Breaking News President Announces Cancelled Policies Fix

Yesterday, the President announced that people with health care coverage that is not Affordable Care Act (ACA)-compliant may be able to keep their plans in 2014. Effectively “Grandfathering” of plans purchased after the original law has passed in 2010 There has been a great deal of concern being reported in the national media around the prospect of millions of people losing their health insurance coverage effective January 1, 2014 because of the Patient Protection and Affordable Care Act (“PPACA” aka “ObamaCare”).

We are awaiting how specifically your State’s Insurance Commissioner will react to this. Questions remain about how this new policy will work, including how insurance commissioners will react, whether insurance companies will choose to continue these policies, what the rates for the policies will be, and whether this grandfathering will extend past 2014.

To be clear, what’s being reported principally has to do with the individual health insurance market in the US which insures approximately 15 million people, or about 5% of the country’s population. Within that segment of the privately insured market, a large percentage, certainly more than half, of individual policies are not considered to be “grandfathered” under the law’s requirements for such status. As a result, to be in compliance with the law’s new mandates and coverage requirements, virtually all “non-grandfathered” policies are scheduled to be terminated January 1st, and it will be up to individuals to replace their existing coverage with new compliant policies after this date.

These recent developments have resulted in

1) President Obama issuing an apology to affected individuals on November 7th.

2) the President’s announcement earlier yesterday during a hastily called press conference at the White House that pursuant to an Executive Order, Americans may keep individual health insurance policies they were told will be canceled because these policies failed to meet requirements established by the new law.

President Obama has left it up to the states to independently determine how they will go about implementing this change which is being characterized as an “administrative fix”. However, since the insurance business is state-regulated, each state will need to determine whether or not they will implement this change, and if they choose to implement it, they will have control over defining some of the specific parameters. Insurance companies will also need to quickly make decisions on how to accommodate this new provision if the change is adapted in a state in which they operate.

In closing, if you should have any further questions or comments about the above or the attached, please let us know.We will continue to monitor this issue and all ACA implementation in an effort to keep you informed of new developments. In the meantime, please visit our https://360peo.com/about-us/blog to view past blogs and Legislative Alerts.

Governor Cuomo announced yesterday that New York’s Health Benefits Exchange have been approved . Additionally, the New York Times yesterday published an article highlighting that the rates in the individual market that will be offered in 2014 are at least 50 percent lower than they are now. The article link and Governor’s office press release are included below.

5 things we now know about the NYS Exchanges:

Importantly, Insurers must still confirm that they will be in either the individual exchange and/ or shop exchange

The rates approved yesterday are subject to final certification of the insurers’ participation in the exchange.

Many of the networks used on the Exchange appear to be smaller than the group rated.

Some new insurers have eneter the marketplace such as OSCAR and Freelancers. While a few such as EmblemHealth have taken a wait and see approach.

Additionally, NYS individual market rate will drop significantly in 2014 but they have been historically always the highest. An individual/Direct Pay HMO is approximately $1,000-$1,200/month. They are still approximately 18% highest.

The Department of Financial Services (DFS) has approved New York’s Health Health Insurance Exchange rates for 17 insurers seeking to offer coverage including eight new entrants into the market that do not currently offer commercial health insurance plans. Please click the following links for the Governor’s Press Release and the Individual and Small Group rates.

The following companies had health insurance plan rates for the health benefits exchange approved today by DFS. The rates approved today are subject to final certification of the insurers’ participation in the exchange.

Aetna

Affinity Health Plan, Inc.

The cheapest you’ll pay for individual health insurance in NY

American Progressive Life & Health Insurance Company of New York

Capital District Physicians Health Plan, Inc.

Health Insurance Plan of Greater New York

Empire BlueCross BlueShield

Excellus

Fidelis Care

Freelancers Co-Op

Healthfirst New York

HealthNow New York, Inc.

Independent Health

MetroPlus Health Plan

MVP Health Plan, Inc.

North Shore LIJ

Oscar Health Insurance Co.

United Healthcare

If you have additional questions regarding how SHOP Exchanges and Individual Exchanges can benefit you please contact our team at Millennium Medical Solutions Corp. Stay tuned for updates as more information gets released. We’re inside of 75 days until exchanges open, and information will be coming quickly in the next few months. Sign up for latest news updates.

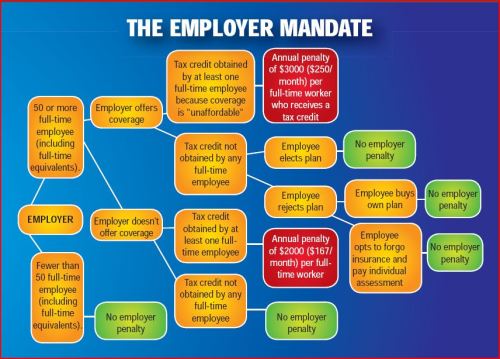

Obama administration announced that the employer shared responsibility mandate also known as “Pay or Play” aspect of the Patient Protection and Affordable Care Act (PPACA) will be delayed by one year.

This mandate requires businesses with 50 or more workers to provide health insurance coverage to employees. As a result, the administration will start enforcing the mandate in 2015, rather than January 1, 2014, in an effort to give businesses more time to prepare.

There will be additional changes tied to this delay, and the administration has stated that they will provide formal guidance within the next week.

More details will be available for our July 11th WebMeeting. Medical Solutions Corp is working with the various regulatory agencies to understand the specifics surrounding this ruling, and will continue to provide updates through Legislative Alerts and on our blog.

The sheer technological volume of it all could bring “rolling brown outs” similar to electrical grids. Try to imagine a scenario of credit union Experien working with IRS then Social Security & Center for Medicare & Medicaid Services’s dated mainframe computer system while balancing HIPAA and privacy sensitive information. All this while millions of people converge simultaneously onto the information highway. Visualize all of the U.S. Daily Commuters driving into Manhattan today.

As reported below by Reuters’ Sharon Begley Obamacare 1.0: States brace for Web barrage when reform goes live: “Obamacare, formally known as the Patient Protection and Affordable Care Act (ACA), could fail for many reasons, including participation by too few of the uninsured and a shortage of doctors to treat those who do sign up. But because its core is government-run marketplaces selling health insurance online, the likeliest reason for failure at the opening bell is information technology snafus, say experts who are helping with the rollout.”

(Reuters) – About 550,000 people in Oregon do not have health insurance, and Aaron Karjala is confident the state’s new online insurance exchange will be able to accommodate them when enrollment under President Barack Obama’s healthcare reform begins on October 1.

What Karjala, the chief information officer at “Cover Oregon,” does worry about, however, is what will happen if the entire population of Oregon – 3.9 million – logs on that day “just to check it out,” he said. Or if millions of curious souls elsewhere, wondering if Oregon’s insurance offerings are better than their states’, log on, causing Cover Oregon to crash in a blur of spinning hourglasses and color wheels and an epidemic of frozen screens.

Multiply that by another 49 states and the District of Columbia, all of which will open health insurance exchanges under “Obamacare” that same day, and you get some idea of what could go publicly and disastrously wrong.

Obamacare, formally known as the Patient Protection and Affordable Care Act (ACA), could fail for many reasons, including participation by too few of the uninsured and a shortage of doctors to treat those who do sign up. But because its core is government-run marketplaces selling health insurance online, the likeliest reason for failure at the opening bell is information technology snafus, say experts who are helping with the rollout.

Although IT is the single most expensive ingredient of the exchanges, with eight-figure contracts to build them, experts expect bugs, errors and crashes. In April, Obama himself predicted “glitches and bumps” when the exchanges open for business.

“This is a 1.0 implementation,” said Dan Maynard, chief executive of Connecture, a software developer that is providing the shopping and enrollment functions for several states’ insurance exchanges. “From an IT perspective, 1.0’s come out with a lot of defects. Everyone is waiting for something to go wrong.”

Two states that intended to build their own exchanges, Idaho and New Mexico, announced this spring that because of the tight timeline and daunting challenges they would have the federal government operate their IT systems.

“Nothing like this in IT has ever been done to this complexity or scale, and with a timeline that put it behind schedule almost before the ink was dry,” said Rick Howard, research director at the technology advisory firm Gartner.

WHAT COLOR WAS YOUR VOLVO?

The potential for problems will begin as soon as would-be buyers log onto their state exchange. They’ll enter their name, birth date, address and other identifying information. Then comes the first IT handoff: Is this person who she says she is?

To check that, credit bureau Experian will check the answers against its voluminous external databases, which include information from utility companies and banks on people’s spending and other history, and generate questions. The customer will be asked which of several addresses he previously lived at, for example, whether his car has one of several proffered license plate numbers, and what color his old Volvo was.

It’s similar to the system that verifies identity for accessing personal Social Security information. If someone gets a question wrong, he will be referred to Experian’s help desk, and if that fails may be asked to submit documentation to prove he is who he claims to be.

The next step is determining if the customer is eligible for federal subsidies to pay for insurance. She is if she is a citizen and her income, which she will enter, is less than four times the federal poverty level. To verify this, the exchange pings the “federal data services hub,” which is being built by Quality Software Services Inc under a $58 million contract with the Centers for Medicare & Medicaid Services (CMS).

The query arrives at the hub, which does not actually store information, and is routed to online servers at the Internal Revenue Service for income verification and at the Department of Homeland Security for a citizenship check.

The answers must be returned in real time, before the would-be buyer loses patience and logs off. If the reported income doesn’t match the IRS’s records, the applicant may have to submit pay stubs.

These federal computer systems have never been connected before, so it’s anyone’s guess how well they’ll communicate.

“The challenge for states,” said Jinnifer Wattum, director of Eligibility and Exchange Solutions at Xerox’s government healthcare unit, is that they have to build “the interfaces needed with the federal data services hub without knowing what this system will look like.” That makes the task akin to making a key for a lock that doesn’t exist yet.

CMS’s contractors are working to finish the hub, but “much remains to be accomplished within a relatively short amount of time,” concluded a report from the Government Accountability Office (GAO), the investigative arm of Congress, in June. CMS spokesman Brian Cook said the hub would be ready by September, and that the beta version had been tested for its ability to interact with the exchanges Oregon and Maryland are building.

The federal hub has to verify even more arcane data, such as whether the insurance offered to a buyer through his job is unaffordable, in which case he may qualify for federal subsidies, and whether the buyer is in prison, in which case she is exempt from the mandate to purchase insurance.

If someone’s income qualifies him for Medicaid, or his children for the Children’s Health Insurance Program (CHIP), software has to divert him from the ACA exchange and into those systems. Many of the computers handling Medicaid and CHIP enrollment are, as IT people diplomatically put it, “legacy systems,” meaning old, even decades old.

Many are mainframes, lacking the connectivity of cloud computing. They typically process eligibility requests in days, not seconds.

The legacy systems “rely on daily or weekly batch files to pass information back and forth,” and often require follow-up phone calls, said Wattum of Xerox, which is working to configure Nevada’s exchange so it can interface with the federal hub.

‘NO WRONG DOOR’

A “we’ll call you” message is unacceptable under Obamacare, which has a “no wrong door” goal: A buyer must never come to a dead end. If she is diverted to Medicaid, for instance, she must not be required to resubmit information, let alone wait a week for an answer about whether she’s now enrolled.

State IT systems must therefore “be interoperable and integrated with an exchange, Medicaid, and CHIP to allow consumers to easily switch from private insurance to Medicaid and CHIP,” said an April report from the Government Accountability Office (GAO), the investigative arm of Congress.

To make all those systems communicate, the state exchanges must either develop entirely new systems or use application programming interfaces (APIs) that work with the legacy systems to exchange data in real time. APIs are programming instructions for accessing Web-based software applications.

GAO’s Stan Czerwinski compares the necessary connectivity to adapters that let Americanelectronics work with European outlets.

State officials told the GAO that verifying eligibility, enrolling buyers and interfacing with legacy systems are the most “onerous” aspects of developing their exchanges, “given the age and limited functionality of current state systems.”

A key goal for exchange officials is keeping would-be buyers in the portal so they don’t give up and use a state’s ACA call center, which could quickly be swamped.

To avoid this, Oregon brought in potential users to test design prototypes, recorded what people did and where they had trouble, and tweaked the consumer interface to make it as user-friendly as possible, said Karjala.

“Even with that, if you have a family of four and you’re eligible for a tax credit to offset your premium,” he said, “you could be sitting at the computer for a long time.”

What everyone hopes to avoid is a repeat of the early days of the Medicare prescription-drug program in 2006. Some seniors who tried to sign up for a plan were mistakenly enrolled in several, while others had the wrong premium amounts deducted from their Social Security checks.

Another challenge is capacity. Websites regularly crash when too many people try to access them.

“I had no choice but to be extremely conservative” in estimates of how many simultaneous users Cover Oregon has to be prepared for, Karjala said. “Building capacity is the only way to avoid the spinning hourglass or the site freezing, so in our performance testing we’re seeing what happens if the whole U.S. population came to Cover Oregon to check it out.”

This summer, state exchanges will test their ability to communicate with the federal data hub, whose security frameworks and connectivity protocols are still works in progress. But whether Obamacare 1.0 flies won’t be known until the new health plans take effect on January 1. Robert Laszewski, president of Health Policy and Strategy Associates Inc, a consulting firm, said he wouldn’t be surprised if some patients showing up at doctors’ offices next year with Obamacare policies are told their insurers never heard of them.

(Additional reporting by Caroline Humer; Editing by Michele Gershberg and Prudence Crowther)

Final Wellness Incentive Rule Released. Final rules set forth the criteria for wellness programsoffered in connection with group health plans that must be satisfied in order for the plan to qualify for an exception to the prohibition on discrimination based on health status under the federal Health Insurance Portability and Accountability Act (HIPAA). The final rules will be effective for plan years beginning on or after January 1, 2014.

Many employers already offered incentives for employees participating in wellness programs. The main change in the new rule is an increase in the maximum incentive levels for several PPACA designated programs. For smoking cessation efforts, employers will be allowed to offer a reward or penalty of up to 50% of an employee’s health plan cost. For all other wellness programs, the number will be 30%, up from the current 20%. These increases are intended to promote healthy behavior which in turn, advocates claim, reduce health care spending.

Key Highlights Significant provisions included in the final rules include:

Increasing the maximum permissible reward under a health-contingent wellness program, from 20% to 30% of the cost of coverage;

Further increasing the maximum permissible reward for wellness programs designed to prevent or reduce tobacco use, from 20% to 50% of the cost of coverage; and

Clarifications regarding the reasonable design of health-contingent wellness programs and the reasonable alternatives they must offer in order to avoid prohibited discrimination.

Types of Participatory Wellness Programs The final rules continue to divide wellness programs into two categories:

1)”participatory wellness programs,” which are a majority of wellness programs,

2)and “health-contingent wellness programs.”

A participatory wellness program is one that either does not provide a reward or does not include any conditions for obtaining a reward that are based on an individual satisfying a standard related to a health factor. These include programs that reimburse for the cost of membership in a fitness center; provide a reward to employees for attending a monthly, no-cost health education seminar; or reward employees who complete a health risk assessment, without requiring them to take further action.

Participatory wellness programs are generally permissible under the HIPAA nondiscrimination rules, provided they are available to all similarly situated individuals regardless of health status.

Health-Contingent Wellness Programs In contrast, a health-contingent wellness program requires an individual to satisfy a standard related to a health factor to obtain a reward. This standard may be performing or completing an activity (an “activity-only wellness program”), or it may be attaining or maintaining a specific health outcome (an “outcome-based wellness program”).

Examples of health-contingent wellness programs include programs that provide a reward to those who do not use, or decrease their use of, tobacco, or programs that reward those who achieve a specified health-related goal, such as a specified cholesterol level, weight, or body mass index, as well as those who fail to meet such goals but take certain other healthy actions.

In order to qualify for an exception to the HIPAA nondiscrimination rules, health-contingent wellness programs must meet five additional standards related to frequency of opportunity to qualify; size of the reward; reasonable design; uniform availability and reasonable alternative standards; and notice of the availability of reasonable alternative standards.

Example

The final rule provides an example of how this reward/penalty might work:

An employer sponsors a group health plan. The annual premium for employee-only coverage is $6,000 (of which the employer pays $4,500 per year and the employee pays $1,500 per year). The plan offers employees a health-contingent wellness program with several components, focused on exercise, blood sugar, weight, cholesterol, and blood pressure. The reward for compliance is an annual premium rebate of $600…[T]he plan also imposes an additional $2,000 tobacco premium surcharge on employees who have used tobacco in the last 12 months and who have not enrolled in the plan’s tobacco cessation program (Those who participate…are not assessed the $2,000 surcharge).

The total of all the rewards (including the absence of a surcharge for participating in the tobacco program) is $2,600…which does not exceed the applicable percentage of 50% of the total annual cost of employee-only coverage ($6,000 x 50%=$3,000). Tested separately, the $600 reward for the wellness program [excluding] tobacco use does not exceed the applicable percentage of 30 percent of the total annual cost of employee-only coverage ($6,000 x 30%=$1,800).

In excellent article in the Atlantic –The Future of Getting Paid to Be Healthy“Incentive programs are not wellness programs,” said Dr. Ronald Goetzel, Director of Emory University’s Institute for Health and Productivity Research and President and CEO of The Health Project. “That can be a component, when done smartly, of a comprehensive program, but if that’s all your program is going to be, you’re going to fail miserably, and people are going to be resentful,” he explained. According to Goetzel — who has studied worksite wellness programs at large corporations such as Dow Chemical and Johnson & Johnson, and is being funded by the Centers for Disease Control and Prevention to study best practices in the field — incentive programs can help get people excited about health and keep them on track, but ultimately people’s habits will only change if they are given the resources to change them and if the workplace norms and environments change.

Without the other pieces to facilitate behavior change — healthy cafeterias, opportunities to exercise, flexible work hours, supportive leadership and middle managers, and health risk assessments and coaching — incentive programs will only penalize, not change, those who are least healthy.

For more information, you may review the final rules in their entirety. For MMS Corp previous blogs on wellness, click here. we will keep you posted on future PPACA wellness program opportunities. In the meantime, please visit to view past blogs and Legislative Alerts at https://360peo.com/feed.

The views expressed in this post do not necessarily reflect the official policy, position, or opinions of MMS Corp. This update is provided for informational purposes. Please consult with a licensed accountant or attorney regarding any legal and tax matters discussed herein.

With only 6 month away from full implementation of 2014 Patient Protection Affordability Care Act (PPACA) employers are understandably uncertain. Below are Health Care reform – five things employers can do now to prepare and take action.

UPDATE JULY 2nd: Since blog posting the President Administration has delayed 1 year Employed Shared Responsibility Mandate i.e. Pay or Play to Jan 2015.

1. Employee Communications

Employers must notify employees of the online insurance marketplace known as a Healthcare Exchange. Recently released federal guidelines require employers to notify their workers of eligibility requirements for their state exchange starting Oct. 1, 2013 Open Enrollments for Jan 2014 effective date. To the relief of many, the U.S. Labor Department also provided model notices that employers can give to their workers, which eliminates the need to develop their own notifications.

Additionally, Employers sponsoring a health plan must give employees a Summary of Benefits and Coverage (SBC). The purpose of the Summary of Benefits and Coverage, or SBC, is to present benefits and coverage information in clear language and in a consistent format. Inspired by the Nutrition Facts Label on packaged food, theSBC (pdf) includes two medical scenarios: having a baby and managing Type II diabetes. It estimates how much a patient would pay for medical care in each scenario with specific insurance plans.

It’s the employer’s responsibility to distribute the SBCs to employees.

This requirement applies to health plan renewals after Sept. 23, 2012.

Department of Labor will NOT impose penalties for non-compliance with the SBC notice during the first year as long as employers show a “good faith” effort to comply. Read the FAQ on SBC and ACA pdf here.

2. Determining which Employers must offer health care.

Because employers with 50 full-time equivalents face penalties for not providing affordable, minimum value insurance an employer should know whether it is subject to these requirements or not. Common law employees of the employer and any commonly controlled company must be counted. Employers with temporary or leased employees will want to discuss with their advisors whether these employees will be considered “common law employees” for purposes of determining how many FTEs an employer has. Employers with employees who are paid based on unique payment models (stipends, work product, etc) will want to discuss how to calculate these employee hours with their benefits advisors.

Employers with 50 or more employees will incur penalties of up to $2,000 per employee if they cancel their existing health care program (which up until 2014 would be considered an optional benefit to provide). They will also incur penalties if their plan is too costly, and they do not meet the affordability standards.

Employers with less than 50 employees will not incur penalties if they cancel their health care plan, and that decision will need to be made on a business by business basis. They can also choose to offer partial coverage and contribute up to the minimum 50% of single coverage not to exceed 9.5% employee

The good news is Employers can subtract 30 FT employees. This portion is known as the Employer “play or pay” option. Specific case example and details are found at Pay or Play Employer Guide.

To encourage businesses to offer health benefits to their employees, the federal government is offering tax credits to small businesses. These credits are available to an estimated 4 million small businesses, including nonprofits.The IRS has set up a web page with information: Small Business Health Care Tax Credit for Small Employers. The maximum “credit” (which offsets taxes dollar for dollar and is better than a “deduction” which reduces taxable income) is 35 percent of the amount an employer pays towards employee health insurance.

Who’s eligible?

To qualify, small employers must:

Have fewer than the equivalent of 25 full-time workers

Pay average annual wages below $50,000

Cover at least 50% of the cost of health care coverage for their workers

Because of the high wages paid in most industries in NY/NJ/CT Tri State, few small employers that provide coverage pay such a low average wage. Note, however, that the calculation of average wages and number of employees excludes the wages of an owner and his or her family members.

medicalsolutionscorp.com help clients gather the appropriate information and do a preliminary estimate of the credit amount. This information will help you and your accountant determine whether applying for the credit makes financial sense. Find out what the new tax credit could mean for your coverage. Call us at 855-667-4621.

4. Determine affordability

Beginning Jan. 1, 2014, an employer with 50 or more employees must pay a tax penalty if they either: a) Do not provide health insurance with minimum benefits or 60 percent of healthcare expenses; b) Require employees to contribute more than 9.5 percent of an employee’s household income for the health insurance and those employees obtain a government subsidy for coverage.

Companies will be required to pay $3,000 per employee without affordable coverage. (Note: there are a number of caveats that might affect the actual penalty paid, so consult your tax advisor.)

It is crucial to Understand the difference between FT and Full Time Equivalent. To determine the FTE (Full Time Equivalent) you must count FT and PT employees. Full Time Employees are those working 30 hours+/week.* The number of full-time employees excludes those full-time seasonal employees who work for less than 120 days during the year.4 The hours worked by part-time employees (i.e., those working less than 30 hours per week) are included in the calculation of a large employer, on a monthly basis, by taking their total number of monthly hours worked divided by 120.

For example, a firm has 35 full-time employees (30+ hours). In addition, the firm has 20 part time employees who all work 24 hours per week (96 hours per month). These part-time employees’ hours would be treated as equivalent to 16 full-time employees, based on the following calculation:

20 employees x 96 hours / 120 = 1920 / 120 = 16

Thus, in this example, the firm would be considered a “large employer,” based on a total full-time equivalent count of 51—that is, 35 full-time employees plus 16 full-time equivalents based on part-time hours.

In the coming months, Millennium Medical Solutions Inc will host seminars and will share information you’ll need to know as the countdown continues to October 1st.

Error: Contact form not found.

This blog is not intended to represent legal advise and one should consult with a tax and/or legal expert.

* IRC 4980H(c)(4)

Disclaimer: This blog is not intended to represent legal advise and one should consult with a tax and/or legal expert.