Clinton vs Trump Healthcare. A helpful overview from SHRM on the differences between the Candidates. They presumably agree on repealing the Cadillac Tax and well-needed price transparencies.

HILLARY CLINTON’S HEALTH CARE REFORM PLAN:

Defend the Affordable Care Act. Clinton will continue to defend the ACA against Republican efforts to repeal it.

Lower out-of-pocket costs like copays and deductibles. The average deductible for employer-sponsored health plans rose from $1,240 in 2002 to about $2,500 in 2013. Clinton believes that workers should share in slower growth of national health care spending through lower costs.

Reduce the cost of prescription drugs. Prescription drug spending accelerated from 2.5 percent in 2013 to 12.6 percent in 2014. It’s no wonder that almost three-quarters of Americans believe prescription drug costs are unreasonable. Clinton believes we need to demand lower drug costs for hardworking families and seniors.

Build on the Affordable Care Act and require plans to provide three sick visits without counting toward deductibles every year. The Affordable Care Act required nearly all plans to offer many preventive services, such as blood pressure screening and vaccines, with no cost-sharing at all. But because average deductibles have more than doubled over the past decade, many Americans would have to pay a significant cost out-of-pocket toward their deductible if they get sick and need to see a doctor. Clinton’s plan will build on the Affordable Care Act by requiring insurers and employers to provide up to three sick visits to a doctor per year without needing to meet the plan’s deductible first.

Provide a new, progressive refundable tax credit of up to $5,000 per family for excessive out-of-pocket costs. For families that still struggle with prescription drug costs even after out-of-pocket limits on drug spending and free primary care visits, Clinton’s plan will provide progressive, targeted new relief. Americans with health coverage will be eligible for a new refundable tax credit of up to $2,500 for an individual, or $5,000 for a family, available to those with substantial out-of-pocket health care costs. The credit will be available to insured Americans with qualifying out-of-pocket health expenses in excess of five percent of their income, and who are not eligible for Medicare or claiming existing deductions for medical costs. This refundable, progressive credit will help middle-class Americans who may not benefit as much from currently-available deductions for medical expenses. This tax cut will be fully paid for by demanding rebates from drug manufacturers and asking the most fortunate to pay their fair share.

Enforce and Broaden the ACA’s Transparency Provisions. Americans deserve real-time, updated, and reliable information to guide them in selecting a health plan, navigating changes to their out-of-pocket costs in their existing plan, choosing a doctor, and determining how much they will need to pay for a prescription drug. Clinton’s plan will vigorously enforce existing law under the Affordable Care Act and adopt further steps to make sure that employers, providers, and insurers provide this information through clear and accessible forms of communication so that Americans can make informed choices about their coverage and realize meaningful savings.

Repeal ACA -Modify existing law that inhibits the sale of health insurance across state lines. As long as the plan purchased complies with state requirements, any vendor ought to be able to offer insurance in any state. By allowing full competition in this market, insurance costs will go down and consumer satisfaction will go up.

Tax deductible health insurance premium payments. Allow individuals to fully deduct health insurance premium payments from their tax returns under the current tax system. -Allow individuals to use Health Savings Accounts (HSAs). Contributions into HSAs should be tax-free and should be allowed to accumulate. These accounts would become part of the estate of the individual and could be passed on to heirs without fear of any death penalty. These plans should be particularly attractive to young people who are healthy and can afford high-deductible insurance plans. These funds can be used by any member of a family without penalty. The flexibility and security provided by HSAs will be of great benefit to all who participate.

Price transparency. Require price transparency from all healthcare providers, especially doctors and healthcare organizations like clinics and hospitals. Individuals should be able to shop to find the best prices for procedures, exams or any other medical-related procedure.

Reform mental health programs. Families, without the ability to get the information needed to help those who are ailing, are too often not given the tools to help their loved ones. There are promising reforms being developed in Congress that should receive bi-partisan support.

Block-grant Medicaid to the states. Nearly every state already offers benefits beyond what is required in the current Medicaid structure. The state governments know their people best and can manage the administration of Medicaid far better without federal overhead. States will have the incentives to seek out and eliminate fraud, waste and abuse to preserve our precious resources.

Remove barriers to entry into free markets for drug providers that offer safe, reliable and cheaper products. Though the pharmaceutical industry is in the private sector, drug companies provide a public service. Allowing consumers access to imported, safe and dependable drugs from overseas will bring more options to consumers.

Add our blog & sign up for newsletter on latest in Healthcare Reform News. Please contact us for a free evaluation on your group’s benefits at 855-667-4621.

Health and Human Services had released earlier this year the final version of its 2017 Notice of Benefit and Payment Parameters. Under the Affordable Care Act (ACA) this is issued annually. While the guidance is mostly relate dot the individual marketplace itt does, however, include several items relevant to employers and group health plans, specifically:

Annual limits for cost sharing (out-of-pocket limits)

Marketplace eligibility notifications to employers

Marketplace annual open enrollment period

Small Business Health Options (SHOP) Exchange

ANNUAL LIMITS FOR COST SHARING:

The annual out of pocket limits for plan years beginning on or after January 1, 2017 are $7,150 for individual coverage and $14,300 for family coverage. These cost sharing limits apply to in-network essential health benefits offered under non-grandfathered health plans, both fully and self-insured. Annual deductibles, in-network co-insurance and other types of in-network cost sharing accumulate toward the out-of-pocket limit, including prescription drug copayments. Not included are premium payments, out-of-network cost sharing and spending on non-essential health benefits.

MARKETPLACE ELIGIBILITY NOTIFICATIONS TO EMPLOYERS:

Beginning in 2017, the Marketplace will notify an employer as soon as possible when one of its employee’s first enrolls in subsidized Marketplace coverage. Since some employers may be liable for a penalty under the ACA’s employer mandate when an employee qualifies for a subsidized Marketplace coverage, this change to a more proactive notification process will hopefully provide employers with the opportunity to work with CMS in cases where an improper subsidy has been provided.

MARKETPLACE ANNUAL OPEN ENROLLMENT PERIOD:

Open Enrollment in the Health Insurance Marketplace, Healthcare.gov, for 2017 and 2018 will take place from November 1, 2016 through January 31, 2017 and November 1, 2017 through January 31, 2018, respectively.

SMALL BUSINESS HEALTH OPTIONS (SHOP) EXCHANGE:

Beginning in 2017, small employers electing coverage in the SHOP Exchange will have the option of “vertical choice,” offering plans across all metal levels (platinum, gold, silver and bronze) from one insurer. States who opt out of the vertical choice option will continue to offer employers the choice of selecting health plans that are available at one single metal level of coverage.

Stay proactive and contact us today for a custmozied consult on how your organization can prepare ahead for ACA, Benefits, Payroll and HR @ (855) 667-4621 or info@medicalsolutionscorp.com.

According to a released study by United Hospital Fund May 2016 report Insurance companies operating on New York’s individual exchange market lost $100 million in 2014.

With recent news of Insurers reporting mounting losses (UnitedHealthcare will drop ACA exchanges) on the Individual Marketplace it wouldn’t be surprising for the next year’s Study to show even greater losses in 2015. As reported last month, the average NYS 2017 Rate Requests for individual marketplace was 17.3%.

Lower premiums, reinsurance and subsidies made coverage more affordable. “For many years in New York, annual individual premium increases far outpaced the offsetting effects of both a $38 million state-funded reinsurance program,12 and a risk-adjustment mechanism that provided a cross-subsidy from the small group market to the individual market, valued at $62 million in 2009.13 In 2014, new enrollment, PHSP participation, more competitive pricing, a better risk pool, and a federal reinsurance program resulted in an average individual monthly premium of $430.97 in New York.” The ACA subsidies reduced premiums by an average of $215/month

NYS Obamacare Future?

“More affordable premiums have been a key factor in the growth of the individual market. The loss of federal reinsurance payments will create an upward pressure on rates, and the absence of federal risk corridor reimbursement will also continue to reverberate.” Consumers with Obamacare subsidies will be shielded from most of the premium increases that may occur, but off-Exchange enrollees and NYSOH customers without subsidies could face significant monthly increases.

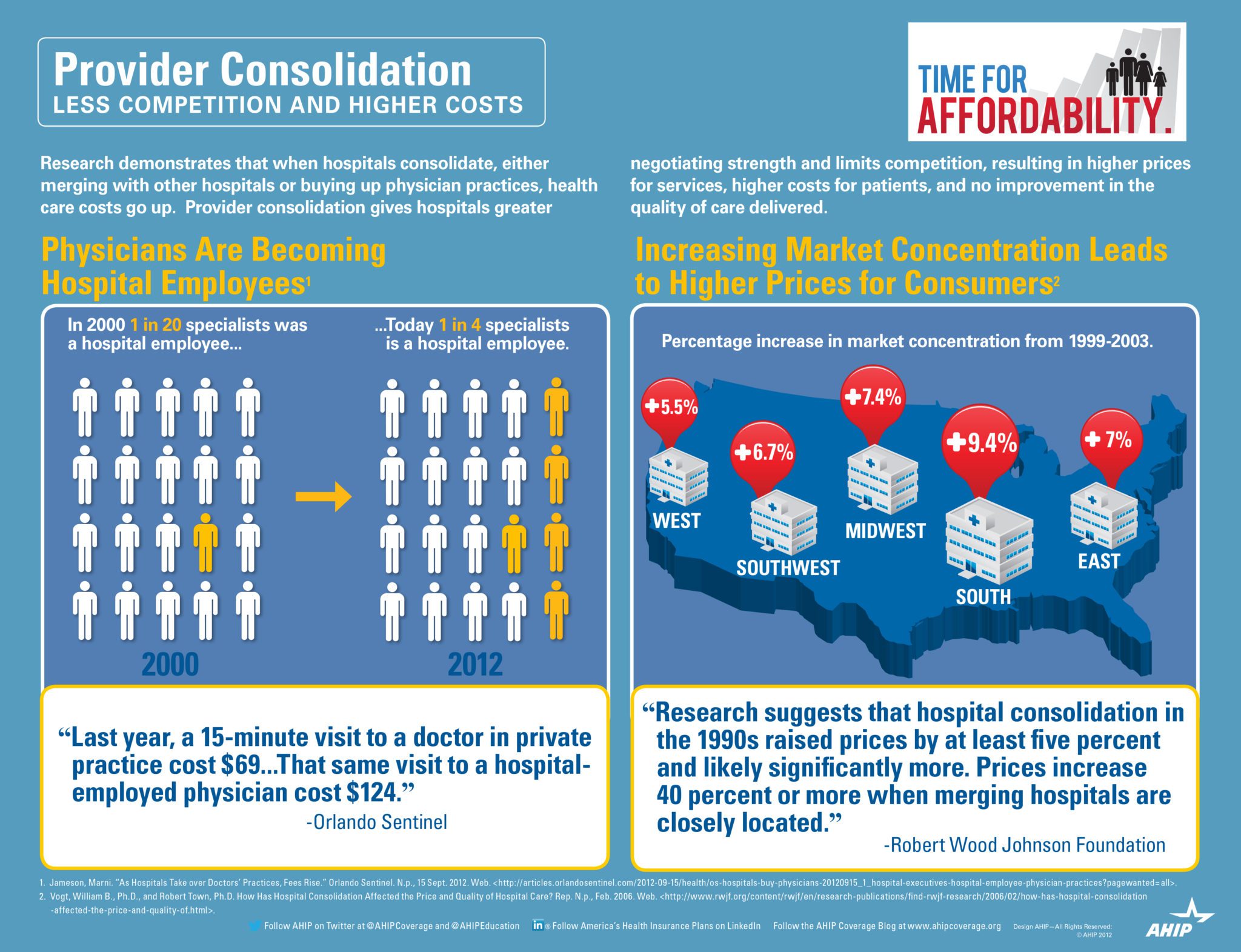

Insurance mergers aka Mergersurance Mania continues at a steady pace with April 2016 Florida’s approval of Anthem Blue Cross and CIGNA merger. This is one month after Florida approved the Aetna and Humana merger. Investors have given their blessings to be sure while 10 States have also given approval. The Anthem Cigna $54 billion merger leaves only three national major providers of health care. Worries remain about the potential effect on consumers and the rising cost of health care.

Health Insurers consolidation argument are that they need to be able to merge in order to absorb added costs and blunted profit margins under the Affordable Care Act. Additionally, medical groups and hospitals groups have merged themselves rapidly giving them negotiation cost controls. This has traditionally been trending in smaller regional markets but are now also felt in major US Cities.

Evidence indeed is pointing to expected large insurance increases due to overwhelming market domination by hospitals. While Doctors and AMA are rightfully concerned about Insurer mergers the vast majority are now working for a Hospital System or Medical IPA.

Without public outcry there seems to be lax Regulator oversight and the arms race should not come as a surprise. On the local level we have yet to see a recent example of hospital merger that was curtailed.

This goes well beyond political partisanship. In a tight Presidential race it is important to understand that whether or not one supports a Single Payer we all suffer. This is bad for consumers, providers and tax payer all around. In an Oligopoly health care system with lack of competition the U.S. tax payers are also stuck with inflated costs.

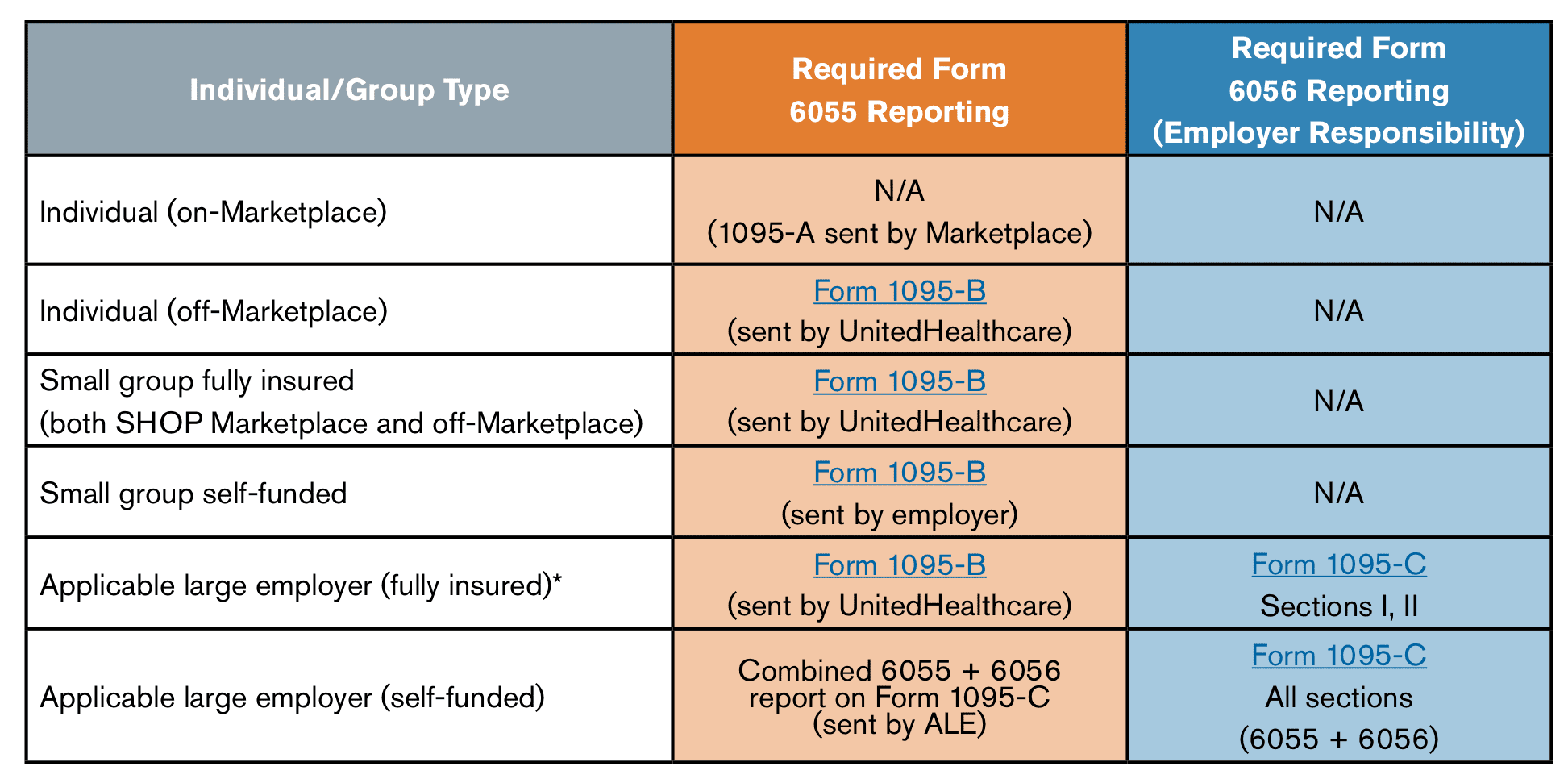

Under Obamacare, the IRS needs to know if your coverage met health care reform standards. The 1095-B is issued by Insurers on behalf of fully insured members directly to the IRS and send members a copy. In short you don’t have to do anything other than reviewing the info and confirming accuracy. 1095B and 6055 Reporting Requirements FAQ

The IRS will accept any number of items to prove that a member had insurance including:

insurance cards

explanation of benefits statements from your insurer

W-2 Form or payroll statements reflecting health insurance deductions

records of advance payments of the premium tax credit

other statements indicating that you, or a member of your family, had health care coverage

What information is on the 1095-B form?

For each person covered on your policy, the 1095-B lists:

Name

Address

Date of birth

Taxpayer identification number (most likely a Social Security number)

Months of coverage with us

If you are missing the taxpayer ID or Social Security numbers for anyone on your policy, the Insurer send you a letter. It’ll explain why they need the information and how to send it to Insurers securely.

How do I know if I should get a 1095-B form?

Insuerers send you a 1095-B form if:

You bought your coverage directly and did NOT go through healthcare.gov.

You get employer coverage and it met the health care reform standards.

6055 Reporting on Form 1095-B

6056 Reporting on Form 1095-C

Provided by Insurer for insured medical plan; by employer for a self-insured medical plan

Provided by applicable large employer (ALE)

Provided to each covered “responsible individual” (e.g., employee, COBRA QB, retiree)

Provided to each full time employee

Provided by March 31, 2016 for coverage in prior calendar year

Provided by March 31, 2016 for coverage offered in prior calendar year

Transmitted with employer’s Form 1094-B to IRS by May 31, 2016 (June 30, 2016 if filed electronically)

Transmitted with employer’s Form 1094-C to IRS by May 31, 2016 (June 30, 2016 if filed electronically)

If your organization can use a helpful audit on ACA, Payroll and HR please contact us today (855) 667-4621 or info@medicalsolutionscorp.com.

This communication is not intended, nor should it be construed, as legal or tax advice. Please contact a competent legal or tax professional for legal advice, tax treatment and restrictions. Federal and state laws and regulations are subject to change.

The Cadillac Tax has been delayed for two years from 2018 to 2020 by President Obama. With this delay, a repeal could be in reach for congressional leaders and business groups who oppose the Cadillac tax. The legislation also suspends the medical device tax until December 31, 2017 and delays the health insurance tax one year.

Whats a Cadillac Tax?

The 40% excise tax applies to the cost of employer health plan coverage exceeding certain threshold amounts, which were originally set for 2018 at $10,200 for individuals or $27,500 for families. These thresholds are indexed and will be higher on the delayed effective date in 2020. The Omnibus also calls for a study on how to determine adjustments to these thresholds to reflect age and gender differences between businesses. While the tax was originally non-tax deductible, the Omnibus changes that treatment and makes the tax deductible. Originally, the Cadillac Tax was pushed back by the behest of Unions to 2018 from the original proposed 2014 date. Most Unions with generous health care packages would not be complaint within that time frame.

Bipartisanship

The bipartisan vote on the Consolidated Appropriations Act was 316 to 113 in the House, and 65 – 33 in the Senate. Many employers, unions, insurers and industry groups have opposed the tax based on concerns around administrative and financial burdens for employers and adverse outcomes for employees.

Medical Device Tax

The tax bill will place a two-year moratorium on the ACA’s 2.3% tax on the sale of medical devices. The tax imposed under this provision will not apply to sales during the period beginning on January 1, 2016, and ending on December 31, 2017. This applies to sales after December 31, 2015.

Health Insurance Industry Tax

The tax bill places a one-year moratorium on the so-called HIT tax (Health Insurance Industry Tax). If passed, the industry tax will not apply for calendar year 2017, which should result in less of an increase to group health insurance premiums for 2017.

So who said Washington bipartisanship was over? There is hope going into the New Years.