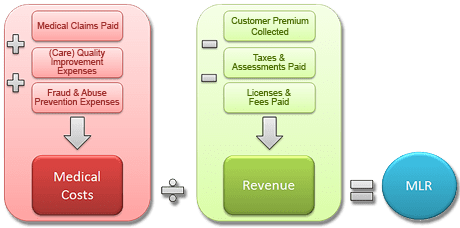

So what are are Medical Loss Ratios and why should we care?

Medical Loss Ratio (MLR) – The minimum percentage of premium dollars a commercial insurance company must spend on the reimbursement of certain medical costs. The health reform law requires insurers in the large group market to have an MLR of 85% and insurers in the small group and individual markets to have an MLR of 80% (with some waivers granted to states to reduce the threshold for certain markets).

The MLR calculation is determined on a state-by-state basis by each insurer or HMO. Rebates are calculated separately for the individual, small group and large group markets in each state.

The final regulations issued onDecember 2, 2011: • The rebate distribution processwassimplified to allowmostrebatesto be distributed to group policyholders rather than to each participantin a group plan. • Employers can distribute rebatesin a variety ofwaysincluding future premiumreductions and benefit enhancementsthatwill allowrebatesto be tax-free to recipients.

This is arguably the most significant change in Health Care Reform. In short, this is a price control on health insurers regulating profits ceilings. Unlike many industries, however, insurers must maintain a high minimum in reserves. After-all if Health Underwriters incorrectly predict unknown future costs by pricing too low there is no recovery of losses. Conversely if they priced policies too high they must return premiums to subscribers. While this is altruistically great, in today’s Oligopoly Business with an avg of 3-4 insurers in a NYC Metro Area the realities are little motivation to compete. Furthermore, health insurers in NYS have higher MLR rates and must place rate filings a year in advance. This complicates the ability of actuarial to predict future costs thus asking for higher rate increase just in case. The State then reacts by cutting increase in half which forces more insurers out of State and actually emboldens remaining health insurers to push for more aggressive cuts in benefits, challenging underwriting participation’s and limit an insurers will to go above and beyond minimum essential benefits requirements.

In full disclosure, the Benefit advisor (broker/consultant) commissions have been cut close to 50% as this cuts into insurers profits. See our interview in Crain’s regarding this https://360peo.com/p/crains-article-on-broker-commissions-cuts. Small Businesses and Sole Prop feel this the most as the resources needed to intelligently shop for benefits, reinsurance, navigate state/federal laws, employee annual open enrollments meetings have been defrayed by using a Broker. In many cases, good Brokers have become the de-facto HR.

The Federal Gov has already spent $2.2 Billion on State Exchanges. And this figures does not include remaining States as there are only 19 States working on an Exchange for 2014. The Exchanges will be built up for 2 years and then must be fully independent by 2016. If 88% of small groups coverage purchased by Brokers acc. to Boston’s Wakely Report in research study- Role of Producers and Other Third Party Assisters in New York’s Individual and SHOP Exchanges the distribution infrastructure is already there. Access to care is not the difficulty in finding a plan its the very cost of the plan! Why then does NYS decide to spend on building up new infrastructures? Agents/Brokers can easily outreach and council to uninsured as well. In fact many small businesses such as construction, consulting services and dining have many uninsured that an Agent/Broker already has a relationship with.

So where is this going? A weakened health insurer market place with the new domination of powerful large Medical groups numbering in the thousands + mega Hospital chains dictating rates. To be sure some the Hospital market is becoming close to an Oligopoly as well see: http://www.nytimes.com/2012/03/08/health/hospital-groups-will-get-bigger-moodys-report-says.html?_r=0.Still disagree? Hospital stocks have averaged 20-30% increases while insurance stocks have remained net net stagnant and down after initial spike. Ask yourself why NYS had 10 – 15 private health insurers 20 years ago while there are no rumors of new insurers or returning insurers?

If additional changes aren’t made, there could be unintended consequences including less competition, a reduction in consumer choice and higher health insurance costs. Oh I almost forgot, most clients especially NY SMB were not entitled to a rebate check with a small minority receiving avg $120.

Why are my rates going up? The recent 2014 health insurance rates ranging in 15-20% increase is having a profound impact especially on small businesses. Benefits are furthermore deteriorating with new deductibles adding a 10% to the out of pocket costs for a net total 25-30% rate increase.

No pre-existing condition. Several new cost contributors aside from Essential Health Benefits Mandate are assigned. Recent articles such as Kaiser’s Popular Provision Of Obamacare Is Fueling Sticker Shock For Some Consumers attributes new Pre-Existing condition waiver as a factor. Starting Jan 1, 2014 anyone with or without prior health insurance can get immediate treatment without a 12 month waiting period. “But the provision also adds costs. To a larger degree than other requirements of the law, it is fueling the “sticker shock” now being voiced by some consumers about premiums for new policies, say industry experts.” With the guaranteed issue there are unknown costs that cannot be accounted for just yet. Example: An uninsured individual we know is delaying needed surgeries until January for this reason. The member will pay a $250/month premium and get a $40,000 surgery paid for immediately. How many young healthy members are needed to offset this cost?

Transitional reinsurance fee. This is paid by fully insured and self-funded plans. The goal of the fee is to stabilize the individual markets by reimbursing companies who insure a disproportionately large number of individuals who are high utilizers of health care services. Fees will be collected between 2014, 2015, and 2016.

Health insurance providers’ fee, also referred to as a health insurance tax, annual fee, and insurer fee. This will be assessed annually beginning in 2014 on health insurance carriers. The total amount to be collected in 2014 is $8 billion. The tax is based on premiums and by some estimates is expected to have a cost impact of 2 to 2.5 percent in 2014, and higher in subsequent years.

Exchange fee. For 2014, our state’s online exchange marketplace is funded through federal start-up grants. But states that run their own exchange, such as Washington, have been tasked with implementing a funding mechanism after 2014. In the session that ended in June, the Washington State Legislature approved a funding plan for our exchange that authorizes the use of a current insurance premium tax for the qualified health plans (QHPs) sold in the exchange and, if necessary, an additional assessment on carriers who sell QHPs through the exchange.

Patient-Centered Outcome Research Institute (PCORI) fee (also known as comparative-effectiveness fee). Health insurance issuers and sponsors of self-funded group health plans will be assessed this annual fee beginning in 2012 and ending in 2019. It funds patient-centered outcomes research. PCORI is a nonprofit corporation whose mission is to help people make informed health care decisions, and improve health care delivery and outcomes. The Group Health Research Institute has received two research awards from PCORI to study ways to improve care for back pain, and connect patients with community resources.

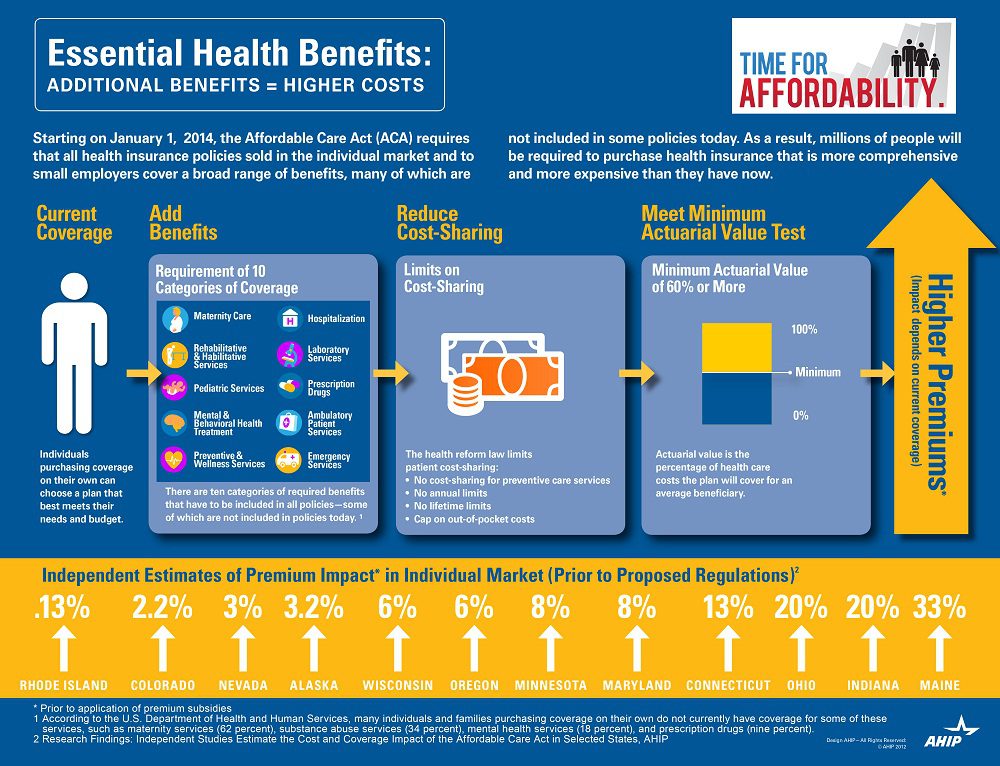

Essential Health benefits. The quintessential question asked is why are my rates going up so much this year has multiple answers with new Essential Health Benefits leading the way. The Essential Health Benefits Not Delayedarticle explains that The Affordable Care Act mandates that the plans include ten essential benefits, from care for pregnant mothers to substance abuse treatment. Popular local plans such as Healthy NY and Brooklyn Healthworks have afforded coverage for over a decade are are missing Mental Health, Chiropractic, and have a $3,000 Rx limit. All Individual Healthy NY and Sole Proprietors are terminating this year . Existing small businesses must buy the full version with Essential Health Benefits.

CASE: A Healthy Ny client just had an increase for singles from $412 to $519. She is a successful generous Caterer who is covering majority of a staff of 10 employees which is unusual for that industry. Her staff had an affordable benefits as well. They loved paying only $20, her Rx copay was only $10/generic and $20/brand for providers she did not have any deductibles. Hospitalization had full coverage with a modest copay. Statistically nearly 90% do not use more than $3,000 Rx. her new plan rolls automatically into the GOLD PLAN increasing her premium 25% along with a new $600 deductible on all benefits and a $40 copay for Specialist. She asked me I thought the new tax was only .9% medicare tax but evidently this IS HER NEW TAX.

So much for if you like your plan you can keep it promise. Even supporters such as Former President ClintonWeighs in on Obamacare. “Obama should honor his health-care promise: Pres. Clinton”, He personally believes President Barack Obama should honor his promise that people who have and like their insurance can keep it.

Do not under estimate the power of the Bill. The President is reviewing ways to allow some to keep their health plan but this would only apply to policyholders losing coverage. Stay tuned.

You can download the complete Essential Health Benefits NYS. Also, for a downloadable guide on self-insuring and secondary market reinsurance for your group please send contact form below. In the meantime, please visit to view past blogs and Legislative Alerts at https://360peo.com/feed.

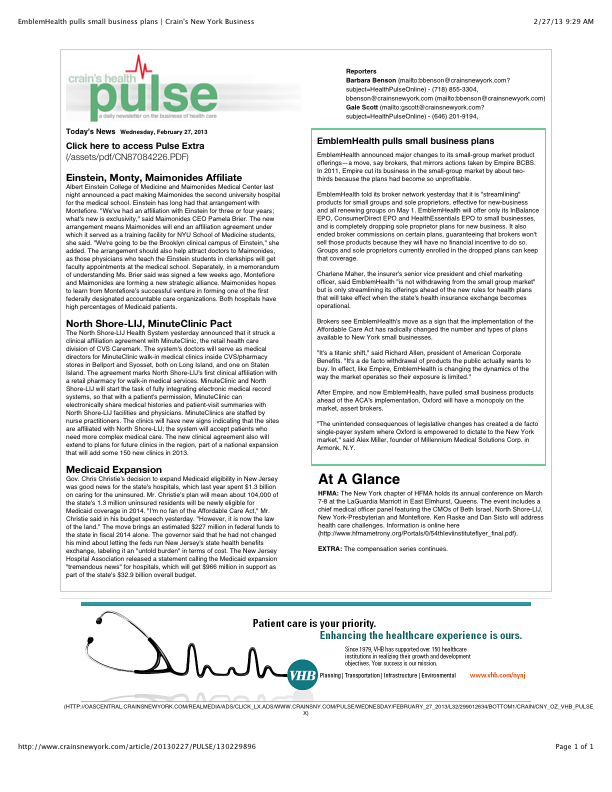

Is EmblemHealth (GHI formerly) leaving the small business market? Yes and no. The popular traditional EPO is slated to be chopped up for new business May 1 pending State approval. The remaining consumer driven health plans which have deductibles and coinsurance (a %) will stay in tact. With that Broker compensation commissions will be significantly cut as well. The family popular 2-tier rating is also phased out and new groups must submit everything clean within 30 days.

Our quote in todays Crains Health Pulse Crains EmblemHealth pulls small business plans Feb 2013 | Crain’s New York Businessreflects our deep concerns on market consolidations. “The unintended consequences of legislative changes has created a de facto single-payer system where Oxford is empowered to dictate to the New York market,” said Alex Miller, founder of Millennium Medical Solutions Corp. in Armonk, N.Y. To be fair Emblem has been steadily streamlining plans with in network only plan offerings and lowest HSA (Health Savings Account) family deductible starting out at $11,600. They are not the first insurer to do this as Empire Blue Crossissued a broader exit back in Nov 2011.

A healthy health insurance marketplace depends on competition as we all agree. From approximately 12 insurers 15 years ago we are today down to 2 active insurers Aetna and Oxford with Oxford claiming approx 2/3 of the small business marketplace. In NYS theMLR(Minimum Loss Ratios) are higher than any other state with additional state taxes. See NYS Surcharge on Health Insurance. The tight State Regulators allowing for razor thin margins while requiring insurers to maintain high reserves makes a burden many insurers are not excited. This resembles more of a utility company environment except ConEd realizes a 10% operating profit and do not have to have insurance reserves to prove solvency. Is there any surprise why there is no rush by outside insurers to compete here?

While on topic of ConEd we all know how customer care was in the aftermath of Hurricane Sandy. When was the last time an independent veteran consultant (not an ESCO) worked with you on your utility bill, servicing, negotiating, educating, and maximizing savings? Sure you can use a different supplier or ESCO but its still the local singular utility company that you are using. In comparison, same is happening in the health insurance field and the consequential exit of Health Insurance Brokers. Sadly, this is precisely the time when their training is most in demand and the most in need will be least likely to afford them.

Few healthcare changes have been more impacted than the out of control out of network charges billed to patients. The health care reform bill known as PPACA has for the most part been insignificant in the Northeast, in particular, as many state laws have already addressed issues such aspre-existing conditions, contraception, coverage rescissions and maximum loss ratios (MLR).

Instead, the market forces are reshaping the medical field into significant insurance & provider consolidation, larger hospital groups and flattening provider reimbursements. The problem is pointed out in Out of Network Medical Costs Affecting NY State Across investigation report commissioned by Governor Cuomo recognizing the unexpected out-of-network claim problem. Officials say that this is now “an overwhelming amount of consumer complaints.” Some examples cited in the report An Unwelcome Surprise – “a neurosurgeon charged $159,000 for an emergency procedure for which Medicare would have paid only $8,493.” Another example: ” a consumer went to an in-network hospital for gallbladder surgery with a participating surgeon. The consumer was not informed that a non-participating anesthesiologist would be used, and was stuck with a $1,800 bill. Providers are not currently required to disclose before they provide services whether they are in-network.” The average out-of-network radiology bill was 33 times what Medicare pays, officials say.

To make matters worse, Health Insurers have reduced their out of network recognized charges from private industry index UCR (usual customary and reasonable) to the Medicare Index known as RBRVS( Resource Based Relative Value Scale ). Insurers moved away from UCR after then-NYS D.A. Mario Cuomo in 2009 forced Unitedhelatcare Group (owners of Inginex) to settle $50 Million in a conflict of interest allegation. D.A. Cuomo future hopes for UCR were to that it be overseen by a non-profit entity. So much for best laid plans.

Today, 90% of SMB members have in network only benefits but the few remaining consumers are paying for eroding out of network benefits with little transparencies and necessary protection from new out of network billing practices. The NY Dept of Financial services is calling for providers in non-emergency situations to disclose whether or not all services are in-network, what out-of-network charges will be and how much insurers will cover.

In an ominous statement” “Failure to recognize this historical out-of-network avalanche will result in shocking financial disasters, as experienced by so many hospitals in 2003″

Why wait until January as Empire will be dropping all plans on 4/1/2012 regardless of renewal date anyway. Plus, you can still take advantage of Q4/2011 pricing. Further, Empire is not allowing mid-year plan change exceptions. Thus, 12/1/2011 enrollments with other carriers is the way to go, and is still attainable.

As per todays Crains article, Empire Blue Cross will be exiting the majority of small group health plans effective April 1, 2012. The news was swirling earlier this week with official Empire communication going out today.

This affects 1/3 of New York Small Businesses as defined by 50 or less FT and eligible employees. Since with large group market the insurer is allowed to rate a group based on true census and make up of a group’s sex, age and family status as well as claims experience of the prior year. In NY State where the small group market is Community rated and independent of census this becomes an important point that I will get back to.

As healthcare has become regulated by MLR(Max Loss ratios) or revenue controls its not surprising that insurers are unhappy but why does it seem that in NYS regulations run deeper than in other states? We are licensed in multiple states and we are not seeing the same pattern this quickly. Numerous companies have already exited such as CIGNA, HealthNet, Horizon, Guardian not to mention M&A of HIP/GHI, Oxford/UnitedHealthcare and Aetna/US Healthcare/NYLCare etc. I can go on.

In NYS the insurance regulations go beyond Health Care Reform (PPACA) with higher MLR than the national one. The Federal level is 80% for small groups and in NYS its 82%

There are new NYS price controls where insurers must anticipate risk a year in advance and ask for larger rate increases to protect on anticipated uncertain risks. With so many unknown variables its almost like asking one to predict who’s going to win the Super Bowl in 2013. Rate increase of 15-20% requests must be higher than usual since after all there are no State protection on the loss side. Furthermore, increases of 10%+ must now require public hearings 60 days prior.

Today, we have so many State mandates that many of the mandates(overage dependents coverage, preventive care, pre-existing for kids) in PPACA didnt even affect NY since they were already in place. Mandates account for approx 17% of the costs of which Small Businesses pay more than fair share. Large corporations and Unions can self insure and avoid some mandates as they are governed by ERISAand not State. To the relief of of our struggling clients on subsidized Healthy NY the State doesn’t play by their own rules and instead opts out of its very own mandates.

So what happened with Empire? The tipping point evidently was rate increase denials of 5 consecutive quarters and that Empire quite frankly got caught with great pricing and products just when healthcare reform came around. Many insurers raised their rates in advance of the law. Emblem (GHI) raised rates 25% on average and even as high as 60% on HSA. Granted they have also removed many plans recently.

Much like in the 70’s its a regulaed oligipoly with insurers too too big to fail. Our clients will have access to only 3 insurer – Aetna, Emblem and Oxford. Just imagine how high your Auto Insurance would cost in the same scenario? This remarkable in a 25 million metropolis like NYC. Insurers do not have to be in NYS, no new carrier is looking to enter the NY market. After 75 years in business and insuring 4 generations of small businesses this should be a shock to the system and a wake up call to every politician.

We ask for greater oversight on Mergers and Acquisition of health insurers,providers and hospitals. Its begining to dawn on everyone that a too big to fail environment is poison and will be the tail that wags the dog. I can only imagine what the other remaining insurers must be thinking whats in store for next year.

Importantly, the community rating ought to be dropped as most states such as NJ, CT are census based. With Health Exchanges coming in 2014 individuals will be able to purchase health insurance on their own which will make Community Rating less relevant. This will be a positive step in allowing great competitors like Humana to enter the market.

If this is not a wake up call for small businesses to have a seat at the table I dont know what is. Anyone in for an Occupy Albany?

Today’s WSJ reports UnitedHealth Buys California Group of 2,300 Doctorsmay be a signal of future trends in healthcare where there is blurring of the lines between insurers and providers. The article goes on to to mention that United Healthcare has stated that providers acquired by Optum will not work exclusively with United’s health plan, and will continue to contract with an array of insurers.

The article goes on to state that “the potential complications that might ensue, Monarch is currently in an arrangement with United competitor WellPoint Inc. to create a cooperative “accountable-care organization” aimed at bringing down health-care costs and improving quality.”

In the aftermath of Health Care Reform, insurers profits will be curtailed. New price limitations imposed by MLR (Maximum Loss ratios) where 85% of large group premiums collected must be spent on healthcare services(claims) and health quality improvement . New state tax surcharges such as New York’s 82% of above MLR applies to small groups. In fact in NY the cost of doing business is a staggering 16%+ added to the usual corporate tax. See The NYS Surcharge.

Additionally, the industry as a whole will be paying an annual tax to help pay for PPACA(Patient Protection Affordability Care Act). This tax rises from $8 billion in 2014 to $14.3 billion in 2018 and in later years, even higher according to a complex index. See Kaiser Bill Summary .

While its unglamorous to defend insurers they are clearly paying their share and like it or not they are good at health care management. Unlike foreign HQ tax loop holes taken advantage by companies such as G.E. , an insurer cannot place patent rights in Zug, Switzerland and take advantage. Each of these taxes is increased regularly by the State and contributes significantly to annual increases in rates. The competition in the health insurance industry is already at a dangerous low levels. Negotiating with insurers has become an overwhelming challenge in the large group market. Hospital groups have merged to mirror this Oligopoly trend and contractual issues are the new normal. See Empire & Stelllaris Reach pact.

So what to do other than to find profits elsewhere? Many issues and questions will abound as to the antitrust nature of this action. A similar issue appeared in the 90s Merck-Medco merger between a pharmaceutical and mail order PBM. The conflict of interest claims will abound, how do you negotiate one provider group owned by United-Healthcare as opposed to one owned by HealthNet? Will insurer share competitive insights with other practices? Are small independent Dr. Groups completely left out of the loop and feel pressured to be bought out? Will the insurers medical group have unfair advantage in buying out the smaller physician practice? Perhaps in the same vein of the Merck-Medco analogy the health insurer shareholders will do well for a decade and then simply split up?

Its all too early to tell but this much is clear, there aint no money in running a health insurance management company today.

Ever Wonder why in a Metropolis of 25 Million there are maybe 5 insurers left?

New York Taxes – As published with the NYS Insurance Dept.

New York adds more insurance taxes than any other state in the country. These consist of both direct taxes and a number of “hidden” taxes amounting to a total of over $4.1 billion in taxes passed on to our customers in the form of higher premiums. These taxes include:

• NYS Premium Tax- this 1.75% tax is on all HMO and insurance contracts and is projected to raise $353 million for the State in 2010. Empire alone pays $103.9 million to the State in premium taxes (this amount includes a special surcharge for customers in the MTA service area).

• Covered Lives Assessment- this “hidden tax” is a charge on all fully and self insured “covered lives” and raises, statewide, projected to raise $1.16 billion for the State in 2010. Empire alone will pay about $296.2 million in covered lives assessments in 2010. The purpose of the Covered Lives Assessment is raise funds for a variety of state programs and for the state Budget. The Assessment is included in claims costs for purposes of calculating the MLR.

• HCRA Surcharge- this is a 9.63% surcharge on all hospital discharges projected to raise $2.33 billion in 2010. Empire alone will pay approximately $379.4 million to the State in HCRA surcharges in 2010. The purpose of the HCRA Surcharge is to raise funds for a variety of state programs and for the state Budget. The Assessment is included in claims costs for purposes of calculating the MLR. NYS Insurance Department “332” Assessment- while this assessment is legitimately intended to fund the cost of the Insurance Department’s regulatory activities there is a “hidden tax” whereby a large portion of the revenue generated by the assessment is used to fund other programs funded not directly related to insurance regulation and is projected to raise $270 million from New York’s health insurers and HMO’s in 2010. Empire will pay the state $57.9 million in 332 assessments for 2010.

Each of these taxes is increased regularly by the State and contributes significantly to annual increases in rates. The competition in the health insurance industry is already at a dangerous low level. Negotiating with insurers has become an overwhelming challenge in the large group market.

Accountable Care Organization (ACO) – These organizations coordinate patient care and provide the full range of health care services for patients. The health reform law provides incentives for providers who join together to form such organizations and who agree to be accountable for the quality, cost, and overall care of Medicare beneficiaries who are enrolled in the traditional fee-for-service program who are assigned to the ACO. Annual Benefit Limit – In the past, some insurance plans have placed a limit on the dollar amount of claims they will pay in a given year for an individual. Beginning in 2010, annual benefit limits on certain “essential health benefits” are restricted on a graduated basis, and annual limits will eventually be prohibited in 2014. Basic Health Plan – Beginning in 2014, states will have the option of creating a basic health plan to provide coverage to individuals with incomes between 133 and 200 percent of poverty instead of enrolling in the health insurance exchange and receiving premium subsidies. The federal government will provide states that choose to offer this plan with 95 percent of what it would have paid to subsidize these enrollees in the health insurance exchange. Benefit Package – The set of health services, such as physician visits, hospitalizations, and prescription drugs, that are covered by a member’s insurance policy or group health plan. Capitation – Under a capitation system health care providers are paid a set amount for each enrolled person assigned to that physician or group of physicians, whether or not that person seeks care. Case Management – The coordination of medical care for patients with specific diagnoses or high health care needs, performed by case managers who can include medical directors or nurses. Catastrophic Coverage – A coverage option with a limited benefit plan design accompanied by a high Deductible. The plan design is intended to protect primarily against the cost for unforeseen and expensive illnesses or injuries. These plans are attractive to young adults in relatively good health. CHIP – The Children’s Health Insurance Program (CHIP) is a program administered by the United States Department of Health and Human Services that provides matching funds to states for health insurance to low income families with children. The program was designed with the intent to cover uninsured children in families with incomes that are modest but too high to qualify for Medicaid. Chronic Care Management – The coordination of health care and supportive services to improve the health status of patients with chronic conditions, such as diabetes and asthma. The goals of these programs are to improve the quality of care and manage costs. COBRA – Consolidated Omnibus Budget Reconciliation Act of 1985 (COBRA) applies to employers who generally employ 20 or more full time equivalent employees. Employees who lose their jobs are able to continue their employer-sponsored coverage for a set period of time. For example, employees are typically entitled to extend coverage for 18 months, however if they are deemed disabled by the Social Security Administration, coverage may continue for up to 29 months. Co-insurance – The amount or percentage of the reimbursed amount of covered expenses a plan member must pay for health services after the Deductible has been met. Community Living Assistance Services and Supports (CLASS) Program – The CLASS program establishes a national voluntary long-term care insurance program for the purchase of non-medical services and support necessary for enrollees who have paid premiums into the program and become eligible (due to disability or chronic illnesses). Enrollees would receive benefits that help pay for assistance in the home or in a facility in future years. Enrollment begins January 1, 2011 (targeting working adults who can make voluntary premium contributions through payroll deductions or directly). The first benefits will be paid out to enrollees in 2016. Community Rating – A method of pricing health insurance plans, where all policyholders are charged the same premium, regardless of health status, age or other factors. “Modified community rating” generally refers to a method where health insurers may vary premiums based on specified demographic characteristics (e.g. age, gender, location), but cannot vary premiums based on the health status or claims history of policyholders. Comparative Effectiveness Research – Research is federally sponsored to compare existing health care interventions to determine which work best for which patients and which pose the greatest benefits and harms. The research also aims to improve the quality of care and to control costs. Consumer-Directed Health Plans – These health plans seek to increase consumer awareness about health care costs and provide incentives for consumers to consider costs when making health care decisions. These plans usually have a high Deductible accompanied by a savings account for health care services. There are two types of savings accounts – Health Savings Accounts (HSAs) and Health Reimbursement Accounts (HRAs). Co-payment – A fixed dollar amount paid by an individual receiving a health care service covered by the member’s plan. Cost-Sharing – Health plan members are required to pay a portion of the costs of their care. Examples of these costs include Co-payments, Co-insurance and annual Deductibles. Deductible – The dollar amount that a plan member must pay for health care services each year before the insurer begins to reimburse for health care services. Beginning in 2014, deductibles for small group insurance plans will be limited to $2,000 for individual policies and $4,000 for family policies. Disease Management – The coordination of care for the entire disease treatment process, including preventive care, patient education and outpatient care in addition to inpatient and acute care. The process is intended to reduce costs and improve the quality of life for an individual with a chronic condition. Donut Hole – A gap in prescription drug coverage under Medicare Part D, where beneficiaries pay 100% of their prescription drug costs after their total drug costs exceed an initial coverage limit until they qualify for a second tier of coverage. Under the standard Part D benefit, Medicare covers 75% of drug costs below the initial coverage limit ($2,830 in 2010), and 95% of spending within the second tier level ($6,440 in 2010). The “donut hole” specifically refers to the range between these two levels. Health care reform also provides a $250 rebate for all Medicare Part D enrollees who enter the donut hole in 2010, increases discounts in subsequent years and completely closes the donut hole by 2020. Dual Eligibles – A term used to describe an individual who is eligible for Medicare and for some Medicaid benefits. Electronic Health Record/Electronic Medical Records – Computerized patient health records, including medical, demographic, and administrative information. These records can be created and stored within one organization or shared across multiple health care organizations and sites. Employee Retirement Income Security Act of 1974 (ERISA) – Enacted in 1974 to provide minimum Federal standards for welfare benefit plans in private industry, and protect the interests of employee benefit plan participants and their beneficiaries by requiring the disclosure to them of financial and other information concerning the plan; by establishing standards of conduct for plan fiduciaries; and by providing for appropriate remedies and access to the Federal courts. Employer Mandate – Beginning in 2014 pursuant to the health reform law, employers meeting size or revenue thresholds will be required to offer minimum essential health benefit packages or pay a set portion of the cost of those benefits for use in the Exchanges. Episode of Care – Refers to all the health services related to the treatment of a condition. For acute conditions (such as a concussion or a broken bone), the episode includes all treatment and services from the onset of the condition to its resolution. For chronic conditions (such as diabetes), the episode refers to all services and treatments received over a given period of time. Some payment reform proposals involve basing provider payment on episodes of care instead of paying on a Fee-for-Service basis. Essential Health Benefits – The health reform law placed certain coverage requirements on essential health benefits, and provides a broad set of benefit categories that would be considered essential to a health benefits package — including hospitalization, outpatient services, emergency care, prescription drugs, maternity care, preventive services and other benefits. The Secretary of HHS will, in the future, define what constitutes “Essential Health Benefits” and this will be guided by the current scope of benefits provided under a typical employer plan. For plan years beginning in 2010 the only requirement for “Essential Health Benefits” is that if they are included in the plan they may not be subject to a lifetime limit and until 2014 can only be subject to a “restricted annual limit”. Exchange or Health Insurance Exchange – The health care reform law creates Health Benefit Exchanges (competitive insurance marketplaces) in each state, where individuals and employers can shop for health plans. External Review – Health care reform requires all health plans (except Grandfathered plans) to provide an external review appeal process that meets minimum standards. With the exception of a few state processes currently in existence, external review has typically been limited to appeals of clinical decisions. The health reform law has expanded the scope of external review for self-funded health plans to non-eligibility administrative appeals as well. Administrative appeals deal with such issues as benefit exclusions, benefit limits and disputes over member financial responsibility for payments such as Co-payments, Co-insurance and Deductibles. Fee-for-Service – A traditional method of paying for medical services where doctors and hospitals are paid a fee for each service they provide.

FTE – Full Time Equivalent -The percent of time worked is based on a standard of 100% or 1.0. For example, an employee who is working 60% and employee who is working 40% of the time would equal 100% or an FTE of 1.0.

For example, a firm has 35 full-time employees (30+ hours). In addition, the firm has 20 part time employees who all work 24 hours per week (96 hours per month). These part-time employees’ hours would be treated as equivalent to 16 full-time employees, based on the following calculation: 20 employees x 96 hours / 120 = 1920 / 120 = 16

Grandfathered Plan – A health plan that was in place on March 23, 2010, when the health reform law was enacted, is exempt from complying with some parts of the health reform law, so long as the plan does not make certain changes (such as eliminating or reducing benefits, increasing cost-sharing, or reducing the employer contribution toward the premium). Once a health plan makes such a change, it becomes subject to other health reform provisions (e.g., appeals and cost sharing restrictions on preventive services).

Group Health Plan – Health insurance that is offered by a plan sponsor, typically an employer on behalf of its employees. Guarantee Issue/Guarantee Renewability – Beginning in 2014, the health reform law requires insurers to offer and renew coverage to non-Grandfathered plans, without regard to health status, use of services, or pre-existing conditions. Health Insurance Portability and Accountability Act of 1996 (HIPAA) – This law sets standards for the security and privacy of personal health information. In addition, the law makes it easier for individuals to change jobs without the risk of extended waiting periods due to pre-existing conditions. Health Maintenance Organization (HMO) – A health plan that provides coverage through a network of hospitals, physicians and other health care providers. HMOs usually require the selection of a primary care physician who is responsible for managing and coordinating all health care. Usually, referrals to specialist physicians are required, and the HMO pays only for care provided by an in-network provider. Health Reimbursement Account (HRA) – A tax-exempt account that can be used to pay for qualified health expenses. HRAs are usually paired with a high-Deductible health plan and are funded solely by employer contributions. Health Savings Account (HSA) – A tax-exempt savings account that can be used to pay for qualified medical expenses. Individuals can obtain HSAs from most financial institutions, or through their employer. Both employers and employees can contribute to the plan. To open an HSA, an individual must have health coverage under an HSA-qualified high-Deductible health plan which has Deductibles of at least $1,200 for an individual and $2,400 for a family in 2010. High-Deductible Health Plan – These health insurance plans have higher Deductibles and lower premiums than traditional insurance plans. High-Risk Pool – The health reform law expands upon the current state-based high-risk pool system. The law requires the government to establish or issue contracts to establish a temporary high risk pool (through 2013) to provide coverage for eligible individuals with pre-existing conditions by appropriating $5 billion to subsidize premiums. Eligibility is limited to individuals who have been uninsured for at least six months prior to applying for pool coverage, and who have a pre-existing condition. Individual Mandate – A requirement that most individuals obtain health insurance or pay a penalty beginning in 2014. Massachusetts was the first state to impose an individual mandate that all adults have health insurance. Interim Final Rule (IFR) – A final rule that has the full force and effect of law; thus, affected parties have an obligation to comply with its requirements. An IFR allows interested parties to submit comments during a public comment period and prior to issuing revised guidance. Internal Review – An internal review of an adverse claim determination. Lifetime Benefit Maximum – A limit on the amount an insurer will pay toward the cost of health care services over the lifetime of the policy. Health care reform prohibits lifetime dollar limits on “essential health benefits” effective for plan/policy years beginning on or after September 23, 2010. Long-Term Care – Services needed for an individual to live independently in the community, such as home health and personal care, as well as services provided in institutional settings such as nursing homes. Many of these services are not covered by Medicare or private insurance (see also the Community Living Assistance Services and Supports program defined above). Managed Care – A health care delivery system that seeks to reduce the cost of providing health benefits and improve the quality of care. These arrangements often rely on primary care physicians to manage the care their patients receive. Mandatory Benefits – A state or federal requirement that health plans provide coverage for certain benefits, treatment or services. Medicaid – A federal and state funded program that provides medical and health related services to certain low-income Americans. The health reform law expands Medicaid eligibility to non-Medicare eligible individuals with incomes up to 133% of the Federal poverty level, establishing uniform eligibility for adults and children across all states by 2014. Medical Loss Ratio (MLR) – The minimum percentage of premium dollars a commercial insurance company must spend on the reimbursement of certain medical costs. The health reform law requires insurers in the large group market to have an MLR of 85% and insurers in the small group and individual markets to have an MLR of 80% (with some waivers granted to states to reduce the threshold for certain markets). Medicare – A federal program that provides health care coverage to people age 65 and older, and to those who are under 65 and are permanently physically disabled or who have a congenital physical disability; or to those who meet other special criteria such as end-stage renal disease. Eligible individuals can receive coverage for hospital services (Medicare Part A), physician based medical services (Medicare Part B) and prescription drugs (Medicare Part D). Medicare Advantage – Also referred to as Medicare Part C, the Medicare Advantage program allows Medicare beneficiaries to receive their Medicare benefits through a private insurance plan. Out-of-Pocket Costs – Health care costs that are not covered by insurance, such as Deductibles, Co-payments, and Co-insurance. Out-of-pocket costs do not include premium costs. Out-of-Pocket Maximum – An annual limit on the amount of money individuals are required to pay out-of-pocket for health care costs, excluding premiums. The health reform law, beginning in 2014, prevents an employer from imposing cost sharing in amounts greater than the current out-of-pocket limits for high-Deductible health plans ($5,950 for an individual policy or $11,900 for a family policy in 2010). These amounts will be adjusted annually. Patient Centered Medical Home – A term defining a health care setting where patients receive comprehensive primary care services, have an ongoing relationship with a primary care provider who directs and coordinates their care; and have enhanced access to non-emergent care. Patient Protection and Affordable Care Act (PPACA) – Also referred to as the “health reform law,” this Act begins the implementation of a staged set of rules with an initial effective date of March 23, 2010. The law is intended to increase access to health care for more Americans, and includes many changes that impact the commercial health insurance market, Medicare and Medicaid. Pay for Performance – A payment system where health care providers receive incentives for meeting or exceeding quality and cost benchmarks. Some systems also penalize providers who do not meet established benchmarks. The goal of pay for performance programs is to improve the quality of care over time. Pre-existing Condition – An illness or medical condition for which a person is diagnosed or treated within a specified period of time prior to becoming insured in a new plan. The heath reform law prohibits the denial of coverage due to a pre-existing condition for plan and policy years beginning after September 23, 2010 for children under 19, and for all others beginning in 2014. Preferred Provider Organization (PPO) – A type of managed care organization that provides health care coverage through a network of providers. Plan members typically pay higher costs when they seek care from out-of-network providers. Premium – The amount paid, often on a monthly basis, for health insurance. The cost of the premium may be shared between employers or government purchasers, and individuals. Premium Subsidies – A fixed amount of money, or a designated percentage of the premium cost, that is provided to help people purchase health insurance. The health reform law provides premium subsidies to individuals with incomes between 133% and 400% of the federal poverty level who purchase policies through the health insurance Exchanges, beginning in 2014. Preventive Care Services – Health care that emphasizes the early detection and treatment of disease. The health reform law requires certain health plans (excludes Grandfathered plans) to provide coverage without member cost-sharing for certain preventive services. Primary Care Provider – A provider, usually a physician, specializing in internal medicine, family practice, or pediatrics, who is responsible for providing primary care and coordinating other necessary health care services for patients. Qualified Health Plan – Insurance plans that are sold through a Health Insurance Exchange must have been certified as meeting a minimum benchmark of benefits (i.e., essential health benefits) under the health reform law. Rate Review – Review by insurance regulators of a health plan’s proposed premium and premium increases. Rates are reviewed to ensure they are sufficient to pay claims, are not unreasonably high in relation to the medical claim costs and the benefits provided, and are not discriminatorily applied. Reinsurance – Insurance purchased by insurance companies and employers that self-insure their employees’ medical costs, to limit liability or exposure to high claims or increased cost trends. The health reform law includes a temporary federal reinsurance program for employers that insure early retirees over age 55 who are not eligible for Medicare. Rescission – Refers to a practice where an approved policy is voided from its inception by the insurer, usually on the grounds of material misrepresentation or omission on the initial application. Under health reform, rescissions are prohibited except in cases of fraud or intentional misrepresentation. Risk Adjustment – The process of increasing or reducing payments to health plans to reflect higher or lower than expected spending. Risk adjusting is designed to compensate health plans that enroll a sicker population as a way to discourage plans from selecting only healthier individuals. Section 125 Plan – These plans are otherwise known as a “cafeteria plan” offered pursuant to Section 125 of the Internal Revenue Code. Its name comes from a set of benefit plans that allows employees to choose between different types of benefits, similar to the ability of a customer to choose among available items in a cafeteria, and the employees’ pretax contributions are not subject to federal, state, or Social Security taxes. Self-Insured Plan – The employer assumes the financial responsibility of health care benefits for its employees in a self-insured or self-funded plan. Employer sponsored self-insured plans typically contract with a third-party administrator to provide administrative services for the plan. Small Business Tax Credit – The health reform law includes a tax credit equal to 50 percent (35 percent in the case of tax-exempt eligible small employers) for qualified small employers that provide health coverage to their employees. The tax credit is available to employers with 25 or fewer employees with average annual wages of less than $50,000. Small Group Market – Businesses with typically 2-50 employees, or eligible employees depending on applicable state law, can purchase health insurance for their employees through this market, which is regulated by states. Tax Credit – An amount that a person or business can subtract from the income tax that they owe. If a tax credit is refundable, the taxpayer can receive a payment from the government to the extent that the credit is greater than the amount of tax they would otherwise owe. Tax Deduction – An amount that a person can subtract from adjusted gross income when calculating the taxes that they owe. Generally, people who itemize deductions can deduct the portion of medical expenses, including health insurance premiums, that exceeds 7.5% of their adjusted gross income. Under health reform, the threshold for deducting medical expenses increases to 10% in 2013 (this increase is waived for individuals 65 and older for tax years 2013-2016). Value-Based Purchasing – A payment reform which provides bonuses to hospitals and other providers based upon their performance against quality measures. Wellness Plan/Program – An employer program to improve health and prevent disease

{kind=link}