by Alex | Jun 2, 2016 | Health Care Reform, Healthy NY, Individual Exchanges, NY News

NYS Obamacare Lost $100 Million

NYS Obamacare Lost $100 Million

According to a released study by United Hospital Fund May 2016 report Insurance companies operating on New York’s individual exchange market lost $100 million in 2014.

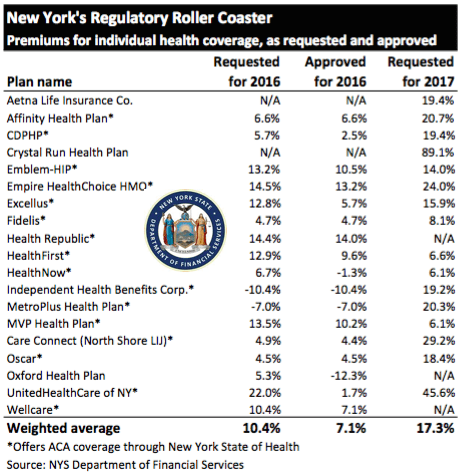

With recent news of Insurers reporting mounting losses (UnitedHealthcare will drop ACA exchanges) on the Individual Marketplace it wouldn’t be surprising for the next year’s Study to show even greater losses in 2015. As reported last month, the average NYS 2017 Rate Requests for individual marketplace was 17.3%.

Lower premiums, reinsurance and subsidies made coverage more affordable. “For many years in New York, annual individual premium increases far outpaced the offsetting effects of both a $38 million state-funded reinsurance program,12 and a risk-adjustment mechanism that provided a cross-subsidy from the small group market to the individual market, valued at $62 million in 2009.13 In 2014, new enrollment, PHSP participation, more competitive pricing, a better risk pool, and a federal reinsurance program resulted in an average individual monthly premium of $430.97 in New York.” The ACA subsidies reduced premiums by an average of $215/month

NYS Obamacare Future?

“More affordable premiums have been a key factor in the growth of the individual market. The loss of federal reinsurance payments will create an upward pressure on rates, and the absence of federal risk corridor reimbursement will also continue to reverberate.” Consumers with Obamacare subsidies will be shielded from most of the premium increases that may occur, but off-Exchange enrollees and NYSOH customers without subsidies could face significant monthly increases.

Read the UHF report here:

NYS Obamacare Study by United Hospital Fund

by Alex | May 19, 2016 | group health insurance, Health Exchanges, Individual Exchanges, individual health insurance, NY News, PPACA, Small Business Group Health

NYS 2017 Rate Requests

The State released NYS 2017 Rate Requests with average increases of 17.3% individual market and 12% for small groups. This early 5/12/16 deadline request requirement is not an Obamacare requirement. As per NY State Law carriers are required to send out notices of rate increase filings to groups and subscribers.

With only 3 months of mature claims in 2016 to work of off Insurance Actuaries have little experience to predict accurate projections. Typically the rate requests must be high and in the past final approvals after negotiations were only half, see https://360peo.com/nys-2016-rates-approved/. The national rate trend, however, has been much higher than in past years due to higher health care costs and the loss of Federal reinsurance fund known as risk reinsurance corridor.

This is one of the reasons why the individual market is significantly more costly to operate than small group as per recent United Healthcare pull out of most State Individual Exchanges, UnitedHealthcare will drop ACA Exchanges. In fact, the Health Republic NY is Shutting Down highlights how an insurer banked on the federal risk corridor reinsurance and underestimated NYS costs of care. Another local example is Oscar Health Insurance which has lost $105 million and is asking for up to 30% rate increase. The 3 year old company said the increase was necessary because medical costs have risen, government programs that helped cover costs are ending, and its members needed more care than expected. That all translates into the need for a price correction.

Importantly, the individual market subsides may be on borrowed time. Last week, The Federal Court ruled that Obamacare subsidies were illegally funded. The ruling while the Obama administration challenges it in D.C. Circuit Court of Appeals, is still allowing the reimbursements to continue for now. The practice of some small businesses dropping group health insuarnce in favor of the Individual Plans known as “cash for insurance” is put into question by this. While the IRS ruled that this is prohibited (see below) some small business are attracted to the simplicity of a public exchange and not getting involved in the managing of plans. Prohibited: The IRS prohibits employers from giving (or reimbursing) employees pre-tax funds to buy health insurance on their own—through the state-based and federally facilitated exchanges or private marketplaces alike.1 This practice may result in a $100 per day excise tax per applicable employee, according to an IRS Q&A released in May 2014.2

Instead, the correct approach for a small business in keeping with simplicity is a Private Exchange. This is a true defined contribution empowering employees with choice of leading insurers offering paperless technologies integrating HRIS/Benefits/Payroll. Both employee and employers still gain tax advantage benefits under the business. Also, the benefits, rates and network size are superior under a group plan as THE RISK OUTLINED ABOVE ARE HIGHER FOR INDIVIDUAL MARKETS THAN SMALL GROUP PLANS.

For more information on how a Private Exchange can help your group please Contact us at (855)667-4621.

Summary of 2017 Requested Rate Actions

INDIVIDUAL MARKET

| Company Name | 2017 Requested Rate Change |

|---|

| Aetna Life Insurance Company | 19.4% |

| Affinity Health Plan, Inc.* | 20.7% |

| Capital District Physicians’ Health Plan* | 11.2% |

| Crystal Run Health Plan, LLC* | 89.1% |

| Empire HealthChoice HMO, Inc.* | 24.0% |

| Excellus Health Plan, Inc.* | 15.9% |

| Health Insurance Plan of Greater New York* | 14.0% |

| Healthfirst PHSP, Inc.* | 6.6% |

| HealthNow New York Inc.* | 6.1% |

| Independent Health Benefits Corporation* | 19.2% |

| MetroPlus Health Plan, Inc.* | 20.3% |

| MVP Health Plan, Inc.* | 6.1% |

| New York State Catholic Health Plan, Inc. dba Fidelis Care New York* | 8.1% |

| North Shore-LIJ CareConnect Insurance Company, Inc.* | 29.2% |

| Oscar Insurance Corporation* | 18.4% |

| UnitedHealthcare of New York, Inc.* | 45.6% |

| Weighted Average Requested Rate Change – Individual Market | 17.3% |

*Indicates that the company makes products available on the “New York State of Health” marketplace.

SMALL GROUP MARKET

| Company Name | 2017 Requested Rate Change |

|---|

| Aetna Life Insurance Company | 12.0% |

| Capital District Physicians’ Health Plan, Inc. | 9.6% |

| CDPHP, Universal Benefits Inc.* | 11.6% |

| Crystal Run Health Insurance Company, Inc. | 61.9% |

| Crystal Run Health Plan, LLC | 66.6% |

| Empire Healthchoice Assur Inc | 10.0% |

| Empire HealthChoice HMO, Inc. | 12.6% |

| Excellus Health Plan, Inc.* | 12.3% |

| Health Insurance Plan of Greater New York* | 10.6% |

| Healthfirst Health Plan (Managed Health) | 5.0% |

| HealthNow New York Inc.* | 5.8% |

| Independent Health Benefits Corporation* | 11.2% |

| MetroPlus Health Plan, Inc.* | 13.1% |

| MVP Health Plan, Inc.* | 5.4% |

| MVP Health Services Corp. | 6.8% |

| North Shore-LIJ CareConnect Insurance Company, Inc.* | 16.8% |

| Oxford Health Insurance, Inc.* | 12.9% |

| UnitedHealthcare Insurance Company of New York | 12.8% |

| Weighted Average Requested Rate Change – Small Group Market | 12.0% |

*Indicates that the company makes products available on the “New York State of Health” marketplace.

Source: https://myportal.dfs.ny.gov/web/prior-approval/summary-of-2017-requested-rate-actions

Resource:

by Alex | Apr 20, 2016 | healthcare, Individual Exchanges, individual health insurance, latest health insurance news, Obamacare, State Exchanges, United Healthcare

UnitedHealthcare will drop ACA exchanges

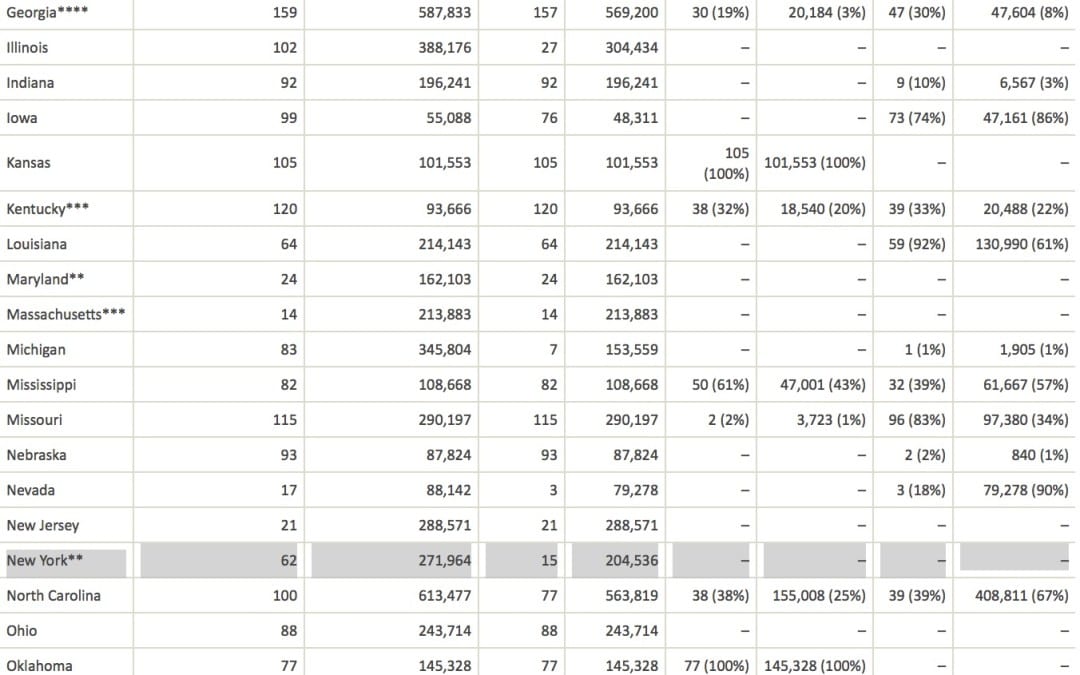

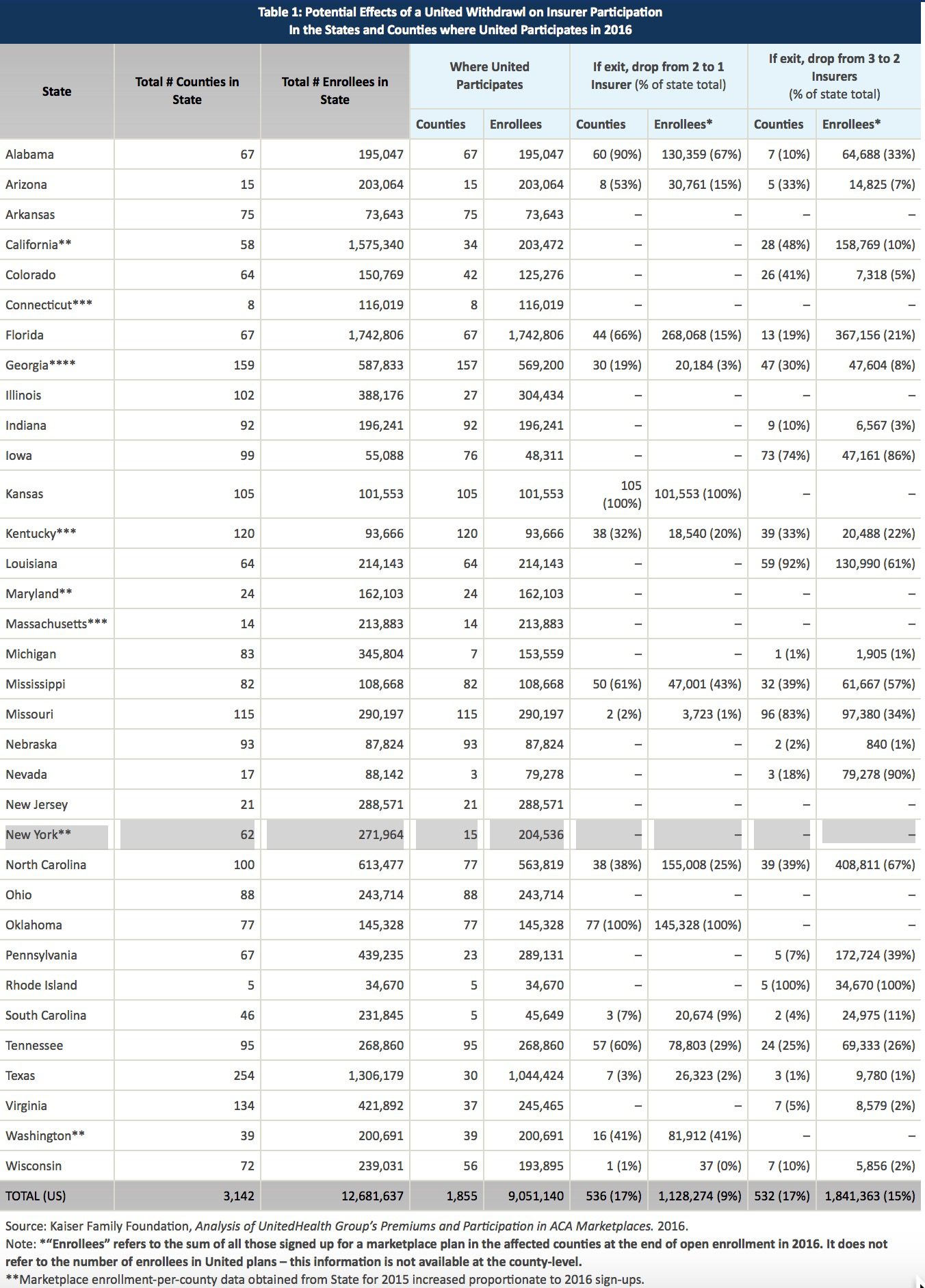

UnitedHealthcare Individual by State

BREAKING:

So far, New York and Nevada have confirmed that UnitedHealth plans to remain on their ACA exchanges next year. The company has also filed plans to participate in Virginia for 2017. Wisconsin said it hasn’t received an exit notice from UnitedHealth, and that it doesn’t comment on insurers’ business plans. A representative of Covered California, the state’s Obamacare exchange, said plan participation is confidential until it’s announced later this year.

UnitedHealthcare will drop out of most ACA Exchanges by 2017 as reported in Modern Healthcare. Just how significant is this to the market? Realistically, United took a cautious wait and see approach. In NYS, for example, they have been the most expensive plan on the Obamacare Exchange Marketplace. They expect to lose over a billion dollars in this space for 2015 and 2016, so to them it makes no sense to stay in that market. The concern for the individual market is to expect large pricing increases in 2017 to reflect the higher risk than the safer Group Market.

UnitedHealth, which had about 795,000 ACA customers as of March 31, warned in November that it was posting losses on ACA policies. In December, the company said it should have stayed out of the individual exchange market longer. UnitedHealth also is withdrawing from some related state insurance markets for small businesses.

See United-healthcare Individual members enrolled by State:

UnitedHealthcare will drop ACA exchanges

MODERN HEALTHCARE

By Bob Herman

April 19, 2016

UnitedHealth Group CEO Stephen Hemsley said Tuesday the health insurance and services conglomerate will pull out of most of its Affordable Care Act marketplaces. But the company won’t bail on the exchanges completely and will sell individual plans in a “handful” of states.

“We cannot broadly serve it on an effective and sustained basis,” Hemsley told analysts and investors on a conference call. UnitedHealth has fully or partially exited five states so far—Arkansas, Georgia, Louisiana, Michigan and Oklahoma, according to various news reports.

The company sold plans in 34 states for this policy year and did not disclose which states it will stay in. Insurers that sell plans through the federal HealthCare.gov portal have until May 11 to file rates for 2017 plans.

A new analysis from the Kaiser Family Foundation, however, notes that UnitedHealth’s exits would only have a modest effect on competition and prices nationally since it has a small ACA footprint and charged higher premiums from the outset.

UnitedHealth recorded an additional $125 million loss on its individual ACA plans, meaning the company’s total ACA losses for 2015 and 2016 will exceed $1 billion. UnitedHealth signed up many sicker-than-expected members, ending the first quarter with 795,000 public exchange enrollees, which is only a fraction of the ACA’s individual market.

The insurer also overpriced its plans in 2015 after barely participating on the exchanges in 2014. UnitedHealth expects its exchange membership will decline to 650,000 by the end of the year.

But despite those heavy losses, which UnitedHealth previewed late last year, the company’s other lines of business like Medicare Advantage and Optum have been making money at a healthy clip. UnitedHealth’s profit climbed 14% year over year, totaling $1.6 billion in the first three months of this year. Adjusted earnings per share rose 17% to $1.81, beating estimates on Wall Street.

Revenue soared almost 25% to $44.5 billion in the first quarter, putting UnitedHealth on pace to hit $182 billion of revenue for the year. The Minnetonka, Minn.-based company recorded double-digit revenue growth across every major segment, including employer, Medicaid, Medicare Advantage and its Optum health services business. UnitedHealth now covers the medical care of nearly 47.7 million Americans.

UnitedHealth’s medical-loss ratio, which shows how much of its premium dollars were spent on medical care or “quality improvement” programs, was 81.7% in the quarter. That was up slightly from the 81.4% posted in the same quarter last year, which UnitedHealth attributed to the leap day.

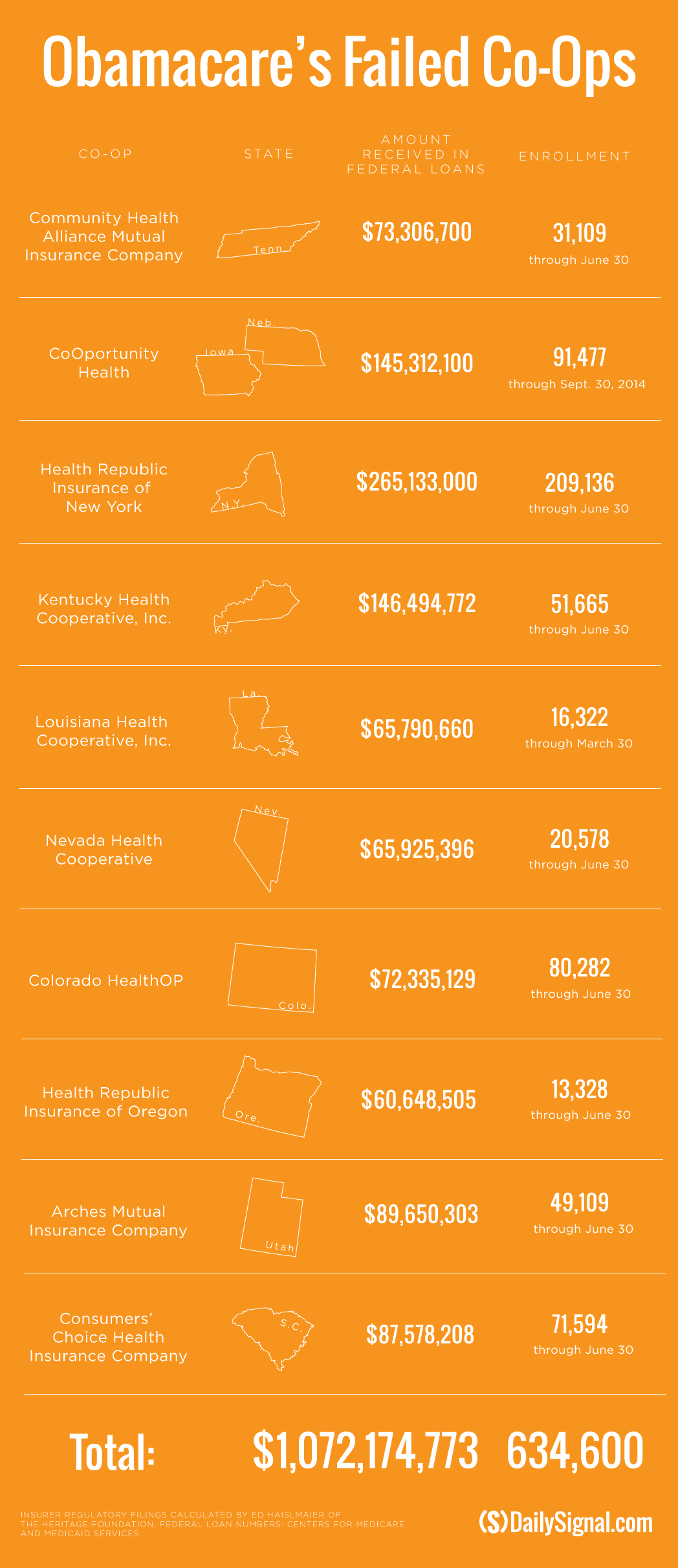

by Alex | Oct 30, 2015 | Health Care Reform, Health Exchanges, Individual Exchanges, individual health insurance, latest health insurance news, NY News, Obamacare, regional health insurance co-ops, State Exchanges

Health Republic NY Shutting Down Nov 30

Breaking: All Health Republic plans (Group and Individual) ending on 11/30. according to early reports the healthcare Co-Op Health Republic NY will be shutting down Nov 30, 2015. New York State Department of Financial Services (NYDFS), the New York State of Health Marketplace (NYSOH), and the Centers for Medicare and Medicaid Services (CMS) announced additional actions regarding Health Republic Insurance of New York (“Health Republic”) and a transition plan for Health Republic customers.

TIMELINE:

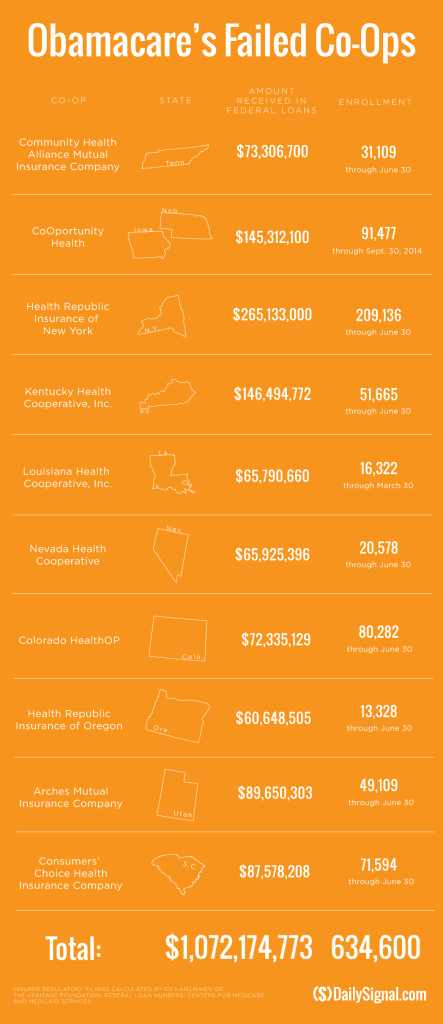

- Oct 28th – Utah Healthcare Co-Op shutting down end of 2015. This sis the 5th Co-Op to shut down

- Sept 25, 2015 – original announcement Health Republic NY is Shutting Down effective Dec 31, 2015.

- June 2015 – With a spike in rate increase of 15-20% for 2016 to reflect unexpected high costs of new 200,000 membership the most affordable health plan was experiencing difficulties. The insurer reported $130 million in losses during its first 18 months of operations, according to financial filings, even as it enrolled more customers than any other insurer. DFS did allow for a 13 percent increase in the second year and a 14 percent increase heading into 2016. Both were lower than what Health Republic requested, though, and were not enough to save the struggling insurer.

- May 2015- Health Republic was dealt its death blow when it became clear that the Affordable Care Act’s risk corridor program would not be fully funded, said one source familiar with the company’s finances. A report from Standard & Poor’s in May said the program had only 10 percent of the funds needed to make payments.

- Summer 2013 -Health Republic had borrowed $265 million to begin operations.

New Insurance Risk Corridors paid for by a combination of both consumer insurance premium surcharge tax of 2-3% and Health Insurers is suppose to reclaim capital to those that are less profitable. Health Republic was owed approximately $147 million but was told by the Centers for Medicare and Medicaid Services to expect less than half that according to sources.

Regrettably, we all suffer when an Insurer exits the market. Furthermore, it will be a while again when Federal funds earmarked to start a low cost affordable health plans will materialize again. We are pulling for neighboring co-op Health Republic of NJ and hope this trend discontinues.

Our agency will be working closely with our clients to mitigate this exposure and transition smoothly for Dec 1, 2015. Individuals on the Marketplace can contact the New York State Department of Financial Services Consumer Hot Line with questions regarding Health Republic by calling 1-800-342-3736. The Hot Line hours are weekdays (Monday through Friday) from 8:00 a.m. to 8:00 p.m., and Saturday from 9:00 a.m. to 1:00 p.m.

Please Click here to read the full Press Release from NYDFS.

Stay posted, more news to follow. Our Agency as in the past will be out and early in front positioning our clients for best options. For more information on this or to schedule a call please contact us info@medicalsolutionscorp.com today.

by Alex | Oct 20, 2015 | Health Exchanges, Individual Exchanges, individual health insurance, Obamacare

2016 Individual Open Enrollment Deadlines:

- November 1, 2015: Open Enrollment starts — first day you can enroll in a 2016 insurance plan through the Health Insurance Marketplace. Coverage can start as soon as January 1, 2016.

2016 plans and prices will be available for preview the third week of October, 2015.

- December 15, 2015: Last day to enroll in or change plans for new coverage to start January 1, 2016.

- January 1, 2016: 2016 coverage starts for those who enroll or change plans by December 15.

- January 15, 2016: Last day to enroll in or change plans for new coverage to start February 1, 2016

- January 31, 2016: 2016 Open Enrollment ends. Enrollments or changes between January 16 and January 31 take effect March 1, 2016.

If you don’t enroll in a 2016 health insurance plan by January 31, 2016, you can’t enroll in a health insurance plan for 2016 unless you qualify for a Marketplace Special Enrollment Period.

Penalty: The uninsured penalty rises to $695 or 2.5% of your income, whichever is higher.

Coverage start dates

If you enroll before the 15th of any month, your coverage starts the first day of the next month. If you enroll after the 15th of the month, you’ll have to wait until the month after that for your coverage to start. So, for example, if you enroll on January 16, your coverage would start on March 1.

Enroll using our online comparison shopping tool for both on and off-Exchange Marketplace to be released next week. Email us or Contact us at (855)667-4621.

by Alex | Oct 18, 2015 | group health insurance, Health Exchanges, Healthy NY, Individual Exchanges, individual health insurance, NY News, Uncategorized

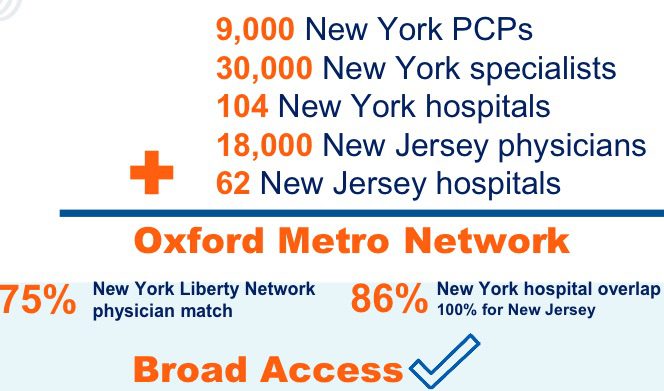

NEW 2016 Oxford Metro Network NY

Oxford has released an affordable new plan for 2016 and not a moment too soon. With the recent exit of popular Health Republic of NY, Health Republic NY is Shutting Down, the market is starving for an affordable option.

Today’s largest networks with in-network only GOLD are priced at $9,000/single annually. They typically are accompanied with $50 copays and non-office exposures of $1,000 deductibles and coinsurance percent in network. The new Metro network is approximately 25% smaller than NY Liberty network with up to 15% IN SAVINGS. For example, an Oxford Liberty HMO Gold is $745 vs Oxford Metro Gold $650.

In 2015 Oxford’s Garden State Network originated the same game plan of offering a third network in addition to FREEDOM and LIBERTY. After all what good is a large network when one cannot afford to visit Providers? The third network answers the call for access to Providers with half the copays priced at approximately $1,500 less.

All Metal Levels will be included for all size groups including 1-99 & 100+. The new Oxford Metro plan will be limited to NY and NJ Garden State Network Providers. Referrals will be needed to see Specialists. Importantly, most NY Hospitals will be participating with the EXCEPTION of NYU Health System, North Shore LIJ Health System (NorthWell Health) and Maimonides Medical Center. In addition, certain key medical IPA Groups such as Mt Kisko Medical Group are NOT in the network.

The Healthy NY and off-exchange Individuals will use exclusively this new Oxford Metro Network.

DOCTOR SEARCH: Click Here

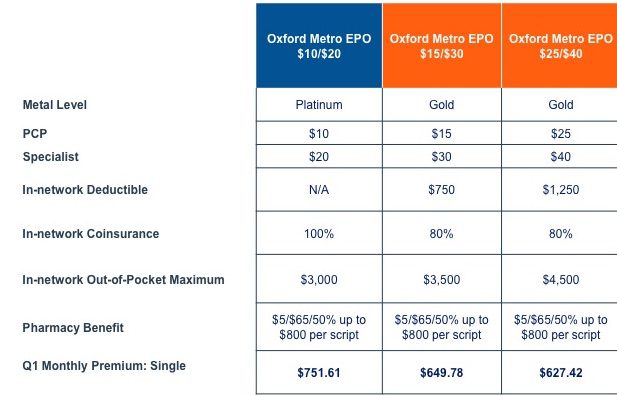

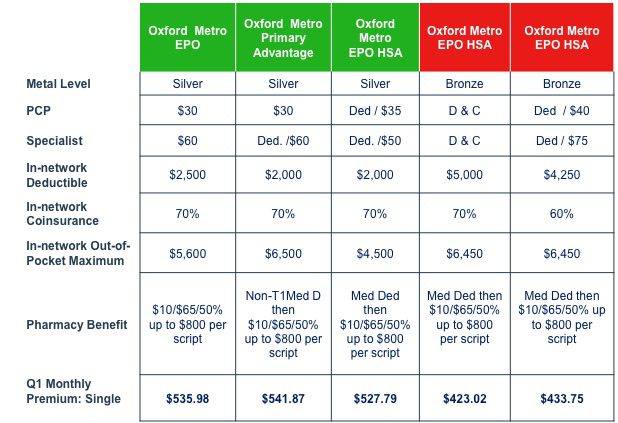

BENEFITS SUMMARY: OXFORD Platinum, Gold, Silver AND Bronze

Individual Sample Rates: Oxford 2016 NY Individual Rate Sheet

Individual Enrollment Forms: Oxford 2016-NY-MMS-Individual-application-Kit

Individual ON-Exchange UHC Network

Oxford Drug Formulary: Click Here

Oxford Metro FAQ. Click Here

Group Sample Rates:

Platinum & GOLD

Silver & Bronze

3 steps:

1. Initial Check Deposit: “Oxford Health Plans”.

2. Proof of address:

- Valid New York State driver’s license

- Voter Registration Card

- Current income tax return, current lease or current utility bill

- If mailing address is different than street address, please provide mailing address under separate cover

3. Enrollment form below and mail back to:

Oxford Individual Product Department

14 Central Park Drive

Hooksett, NH 03106

NOTE: Jan 15th deadline to submit Feb 1, 2016 effective date. Jan 31st is the deadline for a March 1, 2016 effective date.

Sign up for upcoming webinars and newsletters. Please contact us TODAY for a customized analysis for your group-specific needs at info@medicalsolutionscorp.com or Call (855) 667-4621.