Breaking: All Health Republic plans (Group and Individual) ending on 11/30. according to early reports the healthcare Co-Op Health Republic NY will be shutting down Nov 30, 2015. New York State Department of Financial Services (NYDFS), the New York State of Health Marketplace (NYSOH), and the Centers for Medicare and Medicaid Services (CMS) announced additional actions regarding Health Republic Insurance of New York (“Health Republic”) and a transition plan for Health Republic customers.

TIMELINE:

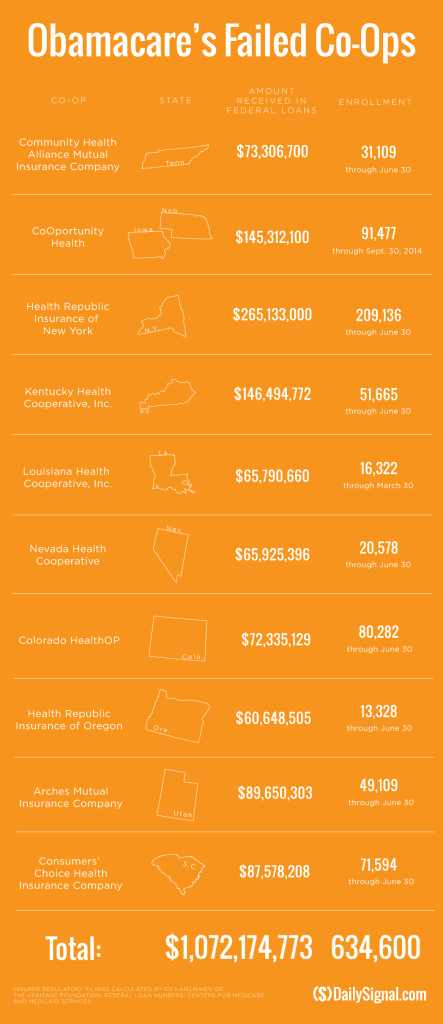

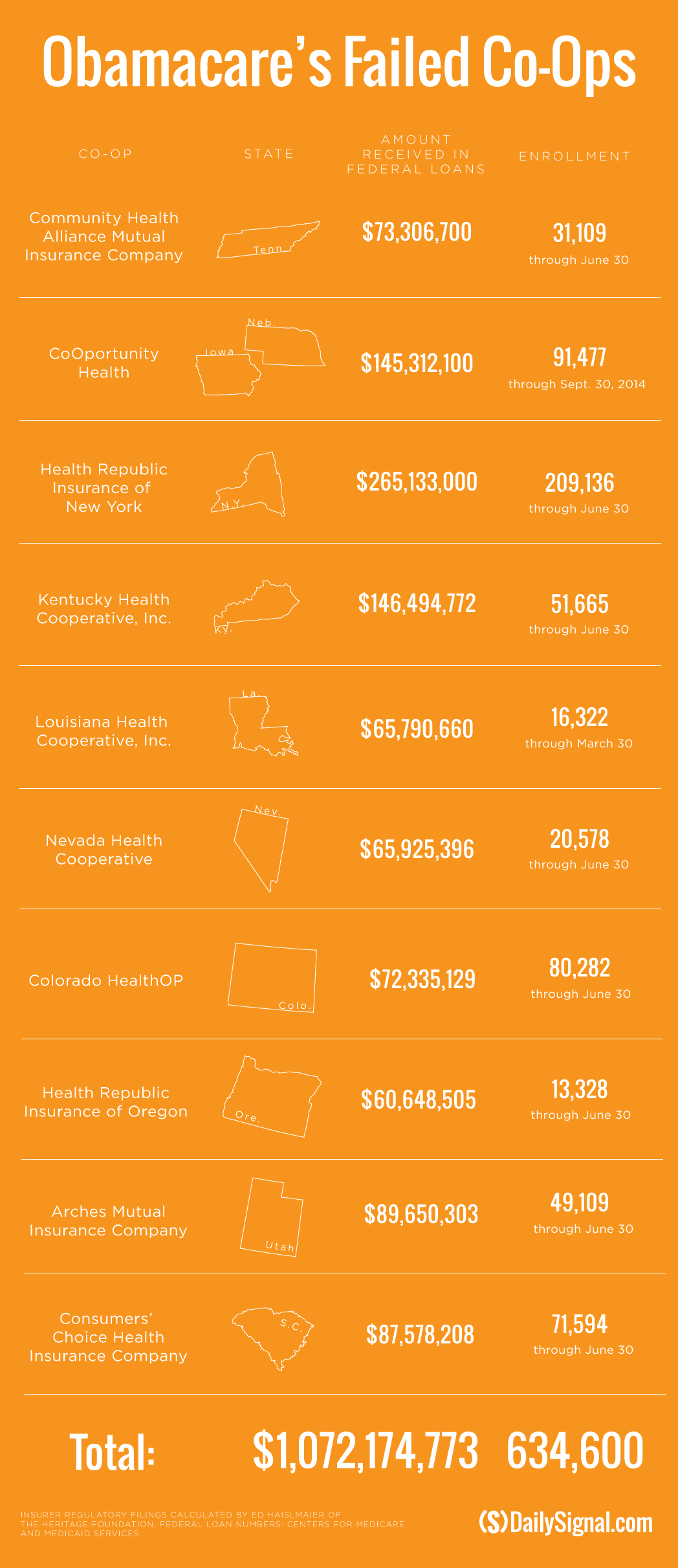

Oct 28th – Utah Healthcare Co-Op shutting down end of 2015. This sis the 5th Co-Op to shut down

June 2015 – With a spike in rate increase of 15-20% for 2016 to reflect unexpected high costs of new 200,000 membership the most affordable health plan was experiencing difficulties. The insurer reported $130 million in losses during its first 18 months of operations, according to financial filings, even as it enrolled more customers than any other insurer. DFS did allow for a 13 percent increase in the second year and a 14 percent increase heading into 2016. Both were lower than what Health Republic requested, though, and were not enough to save the struggling insurer.

May 2015- Health Republic was dealt its death blow when it became clear that the Affordable Care Act’s risk corridor program would not be fully funded, said one source familiar with the company’s finances. A report from Standard & Poor’s in May said the program had only 10 percent of the funds needed to make payments.

Summer 2013 -Health Republic had borrowed $265 million to begin operations.

New Insurance Risk Corridors paid for by a combination of both consumer insurance premium surcharge tax of 2-3% and Health Insurers is suppose to reclaim capital to those that are less profitable. Health Republic was owed approximately $147 million but was told by the Centers for Medicare and Medicaid Services to expect less than half that according to sources.

Regrettably, we all suffer when an Insurer exits the market. Furthermore, it will be a while again when Federal funds earmarked to start a low cost affordable health plans will materialize again. We are pulling for neighboring co-op Health Republic of NJ and hope this trend discontinues.

Our agency will be working closely with our clients to mitigate this exposure and transition smoothly for Dec 1, 2015. Individuals on the Marketplace can contact the New York State Department of Financial Services Consumer Hot Line with questions regarding Health Republic by calling 1-800-342-3736. The Hot Line hours are weekdays (Monday through Friday) from 8:00 a.m. to 8:00 p.m., and Saturday from 9:00 a.m. to 1:00 p.m.

Please Click here to read the full Press Release from NYDFS.

Stay posted, more news to follow. Our Agency as in the past will be out and early in front positioning our clients for best options. For more information on this or to schedule a call please contact us info@medicalsolutionscorp.com today.

Jeb Bush, running for the Republican presidential nomination, put out a detailed health proposal yesterday. The Bush campaign says the former Florida governor’s plan, in broad terms, would accomplish three goals: promote innovation, lower costs and return power to states.

Under Bush’s plan, individuals could get higher tax credits for purchasing health insurance and would be allowed higher contribution limits on health savings accounts for out-of-pocket expenses. He also would overhaul the regulations imposed by the Food and Drug Administration to help spur innovation in the healthcare industry and would put limits on malpractice lawsuits. And he would put caps on federal payments to states and create a “transition plan” for 17 million people “entangled” in Obama’s Affordable Care Act.

Bush also proposes to limit the tax-free status of employer-provided health insurance, an idea labor unions fiercely oppose.

Here are some key points to consider:

It would repeal and replace Obamacare.

Bush wants more people to have catastrophic coverage.

Bush would repeal the so-called Cadillac tax

Instead limit the Employer tax-free health benefits at $12,000 a year for an individual and $30,000 for a family.

The U.S. Supreme Court ruled this morning that the Affordable Care Act may provide nationwide tax subsidies for people who purchase health insurance through an exchange. The Court considered a challenge to a provision of the ACA concerning whether subsidies were available only to those who purchased health insurance on an exchange “established by the state.” The Court, in King v. Burwell, ruled 6 to 3 in favor of upholding the eligibility for people to receive subsidies through either a state or federal health insurance exchange.

The opposite ruling would have had serious implications for the country due to the number of states relying on a federally-run exchange (37 states) and the number of customers who qualify for subsidies based on their income (about 85% of customers nationwide). The Government’s argument prevailing: defending the subsidies, the Government argued that if you look at the entire ACA and its history, it is clear that the subsidies are available to everyone who purchases insurance on an exchange, no matter who created it.

Please join us for upcoming Webinar on How to Prepare for Current and Future ACA Requirements.

Are you able to identify and address all of the ACA requirements? Have you developed a plan of action to help stay in compliance? This webinar will walk you through a three year case study and provide you with current and future solutions to help your group prepare for ACA challenges including the Cadillac Tax.

Some of the key webinar highlights include:

Will Federal subsidies stop in some states making residents unable to access subsidized Exchange coverage?

3 year case study providing a practical view

Will IRS information reporting still be required?

Could Congress step in and propose changes to the existing ACA law?

2015 – Section 125 changes including eligibility, PRAs, excepted benefits and FSA plans for higher OOP exposure

2016 – Renewal focus on HSA’s with a dollar for dollar matching contribution

2017 – Further conversation of reducing benefit costs utilizing post deductible HRA’s and consideration of Defined Contributions

Practical information you can use – a webinar you will not want to miss!

The King Ruling awaits As Supreme Court schedules more decision days. The decision is expected to be possibly on Thursday on the legality of the Health care subsidies. ISSUE RECAP: At issue is whether subsidies that 8.7 million people receive to help pay for their insurance are available in all 50 states, or only those that set up their own health insurance exchanges. (more…)

Great news for families with HSA and high deductible plans. Individual out of pocket maximums will apply EVEN UNDER A FAMILY POLICY. New federal health care reform law regulatory guidance ends lingering uncertainty on how much in out-of-pocket costs employers with high-deductible plans can require employees to pick up.

The guidance, leaves intact the maximum out-of-pocket expenses employers can require employees to pay before health plan coverage kicks in: $6,850 for single coverage and $13,700 for family coverage when the rules go into effect in 2016.

An example illustrates how the HHS-imposed “EMBEDDED” limit on out-of-pocket expenses will work:

An employee and his or her spouse enroll in family coverage with an annual cost sharing limit of $13,000, and during the 2016 plan year, $10,000 of cost sharing payments are attributable to the spouse and $3,000 of cost sharing payments are attributable to the employee. Prior to the HHS’s clarification, the full $13,000 would be payable by the covered individuals because the $13,000 plan limit had not been reached on an aggregate basis. However, with the new EMBEDDED self-only limitation, the cost sharing payments attributable to the spouse must be capped at the self-only limit of $6,850, with the remaining $3,150 being covered 100% by the group health plan. The employee would still be subject to cost sharing, however, until the $13,000 plan limit is reached.

The biggest impact on the new cost-sharing rules will be on employers with high-deductible plans.

For the FAQs, visit: http://www.dol.gov/ebsa/pdf/faq-aca27.pdf

For more information and a free renewal evaluation please

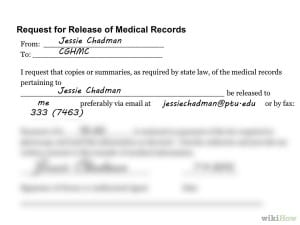

Anyone who has moved has been confronted with the question “How to Order Your Medical Records?”. Requesting your medical records may seem complex at first its simpler than one thinks.

1. Get a HIPAA release form. The federal law known as HIPAA entitles every person the right to access his or her medical records, receive copies of them, and request amendments to them.

2, Select your records. I would make this at least one month no more than 2 months This will give the office plenty of time to get you the records together. Specify the effective date, medical providers name, address, your name, address, medical record number ( you can get this from the staff) any identification numbers; i.e., Social Security Number or insurance ID number.

3. Submit forms. Fill out an authorization form giving one medical provider permission to share your records with another.Mark on that form which types of records you want included. Pay any fees that result.

4. Wait. The turnaround time under HIPAA can be 30 days. Most facilities, however, do not require that much time—many can fulfill a request in five to 10 days. Individual state laws may also dictate how quickly a facility must fulfill a request.

5. Follow up. In an imperfect world things can go wrong. What to do?

If your doctor has moved, you should be able to find your records at the practice she left. If that practice was affiliated with a hospital, the records may be housed within the hospital’s records system.

If your old provider says the records have been sent, but your new doctor’s office hasn’t received them, ask that they be re-sent. Doublecheck to make sure the old provider has the right contact information for your new one. You may find getting someone from your new doctor’s office involved could help. Having a nurse advocate for you, for instance, could put you in a better position.

If you’ve tried everything and are getting nowhere, offer to pick up the records yourself (but be aware that this may cost you), ask to speak with a manager or your doctor directly, or, as a final resort, contact your state medical board to file a complaint. This step is rarely necessary, but even suggesting you’ll have to go this route could get things moving on your request.

The Value of Requesting Your Records

There are many good reasons to request a copy of your medical records. Physicians don’t always share complete patient information or exchange a patient’s health records, so if a patient is seeing a new provider it is beneficial to ensure a copy of their record is sent to the new physician.. Also, it is beneficial for patients or caregivers dealing with multiple doctors and facilities to have all medical records in one place, which can then be used by providers to ensure thorough care.

Reviewing your record is an important way to ensure your provider has complete, correct, and up-to-date information, such as your known allergies. If you find information in your record that is incorrect or that you disagree with, contact the provider’s Health Info Management department.

Finally, it can be good for your health to keep a copy of your medical records, . Keeping an up-to-date copy of your health information will prevent redundant care, like repeat tests, and give all your physicians essential information about your health.