Medicare Part D Employer Notice

Empire recently announced their re-entry back into the New York small group market for 2017. A legendary broad networked PPO is welcome news especially in the NY small group market of 1-100 employees. Recently, the broad national networks have diminished to only 2 national health insurers, Aetna and Oxford. As a result of Empire Blue Cross participation in the BlueCard PPO program members enjoy unparalleled national access network to 96% of hospitals and 93% of doctors across the country. This national program will be on 18 of 28 plans below.

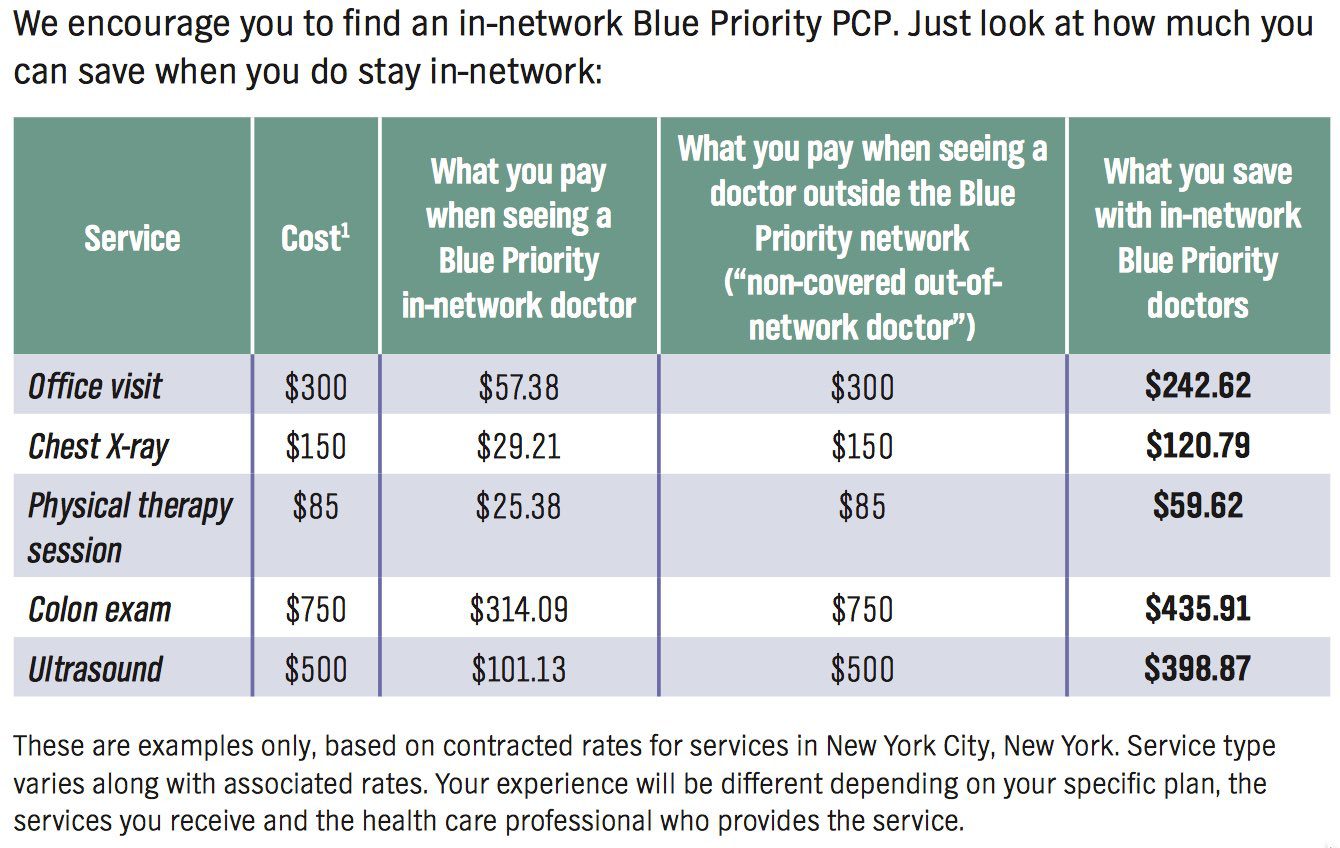

PPO Network Savings

DOCTOR SEARCH: Click Here

BENEFITS SUMMARY: OXFORD Platinum, Gold, Silver AND Bronze

Small Group Rates: 1st Quarter 2017

Drug Formulary: Click Here

Blue Priority FAQ: Click Here

Pathway FAQ: Click Here

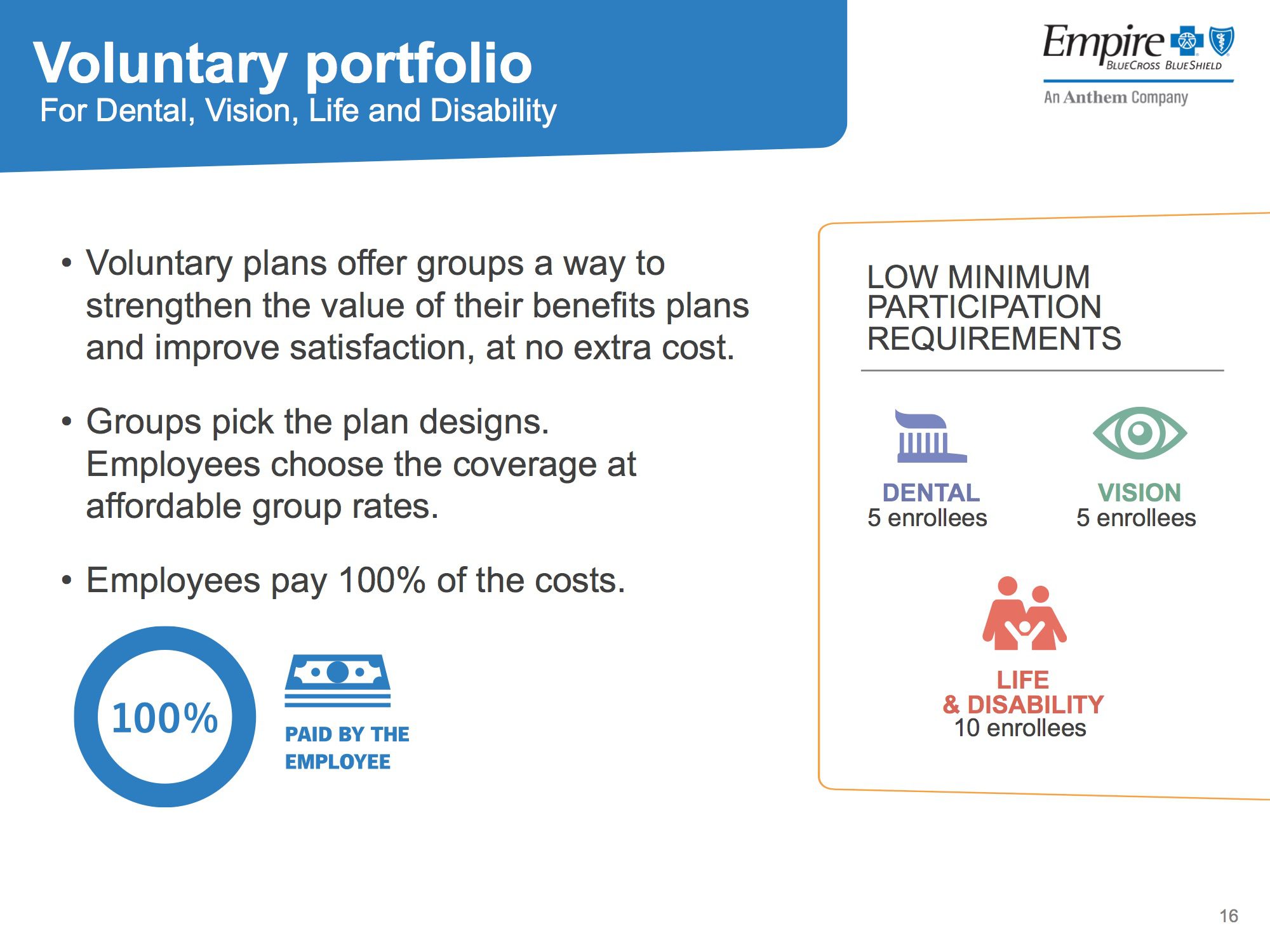

Ask us about Empire’s flexible low participation voluntary group dental, vision, disability and life insurance plans. Stay proactive and contact us today for a customized consult on how your organization can prepare ahead for ACA, Benefits, Payroll and HR @ (855) 667-4621 or info@medicalsolutionscorp.com.

CLINTON VS TRUMP ON HEALTH CARE

Clinton vs Trump Healthcare. A helpful overview from SHRM on the differences between the Candidates. They presumably agree on repealing the Cadillac Tax and well-needed price transparencies.

Source: https://www.hillaryclinton.com/issues/health-care/

Source: https://www.donaldjtrump.com/positions/healthcare-reform

Add our blog & sign up for newsletter on latest in Healthcare Reform News. Please contact us for a free evaluation on your group’s benefits at 855-667-4621.

Oxford Health Plans (NY), Inc. (OHP) License Withdrawal, Effective January 1, 2017, Upon Renewal

Please note the following:

The Oxford Metro NetworkSM is a new network option available to businesses based in New York. The Oxford Metro

Network was developed specifically for the needs of New York employers and is made up of physicians and other health

care professionals in New York and New Jersey.

The Oxford Metro Network consists of over 30,000 physicians and 84 hospitals1 throughout the Oxford New York

service area.2 Members enrolled in an Oxford Metro Network plan will also have access to over 18,000 physicians

and 62 hospitals1 in New Jersey.

Yes, the Oxford Metro Network plan designs are available to both small and large group employers.

There are eight gated, in-network only plan designs. The same plan designs are available for large and small groups.

4. What license are Oxford Metro Network plans on?

Oxford Metro Network plans are written on the Oxford Health Insurance, Inc. (OHI) license.

5. Can we offer this product alongside other Oxford products?

Yes, you can offer Liberty and Freedom Network plan designs, which include plan designs that offer out-of-network

benefits, alongside Oxford Metro Network plan designs. To make it easier to offer these plans, we have updated our

Idea Management SystemSM (IDEA) tool. You can use it to enroll in up to three OHI plans.

If you wish to enroll in more than three plan designs, you must submit a completed paper application with the

required documents. Please refer to our New York Small Group Underwriting Guidelines for required documentation.

A complete copy of our New York Small Group Underwriting Guidelines may be found by logging in to the Employer

portal of oxfordhealth.com. From there, click on “Tools & Resources” and then “Forms” in the drop-down menu of

“Your Benefit Coverage” under the “Practical Resources” menu.

Enrollment is required in each plan design that is offered.

6. Do my employees have to live in New York to enroll in a product offered with the Oxford Metro Network?

No, employees do not have to live in New York to enroll in a product offered with the Oxford Metro Network as long

as they work for a New York-based company and live in New York or New Jersey.

7. Is there coverage outside of the service area?

No, these plan designs offer access to Oxford Metro Network providers in the service area only. Members will not

have access to the UnitedHealthcare Choice Plus Network or to the Freedom and Liberty Networks in New York,

New Jersey or Connecticut. Emergency care is always covered, in or out of the Oxford Metro Network service area.

8. How does the non-embedded family deductible benefit work?

All Oxford Metro Network plan designs will include a non-embedded family deductible. When a member enrolls

in family, couple or parent/child coverage, the entire family has one deductible that must be met before the full

insurance benefits begin. The deductible can be met by one family member or by a combination of family members.

Once the family deductible is met, all family members will be considered as having satisfied their deductible for the

remainder of the benefit year.

9. Do Oxford Metro Network plan designs require referrals?

Yes, all plan designs offered with the Oxford Metro Network require referrals. Upon enrolling in an Oxford Metro Network

plan design, members will need to select a participating primary care physician (PCP) to coordinate their care.

10. Are specialty products like dental and vision available with the Oxford Metro Network?

Yes, pre-packaged specialty benefit options through Oxford Benefit Management (OBM) or stand-alone dental, vision

and disability products may be purchased with Oxford Metro Network plan designs. For ease of administration,

when a group has Oxford medical benefits, we do not require tax documentation or a binder check when they

add specialty lines of coverage. Only two enrolled subscribers are needed for voluntary dental, and one enrolled

subscriber for voluntary vision.

11. How can my employees find a participating Oxford Metro Network provider?

There are several ways that employees can search for a participating Oxford Metro Network physician.

If they already have a username and password for oxfordhealth.com:

1. Log in to the Member portal of oxfordhealth.com.

2. Click on “Find a Physician or Facility” on the home page.

3. On the next page, click the “Network” drop-down menu and choose “Metro.”

4. Enter additional criteria and click “Search.”

If they do not have a username and password, or want to search without logging in:

1. Go to oxfordhealth.com and click on “Members.”

2. Click on the “New Metro Plan – Important information for members” link.

3. On the next page, click the “Provider Search” link.

4. On the “Find a Physician” page, click the “Network” drop-down menu and choose “Metro.”

5. Enter additional criteria and click “Search.”

OR:

1. Go to oxfordhealth.com and click the “Browse our Provider/Facility Resources: Search for an Oxford doctor,

hospital or lab” link at the bottom of the home page.

2. Under “It’s in the details” on the right-hand side, click on “Doctor Search.”

3. On the next page (“Find a Physician”), click the “Network” drop-down menu and choose “Metro.”

4. Enter additional criteria and click “Search.”

Employees may also call the toll-free phone number on the back of their health plan ID card (if they are currently

enrolled in an Oxford plan) or 1-800-444-6222 to have a paper copy of the directory mailed to them. TTY users can

dial 711. Si usted necesita ayuda en español llame al número de teléfono en su tarjeta de identificación, 若需中文協

助, 請致電1-800-303-6719, 한국어로 도움이 필요하시면1-888-201-4746, or the phone number on their ID card

for help in English and other languages.

12. What pharmacies are available with the Oxford Metro Network?

The Oxford Metro Network provides access to retail pharmacies including major chains, mass merchants and

supermarkets. Among others, members can fill prescriptions at Duane Reade, Walgreens and Walmart.

13. How can my employees find a participating pharmacy?

Employees can search for a participating pharmacy from the Member portal on oxfordhealth.com by following the

steps below:

1. Go to oxfordhealth.com and click on “Members.”

2. Click on the “New Metro Plan – Important information for members” link.

3. On the next page, click the “Pharmacy Search” link.

4. Enter search criteria on the following “Find a Pharmacy” page and click “Search.”

Employees may also call the toll-free phone number on the back of their health plan ID card (if they are currently

enrolled in an Oxford plan) or 1-800-444-6222 to find out if a pharmacy is participating. TTY users can dial 711. Si

usted necesita ayuda en español llame al número de teléfono en su tarjeta de identificación, 若需中文協助, 請致

電1-800-303-6719, 한국어로 도움이 필요하시면1-888-201-4746, or the phone number on their ID card for help in

English and other languages.

14. What other resources and tools are available to members enrolled in an Oxford Metro Network plan?

• Oxfordhealth.com offers a convenient, secure way for members to search for doctors, check referrals, get a new

ID card, and access benefits.

• Online health and wellness tools such as Rally™, which is an interactive health and wellness enhancement to

oxfordhealth.com. With Rally, members receive personal lifestyle plans that focus on goals, competition, tracking

progress and healthy living. Rally offers a personalized interactive experience with step-based Challenges,

discussion Communities, individual action plans called Missions, health information and more.

• Oxford On-Call® nurses are available 24 hours a day, seven days a week by phone to give members helpful

information about illness or injury.

• Access to a fully-credentialed network dedicated to complementary and alternative medicine that includes more

than 5,900 providers.3

According to a released study by United Hospital Fund May 2016 report Insurance companies operating on New York’s individual exchange market lost $100 million in 2014.

With recent news of Insurers reporting mounting losses (UnitedHealthcare will drop ACA exchanges) on the Individual Marketplace it wouldn’t be surprising for the next year’s Study to show even greater losses in 2015. As reported last month, the average NYS 2017 Rate Requests for individual marketplace was 17.3%.

Lower premiums, reinsurance and subsidies made coverage more affordable. “For many years in New York, annual individual premium increases far outpaced the offsetting effects of both a $38 million state-funded reinsurance program,12 and a risk-adjustment mechanism that provided a cross-subsidy from the small group market to the individual market, valued at $62 million in 2009.13 In 2014, new enrollment, PHSP participation, more competitive pricing, a better risk pool, and a federal reinsurance program resulted in an average individual monthly premium of $430.97 in New York.” The ACA subsidies reduced premiums by an average of $215/month

“More affordable premiums have been a key factor in the growth of the individual market. The loss of federal reinsurance payments will create an upward pressure on rates, and the absence of federal risk corridor reimbursement will also continue to reverberate.” Consumers with Obamacare subsidies will be shielded from most of the premium increases that may occur, but off-Exchange enrollees and NYSOH customers without subsidies could face significant monthly increases.

Read the UHF report here:

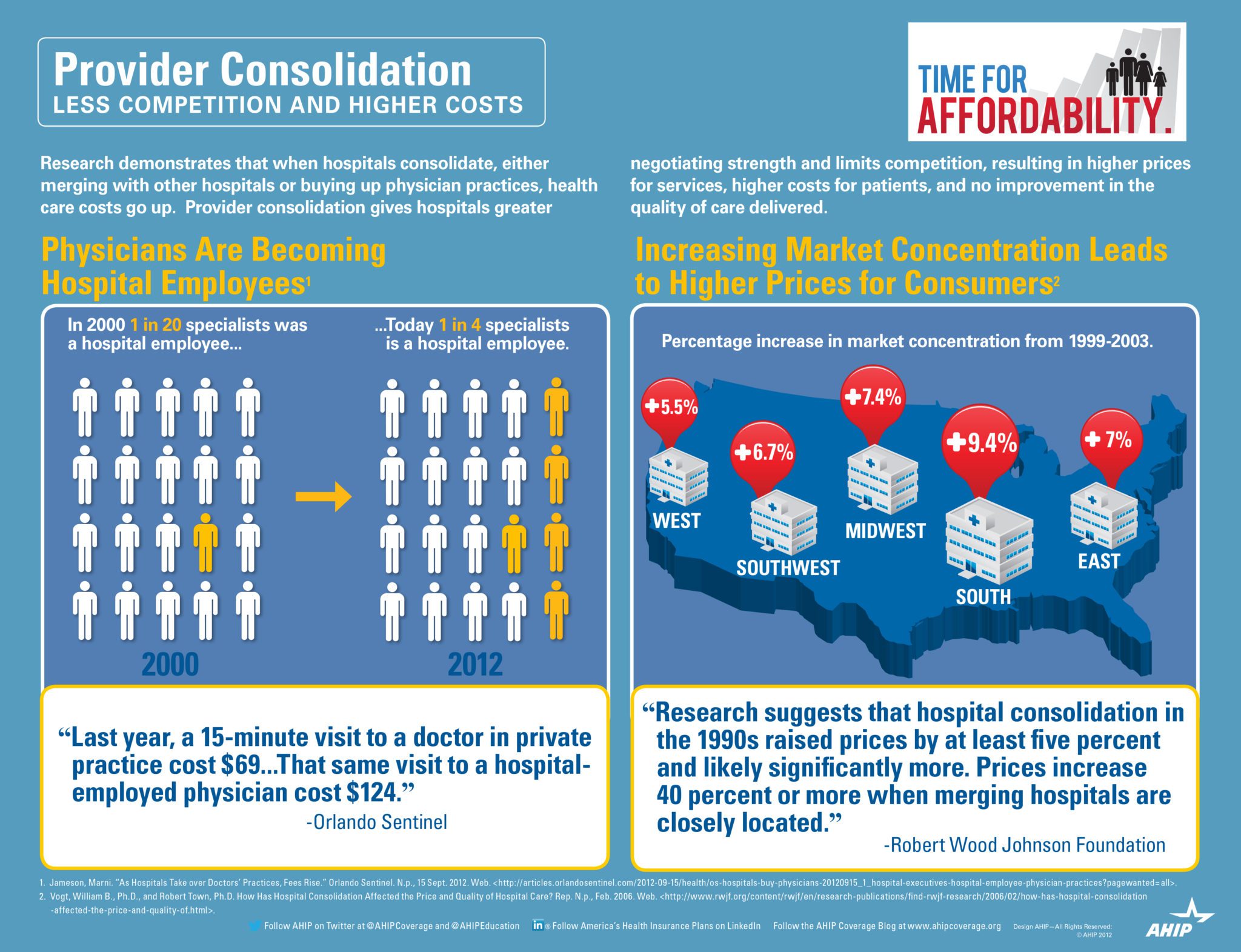

Insurance mergers aka Mergersurance Mania continues at a steady pace with April 2016 Florida’s approval of Anthem Blue Cross and CIGNA merger. This is one month after Florida approved the Aetna and Humana merger. Investors have given their blessings to be sure while 10 States have also given approval. The Anthem Cigna $54 billion merger leaves only three national major providers of health care. Worries remain about the potential effect on consumers and the rising cost of health care.

Health Insurers consolidation argument are that they need to be able to merge in order to absorb added costs and blunted profit margins under the Affordable Care Act. Additionally, medical groups and hospitals groups have merged themselves rapidly giving them negotiation cost controls. This has traditionally been trending in smaller regional markets but are now also felt in major US Cities.

Evidence indeed is pointing to expected large insurance increases due to overwhelming market domination by hospitals. While Doctors and AMA are rightfully concerned about Insurer mergers the vast majority are now working for a Hospital System or Medical IPA.

Without public outcry there seems to be lax Regulator oversight and the arms race should not come as a surprise. On the local level we have yet to see a recent example of hospital merger that was curtailed.

This goes well beyond political partisanship. In a tight Presidential race it is important to understand that whether or not one supports a Single Payer we all suffer. This is bad for consumers, providers and tax payer all around. In an Oligopoly health care system with lack of competition the U.S. tax payers are also stuck with inflated costs.

.

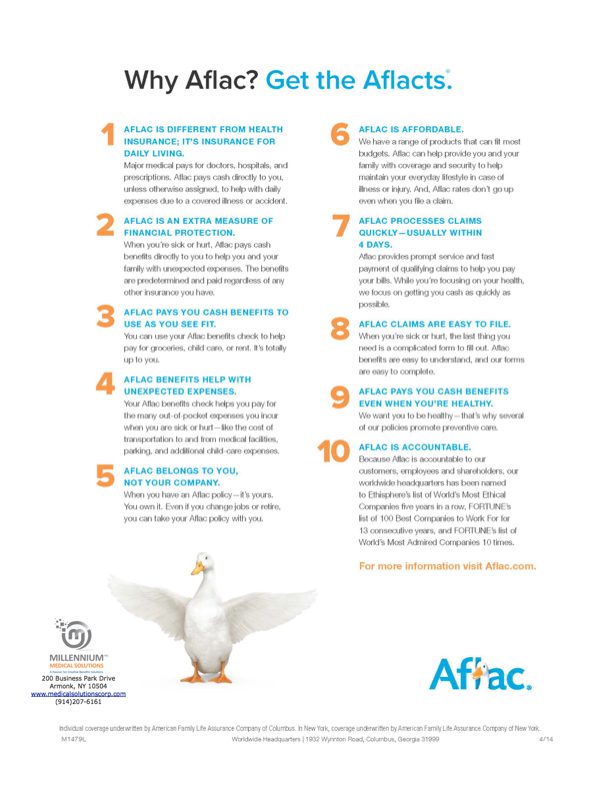

The AFLAC duck has become synonymous with Voluntary Supplememntal and Critical Illness benefits, see Consider Supplements to Primary Medical Plans. Aflac answers the question to “how do I plug in the gaps of eroding medical benefits for employees”. With office copays as high as $60, average hospitalization exposure of $2000, in-network $1000 deductibles for diagnostics and $100 ER copays this is becoming a valid concern.

Payment, not reimbursement: the insured does not have to spend money up front, in terms of a deductible, in order to get the benefit. Having an accident or being diagnosed with a specific illness, such as cancer, triggers the payout. The employee doesn’t have to incur an expense and then wait for reimbursement. This is important because employees may be facing high deductibles in their medical plan coverage, so having the ready cash is a major help.

Not tied to medical plan: A common point of confusion with both accident and critical illness products is that their benefits are somehow “offset” by medical plan benefits. It’s important that the employee and the employer alike understand that these limited benefit policies perform as supplements to medical coverage, but are not in any way linked to them and their benefits are delivered with no offsets or reductions once policy requirements are met.

Use money in any way: The nature of medical plans is that insureds only get reimbursed for “qualified expenses,” which the insurer details within the program. With both accident and critical illness, since insureds receive a lump sum for particular injuries or diseases, they have no such restrictions on how they use the money. For example, a person who loses the use of a limb might use the accident policy’s payout to make home modifications that make life easier. Someone with a cancer diagnosis might wish to consult with a specialist across the country, and can use the critical illness policy’s payout for travel and lodging expenses. If an experimental treatment is not covered by a medical plan, the insured can use the critical illness policy’s payout to spend the $10,000 or more to pay for the treatment.

Direct and transparent: For most people, a glance at the list of potential injuries on an accident policy, or taking on the topic of dread diseases, can generate queasiness. Who really wants to think about winding up in a coma or fighting cancer? But the policy benefits are clear and transparent, unlike the sometimes-mystifying coverage rules in medical policies. Employees will get the message that, by offering these voluntary benefits, the employer is raising important financial-security issues and providing affordable solutions to address them.

Simplified claims: In most cases, to receive a benefit the insured simply provides the insurer with a claim form and applicable paperwork from a care provider that documents the injury or diagnosis of disease. With accident insurance, additional paperwork might be required to determine whether the claim stems from the insured taking part in certain inherently dangerous activities, such as bungee jumping or car racing, in which case benefits might be denied. Such restrictions will be clearly stated in the policy.

Ready availability: Generally, accident insurance payments are issued to employees without any pre-existing condition limitations. Critical illness insurance might require the employee to fill out questions on an application for coverage, although under certain conditions, employees may be eligible for a guaranteed issue offer without requiring answers to health questions. Regardless, employees would have a hard time finding either of these coverage options at such affordable prices outside of the group voluntary benefits context. Premiums of only $20 or $30 a month for each insured are common in these worksite products.

Family coverage: Depending on the carrier, the employee can opt to get coverage for a spouse and dependent children (up to a certain age) as well. This is a real advantage if a working spouse does not have coverage through his or her employer. But, this is equally important for spouses who work in the home, because household finances might be more constrained and thus make the additional policy benefits even more critical. In the case of children, the accident coverage usually pays benefits for non-professional sports injuries, a common occurrence. Depending on the injury, the out-of-pocket costs for emergency room services, copays and deductibles for medical care and follow-up physical therapy can quickly exceed $1,000. An accident policy typically would provide benefits to cover the lion’s share of those costs.

Portability: In most cases, accident insurance allows employees and dependents to continue the coverage after leaving the employer or retiring. For critical illness, there may be certain conditions involved, but the key is that most policies allow employees and dependents to continue enjoying these coverage options at group rates wherever life might lead them next.

The article below summarizes in full the Aftermath of Health Republic Shut Down. The original NYS announcement to shut down Nov 30th was released on Friday October 30th. There are countless anecdotal evidence of our client’s Providers not getting paid for work already done this Fall. Brokers , our Agency included, has NOT been paid since this Summer.

Should My Doctor and Broker be paid? That really ought to be the header for this article. At the same time Health Providers and Brokers honored clients despite the Health Republic’s precarious financial status. The approximate amount owed is $150 Million. If the State truly wants to correct this they have a $1Billion surplus. How can the State obligate Providers and Brokers to meet contractual licensing & professional standards and ignore them now?

As reported in Mahopac NY News 12/9/15 by BRETT FREEMAN

HUDSON VALLEY, N.Y. – When Health Republic Insurance of New York announced early last month that they were ceasing operations at the end of November, individual subscribers and small groups had to scramble for other options to keep themselves and their employees insured.

Doctors and individual insurance brokers weren’t so lucky.

Often overlooked in news reports is how Health Republic’s demise affected thousands of medical providers and individual insurance brokers, who may never see a dime from all that is owed to them.

Health Republic was a not-for-profit health insurance co-op (Consumer Operated and Oriented Plan) established under the Affordable Care Act. According to its website, at its height, it had over 215,000 members, making it the largest new health insurance cooperative in the country.

According to articles linked on Health Republic’s website, it borrowed a $265 million low-interest federal loan to begin its operations and was one of 23 co-ops receiving a total of $2.4 billion. According to reports, about half of them have since failed, with many analyses pointing to the low premiums as the cause of their collapse.

Dr. Scott D. Hayworth, president and CEO of the Mount Kisco Medical Group (MKMG), estimates that his practice, which provides medical care to 500,000 patients in the Hudson Valley (including thousands of patients in Mahopac, Somers, Yorktown and North Salem), has lost millions of dollars due to the collapse of Health Republic.

“It’s more than just the doctors’ fees,” said Hayworth, who oversees 450 physicians in dozens of locations throughout the Hudson Valley. Dr. Hayworth said that insurance reimbursements cover vaccines, chemotherapy and other ambulatory and pharmaceutical products that were paid for out of pocket by MKMG.

Despite its losses, MKMG continued to honor its contract with the insurance carrier to ensure any patients covered by Health Republic would continue to receive medical care.

“The thing we all have to remember is there is a patient in the middle of this,” Hayworth said. “Our first obligation is to our patients.”

Other health care providers, including local hospitals, have been in the same boat as MKMG.

Putnam Hospital Center is owed $1.8 million, according to Marcela Rojas, the manager of public and community affairs. Health Quest, which is the parent company of Putnam Hospital Center, is owed $4.4 million in total and doctors throughout its three hospitals are owed $350,000.

“In meetings with state officials, a discussion has focused on how to recoup any of these payments owed to individual patients as well as hospitals, physicians and other providers,” Rojas said in an email interview this past Friday. “There is a discussion on restructuring Health Republic, but the question is, what assets, if any, remain? Recouping any funds may be both a federal and state matter. There is currently no guarantee, emergency or recovery fund in Washington or Albany to cover those losses. Hospitals are meeting with state legislators this week to discuss how best to proceed to recoup at least some of the money owed.”

Officials at Northern Westchester Hospital estimate that they will be owed $2 million due to nonpayment of services provided to Health Republic patients.

“We believe NWH will recover some unknown portion of that amount,” said Joel Seligman, president and CEO of Northern Westchester Hospital. “Under New York State law, NWH must continue to provide services to patients for 60 days where continuity and transitions of care are an issue. Northern Westchester Hospital has a robust financial assistance policy applicable to all patients, including former Health Republic patients.”

All of these healthcare providers are receiving guidance and advocacy from the Healthcare Association of New York State (HANYS), a non-profit statewide association representing hospitals, health systems, nursing homes, home care agencies and other providers across the state.

In an interview, Melissa Mansfield, associate director of public and media relations for HANYS, explained that other states have something called a guarantee fund, which operates as an insurance company for the insurance company.

“New York is one of the few that does not have one yet,” she said, adding that medical providers statewide are owed $160 million, not including what will be owed for care rendered during the month of November.

“HANYS is aggressively advocating on behalf of our members with Cuomo administration officials and CMS (Centers for Medicare & Medicaid Services) to secure payment for money owed by Health Republic,” Mansfield said. “HANYS is exploring all available options for immediate payment and pursuing the establishment of a guarantee fund as a way to protect providers for Health Republic claims and from future insolvencies. Our members are obviously concerned about the impact Health Republic’s shutdown has had on patients and are committed to providing care during this transition. However, HANYS continues to raise very serious concerns about the consequences of such a tremendous financial loss when hospitals are already financially fragile.”

In Putnam County, there were 4,241 Health Republic enrollees, according to HANYS. In Westchester County, there were 20,404 enrollees, making it the third-most impacted county in the state, behind Nassau and Suffolk counties.

In a recent interview, state Sen. Terrence Murphy, who represents Mahopac, Somers, Yorktown and North Salem, among other communities, expressed outrage at the collapse of Health Republic, calling it, “at a minimum, gross mismanagement and negligence. Where the hell was DFS?” Murphy asked, referring to the Department of Financial Services, the state agency that oversees various industries that operate in the state, including all insurance companies. Murphy said DFS should be investigated.

On Sept. 25, DFS directed Health Republic to cease writing new health insurance policies and announced that the co-op would commence an orderly wind down after the expiration of its existing policies. Weeks later, after a review of Health Republic’s finances, finding it in worse financial condition than the company previously reported in its filings, DFS and New York State of Health, which is the official agency administering the Affordable Care Act, ordered Health Republic to end all of its policies on Nov. 30.

A spokesman for DFS did not return a phone call seeking comment, but on its website, officials with DFS said they opened an official investigation last week on Health Republic’s inaccurate financial reporting.

“NYDFS investigators are collecting and reviewing evidence relating to Health Republic’s substantial underreporting to NYDFS of its financial obligations,” according to the statement. “Among other issues, the investigation will examine the causes of the inaccurate representations to NYDFS regarding the company’s financial condition.”

According to DFS, medical providers who contracted with Health Republic had been legally bound to provide healthcare through the expiration of a patient’s plan with Health Republic, regardless of their concerns about reimbursement.

“NYDFS is taking actions that will apply a New York State law that prohibits providers from collecting or attempting to collect from Health Republic consumers amounts that are owed by Health Republic,” a statement on the website said. In addition, according to the DFS website, doctors must honor all new insurance policies of patients who are in an ongoing course of treatment with a provider for a life-threatening or a degenerative and disabling condition or disease, or in the second or third trimester of pregnancy for up to 60 days or through the pregnancy.

All of this is good for the patients, but Murphy expressed worry about how some local doctors might fare with all the lost reimbursements.

“You have practices that might go belly up,” said Murphy, who is a chiropractor in addition to being a legislator. “This is going to be a disaster…You will see some of them go out of business.”

While Dr. Hayworth at MKMG expressed confidence that his medical group would continue to offer top-notch care for its patients, he said that healthcare is a narrow-margin business and lost reimbursements will affect his group’s ability to recruit the best and brightest physicians, who he fears might be lured to other states.

Hayworth, who is married to former Congresswoman Nan Hayworth, declined to comment on the politics of the Affordable Care Act, but he said there definitely needs to be insurance reform. He also called on Albany and Washington, D.C. to provide “legislative relief” to the medical providers impacted by Health Republic’s collapse.

Sen. Murphy, who is chairman of the Administrative Regulations Review Commission, said he respects the legislative process, which calls for other committees to work on the problem, but has shared his concerns with state Sen. Kemp Hannon, chair of the Health Committee, who has started up round table discussions to determine the next steps.

“Anything to make sure this never happens again,” Murphy said.

Assemblyman David Buchwald, who represents North Salem, is also working on the problem.

“I have heard from constituents who are doctors and are concerned that they will not be paid for the services they provided to Health Republic patients,” Buchwald said in statement. “I have worked to raise this issue in Albany while the legislature is not in session. Understandably, the most immediate concern is ensuring that people who had Health Republic insurance are transitioned as smoothly as possible to new insurance. This is important to both patients and doctors, so that at least people are insured and health providers get paid going forward. Next, New York will hopefully see to it that insurance companies have adequate financial resources and address the needs of health professionals who have been left holding the bag. I expect that work to begin as soon as Health Republic customers are transitioned to their new insurance.”

Assemblyman Steve Katz, who represents Mahopac, Somers and Yorktown, did not return a call seeking comment. Nor did Congressman Sean Patrick Maloney, who represents Mahopac, Somers and North Salem in the U.S. House of Representatives, and Congresswoman Nita Lowey, who represents Yorktown.

In addition to the health care providers, local brokers are also out of luck. Mahopac resident Robert Simone, a broker with INS Brokers Inc., said he is owed thousands of dollars from Health Republic for his September and October commissions.

In an attempt to recoup his commissions, he called Health Republic, which told him to call DFS.

“DFS said, ‘We have nothing to do with it. Health Republic is holding your money.” Simone said he is not optimistic.

Nor is Chris Radding, one of the owners of the Forbes Agency in Katonah. Radding said he had 22 employer groups who had been members of Health Republic and he had lost thousands of dollars in commissions when Health Republic folded.

“Anything I’ve seen, there is no mention of the broker,” Radding said. Both Radding and Simone emphasized that their priority was ensuring that their clients had health coverage.

“The whole thing is pretty frustrating and really kind of disgusting,” Radding said.

In a press release issued Monday, the New York State Association of Health Underwriters estimated that insurance brokers in New York State will have lost millions of dollars due to unpaid commissions.

“What’s needed is a solution that avoids the usual outcomes of a failed insurance carrier,” the release said. It listed the usual outcome as reduced payments or no payments to those who provided their professional services even after the carrier ceased reimbursement for those services. It also said the solution should not inflate future insurance premiums or increase New York residents’ tax burden.

“We think that we have such a solution,” the release said. “NYS recently announced the existence of a $1 billion surplus, $680 million of which was generated by penalties levied by DFS. New York State should use some of that surplus to pay everyone what they are owed—doctors, hospitals and insurance brokers—and NYS should also ensure that Health Republic enrollees who have selected a licensed insurance advisor will continue to benefit from their advice by directing succeeding carriers to automatically appoint those brokers when their clients accept an auto-enrollment offer.”

|

| |||||||||||||||||||||||||||||||

NEW 2016 Oxford Metro Network NY

NEW 2016 Oxford Metro Network NY