Why are my rates going up? The recent 2014 health insurance rates ranging in 15-20% increase is having a profound impact especially on small businesses. Benefits are furthermore deteriorating with new deductibles adding a 10% to the out of pocket costs for a net total 25-30% rate increase.

No pre-existing condition. Several new cost contributors aside from Essential Health Benefits Mandate are assigned. Recent articles such as Kaiser’s Popular Provision Of Obamacare Is Fueling Sticker Shock For Some Consumers attributes new Pre-Existing condition waiver as a factor. Starting Jan 1, 2014 anyone with or without prior health insurance can get immediate treatment without a 12 month waiting period. “But the provision also adds costs. To a larger degree than other requirements of the law, it is fueling the “sticker shock” now being voiced by some consumers about premiums for new policies, say industry experts.” With the guaranteed issue there are unknown costs that cannot be accounted for just yet. Example: An uninsured individual we know is delaying needed surgeries until January for this reason. The member will pay a $250/month premium and get a $40,000 surgery paid for immediately. How many young healthy members are needed to offset this cost?

Transitional reinsurance fee. This is paid by fully insured and self-funded plans. The goal of the fee is to stabilize the individual markets by reimbursing companies who insure a disproportionately large number of individuals who are high utilizers of health care services. Fees will be collected between 2014, 2015, and 2016.

Health insurance providers’ fee, also referred to as a health insurance tax, annual fee, and insurer fee. This will be assessed annually beginning in 2014 on health insurance carriers. The total amount to be collected in 2014 is $8 billion. The tax is based on premiums and by some estimates is expected to have a cost impact of 2 to 2.5 percent in 2014, and higher in subsequent years.

Exchange fee. For 2014, our state’s online exchange marketplace is funded through federal start-up grants. But states that run their own exchange, such as Washington, have been tasked with implementing a funding mechanism after 2014. In the session that ended in June, the Washington State Legislature approved a funding plan for our exchange that authorizes the use of a current insurance premium tax for the qualified health plans (QHPs) sold in the exchange and, if necessary, an additional assessment on carriers who sell QHPs through the exchange.

Patient-Centered Outcome Research Institute (PCORI) fee (also known as comparative-effectiveness fee). Health insurance issuers and sponsors of self-funded group health plans will be assessed this annual fee beginning in 2012 and ending in 2019. It funds patient-centered outcomes research. PCORI is a nonprofit corporation whose mission is to help people make informed health care decisions, and improve health care delivery and outcomes. The Group Health Research Institute has received two research awards from PCORI to study ways to improve care for back pain, and connect patients with community resources.

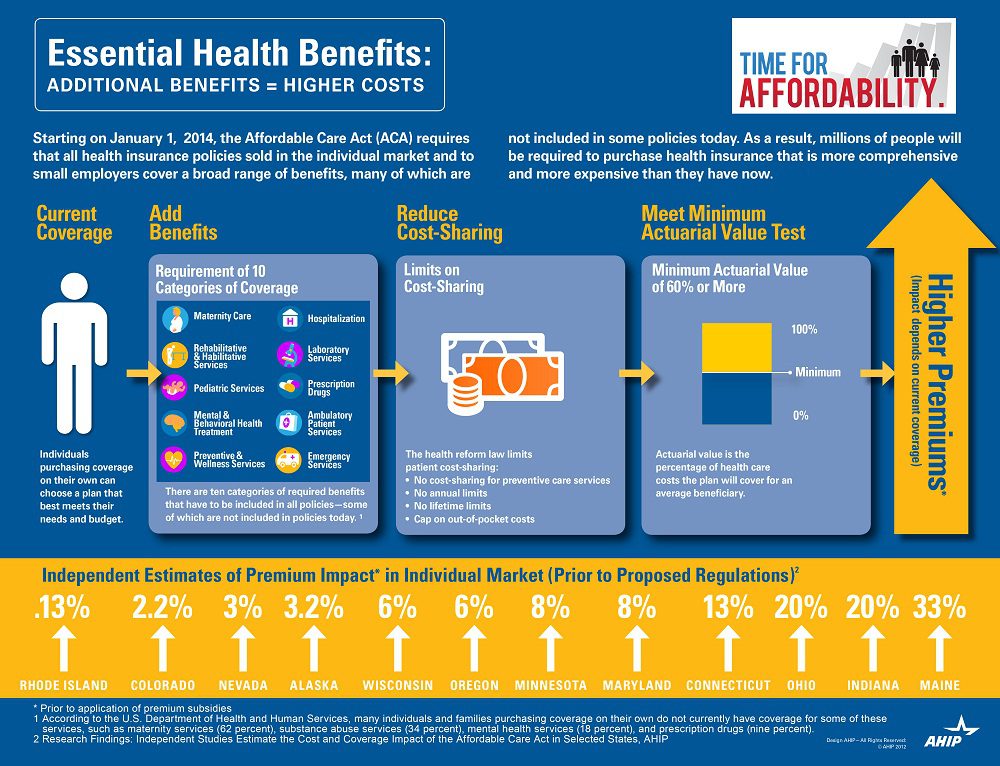

Essential Health benefits. The quintessential question asked is why are my rates going up so much this year has multiple answers with new Essential Health Benefits leading the way. The Essential Health Benefits Not Delayedarticle explains that The Affordable Care Act mandates that the plans include ten essential benefits, from care for pregnant mothers to substance abuse treatment. Popular local plans such as Healthy NY and Brooklyn Healthworks have afforded coverage for over a decade are are missing Mental Health, Chiropractic, and have a $3,000 Rx limit. All Individual Healthy NY and Sole Proprietors are terminating this year . Existing small businesses must buy the full version with Essential Health Benefits.

CASE: A Healthy Ny client just had an increase for singles from $412 to $519. She is a successful generous Caterer who is covering majority of a staff of 10 employees which is unusual for that industry. Her staff had an affordable benefits as well. They loved paying only $20, her Rx copay was only $10/generic and $20/brand for providers she did not have any deductibles. Hospitalization had full coverage with a modest copay. Statistically nearly 90% do not use more than $3,000 Rx. her new plan rolls automatically into the GOLD PLAN increasing her premium 25% along with a new $600 deductible on all benefits and a $40 copay for Specialist. She asked me I thought the new tax was only .9% medicare tax but evidently this IS HER NEW TAX.

So much for if you like your plan you can keep it promise. Even supporters such as Former President ClintonWeighs in on Obamacare. “Obama should honor his health-care promise: Pres. Clinton”, He personally believes President Barack Obama should honor his promise that people who have and like their insurance can keep it.

Do not under estimate the power of the Bill. The President is reviewing ways to allow some to keep their health plan but this would only apply to policyholders losing coverage. Stay tuned.

You can download the complete Essential Health Benefits NYS. Also, for a downloadable guide on self-insuring and secondary market reinsurance for your group please send contact form below. In the meantime, please visit to view past blogs and Legislative Alerts at https://360peo.com/feed.

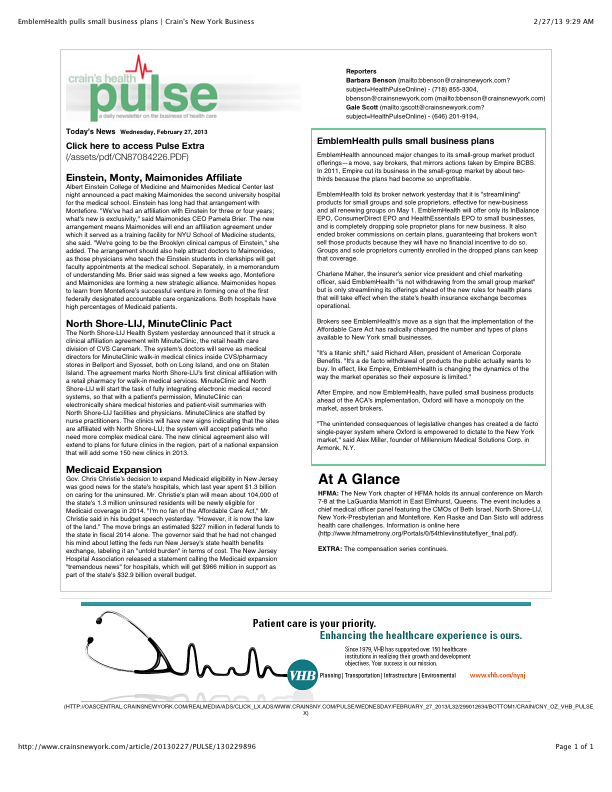

Is EmblemHealth (GHI formerly) leaving the small business market? Yes and no. The popular traditional EPO is slated to be chopped up for new business May 1 pending State approval. The remaining consumer driven health plans which have deductibles and coinsurance (a %) will stay in tact. With that Broker compensation commissions will be significantly cut as well. The family popular 2-tier rating is also phased out and new groups must submit everything clean within 30 days.

Our quote in todays Crains Health Pulse Crains EmblemHealth pulls small business plans Feb 2013 | Crain’s New York Businessreflects our deep concerns on market consolidations. “The unintended consequences of legislative changes has created a de facto single-payer system where Oxford is empowered to dictate to the New York market,” said Alex Miller, founder of Millennium Medical Solutions Corp. in Armonk, N.Y. To be fair Emblem has been steadily streamlining plans with in network only plan offerings and lowest HSA (Health Savings Account) family deductible starting out at $11,600. They are not the first insurer to do this as Empire Blue Crossissued a broader exit back in Nov 2011.

A healthy health insurance marketplace depends on competition as we all agree. From approximately 12 insurers 15 years ago we are today down to 2 active insurers Aetna and Oxford with Oxford claiming approx 2/3 of the small business marketplace. In NYS theMLR(Minimum Loss Ratios) are higher than any other state with additional state taxes. See NYS Surcharge on Health Insurance. The tight State Regulators allowing for razor thin margins while requiring insurers to maintain high reserves makes a burden many insurers are not excited. This resembles more of a utility company environment except ConEd realizes a 10% operating profit and do not have to have insurance reserves to prove solvency. Is there any surprise why there is no rush by outside insurers to compete here?

While on topic of ConEd we all know how customer care was in the aftermath of Hurricane Sandy. When was the last time an independent veteran consultant (not an ESCO) worked with you on your utility bill, servicing, negotiating, educating, and maximizing savings? Sure you can use a different supplier or ESCO but its still the local singular utility company that you are using. In comparison, same is happening in the health insurance field and the consequential exit of Health Insurance Brokers. Sadly, this is precisely the time when their training is most in demand and the most in need will be least likely to afford them.

Few healthcare changes have been more impacted than the out of control out of network charges billed to patients. The health care reform bill known as PPACA has for the most part been insignificant in the Northeast, in particular, as many state laws have already addressed issues such aspre-existing conditions, contraception, coverage rescissions and maximum loss ratios (MLR).

Instead, the market forces are reshaping the medical field into significant insurance & provider consolidation, larger hospital groups and flattening provider reimbursements. The problem is pointed out in Out of Network Medical Costs Affecting NY State Across investigation report commissioned by Governor Cuomo recognizing the unexpected out-of-network claim problem. Officials say that this is now “an overwhelming amount of consumer complaints.” Some examples cited in the report An Unwelcome Surprise – “a neurosurgeon charged $159,000 for an emergency procedure for which Medicare would have paid only $8,493.” Another example: ” a consumer went to an in-network hospital for gallbladder surgery with a participating surgeon. The consumer was not informed that a non-participating anesthesiologist would be used, and was stuck with a $1,800 bill. Providers are not currently required to disclose before they provide services whether they are in-network.” The average out-of-network radiology bill was 33 times what Medicare pays, officials say.

To make matters worse, Health Insurers have reduced their out of network recognized charges from private industry index UCR (usual customary and reasonable) to the Medicare Index known as RBRVS( Resource Based Relative Value Scale ). Insurers moved away from UCR after then-NYS D.A. Mario Cuomo in 2009 forced Unitedhelatcare Group (owners of Inginex) to settle $50 Million in a conflict of interest allegation. D.A. Cuomo future hopes for UCR were to that it be overseen by a non-profit entity. So much for best laid plans.

Today, 90% of SMB members have in network only benefits but the few remaining consumers are paying for eroding out of network benefits with little transparencies and necessary protection from new out of network billing practices. The NY Dept of Financial services is calling for providers in non-emergency situations to disclose whether or not all services are in-network, what out-of-network charges will be and how much insurers will cover.

In an ominous statement” “Failure to recognize this historical out-of-network avalanche will result in shocking financial disasters, as experienced by so many hospitals in 2003″

Today’s WSJ reports UnitedHealth Buys California Group of 2,300 Doctorsmay be a signal of future trends in healthcare where there is blurring of the lines between insurers and providers. The article goes on to to mention that United Healthcare has stated that providers acquired by Optum will not work exclusively with United’s health plan, and will continue to contract with an array of insurers.

The article goes on to state that “the potential complications that might ensue, Monarch is currently in an arrangement with United competitor WellPoint Inc. to create a cooperative “accountable-care organization” aimed at bringing down health-care costs and improving quality.”

In the aftermath of Health Care Reform, insurers profits will be curtailed. New price limitations imposed by MLR (Maximum Loss ratios) where 85% of large group premiums collected must be spent on healthcare services(claims) and health quality improvement . New state tax surcharges such as New York’s 82% of above MLR applies to small groups. In fact in NY the cost of doing business is a staggering 16%+ added to the usual corporate tax. See The NYS Surcharge.

Additionally, the industry as a whole will be paying an annual tax to help pay for PPACA(Patient Protection Affordability Care Act). This tax rises from $8 billion in 2014 to $14.3 billion in 2018 and in later years, even higher according to a complex index. See Kaiser Bill Summary .

While its unglamorous to defend insurers they are clearly paying their share and like it or not they are good at health care management. Unlike foreign HQ tax loop holes taken advantage by companies such as G.E. , an insurer cannot place patent rights in Zug, Switzerland and take advantage. Each of these taxes is increased regularly by the State and contributes significantly to annual increases in rates. The competition in the health insurance industry is already at a dangerous low levels. Negotiating with insurers has become an overwhelming challenge in the large group market. Hospital groups have merged to mirror this Oligopoly trend and contractual issues are the new normal. See Empire & Stelllaris Reach pact.

So what to do other than to find profits elsewhere? Many issues and questions will abound as to the antitrust nature of this action. A similar issue appeared in the 90s Merck-Medco merger between a pharmaceutical and mail order PBM. The conflict of interest claims will abound, how do you negotiate one provider group owned by United-Healthcare as opposed to one owned by HealthNet? Will insurer share competitive insights with other practices? Are small independent Dr. Groups completely left out of the loop and feel pressured to be bought out? Will the insurers medical group have unfair advantage in buying out the smaller physician practice? Perhaps in the same vein of the Merck-Medco analogy the health insurer shareholders will do well for a decade and then simply split up?

Its all too early to tell but this much is clear, there aint no money in running a health insurance management company today.

Ever Wonder why in a Metropolis of 25 Million there are maybe 5 insurers left?

New York Taxes – As published with the NYS Insurance Dept.

New York adds more insurance taxes than any other state in the country. These consist of both direct taxes and a number of “hidden” taxes amounting to a total of over $4.1 billion in taxes passed on to our customers in the form of higher premiums. These taxes include:

• NYS Premium Tax- this 1.75% tax is on all HMO and insurance contracts and is projected to raise $353 million for the State in 2010. Empire alone pays $103.9 million to the State in premium taxes (this amount includes a special surcharge for customers in the MTA service area).

• Covered Lives Assessment- this “hidden tax” is a charge on all fully and self insured “covered lives” and raises, statewide, projected to raise $1.16 billion for the State in 2010. Empire alone will pay about $296.2 million in covered lives assessments in 2010. The purpose of the Covered Lives Assessment is raise funds for a variety of state programs and for the state Budget. The Assessment is included in claims costs for purposes of calculating the MLR.

• HCRA Surcharge- this is a 9.63% surcharge on all hospital discharges projected to raise $2.33 billion in 2010. Empire alone will pay approximately $379.4 million to the State in HCRA surcharges in 2010. The purpose of the HCRA Surcharge is to raise funds for a variety of state programs and for the state Budget. The Assessment is included in claims costs for purposes of calculating the MLR. NYS Insurance Department “332” Assessment- while this assessment is legitimately intended to fund the cost of the Insurance Department’s regulatory activities there is a “hidden tax” whereby a large portion of the revenue generated by the assessment is used to fund other programs funded not directly related to insurance regulation and is projected to raise $270 million from New York’s health insurers and HMO’s in 2010. Empire will pay the state $57.9 million in 332 assessments for 2010.

Each of these taxes is increased regularly by the State and contributes significantly to annual increases in rates. The competition in the health insurance industry is already at a dangerous low level. Negotiating with insurers has become an overwhelming challenge in the large group market.

{kind=link}