The pre-July 4th news of Obamacare Employer Mandate Delayed until 2015 decision may have started early fireworks. The administration did not, however, delay the larger new requirements facing employers who choose to offer health insurance in the small group market––employers with less than 50 workers. The biggest requirement – Essential Health Benefits not delayed.

Whether the rationale was to alleviate business pressure to meet new mandates by Jan 2014 or the real fear that Employers have already begun making necessary employment hours cut backs to avoid the $2,000 penalty. A $3,000/employee penalty was also looming for Employers offering unaffordable insurance.

Keep in mind that this limited delay does not affect other provisions of the Affordable Care Act slated to go into effect in or before 2014, such as:

Individual mandate which requires most individuals to purchase insurance by January 1, 2014, or pay a tax penalty.

a 90-day maximum on eligibility waiting periods;

monetary caps on annual out-of-pocket maximums;

total elimination of lifetime and annual limits (including expiration of waivers that permitted certain “mini-med” plans and stand-alone Health Reimbursement Arrangements to stay in place through plan years beginning in 2013);

Patient Centered Outcomes Research Institute (PCORI) excise taxes and transitional reinsurance program fees; HRA/HSA/FSA clients also pay a monthly $1/employee tax.

a notice informing employees of the availability of the new health insurance Exchanges (a model notice is available on the U. S. Department of Labor website); and insurance market reforms.

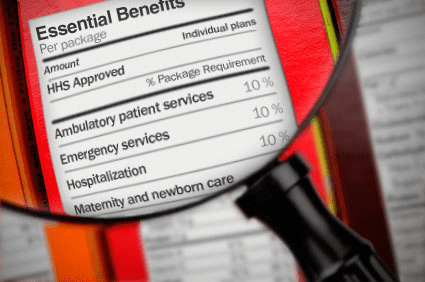

The biggest impact is the Essential Health Benefits (EHB) which will not be delayed and this affects fully insured or ALL Small Businesses. While small employers are not required to offer coverage, if they do then they come under that large number of new essential health benefit mandates and group rating rules that won’t apply to large employers. These small group requirements are expected to increase the cost of small group coverage by an average of 15%––with wide variation by state and the average age of the group.

An employer sponsoring a Healthy NY or Brooklyn Healthworks Plan today for example would be disqualified as this does not carry all Essential Health Benefits. The very popular Healthy NY is slated to shut down for Jan 2014 and most Employers have just received this transition letter last week. Individual and Sole Prop Healthy NY is terminating and small business Healthy NY must be reapplied under a new higher cost version. While the plan did not carry Ambulance and had a $3,000 limited Pharmacy plan it is priced 35% below market and did manage to capture hundreds of thousands that would otherwise had been uninsured. The same is true for those on Hospital Only or high deductible catastrophic plans.

So what are these Essential Health Benefits?

All individual and small group policies on and off-Exchangemust cover ten categories of minimum essential health benefits.

Under the ACA, each state must choose one plan from among popular health insurance plans offered statewide to serve as a benchmark for EHBs. The benchmark plan will act as the model for how plans must define and include EHBs in their coverage — in both the individual and small group markets. New York selected the benefits of the State’s largest small group plan as its EHB benchmark. There is also a Minimum Value requirement, See NYS Minimum Value STANDARD BENEFIT DESIGN COST SHARING DESCRIPTION CHART (5-6-2013) Some of the plan’s components include:

No cost-sharing for routine preventive services

Pediatric dental and vision coverage

Habilitative and rehabilitative services, including physical therapy, speech therapy and occupational therapy

Rich mental/behavioral health services

No annual or lifetime dollar limits on benefits

Conversely, a shift to self- insurance is underway as self-insureds can avoid many taxes and instead ONLY cover the Minimum Essential Coverage which is different than the Essential Health Benefits. The strategy coupled with reinsurance is a great sophisticated model usually reserved for larger groups. This segment will be able to avoid local additional State mandates which in States like NY account for 14-16%% of the costs. Thats a total swing of 30% for a fully insured NY group. Also, self-insured groups do NOT pay added taxes such as the health insurance tax of $9 Billion annually over the next 10 years.

The administration has shown their sensitivity to larger groups. This segment already covers 94% of its employees at least in some fashion while small businesses cover less than 50%.

Why not do the same for small employers as well? And while they are at it, use the time to reconsider the impact many of these regulations are likely to have on the number of small employers continuing to offer coverage.

For a downloadable guide on self-insuring and secondary market reinsurance for your group please send contact form below. In the meantime, please visit to view past blogs and Legislative Alerts at https://360peo.com/feed.

In an effort to improve the safety and efficacy of sunscreen products sold in the U.S. and limit misleading claims, the U.S. Food and Drug Administration officially released a new set of requirements that sunscreen manufacturer’s must begin to follow when making and marketing their products. No more claims of “waterproof” or “sweat proof” (thee claims are overstated). No agonizing over SPFs higher than 50 (there is no sufficient data to show that products with SPF values higher than 50 provide greater protection). And if a manufacturer wants to slap a “broad spectrum” claim on the label, first the product will need to pass a test that proves it does indeed protect against both UVA and UVB rays. Some manufacturers will begin to incorporate these mandates right away, while others may wait until the official ruling kicks in the summer of 2012.

So what’s a sun-savvy consumer to do in the meantime? Dermatologist John Anthony, M.D. of Cleveland Clinic’s Strongsville Family Health and Surgery Center weighs in with these helpful tips about choosing the best sun protection:

• The jury is still out on how chemical sunscreens with ingredients such as oxybenzone, Vitamin A (retinol), and PABA (para-aminobenzoic acid) affect human health. But Dr. Anthony says that if you’re looking to avoid chemical sunscreens, choose a mineral-based one instead since these use physical blockers such as zinc oxide or titanium dioxide. Because mineral sunscreens in spray form create nanoparticles that can be absorbed into the lungs, play it safe and use mineral-based creams and lotions instead of sprays.

• Look for sunscreens that block both ultraviolet A rays (UVA rays contribute to photo-aging and may cause skin cancer) and UVB rays (the ones that cause those red sunburns that blister).

• Choose a middle-of-the road sun protection factor (SPF) of 30 to 50. Any lower and you really limit the amount of time you can spend in the sun before getting burned by UVB rays (roughly 30 minutes) and needing to reapply. Any higher and Dr. Anthony says you risk thinking that you’ve got so much protection you need not reapply every two hours or after swimming, the standard recommendation. Be smart and always reapply sunscreen after swimming or exercising.

• Get sun-sensible: If you can avoid being in the sun during primetime sun hours — from 10 a.m. to 2 p.m. — do. If not, wear a hat and protective clothing, and seek out the shade, says Dr. Anthony. “Sunscreen isn’t a bulletproof vest against sun damage. It’s just one tool that we can use to help protect us.”

Yoga initiatives improves health and reduces costs according to Aetna studies. A yoga and meditation initiative for stressed employees helped them reduce their heart rates and helped Aetna increase productivity and lower health benefit costs 7%, CEO Mark Bertolini told the Third Metric conference.

Ezekiel Emanuel of the University of Pennsylvania said while data on the efficacy of wellness programs overall is mixed, prevention efforts, including traditional wellness programs, are important for saving money and improving health.

In Huffington Post article Company Wellness Programs May Boost Bottom Lines, Aetna CEO Mark Bertolini Says when Aetna determined in 2010 that its workers with the highest levels of stress were costing the company $2,000 more each year than co-workers, the company created an initiative to promote yoga and meditation. Bertolini said at the Third Metric conference co-sponsored by The Huffington Post in New York Thursday. The results include improvements in heart rates and increased productivity.

“Stress can have a significant impact on physical and mental health, so there is a strong need for programs that help people reduce stress as part of achieving their best health,” said Aetna Chairman and CEO Mark T. Bertolini. “The results from the mind-body study provide evidence that these mind-body approaches can be an effective complement to conventional medicine and may help people improve their health, something that I have experienced personally.”

Yoga and Stretching

The study participants included 239 Aetna employees in California and Connecticut who volunteered for the two mind-body stress reduction programs. As part of the studies, 96 employees were randomly assigned to mindfulness-based classes, 90 were randomly assigned to therapeutic yoga classes and 53 were randomly assigned to the control group.

The Affordable Care Act recognizes the benefits of wellness which also includes alternative medicines such as yoga, massage therapy, acupuncture etc. Long awaited guidance on how employers can institute a wellness program using financial incentives and discounts were released recently – Final Wellness Incentive Rule Released.

Does your company offer a wellness program? For more information, you may review the final rulesin their entirety. For MMS Corp previous blogs on wellness, clickhere. we will keep you posted on future PPACA wellness program opportunities. Ask us for more info on Aetna Wellness, Yoga, and how we can help you implement a healthy program for your staff.

Error: Contact form not found.

The views expressed in this post do not necessarily reflect the official policy, position, or opinions of MMS Corp. This update is provided for informational purposes. Please consult with a licensed accountant or attorney regarding any legal and tax matters discussed herein.

Want to cook up a plan to keep your immune system in tip-top shape? Some experts believe that even slight deficiencies in certain nutrients can lower our defenses. hile an apple a day is a good start, it definitely takes a bigger — and brighter — cornucopia to boost your disease-fighting ability. Here below are natural best foods to boost immunity.

Quick, Don’t Get Sick! We’ve all been there: We feel a cold coming on, so we start popping megadoses of vitamin C. We’ve been doing it for decades even though there’s little evidence to suggest it will keep us from getting sick. According to the Cochrane Database of Systematic Reviews, which looked at 30 trials involving a total of 11,350 participants,vitamin Chad no effect on how often people caught colds. It did slightly reduce the cold’s duration — by 8 percent, or roughly 9.5 hours for a five-day illness — but only if taken before symptoms arose.

However, a Canadian over-the-counter pill (available in the U.S.) called COLD-fX, made from North American ginseng, has shown dramatic results. Healthy people reduced their risk of colds by 56 percent, the severity by 31 percent and duration by 35 percent. And in nursing home seniors, it reduced their risk of the flu by 89 percent. The only downside: You have to take it twice a day for the entire cold and flu season (four months).

Color of Health A healthy diet full of antioxidant-rich fruits and vegetables is a vital part of a well-functioning immune system. Antioxidants are food-based chemicals, such as vitamins and minerals, that neutralize free radicals in our bloodstream. Free radicals — toxic by-products of digestion, pollution and cigarette smoke — damage DNA, cause many types of cancer and suppress the immune system.

Eating fortified, processed foods, supplemented with a multivitamin, might get you all of the vitamins you need, but, explains Joel Fuhrman, MD, author of Eat for Health and Eat to Live, we’re depriving ourselves of thousands of micronutrients that we haven’t even discovered yet. “It’s very hard to duplicate Mother Nature,” he says. “More than half of the micronutrients in plants are phytochemicals, not vitamins.” Phytochemicals are compounds produced by plants to protect themselves from environmental stresses like UV damage. Research shows that by eating foods rich in phytochemicals, we can boost our health as well. According to Dr. Fuhrman, these chemicals keep our cells from aging, while some even cause cancer cells to self-destruct. A few of the heavy hitters you’ve probably heard of include lycopene (tomatoes), polyphenols (tea) and resveratrol (grapes). Broccoli and other cruciferous vegetables, like cabbage, brussels sprouts and cauliflower, contain some of the most powerful cancer fighters that we know of — actually shrinking tumors in laboratory experiments.

For the best protection, David Katz, MD, MPH, director of the Yale University Prevention Center, and Dr. Fuhrman recommend eating a wide variety of fruits and vegetables that cover the entire color spectrum. “Foods work together to maximize immune function, which then prolongs health and helps prevent chronic disease,” Dr. Fuhrman says.

Good Fat, Bad Fat To beef up your immune system, try to reduce the amount of red meat and saturated fat that you eat, and replace them with fish andomega-3 fatty acids, recommends Charles Stephensen, PhD, a research scientist with the USDA at the Western Human Nutrition Research Center. “Saturated fats activate the immune system, promote inflammation and are associated with increased cardiovascular risk,” Dr. Stephensen says.

Inflammation occurs when the immune system senses an intruder, so in a sense, these fats make the body think there’s an invader that has to be isolated and wiped out. Chronic inflammation can result in Alzheimer’s, diabetes, heart disease and arthritis.

“Omega-3s, on the other hand, seem to have the opposite effect on the immune system,” Dr. Stephensen says. Eating fatty fish or taking afish oil supplement (one to two grams a day) reduces levels of inflammation in the body.

D Is for Defense When we talk about boosting the immune system, what we’re really discussing is making it run optimally, Dr. Stephensen says. Once an infection or virus is gone, the immune system needs to be able to stop its attack. An overactive response can lead to autoimmune diseases, where the body turns on itself, attacking its own tissue as if it were a foreign threat. Some examples are rheumatoid arthritis, type 1 diabetes and lupus. According to Dr. Stephensen, it is now suspected that a vitamin D deficiency may increase our risk of flu and worsen the effects of autoimmune diseases. “Vitamin D can act directly on the immune system. It seems to be able to protect against bacterial infections and regulate our immune response. A deficiency allows an overstimulation of the system,” he explains.

Vitamin D is produced in our body when our skin absorbs the sun’s ultraviolet rays. Because it’s present in very few foods, and sunscreen blocks the sun’s effects, it’s very difficult to get your daily recommended dose. In fact, a recent study published in the Archives of Internal Medicine reports that 75 percent of U.S. teenagers and adults are vitamin D deficient. What’s more, Dr. Stephensen says that the recommended daily allowance, which ranges from 200 to 600 IU, depending on your age, may be too low. Thomas Morledge, MD, of the Center for Integrative Medicine at the Cleveland Clinic,recommends aiming for 1,000 IU daily. Although higher doses may be needed, this should be guided by your doctor. Good sources include fortified milk and fish; a 3.5-ounce serving of salmon contains 360 IU, while a glass of milk has about 100 IU. Ten minutes of sun (sans sunscreen) is also a good source of vitamin D. That said, Dr. Morledge recommends that everyone take a vitamin D supplementsince it’s unlikely you will get your required daily allowance through food and limited, unprotected sun exposure.

An interesting NYT article today “Slower Growth of Health Costs Eases U.S. Deficit” describes the good news that actual spending has been reduced by 15% or $200 Billion than projected 3 years ago. New data also show overall health care spending growth continuing at the lowest rate in decades for a fourth consecutive year.

Its any ones guess to the exact cause of this good news I will venture to say a good part of is the severe escalating out of pocket costs. With average office copays $50 and $200 for ER and many replacing these plans with high deductibles is it any wonder there is lower utilization? One might argue are poor health plans the cause for middle class leading to lower usage? To get an updated picture of todays NY Small Business rates once can get instant quote on our site and implement strategies in “How to Reduce My Health Care Costs“. In some instances people are turning to self insured Health Savings Accounts carrying deductibles as high as $5000 Individual and $10,000 Family.

In 2014 Individual Health Exchanges will offer a subsidized rate for lower income. For example, a $25,000 Individual filer would get approximate 80% subsidized rate and pay approx. $100/month. However salaries are not geo-sensitive and the average NY Middle Class Household will not see this subsidy. There are a number of questions outstanding such as the quality of the network. Also some Governors such as Christy Has Rejected Exchange is capable of running this Exchange version.

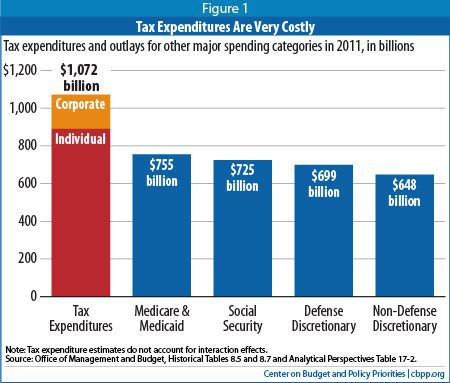

On the higher end according to CBO “tax expenditures disproportionately benefit the most well-off. As Figure 2 shows, the most affluent 20 percent of Americans receive 66 percent of all tax expenditure benefits (the richest 1 percent alone getting 24 percent of the benefits), while the middle 60 percent of households received just 31 percent of the benefits. In contrast, the middle 60 percent of households receive a proportionate share (58 percent) of the benefits of entitlement programs on the spending side of the budget (see Figure 3). The poorest fifth of households receive 32 percent of these benefits.”

But the greatest looming concern are costs. is behavior changing? Are people initiating preventive care more readily? Are they enrolled in wellness programs, managing chronic conditions, seeking Urgent Care vs. ER, using generics vs brands? Is technology playing a greater role such as mobile devices in managing care? Are modern medicine efficiencies such as avoiding testing redundancies and EMR helping?

No one argues that medical costs are a drag on the economy and are directly linked to our prosperity. “Slower cost growth would have ramifications far beyond the deficit. According to calculations by White House economists, slowing the annual growth rate of health care costs by 1.5 percentage points might increase economic output by 2 percent in 2020 and 8 percent in 2030. It might also lead to higher wages for workers and more room for productive investments in the budget.”

The hope is medical care is becoming more efficient. Whether or not the rate is subsidized it is still being paid for by someone. With this new finding it does offer hope but unless there are added incentives such a preventive medications under an Health Savings Account card covered without a deductible the concerns are Middle Class families will be reluctant to access care and we all end up paying for this.

You can self quoteon our site. Contact us at 1-855-667-4621 for more customized information.

In years past, most health insurance policies had limits or “caps” on the benefits they would pay. These limits were on any health plan participant (individual or family) – either over a lifetime or in a plan year. If someone exceeded that limit, benefits ended. While this rarely occurred, it resulted in major financial troubles for the few people it hit. The new law does not allow lifetime limits on”essential health benefits”. The law also restricts annual limits from now until 2014, when their use will become more limited. However, the law doesn’t prevent a plan from excluding all benefits for a condition.

Lifetime limits Employers must eliminate lifetime limits on essential health benefits.

Effective This applies to all health plans, including grandfathered plans.

Grandfathered plans will lose their grandfathered status if they impose an overall annual or lifetime limit on the dollar value of essential benefits if their plan did not include that limit prior to March 23, 2010. Plans can keep their grandfathered status if they convert lifetime limits into an annual limit at a dollar value that is lower than the lifetime limit on March 23, 2010.

Annual limits Employers must eliminate annual limits by 2014. Until then, plans may place only “restrictive” annual limits on essential health benefits. The limits have been set for plan years that begin:

9/23/2010 to 9/22/2011 – $750,000 annual limit

9/23/2011 to 9/22/2012 – $1.25 million annual limit

9/23/2012 to 12/31/2013 – $2 million annual limit

Annual limits must apply on an individual-by-individual (not family) basis.

Essential Health Benefits defined According to the law, the list of essential health benefits must include:

Ambulatory patient services

Emergency services

Hospitalization

Maternity and newborn care

Mental health and substance use disorder services, including behavioral health treatment

Prescription drugs

Rehabilitative and habilitative services and devices

Laboratory services

Preventive and wellness services and chronic disease management

Pediatric services, including oral and vision care

The government has not released the final regulation on essential benefits. Until it does, the government will take into account an employer’s “good faith effort” to comply with reasonable consistent interpretation.

After a six-month delay in the original effective date, group health plans (including grandfathered plans) will soon need to comply with a new requirement under Health Care Reform to provide a summary of benefits and coverage (SBC) so that employees can more easily compare insurance options.

The new SBC notice requirements are effective for plan years and open enrollment periods beginning on or after Sept. 23, 2012. If you need a refresher, the following are some key points for group health plans:

An SBC must be provided to plan enrollees at specific times, such as upon application for coverage and at renewal, as well as upon request.

Insured group health plans can satisfy the requirement if the issuer provides a timely and complete SBC to the participant or beneficiary.

Combining information for different coverage tiers, different cost-sharing selections (such as levels of deductibles and copayments), and different add-ons to major medical coverage (such as FSAs, HRAs, HSAs, or wellness programs) into one SBC is permissible, provided the appearance is understandable.

SBCs may be provided either as a stand-alone document or in combination with other summary materials (for example, an SPD), if the SBC information is intact and prominently displayed at the beginning of the materials and in accordance with the SBC timing requirements.

The SBC must comply with certain appearance and format requirements and must use terminology understandable by the average plan enrollee; an SBC template along with instructions and related materials that may be used to satisfy the notice requirements, is available online.

The U.S. Department of Labor has released three sets of Frequently Asked Questions (FAQs) which address a number of issues relating to the SBC notice requirements. The FAQs also make clear that, during the first year of applicability of the new SBC rules, penalties will not be imposed on plans that are working diligently and in good faith to provide the required content in an appearance that is consistent with the final regulations.

Bluecard PPO – Outside members home region, the PPO medical plan is known as BlueCard PPO. The BlueCard plan offers a network of quality doctors and hospitals known as the BlueCard Provider Network.

freedom to seek care in-network or out-of-network;

no need to select a primary care physician to coordinate your care;

visit specialists directly — no referrals are required;

no claim forms to submit when using an in-network provider;

no balance bills when using an in-nework provider;

wellness programs, including fitness reimbursement and discounts on alternative health care services, at no additional cost;

enhanced programs to control and manage chronic conditions;

preventive care for children and adults;

enjoy in-network coverage anywhere in the United States when you use providers that participate in the Personal Choice or BlueCard PPO networks;

worldwide coverage and recognition of the Blue Cross® symbol.

How Does it Work?

Blank Suitcase Logo

A blank suitcase logo on a member’s ID card means that the patient has Blue Cross Blue Shield traditional, POS, or HMO benefits delivered through the BlueCard Program.

“PPO in a Suitcase” Logo

You’ll immediately recognize BlueCard PPO members by the special “PPO in a suitcase” logo on their membership card. BlueCard PPO members are Blue Cross and Blue Shield members whose PPO benefits are delivered through the BlueCard Program. It is important to remember that not all PPO members are BlueCard PPO members, only those whose membership cards carry this logo. BlueCard PPO members traveling or living outside of their Blue Plan’s area receive the PPO level of benefits when they obtain services from designated BlueCard PPO providers.

How to Verify Membership and Coverage

Once you’ve identified the alpha prefix, call BlueCard Eligibility to verify the patient’s eligibility and coverage.

1. Have the member’s ID card ready when calling.

2. Dial 1.800.676.BLUE.

Operators are available to assist you weekdays during regular business hours (7am – 10pm EST). They will ask for the alpha prefix shown on the patient’s ID card and will connect you directly to the appropriate membership and coverage unit at the member’s Blue Cross Blue Shield Plan. If you call after hours, you will get a recorded message stating the business hours.

Keep in mind BCBS Plans are located throughout the country and may operate on a different time schedule than Anthem Blue Cross and Blue Shield. It is possible you will be transferred to a voice response system linked to customer enrollment and benefits or you may need to call back at a later time.

International Claims

The claim submission process for international Blue Cross and Blue Shield Plan members is the same as for domestic Blue Cross and Blue Shield Plan members. You should submit the claim directly to Anthem Blue Cross and Blue Shield.

Updated Guidance for Reporting Employer-Sponsored Health Coverage on Form W-2

New guidance from the IRS provides additional information for employers that are subject to the requirement under Health Care Reform to report the value of the health insurance coverage they provide employees beginning with 2012 Forms W-2 (generally furnished to employees in January 2013).

The requirement continues to be optional for smaller employers filing fewer than 250 Forms W-2 in the preceding calendar year unless and until further guidance is issued (but be sure to comply with any state-specific requirements regarding reporting the cost of health coverage provided to adult children).

New Guidance Updates Information on How to Report, Coverage to Include, and Determining Costs of Coverage Among other things, the new guidance:

– Clarifies the application of the interim relief from the reporting requirement for employers filing fewer than 250 Forms W-2 for the preceding calendar year; – Adds a new example that demonstrates that the reporting requirement does not apply to coverage under a health flexible spending arrangement (FSA) if contributions occur only through employee salary reduction elections; and – Provides that employers are not required to include the cost of coverage under an employee assistance program (EAP), wellness program, or on-site medical clinic in the reportable amount if the employer does not charge a premium with respect to that type of coverage provided under COBRA to a qualifying beneficiary.

Additional Information To read the new guidance in its entirety, see Notice 2012-9. You can also view the Frequently Asked Questions regarding this requirement from the IRS.

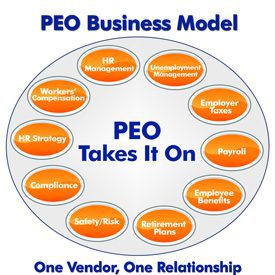

A Professional Employer Organization- FAQ. Hope this FAQ is a helpful resource as so many Employer groups have been asking about the use of Professional Employer Organization to handle their full HR, payroll and insurance solutions.

Q | What is a PEO, ASO, HRO and why should I care about them?

A PEO is a Professional Employer Organization a single source provider of integrated services which enable business owners to cost-effectively outsource the management of human resources, employee benefits, payroll and workers’ compensation and other strategic services, such as, recruiting, risk/safety management, and training and development through co-employment. It does this by hiring a client company’s employees, thus becoming their employer of record for tax purposes and insurance purposes.

An ASO is an Administrative Services Organization provides business transaction-based human resources services such as support with payroll, benefits, and employee data management. An ASO solution differs from a Professional Employer (PEO) model because there is no co-employment – the employment relationship is maintained by the client.

HRO is Human Resource Outsourcing in an HRO model, the solution focuses on managing the entire HR business process, unlike the Administrative Service (ASO) model which focuses on the transaction. An Employee Call Center is inherent to the solutions within an HRO offering. An HRO solution differs from a Professional Employer (PEO) model because there is no co-employment – the employment relationship is maintained by the client.

Q | What services and solutions does a PEO offer?

A PEO offers a complete suite of services and solutions; through our strategic partnerships we have established relationships with the industry leaders in their respective markets. We offer solutions’ in the following areas:

Payroll and Human Resource Administration

Human Resource Management Systems (HRMS)

Benefit Plans and Total Benefit Management

COBRA, HRA, HSA, FSA Management and Implementation

Commuter benefits and Health and Wellness programs

401-k plan designs and TPA services and financial planning

Employee Assistance Programs

Q | I have heard of Human Resource Outsourcing, what is the advantage to dealing with Millennium Medical Solutions versus a company directly?

A| The advantage is that while working with one company can provide a solution, however they only can quote their respective services. Millennium Medical Solutions works with numerous Human Resource Outsourcing organizations; we enable you to efficiently compare all providers through one simple application. Since there is no fee for our service, we offer an unbiased comparison and aren’t tied to one specific provider, leaving us the ability to objectively compare all solutions with your best interest at the core of solution.

Q | What does human capital mean?

A | Human Capital refers to the management of a company’s most valuable asset, their employees. At Millennium Medical Solutions we refer to human resources as human capital.

Q | What if I already work with a PEO, ASO, or HRO provider?

A | That in fact is many times the case; however our platform has every PEO, ASO, and HRO provider in one location. We scoured the market to find the best in breed in the PEO, ASO, and HRO market and our strategic partnerships for a la carte services are industry leaders. Our proprietary software allows you to shop the entire PEO, ASO, and HRO market in one submission, versus going it alone and collecting quotes from each individual provider. Many of our current clients were with other providers prior to working with us; we ensure that your current solution is giving you the best deal. If you current solution is the best fit for you, then we will advise of that as well.

Q | Who are the providers you work with?

A | Millennium Medical Solutions e works with the leading providers, some national in scope and others regional in scope. We are constantly evaluating and adding new providers, so our vendors are currently growing daily. For a list of our current providers we invite you to visit our strategic partners’ page to learn more about our providers.

Q | What are the costs for your services?

A| For our PEO, ASO, and HRO services, there are no fees, we are compensated by our strategic partners. Very few of our services actually have a fee, contact us for more information and we’ll be happy to tailor a solution to fit your needs and breakdown all the costs associated with our services and solutions.

Q | If I am a PEO, ASO or HRO provider and would like to be a part of Millennium Medical Solutions, whom do I contact?

A Millennium Medical Solutions is always looking to add and build strategic partnerships, to learn more, feel free to contact us at info@medicalsolutionscorp.com.

Q | If I am interested in learning more about PEO, how can I get more information?

A | Millennium Medical Solutions is all about options; you can call us, email us or just add our RSS feed. Our number is (914)207-6161,info@medicalsolutionscorp.comor 200 Business Park Dr, Suite 200 Armonk NY 10504 If you have a question that was not answered here or have additional questions, please feel free to contact us and we’ll be happy to answer your questions.