In Time magazine’s March issue Bitter Pill: Why Medical Bills Are Killing Us Steven Brill gets to work on answering the ever elusive Why are Medical Costs So High? The 21,000 word article is longest article in Time Magazine history that can boiled down to simply there is no free marketplace in health care. We think everything in this country is a free market but is there a free market when one needs to got to an emergency room or a free market when one must take a cancer pill? According to Howard Dean the singular reason is to get away form the current fee for service system where providers get paid per procedure and not per patient.

Here’s an eye opener: “Insurance Companies are not really the problem they run pretty terribly. They process claims, a lot of us think they process claims and fairly consistently but they are increasingly at the mercy of hospitals which are consolidating buying a doctors practices. We should tax profits on so-called nonprofit hospitals and put that money back into the system. We should control all the prices for prescription drugs because if I have a monopoly a cancer wonder drug I can charge anything I want for them that’s obviously not a free market and it’s completely two different uses you see this article once you follow the money.”

Transcript of the video:

“This is not a free-market. You don’t get health care because you want it. You don’t wake up in the morning and gee I love to go down to the emergency room today. You enter that market and will you know nothing about the products of you being asked by no choice of those products. Hi I am Steve Brill I’ve got the cover story this week in TIME Magazine looking at the health care debate from a very different perspective. Everybody focuses on who should pay for the exorbitant cost of health care and that I decided to do was ask for more fundamental question which is why does health care cost so much.

I look behind the bills and trace the bills all the way back to who’s getting what money is making what profits and the results are really surprised one of the things I found that everybody in the healthcare industry knows about that that nobody else knows his something called the charge-master. The charge master is a internal listing each hospital of the thousands of different items that they charge and nobody could explain it to me. Indeed would be hard to explain for example why would you charge $77 for a box of gauze pads? You can buy for a dollar at the drugstore. why would you charge thousands of dollars for CAT scan it really isn’t cost you anything?

It’s emblematic if you will, of the irrationality of the higher healthcare system because no one can explain the cost no one tries to and the only people who are guaranteed surefire to pay to be asked to pay the charge-master prices are the poorest people who don’t have health insurance.

Real profit makers are way hospitals markup very expensive drugs that you get. If you have cancer to have pneumonia but they’re making thousands of dollars on these drugs and drug companies in turn making still more thousands of dollars.

Obamacare does very little to solve any of these problems and just probably why you got to Congress I’m it doesn’t do anything to control the prices of prescription drugs or medical devices CAT scan. In fact if anything it will increase the profitable the players in the market by making equal insurance and therefore more people are in the marketplace with the funds from insurance companies to buy all these products.

Insurance Companies are not really the problem they run pretty terribly. They process claims, a lot of us think they process claims and fairly consistently but they are increasingly at the mercy of hospitals which are consolidating buying a doctors practices. See Provider Consolidation Info-graph– “The proliferation of hospital mergers and hospitals’ appetite for buying doctors’ practices—in part to assure a steady stream of patients to fill hospital beds—could create local monopolies that raise prices without increasing efficiency. ‘Historically,’ says Deloitte’s Mr. Keckley, ‘hospital consolidation hasn’t reduced costs.’”

We should tax profits on so-called nonprofit hospitals and put that money back into the system. We should control all the prices for prescription drugs because if I have a monopoly a cancer wonder drug I can charge anything I want for them that’s obviously not a free market and it’s completely two different uses you see this article once you follow the money.”

The ACO (Accountable Care Organization) referenced in our post NYU Beth Israel Merger and ACOs are models encouraged in Obamacare in fact as examples of Provider capitated reimbursement that Howard Dean is in favor of. An ACOI cordiantes patient care and provide the full range of health care services for patients. The health reform law provides incentives for providers who join together to form such organizations and who agree to be accountable for the quality, cost, and overall care of Medicarebeneficiaries who are enrolled in the traditional fee-for-service program who are assigned to the ACO.

The fee-for-service system has evidentially driven costs by incentivizing volumes of added procedures. The ACO model is built on par excellence hospitals such as Mayo Clinic where there is team of providers are financially incentivized for patient care coordination outcomes and high quality of care. The ACO’s payment would be tied to achieving goals that improve health care and save money. Members of the ACO would divvy up that payment. Today’s payment system, investments in providing better care are doubly penalized. If a hospital hires a nurse to follow up with patients after they are discharged in order to reduce readmissions — for example, to help patients with diabetes improve blood sugar control — it must pay for the nurse, which is typically not reimbursed by insurance companies or Medicare, and it loses revenue by preventing the readmission.

Congress included ACOs in the health care law as a way to rein in Medicare spending. That federal program pays for health care for people 65 and older and the disabled. The federal government estimates ACOs could save the Medicare program up to $940 million over four years. Medicare recently began testing this system with 32 pilot ACOs in 18 states, including one in the New York City area – Bronx Accountable Healthcare Network.

Some have pointed to ACO Model just as a pro-merger supporting argument with the FTC. These significant mergers create market dominance and therefore limit competition and drive up health care dollars. And yet Hospitals operate on thin profit margins and cannot afford to lose market share therein lies is the conundrum.

Note: At time of this article MVP and Hudson Valley Health Plans announced a merger –Hudson Health Plans joins MVP. Hudson Health Plan, the Medicaid managed care organization based in Tarrytown, will join the MVP Health Care group of companies, the two nonprofit health plans jointly announced today.

“Size and diversity of offerings are important for health plans in the new world of the health insurance marketplaces. A 55-year-old person would like to join a health plan that can continue to cover him when he turns 65. Likewise, if someone is no longer eligible for Medicaid, she might prefer to buy a commercial product from that same insurer. Together, MVP and Hudson now can cover people through all of life’s stages and changing needs.

In the coming months, Millennium Medical Solutions Inc will host seminars and will share information you’ll need to know as the countdown continues to October 1st. Please contact us for immediate information on how to implement these initiatives for your group-specific needs at info@medicalsolutionscorp.com or Call (855) 667-4621.

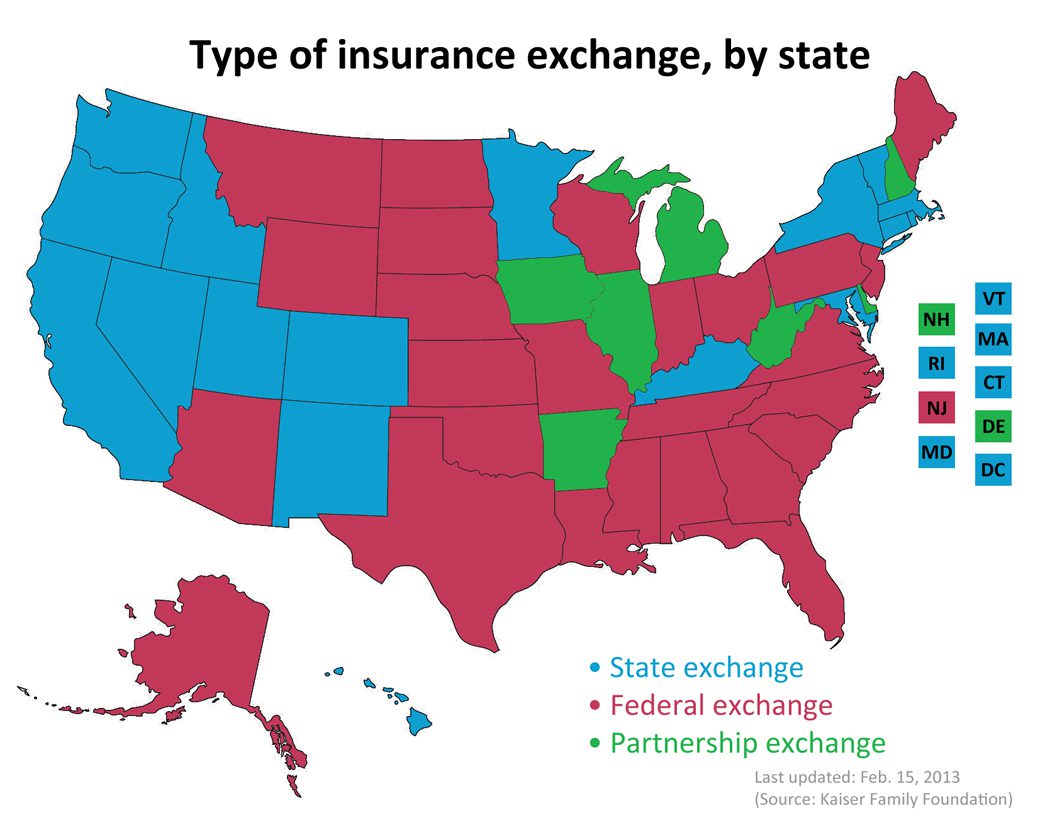

Map of State Exchanges Final. The final map of 2014 State Exchanges or health insurance marketplaces are now in.

States have had the option of either using Federal Grants to establish their own Exchanges or letting the Federal run their State’s Exchange. There is even a middle version, a Partnership Exchange Program. Under this arrangement, the State might oversee the selection and management of health plans and assisting people with enrollment. The federal government would have primary responsibility for the remaining marketplace operations, including managing the marketplace, their websites and call centers, accepting applications, and determining eligibility for premium subsidies.

Seventeen states and the District of Columbia have received conditional approval from HHS to operate a state-run marketplace in 2014. These states are: California, Colorado, Connecticut, Hawaii, Idaho, Kentucky, Maryland, Massachusetts, Minnesota, Nevada, New Mexico, New York, Oregon, Rhode Island, Utah, Vermont, and Washington.

This map is very close to last years blog we posted Map of State Exchanges Status May 2012 . For the most part this goes by partisan lines with majority of Federally Run State Exchanges located in GOP Governor States. An example of this is highlighted in our blog on NJ Exchange Chrstie Rejects State Exchange.

It is vital that as many uninsured’s get health coverage. Nationally approximately 30 million people are expected to gain coverage with 600,000 in States like NY.

Tick! tick! tick! As the 2014 Employer Mandate to either pay or play gets closer the nation’s employers move a step closer to having to make a decision: Do I play or pay? This Employer mandate under Patient Protection and Affordable Care Act (PPACA) does not apply to smaller groups under 50 FTE (full time equivalent) employees. Many small groups such as food service industry, retailers, construction etc. in fact have many FTE and while they may work minimal hours can trigger the “pay or play” mandate.

The IRS has released recently guidance published in the form of a Notice of Proposed Rulemaking (NPRM), addresses a number of issues tightly linked to an array of practical considerations related to the employer mandate. These include defining a “large employer,” determining “full-time” status for employees, clarifying the meaning of “dependents,” and determining what constitutes “affordable” coverage.

The guidance also tackles several stickier questions such as how and whether to count foreign or seasonal workers, as well as how to calculate the full-time status of employees who work unusual hours, such as teachers or airline pilots.

Three safe harbors relating to the provision of “affordable” coverage to employees in order to avoid exposure to the mandate penalties are also included in the guidance. Transition relief is offered in recognition of certain employers’ needing time to bring their plans into compliance.

Still, there are several regs that the IRS is awaiting commentary and resolution on due on March 18, 2013.

A Q&A summary of the rule has been released by the IRS and is available by clickinghere.

Some employers assert that the play-or-pay mandate will raise their costs and force them to make workforce cutbacks. As a result, a number are considering eliminating their health care coverage altogether and instead paying the penalty on their full-time employees. While the “pay” option might be worth considering, there are strong reasons why employers should look carefully at all of their options and do their best to calculate the actual outcomes of each.

Other Key Issues Addressed in the Proposed Rules Additional issues addressed in the proposed regulations include:

Determining which employers are subject to the “pay or play” requirements;

Determining who is a full-time employee, including approaches that can be used for employees who work variable hour schedules, seasonal employees, and teachers who have time off between school years;

Determining whether coverage is affordable and provides minimum value; and

Calculating the amount of the penalty due and how the penalty will be assessed.

When conducting a cost-benefit analysis, the key tax issues the employer should consider are:

Employer Tax Penalty for Not Offering “Qualified” Group Health

Not applicable for employers with less than 50 FTEs

$2,000 penalty per full-time employee (minus 30 employee credit)****

Employer Tax Penalty for Offering “Qualified” Health That is Not “Affordable”

Not applicable for employers with less than 50 FTEs

$3000 per employee receiving subsidy

Example:

Jungle Corp. has 100 full-time employees and is a leader in its market, using a talent differentiation strategy. Jungle’s family coverage costs $15,000, of which employees pay $3,000. Bob Smith, a highly skilled worker with a strong performance record, earns $50,000 and has family coverage through Jungle’s plan.

On Jan. 1, 2014, Jungle Corp. announces it is dropping its group health plan coverage and will instead pay the $2,000-per-full-time-employee penalty. On Jan. 2, Bob walks into HR and asks about receiving replacement compensation for the $12,000 that the business had been paying toward his family coverage.

Wanting to retain Bob in accordance with its strategy of maintaining market leadership with an experienced workforce, Jungle offers him another $12,000. But clever Bob points out that his share of Social Security and Medicare payroll (FICA) taxes will take a bite out of that $12,000, as will federal and state income taxes, so the HR manager agrees to make good on those amounts as well. Of course, the company will also have to pay its share of FICA taxes on Bob’s additional compensation. As a result, instead of paying $12,000 toward Bob’s family coverage using pre-tax dollars, Jungle Corp. now finds itself paying an additional:

Bob’s salary adjustment: $14,500

Employer’s share of FICA taxes: $1,109

Excise tax (penalty): $2,000 ———————————-

Total: $17,609 (versus $12,000 currently)

Similar per-employee costs will be reflected across the company’s workforce. A move that seemed like a no-brainer, the consequences could make you look silly.

For More Information Due to the complexity of the law in this area, and the absence of finalized guidance, employers are strongly advised to review their benefit plans to prepare for the changes ahead. Additional information regarding the penalty is featured on our Employer Shared Responsibilitypage.

In the coming months, Millennium Medical Solutions Inc will host seminars and will share information you’ll need to know as the countdown continues to October 1st. Please contact us for immediate information on how to implement these initiatives for your group-specific needs at info@medicalsolutionscorp.comor Call (855) 667-4621.

Fiscal Cliff Deal: Doc Cuts Spared. Happy 2013 Fiscal Cliff averted! At least for another year the dreaded 27% Medicare reimbursement have been spared. The so-called “doc fix” would boost the deficit by $31 billion. The President stood firm against any proposed Republican cuts to the Affordable Care Act.

The fear in provider cuts is grounded. According to The Lewin Report Patient Protection and Affordable Care Act (PPACA): Long Term Costs for Governments, Employers, Families and Providers “About half of program costs will be funded with reductions in payments to providers and health plans under the Medicare and Medicaid programs, which the CBO estimates will amount to $498 billion over the ten year period“. The new cost estimate has been updated to $1.4445 trillion from original estimate $938 billion over 10 years.

With millions of new uninsured patients slated to enter the system this would help providers recover reimbursement losses. Additionally, the President was firmly against any Provider cuts in 2013.

The Lewin Report predicts in fact that Provider Reimbursement will recover losses long term and in fact increase gross payments to $129.8 billion under the Act.

“..estimate that utilization of physician services will increase by about $102.7 billion under the Act. This estimate reflects Medicaid the payment levels for the portion of newly insured people covered under that program and commercial payment levels for those who become covered under private insurance. As discussed above, our key assumption is that utilization of services for newly insured people adjusts to the levels reported by insured individuals with similar age, gender, health status and income characteristics. Physicians also will be paid for services formerly provided free to uninsured people resulting in revenues of $8.4 billion. There will be an increase in reimbursement for people who shift from Medicaid to private coverage, and payment rates for Medicare primary care services will be increased for a three year period under the Act. These factors will add 18.7 billion in revenues for physicians.

While there was large Senate consensus 89-8 approval for the American Taxpayer Relief Act the health care debate is far from over. With rising health care costs, combined with the aging of the baby boomers, means the entitlement programs will remain at the heart of the tax-and-spending battles to come.

New Proposed Rules for Wellness ProgramsIn another step forward to ncentivize wellness new proposal can give discounts for managing good health much like good drivers with auto insurance.Newproposed rules issued under Health Care Reform address certain amendments to the nondiscrimination requirements for group health plans offering a wellness program to comply with the federal Health Insurance Portability and Accountability Act(HIPAA).Specifically, the proposed rules would increase the maximum permissible reward under a wellness program that requires an individual to satisfy a standard based on a health factor in order to obtain a reward, from 20% to 30% of the cost of coverage (and to 50% for programs designed to prevent or reduce tobacco use). The rules also include other proposed clarifications regarding the requirements for such wellness programs to avoid prohibited discrimination, including reasonable design and reasonable alternatives that must be offered for individuals to obtain the reward.Other Proposed Rules Released Under Health Care Reform Separately, new proposed rules have been issued for health insurance companies regarding the law’s requirements related to guaranteed availability of coverage and essential health benefits.

Under one set of proposed rules, issuers offering non-grandfathered health insurance coverage in the individual or group market would be required to accept every individual and employer that applies for coverage, with limited exceptions. Issuers in the individual and small group markets would be allowed to vary premiums within limits, only based on age, tobacco use, family size, and geography.

Another set of proposed rules outline issuer standards related to coverage of “essential health benefits.” Essential health benefits are a core set of items and services that must be covered by non-grandfathered plans in the individual and small group markets beginning in 2014.

While its always been known a healthy livingfor employees makes a productive employee. Large businesses have benefited from a healthy work force as they can better afford programs and have a direct rate reduction in rates.

Although employers continue to use cost shifting to control health insurance expenses, many companies are also making wellness programs part of the overall strategy to keep costs down by keeping staff members healthy.“Our entire health care system is organized around treating diseases after they occur, not preventing them before they occur. We need a paradigm shift that places prevention at the center of our health priorities.” – Lynn C. Swann, Chairman, President’s Council on Physical Fitness and Sports

The new proposed rules would apply for plan years beginning on or after January 1, 2014. An overview of the proposed rules is available on Healthcare.gov. Our Summary by Year offers updates on other requirements related to Health Care Reform.

“New Jersey and all other states still await substantial federal guidance on the functioning of all three types of exchanges,” Mr. Christie said in his veto message. “To be sure, the decision of whether to move forward with a state-based exchange can only be fully understood when competitively compared to the overall value of the other options.”

States have until Dec. 14 to decide whether to establish a state-based exchange. They have more time to decide whether to partner with the federal government or let federal bureaucrats design and run the state exchange. Many states with Republican governors have said they would not participate in the process, citing their opposition to the law and its potential costs. This is the current Map of State Exchange Status.

What is an Exchange? One of the centerpieces of the recently passed Patient Protection and Affordable Care Act (PPACA) is the establishment of state based health insurance exchanges by the year 2014.

An “Exchange” is a mechanism for organizing the health insurance marketplace to help consumers and small businesses shop for coverage in a way that permits easy comparison of available plan options based on price, benefits, service and quality. By pooling individuals and small groups together, transaction costs can be reduced and transparency can be increased. Exchanges can create more efficient and competitive markets for individuals and small employers.

States have until Dec. 14 to decide whether to establish a state-based exchange. They have more time to decide whether to partner with the federal government or let federal bureaucrats design and run the state exchange. Many states with Republican governors have said they would not participate in the process, citing their opposition to the law and its potential costs.

Many Republican governors were saying before the Court ruling that the Medicaid expansion was yet another unfunded federal mandate they could not afford. Yes the Supreme Court ruling has given the Republican governors enormous leverage. Republican governors have long argued that state control and flexibility can save lots of Medicaid money. If they put a reasonable plan on the table to expand their Medicaid programs to 133% of poverty–one that saves at least as much as their state match–it could be a win for everyone. The Republican governors get their flexibility and the Obama administration gets their expansion.