from Form 1095-A on my tax return?

Do I need to complete Form 8962?

How do I complete Form 8962 on my tax return? How do I use the Form 1095-A to complete my Form 8962. What counts as income? What is my FPL?

Do I owe money to the IRS? Will I get a refund from the IRS? How much tax credits will I have to repay to the IRS? How much extra in tax credits will I get from the IRS?

I am self-employed. Can I claim my NY State of Health premiums as a business expense on my tax returns?

I had to pay back tax credits or got extra tax credits. Should I estimate my income differently for 2015?

How do I claim an exemption from the Individual Responsibility requirement?

Do I owe an Individual Share Responsibility Payment?

What income needs to be considered when calculating the Individual Shared Responsibility Payment?

I enrolled in a health plan with financial assistance and my income is now less than 100% FPL. Am I still eligible for the PTC?

If you have questions about Form 1095-A, Minimum Essential Coverage, PTC or the SLCSP table, call Community Health Advocates’ Helpline at 1-888-614-5400.

If you think we made a mistake on your 1095-A, call NY State of Health at 1-855-766-7860.

If you have questions about Form 8962 or other tax-related questions, visit www.irs.gov.

Please take the time to review. For more information, please

单击此处,了解 简体中文 保费税收抵免和 Form 1095-A 的相关信息。

Cliquez ici pour accéder à des informations sur les crédits d’impôt pour cotisation d’assurance et sur le Form 1095-A en français.

Klike la a pou jwenn enfòmasyon sou Kredi nan Taks sou Prim ak Form 1095-A nan Kreyòl Ayisyen.

Per ricevere maggiori informazioni in italiano sul credito d’imposta sul premio (Premium Tax Credit, PTC) e sul Form 1095-A, cliccare qui.

한국어로 된 보험료 세금 공제(Premium Tax Credits, PTA) 및 Form 1095-A에 대한 정보가 필요하신 경우 여기를 클릭하십시오.

Нажмите здесь, чтобы получить информацию о налоговых вычетах за страховые взносы и форме Form 1095-A на русском языке.

Haga clic aquí para obtener información en español acerca de los Créditos tributarios para la prima y el formulario 1095-A.

Open enrollment for the 2015 New York individual market season is right around the corner. Below are answers to commonly asked questions pertaining to individual market coverage for residents of New York State:

Q: What is the New York State of Health (NYSOH) exchange website? A:NYSOH provides NYS residents living between 139%-400% of the Federal Poverty Level, access to lower cost health insurance by supplying them with tax credit premium subsidies. Additional Cost Sharing subsidies are available to those living between 139%-250% of the FPL. All subsidy programs are subject to eligibility requirements. Additionally, NYSOH is where individuals can enroll in Medicaid (for those living below 139% of the FPL).

Q: Is the NYSOH government health insurance? Is that what “Obamacare” means? A: No. Individual health insurance is a relationship between a consumer, and a private health insurance company. NYOSH slips in between this relationship by forwarding tax credit money to the carrier on behalf of the subsidy-eligible consumer, and then the carrier bills the consumer for the difference in premium owed. “Obamacare” is simply the nickname of the new health insurance law, which (in part) assists individuals in obtaining health insurance.

Q: Do I have to have health insurance? A: Yes. As part of the individual mandate, all US citizens must enroll in Affordable Care Act-compliant health insurance…be it through your employer, the individual market, Medicare, or Medicaid. Citizens not enrolled in coverage will be fined by the IRS (less those who qualify for exemptions).

Q: What is the fine for not having health insurance? A: In 2015, the fine is 2% of household income per uninsured month. In 2016, this increases to 2.5% of household income per uninsured month.

Q: Do I have to enroll in individual coverage through NYSOH? A: No. Only people in need of tax credit subsidy assistance must enroll through the NYSOH exchange website.

Q: What if I don’t earn enough income to qualify for subsidy assistance for on-exchange health plans? A: People in NY living below 139% of the FPL will be eligible for Medicaid. Medicaid enrollments are conducted on the NYSOH website.

Q: If I am over the subsidy income limit threshold, how do I apply for coverage outside of the NYSOH website? A: You can enroll directly with a carrier, or, by contacting a licensed insurance broker for assistance. Off-exchange carrier applications are extremely simplified, requiring only a 1-2 page paper/PDF application to be completed in most cases, and with no government intervention.

Q: Can brokers assist me with my individual coverage written through the NYSOH website as well? A: Yes. Licensed brokers, who are also certified to write health plans on the exchange, can be found in the Broker directory on the NYSOH website. You can search using a specific broker’s first and last name, by selecting a specific Agency from the drop down list, or you can enter your ZIP Code to find one in your region.

Q: Do brokers charge fees for helping me secure an individual health plan? A: Brokers are not allowed to charge fees for assisting individuals with writing their health insurance.

Q: How do brokers get paid? A: Every time you pay your health insurance bill, a portion of your payment is allocated towards compensating a broker (just like with your auto or homeowners insurance). Most carriers pay broker commissions on the back end, which is completely transparent to the consumer. If no broker is utilized by the consumer, the carrier retains the commission. This means that whether you use a broker or not, you’ll be paying for one anyway.

Q: Don’t Navigators already provide these broker services? A: No. Sometimes referred to as “in person assistors” or “experts” by the NYSOH, Navigators are not licensed to write health insurance. They are trained employees or contracted agencies of the NYS government (funded by Federal grant money) to help individuals navigate the enrollment process on the NYSOH website only. They are not required by federal law to undergo criminal background checks, nor are they licensed by the NYS Department of Financial Services, which means they cannot make plan recommendations to health insurance consumers.

Q: Can a certified broker process my NYSOH enrollment for me? A: Yes. Brokers that are certified to write business on the NYSOH exchange website can drive the entire online enrollment process for the consumer. You just need to authorize a broker through your NYSOH account by logging in, and then clicking “Find a Navigator/Broker” towards the bottom left side of your NYSOH account home page. Once authorized, the broker you have selected will receive an email from the NYSOH that you are in need of assistance, and can now enroll you on your behalf.

Q: When can I enroll in individual health insurance? A: Like Medicare, the individual health insurance market is setup to have an open enrollment season. The individual market open enrollment window is from 11/15/14 through 2/15/15.

Q. Are there any exceptions to the open enrollment period?

A. Enrollment in Medicaid, Child Health Plus and the Small Business Marketplace continues all year.

Have a Qualifying Event?

Enroll Now using our online shopping tool where you can compare plans and prices and enroll

Find us on the Health Insurance Marketplace where you may qualify for help to pay for your health insurance. Qualifying Events for Exchange Marketplace. 76 percent of the uninsured are unaware of the looming March 31 sign-up deadline. Contact us at (855)667-4621.

Q: Can I enroll in coverage outside of the open enrollment season? A: Consumers can enroll in individual coverage outside the open enrollment season so long as a “Qualifying Life Event” exists. Examples of such events include the loss of a job, marriage, divorce, birth of a child, a change in subsidy eligibility, and others. Written proof of the QLE will be required when enrolling outside of the open enrollment season as established by the US Department of Health and Human Services.

Q: If I am subsidy eligible, and my income changes, what do I do? A: Consumers enrolled through the exchange who receive tax credits must notify the NYSOH Marketplace whenever a change of income is experienced. You can contact the marketplace call center at 855-355-5777 to update your income information.

Q: Am I limited to certain insurance companies if I am subsidy-eligible? A: No. Consumers who are subsidy-eligible may pick any plan they wish that is available on the NYSOH exchange website. However, subsidy-eligible individuals may not apply those tax credits towards health plans written outside of the NYSOH website (for example, Oxford Liberty plans, which are only available outside of the NYSOH Marketplace).

Q: I have completed the income portion of my on-exchange application, and I’m now ready to pick a plan. How can I find out more specific information pertaining to the available options in the market? A: A licensed insurance broker can help you understand the available health plans in the market, and can make plan recommendations specific to your needs and financial situation.

Q: I started my current individual plan in July 2014. Do I have to renew my plan on January 1st 2015? A: Yes. All individual market plans have calendar year deductible and maximum out of pocket accumulation periods, which resets on January 1st of any given year. So for example, if you lost your job (and your health insurance) effective 12/1/14, and then you enroll for individual coverage effective 12/1/14, you must renew your individual plan the following month (for 1/1/15) at the new carrier plan structures and rates.

Q: I already have individual market based health insurance. Can I change plans during the open enrollment season? A: Yes. Existing individual health insurance policyholders may change their plan during the open enrollment season. You may also change carriers should you wish to find a better solution for your needs. Talk to your licensed insurance broker about the available plan options in the market for 2015.

Q: My employer is offering me a health plan that I am not interested in. Can I waive my employer health plan and replace it with an individual plan, and receive tax credit subsidy assistance? A: The answer to the first part of the question is yes. Employees can choose to opt out of employer-sponsored health insurance, and can replace their coverage in the individual market.

With regards to receiving tax credit subsidies in these situations, yes, an individual can receive tax credit subsidies to help pay the cost of individual health insurance. However, in addition to the employee needing to meet tax credit eligibility requirements as discussed earlier, one of two additional conditions must be met to be eligible to receive subsidy assistance: 1) The employer’s health plan does not meet the minimum actuarial value of 60%, or 2) The employee’s single rate cost (self-only coverage, no dependents) for employer-sponsored coverage exceeds 9.5% of their household adjusted gross income (defined as “unaffordable” under the health care law).

Q: I’m applying for a tax credit subsidy. How do I determine my adjusted gross income? A: Your adjusted gross income can be found on line 37 of your 1040 tax return. Subsidy applicants who have a steady income can use this figure as a guide when determining tax credit eligibility for the upcoming tax year.

Those that do not have a steady income (e.g. sole proprietors, freelancers, single-person businesses, etc.) should speak with their accountants to determine their estimated adjusted gross income for the upcoming tax year.

Q: I was determined Medicaid eligible after applying for tax credit subsidy on the NYSOH website. However, my doctors do not take Medicaid. Can I opt out of medicaid and get a subsidized individual health plan instead? A: You may choose to opt out of Medicaid if you wish. However, those who are Medicaid eligible will not qualify for tax credit subsidies for individual health plans. You can enroll in a health plan, but you must pay the full price of the plan.

Q: I was determined subsidy eligible, and I want to pick a plan to enroll in through the NYSOH website. Can I put my children on my health plan with my spouse and I? A: No. Those who are subsidy eligible must insure their dependent children through a Child Health Plus plan. CHP (or “chip”) plans are selected during the plan check out process at the end of the NYSOH application. Only the applicant and spouse will qualify for a private health plan with subsidy assistance. If you choose to opt your children out of CHP, you and your spouse will lose subsidy eligibility for your private health plan.

Q: How can I find out if my doctors take a particular health plan? A: Your licensed insurance broker can provide you with carrier-specific tools to look up providers in particular networks.

Q: How can I get a copy of the full benefit summary for a particular health plan I’m interested in? A: Your licensed insurance broker can provide you with electronic benefit summaries for most health plans upon request.

Q: How can I find a licensed broker to assist me? A: Licensed insurance brokers, and who are also certified to write on-exchange plans, can be found in the Broker directory on the NYSOH website. You can search using a specific broker’s first and last name, by selecting a specific Agency from the drop down list, or you can enter your ZIP Code to find one in your region.

For more information regarding both Exchanges – Individual Exchanges or SHOP please contact our team at Millennium Medical Solutions Corp (855)667-4621. We have Spanish, Russian, and Hebrew speakers available. Quotes can also be viewed on our site.