At 10 AM today the Supreme Court in a 5-4 decision upheld the Patient Protection and Affordable Health Care Act’s individual mandate as constitutional.

Imposition of a tax “leaves an individual with a lawful choice to do or not do a certain act, so long as he is willing to pay a tax levied on that choice,” Roberts says. “The Affordable Care Act’s requirement that certain individuals pay a financial penalty for not obtaining health insurance may reasonably be characterized as a tax. Because the Constitution permits such a tax, it is not our role to forbid it, or to pass upon its wisdom or fairness.”

According to Footnote 11, which is on page 44 of the slip opinion: Those subject to the individual mandate may lawfully forgo health insurance and pay higher taxes, or buy health insurance and pay lower taxes. The only thing that they may not lawfully do is buy health insurance and not pay the resulting tax.With this decision finalized, New York State (and the rest of the country) can now move forward with implementing the law. We embrace the much-needed clarity and looking forward to working with our clients moving ahead.Millennium Medical Solutions Corp will be planning health care seminars to review the decision and overview to help understand the impact on employers, plan benefits, and providers. We welcome your suggestions on specific topics or questions you want us to focus on. Please join us!

Our office will continue to monitor events and inform our members of any other important news.

2021 Open Enrollment Checklist To download this entire document as a PDF, click here: Open Enrollment eBook This Compliance Overview is not intended to be exhaustive nor should any discussion or opinions be construed as legal advice. Readers should contact legal...

In preparation of 2020 open enrollment, Employers should review their plan documents to confirm that they include these required changes. Learn how our Agency is helping businesses thrive in today’s economy. Please contact us at info@medicalsolutionscorp.com or (855)667-4621.

The 2017 Election Results and ACA is a hot topic creating buzz. With the outcome of the 2016 elections now official, the Republicans will hold the majority in both chambers of Congress and control of the White House beginning in 2017. Our posting CLINTON VS TRUMP ON HEALTHCARE was a general summary of their differences on Healthcare.

Since President-elect Trump ran on a platform of “Replace and Repeal” of the Affordable Care Act (ACA), we anticipate that acting on this campaign promise will be one of the top priorities of the new Trump administration. We anticipate there will be significant disruption for individuals, employers, brokers and carriers across the country.

Republicans will likely need to use the process of Budget Reconciliation to pass legislation through the Senate, given the party did not secure enough seats to control a filibuster-proof supermajority. In other words, the legislation can pass in the Senate with a simple majority vote and not a super majority (which requires 60 votes). Reconciliation can be used to take away some, but not all, of the ACA. It is anticipated that certain provisions of the ACA would be targeted such as Medicaid expansion, the availability of subsidies and premium tax credits in the Marketplace, and the employer and individual mandate. It cannot be used to remove non-budgetary provisions (for example, insurance mandates like “to age 26”). In addition, it is conceivable that a Trump administration may simply direct various federal agencies (such as the Department of Labor) to not enforce certain ACA provisions.

The Republicans have not laid out a specific plan on what will replace the ACA. Generally, the party has supported the existing employer-based system (with some party members calling for limits on the tax exclusion). Based on published white papers on the President-elect Trump’s website, other aspects of a healthcare overhaul plan may include:

Tax credits for purchasing individual health insurance;

Expansion of Health Savings Accounts and HighDeductible Health Plans;

Continuation of the prohibition on pre-existing condition exclusions from health insurance;

High risk pools;

Interstate sales of insurance; andMedical malpractice reform.

The process to repeal and replace the ACA will take time and nothing will happen between now and the New Year. Open enrollment is currently underway in the Marketplaces across the country and it is expected that individual policies (and subsidies for lower and middle-income individuals) will be available to enrollees as of January 1, 2017. What is unknown is whether the Trump administration and subsequent legislation will affect the Marketplace and subsidies in mid-2017 or instead phase out this coverage after the 2017 calendar year.

The employer mandate (for applicable large employers);

Form 1094-C and 1095-C reporting for CalendarYear 2016;

Any ACA taxes and fees for self-funded plans to pay directly (such as reinsurance fees); and

Plan design changes applicable to plan years thatbegin on or after January 1, 2017.

In addition, all other federal law mandates impacting employer health and welfare plans such as ERISA,HIPAA, COBRA, Code Section 125, the Mental Health Parity and Addiction Equity Act, and the Service Contract Act / Davis Bacon and Related Acts are still good law. There has been no indication that these non-ACA laws are targeted for repeal or replacement.

Stay tuned for updates as more information gets released. Sign up for latest news updates. Please contact our team on your 2017 health plan renewal at Millennium Medical Solutions Corp (855)667-4621 for immediate answers.

Health and Human Services had released earlier this year the final version of its 2017 Notice of Benefit and Payment Parameters. Under the Affordable Care Act (ACA) this is issued annually. While the guidance is mostly relate dot the individual marketplace itt does, however, include several items relevant to employers and group health plans, specifically:

Annual limits for cost sharing (out-of-pocket limits)

Marketplace eligibility notifications to employers

Marketplace annual open enrollment period

Small Business Health Options (SHOP) Exchange

ANNUAL LIMITS FOR COST SHARING:

The annual out of pocket limits for plan years beginning on or after January 1, 2017 are $7,150 for individual coverage and $14,300 for family coverage. These cost sharing limits apply to in-network essential health benefits offered under non-grandfathered health plans, both fully and self-insured. Annual deductibles, in-network co-insurance and other types of in-network cost sharing accumulate toward the out-of-pocket limit, including prescription drug copayments. Not included are premium payments, out-of-network cost sharing and spending on non-essential health benefits.

MARKETPLACE ELIGIBILITY NOTIFICATIONS TO EMPLOYERS:

Beginning in 2017, the Marketplace will notify an employer as soon as possible when one of its employee’s first enrolls in subsidized Marketplace coverage. Since some employers may be liable for a penalty under the ACA’s employer mandate when an employee qualifies for a subsidized Marketplace coverage, this change to a more proactive notification process will hopefully provide employers with the opportunity to work with CMS in cases where an improper subsidy has been provided.

MARKETPLACE ANNUAL OPEN ENROLLMENT PERIOD:

Open Enrollment in the Health Insurance Marketplace, Healthcare.gov, for 2017 and 2018 will take place from November 1, 2016 through January 31, 2017 and November 1, 2017 through January 31, 2018, respectively.

SMALL BUSINESS HEALTH OPTIONS (SHOP) EXCHANGE:

Beginning in 2017, small employers electing coverage in the SHOP Exchange will have the option of “vertical choice,” offering plans across all metal levels (platinum, gold, silver and bronze) from one insurer. States who opt out of the vertical choice option will continue to offer employers the choice of selecting health plans that are available at one single metal level of coverage.

Stay proactive and contact us today for a custmozied consult on how your organization can prepare ahead for ACA, Benefits, Payroll and HR @ (855) 667-4621 or info@medicalsolutionscorp.com.

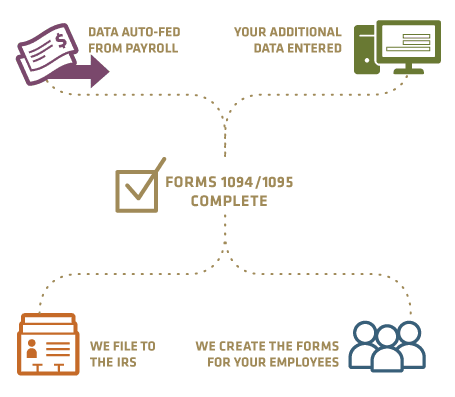

This list of FAQs has been compiled from common questions posed by clients regarding reporting obligations on Form 1095-C. For purposes of these FAQs:

An applicable large employer (ALE) means an employer who employed on average at least 50 full-time employees (including full-time equivalent employees) in the preceding calendar year.

An ACA FTE is an employee of the ALE who had on average at least 30 hours of service a week (or 130 hours of service a month) as determined under the applicable measurement method (i.e., monthly or look-back).

Minimum essential coverage (MEC) means employer-sponsored group health plan coverage unless otherwise noted. Minimum value (MV) means a plan that pays at least 60% of the total benefits.

Calendar year (CY) means January 1 – December 31 and generally refers to CY 2015, unless otherwise noted.

1. An ALE sponsors an insured group health plan. Coverage is offered to employees who work at least 20 hours per week. Who receives a Form 1095-C?

The ALE provides a Form 1095-C to any individual who is an ACA FTE for at least one month of the calendar year.

Each ACA FTE must receive a 1095-C that describes the offer (or no offer) of coverage made for each month of the calendar year. The ALE completes Parts I and II of the Form 1095-C (and not Part III). The health insurance carrier issues a Form 1095-B to the covered individual (including any family members) that provides information on MEC.

Individuals who are not ACA FTEs for any month of the CY (e.g., part-time employees who average 20 hours of service a week throughout the calendar year) do not receive a Form 1095-C. If the individuals are enrolled in MEC through the group health plan, the carrier will issue a 1095-B.

2. Does the answer in Q/A-1 change if the group health plan is self-insured?

Yes.

If the plan is self-insured, then:

a.The ALE provides any individual who is an ACA FTE for at least on month of the CY with a Form 1095-C and completes Parts I and II. This describes the offer (or no offer) of coverage made for each month of the CY.If the ACA FTE is covered under the ALE’s self-insured group health plan for at least one month of the CY, then the ALE completes Part III of Form 1095-C to reflect the months of coverage (including coverage of family members).

b.In addition, any individual who is the primary insured for one month of the calendar year will receive a Form 1095-C that reflects the coverage of the primary insured and family members. This may include:

Employees who are not ACA FTEs (e.g., a 20 hour/week part-time employee who takes the self-insured health plan coverage).

A COBRA qualified beneficiary who has COBRA through the self-insured plan and is a former employee of the ALE that was not employed during the applicable calendar year.

A retiree of the ALE who receives coverage through the self-insured health plan even though he was not employed by the ALE during the calendar year.

A divorced spouse who receives coverage through COBRA under the self-insured health plan even though he was never an employee of the ALE.

A child who receives coverage through COBRA under the self-insured health plan of the ALE due to aging out of the health plan even though she was never an employee of the ALE.

IRS Extends 1094 and 1095 Deadlines to March 31, 2016 and May 31, 2016 respectively.

Important to note:

No Form 1095-C is provided to individuals who are not ACA FTEs and do not have coverage for any month of the CY through the self-insured plan (e.g., a part-time employee who declined the ALE’s offer of coverage does not receive a Form 1095-C).

If the ACA FTE declines the offer of self-insured coverage, the ALE still must provide him with a Form 1095-C which reflects:

the offer of coverage (e.g., 1E in line 14);

the cost for self-only coverage in the lowest cost MV plan (line 15); and

any safe harbor code that applies (e.g., 2H for the rate of pay safe harbor).

3. How do you report for the individuals described in (b) of Q/A-2?

Non-ACA FTEs who have coverage through an ALE’s self-insured plan must receive information regarding the months of the CY for which they had MEC. The easiest way to report on these individuals is to use Form 1095-C because ALEs are already using this Form to report on all ACA FTEs. In the case of the individuals described in section (b):

Complete Part I.

In Part II, use Code 1G in line 14 and do not complete lines 15 or 16.

In Part III, list the primary insured and any covered family members (including SSN or DOB). Then check the boxes to reflect the months of the CY that the individual(s) has MEC through the self-insured plan.Alternatively, an ALE may use Form 1095-B to report MEC to covered individuals and then use Form 1094-B in the IRS submission process. This may create additional work as the “B” Forms are different from the “C” Forms that the ALE must complete. For consistency and administrative ease, many self-insured ALEs are meeting their reporting obligations through the “C” Forms.

4. An ALE uses the look-back measurement method to determine its ACA FTEs. The ALE hires summer seasonal employees each year and uses a 12-month Initial Measurement Period (IMP) to determine if these new hire seasonal employees are ACA FTEs. While they work 40 hours a week during the season, after 4 months employment terminates and these individuals are not hired back for another 8 months (if at all). These individuals are not eligible for health insurance. Is the ALE required to provide them with a Form 1095-C?

No.

A “limited non-assessment period” is a waiting period, including an IMP and initial administrative period (IAP). An ALE does not need to file a Form 1095-C for an individual who, for each month of the calendar year, is in a limited non-assessment waiting period. So in this specific example, no 1095-C is required with respect to these seasonal employees because they:

1. are in a limited non-assessment period (the IMP), and 2.are not covered by the ALE’s self-insured health plan for any month of the calendar year.

The result is the same if these individuals were new hire part-time employees and at the end of the IMP were identified as non-ACA FTEs and were not offered health insurance coverage.

Important to note:

1. If, at the end of the IMP (and IAP) the employee is identified as an ACA FTE, then reporting on Form 1095-C would be required for the entire calendar year that includes the end of the IMP

2.Use 1H (line 14) and 2D (line 16) for each month during the calendar year the individual was in a limited non- assessment period.

3.Once the IMP (and IAP) is over and the individual earns ACA FTE status in the CY, then use:

In line 14: 1A, 1E or 1H (offer of coverage codes); and

In line 16:

2C if the individual has coverage under the plan; or

the applicable safe harbor code if affordable coverage was offered and the employee declined(2F, 2G or 2H), or

if code 1H is used or the offer of coverage is unaffordable, leave line 16 blank.

See Q/A-13 for a similar example.

5. ALE has union workers who are ACA FTEs. The ALE is required by a collective bargaining agreement to make contributions for the union employees to a multiemployer plan. The multiemployer plan offers affordable and MV health coverage to the union employees and their children to age 26. Who is responsible for providing Form 1095-C and what codes are used in this situation?

The ALE has the obligation to furnish Form 1095-C to its identified union ACA FTEs.

Even though the ALE does not directly provide the health insurance coverage to the union employee, the ALE is treated as offering MEC to an employee if the ALE is required by a collective bargaining agreement or related participation agreement to make contributions for that employee to a multiemployer plan that offers, to individuals who satisfy the plan’s eligibility conditions, health coverage that is affordable and provides MV, and that also offers health coverage to those individuals’ dependents (multiemployer arrangement interim guidance).

For reporting offers of coverage for CY 2015, an ALE should enter code 1H on line 14 for any month for which the ALE enters code 2E on line 16 (indicating that the ALE was required to contribute to a multi-employer plan on behalf of the employee for that month and therefore is eligible for multiemployer interim rule relief). For this purpose the ALE only completes Parts I and II.

Part II

Employer Offer and Coverage

Plan Start Month (Enter 2-digit number):

All 12 months

Jan

Feb

Mar

Apr

May

June

July

Aug

Sept

Oct

Nov

Dec

14 Offer of Coverage (enter required code)

1H

15 Employee Share of Lowest Cost Monthly Premium, for Self-Only Minimum Value Coverage

16 Applicable Section 4980H Safe Harbor (enter code, if applicable)

2E

The multiemployer plan is required to issue a Form 1095-B to any covered union employee reflecting the union’s MEC during the CY.

6. An ALE offers MEC that provides MV and is affordable. What affordability safe harbor is used and how is it illustrated on Form 1095-C?

There are three affordability safe harbors:

•W-2 safe harbor (Code 2F): Coverage is affordable if the employee’s required annual contribution for self-only coverage in the lowest cost MV plan does not exceed 9.56% of Box 1 W-2 wages (does not include any elective deferrals to a 401(k), 403(b) or cafeteria plan).

•Federal Poverty Level (FPL) safe harbor (Code 2G): Coverage is affordable if the employee’s required monthly contribution for self-only coverage in the lowest cost MV plan does not exceed 9.56% of the monthly income for a single individual at 100% of FPL. For 2015, this amount is $93.77 in the 48 contiguous states. For 2016, 9.56% increases to 9.66% ($95.63 for FPL safe harbor).

• Rate of Pay safe harbor (Code 2H): Coverage is affordable if the employee’s required monthly contribution for self- only coverage in the lowest cost MV plan does not exceed:

for hourly employees, 9.56% of the employee’s hourly rate multiplied by 130 hours, or

for salaried employees, 9.56% of the employee’s monthly salary.

Generally, these safe harbors are used in Line 16 when the ALE offers ACA FTEs affordable (under one of the safe harbors) MV coverage and the employee declines the coverage. This demonstrates to the IRS that the ALE should not be penalized with respect to this employee as he received an offer of MV/affordable coverage in accordance with the employer mandate.

If the employee takes coverage under the affordable/MV plan, Code 2C is used in line 16 (as opposed to the applicable safe harbor).

If the ALE did not use a safe harbor or coverage is unaffordable, line 16 is left blank.

An ALE sponsors a fully-insured group health plan for the first six months of CY 2015. In July, the ALE changed to a self-insured group health plan. Should the ALE complete two Forms 1095-C to reflect the funding change? No. The ALE may only complete one Form 1095-C for each employee. The plan changes will be reflected on the same form.Generally, if the plan is insured, the ALE is not required to complete Part III of Form 1095-C. Given the mid-CY change in funding structure, the ALE will need to complete Part III for the months of the CY the plan was self-insured.

An ALE offers MEC that provides MV and is affordable to 100% of its ACA FTEs. For 2015, the cost of employee’s share for self-only coverage is $100/month. Can the ALE select 1A (Qualifying Offer) for line 14 on Form 1095-C?No. An ALE may only select 1A (Qualifying Offer) if all of the following apply: • The offer is made for all 12 months of the CY; • The employee contribution for self-only coverage that meets MV does not exceed $93.77/month (2015); and • There is an offer of MEC to a spouse and dependents, if applicable.In this example, the employee’s contribution for self-only coverage in the lowest cost MV plan exceeds $93.77, so the ALE would not select 1A (Qualifying Offer). Instead, the ALE would select 1E and complete line 15 reflecting the $100/ month contribution for self-only coverage.

An ALE sponsors a group health plan. An ACA FTE had coverage under the plan and then terminated employment during the CY. What codes are used in lines 14 and 16 for the months following the qualified event? Because COBRA continuation of coverage was offered due to termination of employment, the ALE uses code 1H in line 14 and code 2A in line 16, regardless of whether the employee elected COBRA.If the group health plan is self-insured and the employee (or family member) elects COBRA continuation of coverage, the months of coverage (both active and COBRA) must be reflected in Part III.

An ALE sponsors a MV group health plan that is affordable under a safe harbor. An employee earned ACA FTE status during the standard measurement period (SMP) for the entire stability period (SP). The employee elects coverage under the plan. The employee’s hours were reduced during the SP. Under the terms of the group health plan, eligibility for group health plan coverage is lost when hours drop below 130/month in the SP. Therefore, the individual has a COBRA qualified event (a reduction in hours) with a loss of eligibility for group health plan coverage. How is this illustrated in Part II of Form 1095-C? If an ALE offers COBRA due to a reduction in hours, then the ALE will use the following Codes:

Line 14 – use the 1 Code that corresponds with the offer made (this is likely Code 1E as COBRA qualifies as an offer of MEC)

Line 15 – use the cost the individual has to pay for self-only coverage (likely the full COBRA premium for self-only coverage)

Line 16:

• If enrolled in COBRA, use code 2C

This document is designed to highlight various employee benefit matters of general interest to our readers. It is not intended to interpret laws or regulations, or to address specific client situations.You should not act or rely on any information contained herein without seeking the advice of an attorney or tax professional.

• If COBRA is not elected, line 16 is left blank unless the ALE can use an affordability safe harbor (codes 2F, 2G, or 2H). However, because most ALEs charge the full COBRA premium to COBRA beneficiaries the offer of COBRA is likely an offer of unaffordable coverage and Line 16 is left blank (as illustrated below).

Part II

Employer Offer and Coverage

Plan Start Month (Enter 2-digit number): 01

All 12 months

Jan

Feb

Mar

Apr

May

June

July

Aug

Sept

Oct

Nov

Dec

14 Offer of Coverage (enter required code)

1E

1E

1E

1E

1E

1E

1E

1E

1E

1E

1E

1E

15 Employee Share of Lowest Cost Monthly Premium, for Self-Only Minimum Value Coverage

$50

$50

$50

$50

$50

$400

$400

$400

$400

$400

$400

$400

16 Applicable Section 4980H Safe Harbor (enter code, if applicable)

2C

2C

2C

2C

2C

Important to note: In this scenario, the employee earned ACA FTE status through the end of the SP. If the employee declines the offer of unaffordable coverage (COBRA) and receives a subsidy in the Marketplace, this ALE will be penalized for each month that the ACA FTE has unaffordable coverage (the “B” penalty)

11. SamefactsasQ/A-10,buttheALE’seligibilitytermscontinuecoveragethroughtheSPeventhoughtherehas been a reduction in hours. The ALE’s cafeteria plan includes a permitted election change rule that allows the employee to drop coverage even though he did not lose coverage as a result of the reduction in hours. The employee elects to drop coverage and take coverage through his spouse’s health plan. How is this illustrated in Part II of Form 1095-C?

In this case, it is reported as follows:

• Line 14 – use the 1 Code that corresponds with the offer made (Code 1A or 1E)

• Line 15 – if using Code 1E then state the cost for self-only coverage in the lowest cost MV plan (likely the same code as before the individual had the reduction in hours)

• Line 16: • Use the safe harbor code that applies (codes 2F, 2G, or 2H)

Part II

Employer Offer and Coverage

Plan Start Month (Enter 2-digit number): 01

All 12 months

Jan

Feb

Mar

Apr

May

June

July

Aug

Sept

Oct

Nov

Dec

14 Offer of Coverage (enter required code)

1E

1E

1E

1E

1E

1E

1E

1E

1E

1E

1E

1E

15 Employee Share of Lowest Cost Monthly Premium, for Self-Only Minimum Value Coverage

$50

$50

$50

$50

$50

$50

$50

$50

$50

$50

$50

$50

16 Applicable Section 4980H Safe Harbor (enter code, if applicable)

2C

2C

2C

2C

2C

2G

2G

2G

2G

2G

2G

2G

In this scenario, a penalty would not apply because the ALE continues to offer the ACA FTE MV coverage that is affordable under the FPL safe harbor (2G) for the duration of the SP. If the employee went to the Marketplace to purchase coverage, he would not qualify for a subsidy as he has an affordable offer of ALE-provided health insurance through the end of the SP.

12. What codes are used to show a mid-month hire or a mid-month termination?

If an employee was hired mid-month, use code 1H on line 14 and code 2D on line 16. An employee was hired June 15 with coverage effective first of the month following date of hire and the employee elects coverage.

Part II

Employer Offer and Coverage

Plan Start Month (Enter 2-digit number): 01

All 12 months

Jan

Feb

Mar

Apr

May

June

July

Aug

Sept

Oct

Nov

Dec

14 Offer of Coverage (enter required code)

1H

1H

1H

1H

1H

1H

1E

1E

1E

1E

1E

1E

15 Employee Share of Lowest Cost Monthly Premium, for Self-Only Minimum Value Coverage

$50

$50

$50

$50

$50

$50

16 Applicable Section 4980H Safe Harbor (enter code, if applicable)

2A

2A

2A

2A

2A

2D

2C

2C

2C

2C

2C

2C

In most cases, if an employee is terminated from an ALE mid-month, coverage continues through the end of the month (then COBRA is triggered with the loss of coverage). In this case, because the employee continues to receive the offer of coverage in this month, use:

• 1A or 1E in line 14

• In line 16 use either: 2C if the employee has coverage, or the applicable safe harbor code if no coverage, or leave blank if no safe harbor applies.

For example, assume the employee terminates employment May 15 and has coverage through May 31.

Part II

Employer Offer and Coverage

Plan Start Month (Enter 2-digit number): 01

All 12 months

Jan

Feb

Mar

Apr

May

June

July

Aug

Sept

Oct

Nov

Dec

14 Offer of Coverage (enter required code)

1E

1E

1E

1E

1E

1H

1H

1H

1H

1H

1H

1H

15 Employee Share of Lowest Cost Monthly Premium, for Self-Only Minimum Value Coverage

$50

$50

$50

$50

$50

16 Applicable Section 4980H Safe Harbor (enter code, if applicable)

2C

2C

2C

2C

2C

2A

2A

2A

2A

2A

2A

2A

In the case where coverage is lost as of the date of termination and an employee is terminated mid-month, use code 1H on line 14 and code 2B in line 16. In this instance, code 1H is used because an offer is considered to be made if the employee was eligible for coverage every day of the month. If the employee is not eligible for even one day, an offer is not considered to have been made.

For example, assume the employee terminates employment May 15 and coverage is lost effective May 15.

13. An ALE offers MEC that is not a MV plan to employees and their dependents (also referred to as a “skinny plan”). What Codes are used?

An ALE will use code 1F on line 14 and will not complete line 15. If the employee has coverage through the “skinny plan,” use code 2C in line 16. If the employee declines coverage in the “skinny plan”, leave line 16 blank.

Part II

Employer Offer and Coverage

Plan Start Month (Enter 2-digit number): 01

All 12 months

Jan

Feb

Mar

Apr

May

June

July

Aug

Sept

Oct

Nov

Dec

14 Offer of Coverage (enter required code)

1F

15 Employee Share of Lowest Cost Monthly Premium, for Self-Only Minimum Value Coverage

16 Applicable Section 4980H Safe Harbor (enter code, if applicable)

The ALE has made an offer of MEC which insulates the ALE from an “A” penalty. However, because it is not MV, the affordability safe harbors are not available. ALE has potential “B” penalty exposure if the individual declines the coverage and receives a subsidy in the Marketplace.

14. An ALE offers MEC that provides MV and is affordable under the FPL safe harbor. The ALE uses a look-back measurement period to determine ACA FTE status. A new hire variable hour employee is in his IMP from January to May of the CY and in an IAP in June and July. The ALE determines the employee earned ACA FTE status and the employee enrolls effective August 1, 2015. What codes are used for the year?

Part II

Employer Offer and Coverage

Plan Start Month (Enter 2-digit number): 01

All 12 months

Jan

Feb

Mar

Apr

May

June

July

Aug

Sept

Oct

Nov

Dec

14 Offer of Coverage (enter required code)

1H

1H

1H

1H

1H

1H

1H

1E

1E

1E

1E

1E

15 Employee Share of Lowest Cost Monthly Premium, for Self-Only Minimum Value Coverage

$50

$50

$50

$50

$50

16 Applicable Section 4980H Safe Harbor (enter code, if applicable)

2D

2D

2D

2D

2D

2D

2D

2C

2C

2C

2C

2C

This document is designed to highlight various employee benefit matters of general interest to our readers. It is not intended to interpret laws or regulations, or to address specific client situations.You should not act or rely on any information contained herein without seeking the advice of an attorney or tax professional.

15. Same facts as in Q/A-13, except this ongoing employee was measured as not an ACA FTE in prior SMP. Thus he was not eligible for health insurance coverage for August 1, 2014 – July 31, 2015. For the upcoming SMP and SP (that begins August 1, 2015) the individual becomes an ACA FTE and elects MV and is affordable under the FPL safe harbor. What codes are used for the year?

Part II

Employer Offer and Coverage

Plan Start Month (Enter 2-digit number): 08

All 12 months

Jan

Feb

Mar

Apr

May

June

July

Aug

Sept

Oct

Nov

Dec

14 Offer of Coverage (enter required code)

1H

1H

1H

1H

1H

1H

1H

1E

1E

1E

1E

1E

15 Employee Share of Lowest Cost Monthly Premium, for Self-Only Minimum Value Coverage

$50

$50

$50

$50

$50

16 Applicable Section 4980H Safe Harbor (enter code, if applicable)

2B

2B

2B

2B

2B

2B

2B

2C

2C

2C

2C

2C

16. An ACA FTE was offered health coverage and is enrolled from January to May. From June to August, the employee goes on approved leave under the Family Medical Leave Act (FMLA). From June to August the employee is enrolled in health coverage, what codes are used? Employee returns to employment after the leave.

The employee is coded in the same manner as the codes used from January to May. The fact that the employee was not actively working does not affect coverage coding unless the employee decided not to continue health coverage during FMLA leave.

Part II

Employer Offer and Coverage

Plan Start Month (Enter 2-digit number): 01

All 12 months

Jan

Feb

Mar

Apr

May

June

July

Aug

Sept

Oct

Nov

Dec

14 Offer of Coverage (enter required code)

1E

15 Employee Share of Lowest Cost Monthly Premium, for Self-Only Minimum Value Coverage

$50

16 Applicable Section 4980H Safe Harbor (enter code, if applicable)

2C

If the employee elects to drop health insurance coverage during the period of FMLA leave, then line 16 will reflect any applicable affordability safe harbor (2G, 2F or 2H) or is left blank if a safe harbor does not apply.

Part II

Employer Offer and Coverage

Plan Start Month (Enter 2-digit number): 08

All 12 months

Jan

Feb

Mar

Apr

May

June

July

Aug

Sept

Oct

Nov

Dec

14 Offer of Coverage (enter required code)

1E

1E

1E

1E

1E

1E

1E

1E

1E

1E

1E

1E

15 Employee Share of Lowest Cost Monthly Premium, for Self-Only Minimum Value Coverage

$50

$50

$50

$50

$50

$50

$50

$50

$50

$50

$50

$50

16 Applicable Section 4980H Safe Harbor (enter code, if applicable)

2C

2C

2C

2C

2C

2G

2G

2G

2C

2C

2C

2C

17. Doself-employedindividualsreceiveaForm1095-C?

A self-employed individual includes a sole proprietor, a partner in a partnership, a 2% shareholder in an S-Corp and a member/owner of an LLC, who would be treated as a partner for tax purposes.

For an insured group health plan, these individuals are not ACA FTEs, because they are not considered employees of the ALE. As such, these individuals do not receive a Form 1095-C. ALEs should discuss the status of individuals who go from a common law employee (W-2) status to self-employed status mid-year as the implications may vary and additional reporting may be necessary If the self-employed individual is covered through the insured group health plan, then the insurance carrier will issue the individual a Form 1095-B to reflect MEC.

For a self-insured group health plan, if the individual is enrolled in coverage under the group health plan for at least one month of the calendar year, that individual receives a Form 1095-C for that calendar year, with code 1G on line 14. This reflects the individual’s MEC during the calendar year under the self-insured health plan. However, if a partner or 2% S-Corp shareholder declined coverage for the entire calendar year, then a Form 1095-C is not provided.

This document is designed to highlight various employee benefit matters of general interest to our readers. It is not intended to interpret laws or regulations, or to address specific client situations.You should not act or rely on any information contained herein without seeking the advice of an attorney or tax professional.

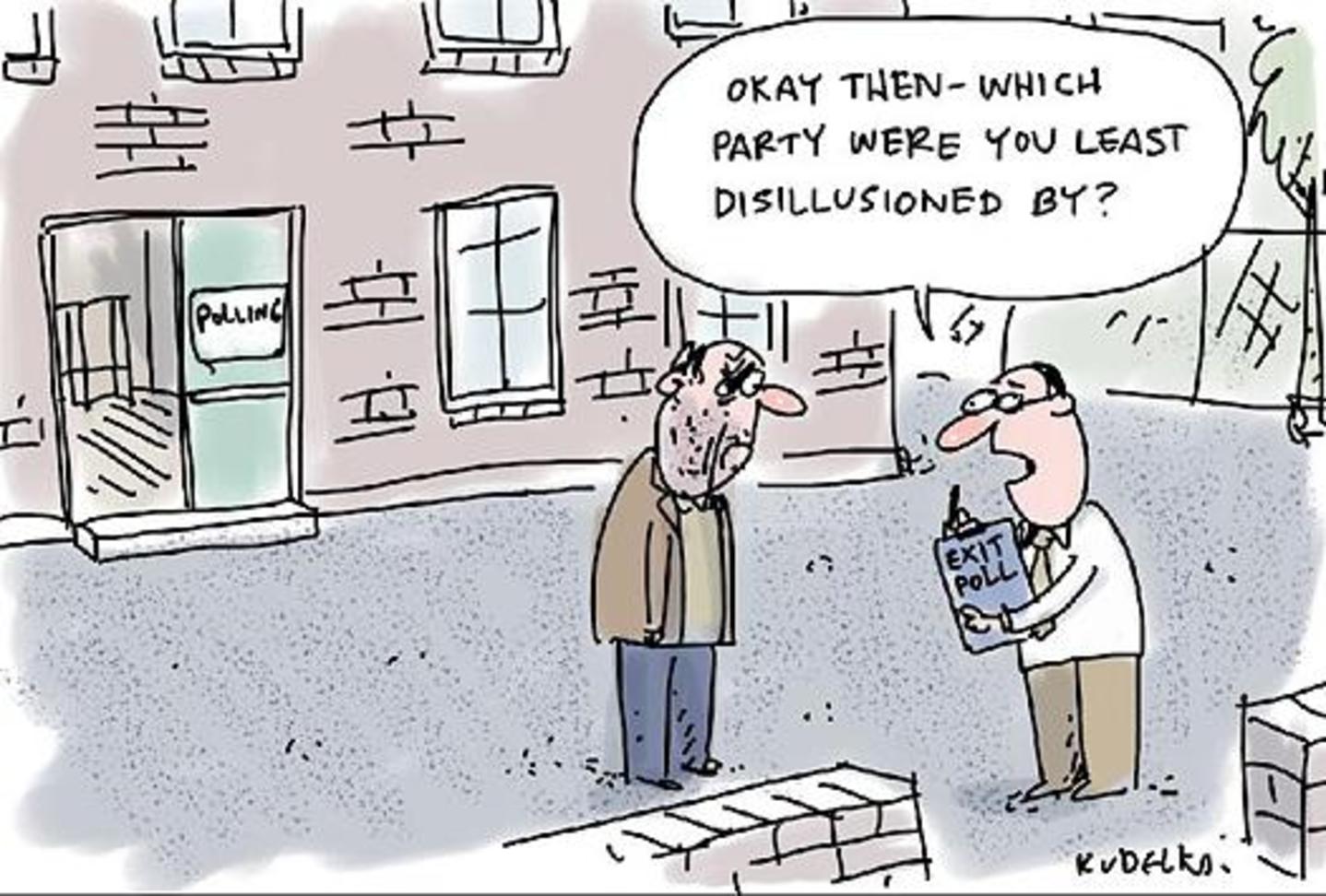

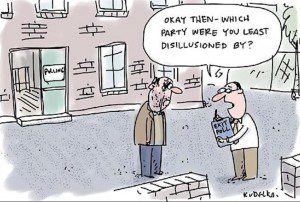

The people have spoken at least for now and they are saying they are unhappy. The storm clouds over Obmacare has ushered in GOP victories: +7 Senate + 13 House. 47% of those who cast ballots in the midterms said the 2010 health care law, which opened for enrollment a year ago, went too far. On the other hand, 26 percent said the law didn’t go far enough, CNN exit polls reported. Only 22 percent said Obamacare was just about right.

How will GOP use these powerful election gains on Obamacare?

GOP still will not have the needed 60 Senate Seats to repeal the Affordable Care Act. That said, they will now be able to pass budget rules on the legislation since the Courts ruled individual mandate penalty as a “tax”. Reinsurance funds such as Risk corridors could also be on the chopping block. Other examples would be the definition of “full-time” employee taxes on employer penalties (bipartisan support), medical devices & tanning salons etc.

According to Huffington Post article GOP-Controlled Congress Expected To Try To Repeal, Weaken ACA while Republicans have been “chomping at the bit to repeal Obamacare” since it was signed into law in 2010, even a GOP-controlled Congress is unlikely to undo the law. However, that won’t stop Republicans from forcing at least one vote on repeal. President Obama “would then swiftly veto it, but not before Democratic senators were forced to cast a vote very directly in support of Obamacare, which remains generally unpopular.” Additionally, the GOP might take aim at several provisions of the ACA, such as the individual mandate, the employer mandate, the Independent Payment Advisory Board, and the medical device tax. Some Senate Democrats would likely join them in eliminating or amending some of these measures.

A Democrat President governing with both Houses going GOP may not be so bad after all. The successful Clinton Presidency had to contend with the same balancing act. Two decades later, the key question is can both branches find a common ground and a productive working relationship?

For specific details on all available health plans in 2015, contact our team at Millennium Medical Solutions Corp (855)667-4621. We work in coordination with Navigators to assist with medicaid, CHIP Child Health Plus, Family Health Plus and Medicare Dual Eligibles. We have Spanish, Russian, and Hebrew speakers available. Quotes can also be viewed on our site.

The Health Exchange also known as The Health Marketplace or Obamacare Exchanges are set to open in less than 12 hours. Are you ready or aye you like most asking What is an Exchange? Starting Oct 1 you can enroll until March 31, 2014, though you’ll generally need to sign up by Dec. 15 of this year, to be covered as of Jan. 1. You can find your state’s marketplace at healthcare.gov. The prices for the marketplace plans are likely to be similar to those sold privately. A plan that is also available on the exchange may be eligible for subsidies. Heres an easy top 10 list of what you need to know.

10. Locate your State Exchange

Look up your state’s exchange here and Healthcare.gov. Some states are running their own exchange, others are running it through the federal government see www.healthcare.gov. For NY Tri-State the sites are:

NYS – http://info.nystateofhealth.ny.gov See rates here

CT – https://www.accesshealthct.com See rates here

9. Individual Mandate Penalty

For 2014, the annual penalty is $95 or 1% of your income, whichever is greater. The penalty will increase over the first three years. Coverage can include employer-provided insurance, individual health insurance, Medicare or Medicaid.

Health Insurance Individual Penalty for Not Having Insurance Pay the greater of the two amounts

Year

Percentage of Income

Set Dollar Amount

2014

1%

$95 & $285/family max

2015

2%

$325 & $975/family max

2016

2.5%

$695 & $2,085/family max

8. Individual Subsidies

Individuals who do not have affordable minimum essential coverage from their employer will be eligible for tax credit subsidies for their health insurance purchase on a state exchange if their income is below 400 percent of federal poverty level.

If you make under $45,960 or your family makes under $94,200, you could get a real break on health insurance costs More low-income people will also be eligible for free coverage under Medicaid For those eligible, the subsidies will cap the amount you pay for your exchange policy at between 2% and 9.5% of your income (on a sliding scale, based on your income). To find out how much you would pay, estimate your income for this year and plug it into any health subsidy calculator. You can also see estimate subsidies with these “health subsidy charts”.

7. Small Business Subsidy – SHOP Exchange

A key change is that the small business health care tax credits will only be available ONLY through the SHOP Exchange marketplace in 2014. Small businesses with 25 or fewer employees who receive less than $50,000 a year in wages may be eligible for tax credits if they purchase the plan through the SHOP marketplace. These credits will cover up to 50% of the employer’s cost (35% for non-profits) for the first two years of coverage. Click here to read more about the small business health care tax credits.

6. Your income

not your assets, such as your house, stocks or retirement accounts – will count toward determining whether you can get tax credits. When you buy your plan, you estimate your income for next year, and your tax credit is based on that estimate. The next year, your tax returns will be checked by the IRS and compared against your estimate.

5. Pre-Existing Conditions Eliminated

Your insurer generally can’t drop you, as long as you keep up with your insurance premiums and don’t lie on your application. Generally, people will be able to enroll in or change plans once a year during the annual open enrollment period. This first year, open enrollment on the exchanges will run for six months, from Oct. 1 through March of next year. But in subsequent years the time period will be shorter, running from October 15 to December 7.

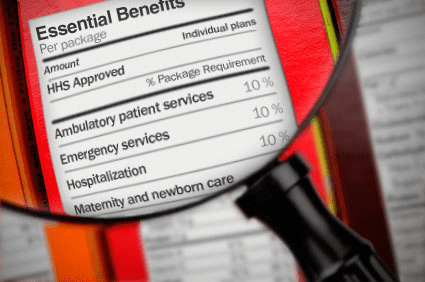

4. Essential Health Benefits Covered

Each plan covers 10 “essential health benefits,” which include prescription drugs, emergency and hospital care, doctor visits, maternity and mental health services, rehabilitation and lab services, among others. In addition, recommended preventive services, such as mammograms, must be covered without any out-of-pocket costs to you. More info here.

3. Ninety-Day Maximum Waiting Period

Group health plans and health insurance issuers may not impose waiting periods of more than ninety days before coverage becomes effective. This also applies to grandfathered plans.

2. Annual or Lifetime Limits

Group health plans, including grandfathered plans, may no longer include more than restricted annual or any lifetime dollar limits on essential health benefits for participants. Limits may exist in and after 2014 for non-essential benefits.

1. Not Everyone is Eligible

Immigrants who are in the country illegally will be barred from buying insurance on the exchanges. However, legal immigrants are permitted to use the marketplaces and may qualify for subsidies if their income is no more than 400 percent of the federal poverty level (about $46,000 for an individual and $94,200 for a family of four).

members of certain religious groups and Native American tribes

incarcerated individuals

people whose incomes are so low they don’t have to file taxes (currently $9,500 for individuals and $19,000 for married couples)

Conclusion:

There has been a lot of news about individual Obamacare provisions getting delayed – Obamacare Employer mandate Delayed. Some people may assume that means the health law is being slowly dismantled, or put off for an additional several years. .The Affordable Care Act is an extremely complicated law with a lot of moving parts, but ultimately, the biggest provisions are still moving forward. There will likely be more hiccups along the way. As the enrollment period opens for Obamacare’s new exchanges, industry experts predict there will probably be other issues that need to be ironed out — but that doesn’t mean the whole law is collapsing

Still confused?

Don’t be. These are the common questions that we are working through with our clients daily. Am I better off going SHOP Exchange vs. Individual for my business? Am I better off going off Exchanges or onto Private Exchanges? Whats my minimum employer contribution? Do I have to cover employee and dependents? Is dental and vision included? What happens to my Healthy NY when it shuts down Jan 1, 2014? What employer notices must I be posting?

Please contact our team at Millennium Medical Solutions Corp if you have additional questions regarding how SHOP Exchanges and Individual Exchanges can benefit you Stay tuned to our site for updates as more information gets released. Sign up for latest news updates.

The pre-July 4th news of Obamacare Employer Mandate Delayed until 2015 decision may have started early fireworks. The administration did not, however, delay the larger new requirements facing employers who choose to offer health insurance in the small group market––employers with less than 50 workers. The biggest requirement – Essential Health Benefits not delayed.

Whether the rationale was to alleviate business pressure to meet new mandates by Jan 2014 or the real fear that Employers have already begun making necessary employment hours cut backs to avoid the $2,000 penalty. A $3,000/employee penalty was also looming for Employers offering unaffordable insurance.

Keep in mind that this limited delay does not affect other provisions of the Affordable Care Act slated to go into effect in or before 2014, such as:

Individual mandate which requires most individuals to purchase insurance by January 1, 2014, or pay a tax penalty.

a 90-day maximum on eligibility waiting periods;

monetary caps on annual out-of-pocket maximums;

total elimination of lifetime and annual limits (including expiration of waivers that permitted certain “mini-med” plans and stand-alone Health Reimbursement Arrangements to stay in place through plan years beginning in 2013);

Patient Centered Outcomes Research Institute (PCORI) excise taxes and transitional reinsurance program fees; HRA/HSA/FSA clients also pay a monthly $1/employee tax.

a notice informing employees of the availability of the new health insurance Exchanges (a model notice is available on the U. S. Department of Labor website); and insurance market reforms.

The biggest impact is the Essential Health Benefits (EHB) which will not be delayed and this affects fully insured or ALL Small Businesses. While small employers are not required to offer coverage, if they do then they come under that large number of new essential health benefit mandates and group rating rules that won’t apply to large employers. These small group requirements are expected to increase the cost of small group coverage by an average of 15%––with wide variation by state and the average age of the group.

An employer sponsoring a Healthy NY or Brooklyn Healthworks Plan today for example would be disqualified as this does not carry all Essential Health Benefits. The very popular Healthy NY is slated to shut down for Jan 2014 and most Employers have just received this transition letter last week. Individual and Sole Prop Healthy NY is terminating and small business Healthy NY must be reapplied under a new higher cost version. While the plan did not carry Ambulance and had a $3,000 limited Pharmacy plan it is priced 35% below market and did manage to capture hundreds of thousands that would otherwise had been uninsured. The same is true for those on Hospital Only or high deductible catastrophic plans.

So what are these Essential Health Benefits?

All individual and small group policies on and off-Exchangemust cover ten categories of minimum essential health benefits.

Under the ACA, each state must choose one plan from among popular health insurance plans offered statewide to serve as a benchmark for EHBs. The benchmark plan will act as the model for how plans must define and include EHBs in their coverage — in both the individual and small group markets. New York selected the benefits of the State’s largest small group plan as its EHB benchmark. There is also a Minimum Value requirement, See NYS Minimum Value STANDARD BENEFIT DESIGN COST SHARING DESCRIPTION CHART (5-6-2013) Some of the plan’s components include:

No cost-sharing for routine preventive services

Pediatric dental and vision coverage

Habilitative and rehabilitative services, including physical therapy, speech therapy and occupational therapy

Rich mental/behavioral health services

No annual or lifetime dollar limits on benefits

Conversely, a shift to self- insurance is underway as self-insureds can avoid many taxes and instead ONLY cover the Minimum Essential Coverage which is different than the Essential Health Benefits. The strategy coupled with reinsurance is a great sophisticated model usually reserved for larger groups. This segment will be able to avoid local additional State mandates which in States like NY account for 14-16%% of the costs. Thats a total swing of 30% for a fully insured NY group. Also, self-insured groups do NOT pay added taxes such as the health insurance tax of $9 Billion annually over the next 10 years.

The administration has shown their sensitivity to larger groups. This segment already covers 94% of its employees at least in some fashion while small businesses cover less than 50%.

Why not do the same for small employers as well? And while they are at it, use the time to reconsider the impact many of these regulations are likely to have on the number of small employers continuing to offer coverage.

For a downloadable guide on self-insuring and secondary market reinsurance for your group please send contact form below. In the meantime, please visit to view past blogs and Legislative Alerts at https://360peo.com/feed.