Whether you’re evaluating your company’s current dental benefits or preparing to offer a plan for the first time,

choosing the best program can be a bit of a balancing act. The challenge of achieving this balance is made more difficult when you consider the options available in the dental benefits marketplace today.Dental carriers typically offer one or more of three basic types of plans:

1. Fee-For-Service (or Indemnity) Plan

The original dental benefits plan and the one which continues to dominate the market is the fee-for-service plan. Under this type of plan, employers and/or their covered employees pay a monthly premium to an insurance carrier, which is responsible for reimbursing dentists for the services they provide. Fee-for-service plans allow employees the most freedom in choosing their dentists, which is why they remain a popular choice. If the main concern for you or the employees you’re covering is the ability to choose a certain dentist, a fee-for-service plan is probably your best choice.

2. Dental PPO

Dental preferred provider organizations (PPOs) are a good option for groups seeking lower cost advantages while providing enrollees with a high level of freedom of choice in selecting providers. Enrollees have the freedom to visit any dentist who is part of a network

Preventive Care Usually Includes:

Annual bite wing x-rays.

Semiannual cleaning, polishing, and possibly semiannual fluoride.

Treatment for employees and their dependents 18-years-old and younger.

Basic Dental Care Includes:

Restorations and basic oral surgery.

Major Care Includes:

Crowns, root canals and prosthetics.

Complex restorations and advanced oral surgery.

established by the dental benefits company or, for higher out-of-pocket costs, can visit any non-network dentist.

3. Dental HMO

Dental health maintenance organizations (DHMOs) give subscribers access to a select group of dentists, with even greater cost savings. This type of program is a good choice for groups seeking lower costs with an emphasis on prevention and a pre-selected network of dentists from which to choose.

Whether it’s a fee-for-service, PPO or DHMO plan, coverage of specific services can vary. Some dental benefits programs cover diagnostic and preventive services only. Others cover the full range of dental services, from preventive to basic and major care. (See right-hand box.)

Riders:Many insurers also offer riders for popular extras, like coverage for orthodontics or cosmetic dentistry. For a little additional cost, riders enable you to customize or supplement a basic dental benefits package.

In the end, finding the right dental benefits program is a combination of many factors. In addition to matching a plan with your company and employees, look closely at other issues such as cost management, rate stability, the network of participating dentists, ease of administration, customer service and company reputation.

Knowing what to ask and how to communicate your company’s wishes makes it more likely your dental insurance will do what it’s meant to do — attract good employees and help them preserve their oral health.

IMPORTANT: A great value is a discounted dental plan. Our very own Bonus Card extends the Aetna Dental Access PPO negotiated rates to members. There are NO pre-existying conditions, NO annual deductibles & NO annual maximums. Cosmetics such as orthodontia and implants are covered. The Bonus Card also covers Vision with Coast to Coast, Rx discount and Telemedicine for $10/month!

Sample Discounted Fees and Savings

Procedure Description

Usual Fee

Discounted Fee

Member Savings

% Savings

Routine 6 Month Check-Up

$43

$24

$19

44%

In Depth Check-Up

$69

$37

$32

46%

Full Mouth X-Rays

$114

$65

$49

43%

Four Bitewing X-Rays

$55

$25

$30

55%

Panoramic Film

$97

$50

$47

48%

Adult Teeth Cleaning

$83

$44

$39

47%

Child Teeth Cleaning

$62

$32

$30

48%

Protective Sealant / Tooth

$46

$26

$20

43%

1 Surface White Filling

$135

$71

$64

47%

Single Crown Porcelain

$981

$566

$415

42%

Molar Root Canal Treatment

$919

$522

$397

43%

Perio Scaling and Root Planning

$217

$123

$94

43%

Full Upper Denture

$1,353

$725

$628

46%

* Actual Costs and savings vary by provider and geographical area. * Dental benefit not available to Vermont residents.

Insurance Versus Dental Cost Examples

The following is a comparative example between a typical insured dental plan versus the Aetna Access Dental discount plan. This illustrates the possible out of pocket costs for each.

Insurance Charges

First 12 Months Premium (Family)

$627.12

Adult Cleaning

$5.00

Child Cleaning

$5.00

Routine Check-Up

$5.00

Four Bitewing X-Rays

$5.00

Composite (white) Filling

$10.00

Crown

$878.00

Molar Root Canal

$855.00

Extraction (single tooth)

$11.00

Total Insurance Charge:

$2,401.12

Total Savings:

$988.12

Discount Charges

Annual Member Fee

$33.00

Adult Cleaning

$54.00

Child Cleaning

$38.00

Routine Check-Up

$28.00

Four Bitewing X-Rays

$32.00

Composite (white) Filling

$78.00

Crown

$604.00

Molar Root Canal

$474.00

Extraction (single tooth)

$72.00

Total Discount Charge:

$1,413.00

Percent Savings:

41%

The select regional average fee represents the average fees for the procedures listed above in Los Angeles, Orlando, Chicago and New York City, as displayed in the Estimate the Cost of Care tool as of November, 2005.

* Insurance plan based on the Aetna DMO Plan. * Actual costs and savings vary by provider and geographical area. Numbers given are regional average fees.

Sources: http://newbenefits.com – New Benefits Dental Care and Aetna Dental Access® Marketing Materials and FAQ http://cdc.gov/OralHealth – Centers for Disease Control and Prevention (statistics) http://moreinformationplease.com – Dental Care Program Information http://adha.org – Oral Health Statistics and Facts http://dentalplans.com – Aetna Dental Access® Nationwide Dental Discount Program (savings information)

SHOP Exchange Delayed One Year. The White House just announced that the online Small Business Health Marketplace also known as SHOP Exchange has been delayed until 2015. Small businesses will still have the option to purchase coverage through the new marketplace but will not be able to do so online. Instead, until next fall, employers with fewer than 50 workers will need to work through a broker or agent to buy health plans for their employees.

The Small Business Health Options Program, or SHOP Exchange, has already had a troubled launch with multiple delays as the Obama administration has focused much of its efforts on launching the individual insurance marketplace where Americans can shop for subsidized health insurance coverage.

Small businesses buying coverage will still be eligible for small business tax credits to bring down the cost, according an administration memo. Also, businesses can still purchase the same plans and same rates available on Off-Exchange. Medical Insurance premiums through the business is an ordinary tax deductible expense.

According to NY Times Article, Online Health Law Sign-Up Is Delayed for Small Business – “The announcement of the delay, just before Thanksgiving, is reminiscent of the way the White House announced, just before the Independence Day weekend, a one-year delay in the requirement for larger employers to offer health insurance to employees.”

The recent setback is the latest in a stream of missed deadlines, including a postponement for a Spanish language sign-up tool announced this week. The administration also recently pushed back the enrollment deadline for individuals: People who sign up by Dec. 23 can get coverage that starts on Jan. 1. In an earlier delay, businesses with more than 50 workers were given until 2015 to meet the requirement to provide health insurance without paying a penalty. And the deadline date for individuals to avoid penalties for failing to get coverage was pushed back six weeks.

If you should have any further questions regarding the SHOP program or comments about the above or the attached, please let us know. We will continue to monitor this issue and all ACA implementation in an effort to keep you informed of new developments. In the meantime, please visit our https://360peo.com/about-us/blog to view past blogs and Legislative Alerts.

Health Republic Insurance of New York, a new not-for-profit Consumer Operated and Oriented Plan (CO-OP) offering health insurance coverage in New York State, New jersey and Oregon. In NYS Health Republic Insurance is offering new competitive options for individuals and small businesses both on and off the New York State of Health Benefit Exchange. In partnership with MagnaCare, its network comprises more than 70,000 providers in 32 counties, including New York City, Long Island, the Hudson Valley, the Capital District, parts of North County, Syracuse, and parts of Western New York.

Health Republic Insurance is now offering three health insurance plans on the Exchange: EssentialCare (the New York State mandated “standard plan”), PrimarySelect (an alternative plan where members can access better outpatient benefits when they select a primary care physician), and PrimarySelect EPO (a plan similar to PrimarySelect, but members must choose their primary physician from a menu of primary care medical homes).

Breaking News President Announces Cancelled Policies Fix

Yesterday, the President announced that people with health care coverage that is not Affordable Care Act (ACA)-compliant may be able to keep their plans in 2014. Effectively “Grandfathering” of plans purchased after the original law has passed in 2010 There has been a great deal of concern being reported in the national media around the prospect of millions of people losing their health insurance coverage effective January 1, 2014 because of the Patient Protection and Affordable Care Act (“PPACA” aka “ObamaCare”).

We are awaiting how specifically your State’s Insurance Commissioner will react to this. Questions remain about how this new policy will work, including how insurance commissioners will react, whether insurance companies will choose to continue these policies, what the rates for the policies will be, and whether this grandfathering will extend past 2014.

To be clear, what’s being reported principally has to do with the individual health insurance market in the US which insures approximately 15 million people, or about 5% of the country’s population. Within that segment of the privately insured market, a large percentage, certainly more than half, of individual policies are not considered to be “grandfathered” under the law’s requirements for such status. As a result, to be in compliance with the law’s new mandates and coverage requirements, virtually all “non-grandfathered” policies are scheduled to be terminated January 1st, and it will be up to individuals to replace their existing coverage with new compliant policies after this date.

These recent developments have resulted in

1) President Obama issuing an apology to affected individuals on November 7th.

2) the President’s announcement earlier yesterday during a hastily called press conference at the White House that pursuant to an Executive Order, Americans may keep individual health insurance policies they were told will be canceled because these policies failed to meet requirements established by the new law.

President Obama has left it up to the states to independently determine how they will go about implementing this change which is being characterized as an “administrative fix”. However, since the insurance business is state-regulated, each state will need to determine whether or not they will implement this change, and if they choose to implement it, they will have control over defining some of the specific parameters. Insurance companies will also need to quickly make decisions on how to accommodate this new provision if the change is adapted in a state in which they operate.

In closing, if you should have any further questions or comments about the above or the attached, please let us know.We will continue to monitor this issue and all ACA implementation in an effort to keep you informed of new developments. In the meantime, please visit our https://360peo.com/about-us/blog to view past blogs and Legislative Alerts.

Why are my rates going up? The recent 2014 health insurance rates ranging in 15-20% increase is having a profound impact especially on small businesses. Benefits are furthermore deteriorating with new deductibles adding a 10% to the out of pocket costs for a net total 25-30% rate increase.

No pre-existing condition. Several new cost contributors aside from Essential Health Benefits Mandate are assigned. Recent articles such as Kaiser’s Popular Provision Of Obamacare Is Fueling Sticker Shock For Some Consumers attributes new Pre-Existing condition waiver as a factor. Starting Jan 1, 2014 anyone with or without prior health insurance can get immediate treatment without a 12 month waiting period. “But the provision also adds costs. To a larger degree than other requirements of the law, it is fueling the “sticker shock” now being voiced by some consumers about premiums for new policies, say industry experts.” With the guaranteed issue there are unknown costs that cannot be accounted for just yet. Example: An uninsured individual we know is delaying needed surgeries until January for this reason. The member will pay a $250/month premium and get a $40,000 surgery paid for immediately. How many young healthy members are needed to offset this cost?

Transitional reinsurance fee. This is paid by fully insured and self-funded plans. The goal of the fee is to stabilize the individual markets by reimbursing companies who insure a disproportionately large number of individuals who are high utilizers of health care services. Fees will be collected between 2014, 2015, and 2016.

Health insurance providers’ fee, also referred to as a health insurance tax, annual fee, and insurer fee. This will be assessed annually beginning in 2014 on health insurance carriers. The total amount to be collected in 2014 is $8 billion. The tax is based on premiums and by some estimates is expected to have a cost impact of 2 to 2.5 percent in 2014, and higher in subsequent years.

Exchange fee. For 2014, our state’s online exchange marketplace is funded through federal start-up grants. But states that run their own exchange, such as Washington, have been tasked with implementing a funding mechanism after 2014. In the session that ended in June, the Washington State Legislature approved a funding plan for our exchange that authorizes the use of a current insurance premium tax for the qualified health plans (QHPs) sold in the exchange and, if necessary, an additional assessment on carriers who sell QHPs through the exchange.

Patient-Centered Outcome Research Institute (PCORI) fee (also known as comparative-effectiveness fee). Health insurance issuers and sponsors of self-funded group health plans will be assessed this annual fee beginning in 2012 and ending in 2019. It funds patient-centered outcomes research. PCORI is a nonprofit corporation whose mission is to help people make informed health care decisions, and improve health care delivery and outcomes. The Group Health Research Institute has received two research awards from PCORI to study ways to improve care for back pain, and connect patients with community resources.

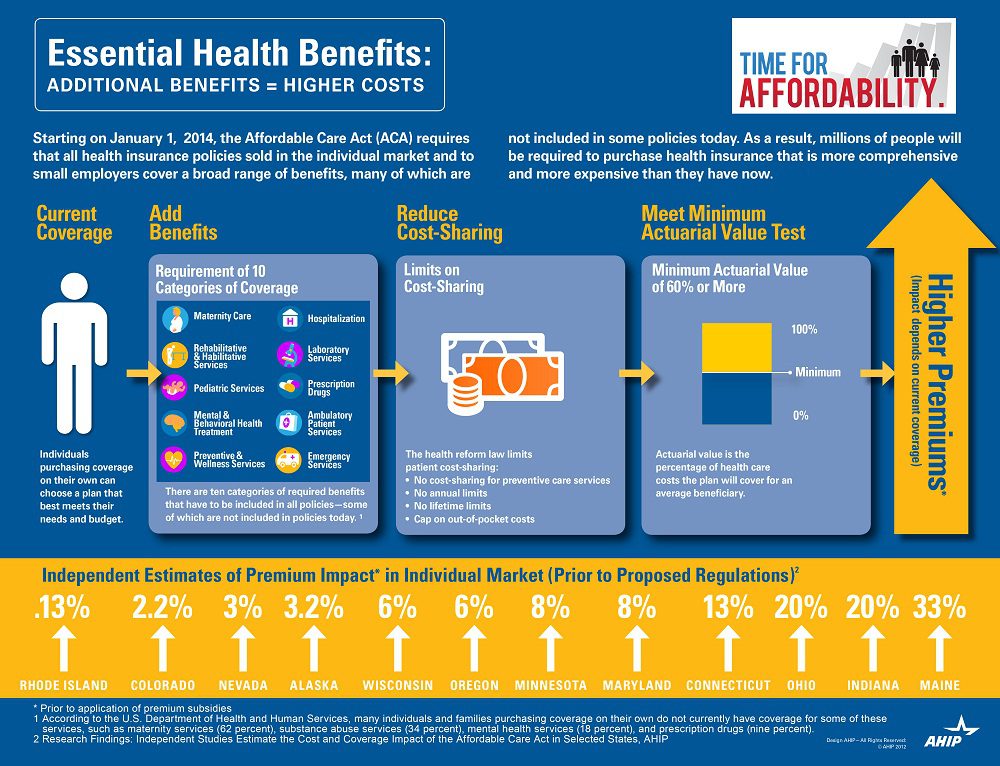

Essential Health benefits. The quintessential question asked is why are my rates going up so much this year has multiple answers with new Essential Health Benefits leading the way. The Essential Health Benefits Not Delayedarticle explains that The Affordable Care Act mandates that the plans include ten essential benefits, from care for pregnant mothers to substance abuse treatment. Popular local plans such as Healthy NY and Brooklyn Healthworks have afforded coverage for over a decade are are missing Mental Health, Chiropractic, and have a $3,000 Rx limit. All Individual Healthy NY and Sole Proprietors are terminating this year . Existing small businesses must buy the full version with Essential Health Benefits.

CASE: A Healthy Ny client just had an increase for singles from $412 to $519. She is a successful generous Caterer who is covering majority of a staff of 10 employees which is unusual for that industry. Her staff had an affordable benefits as well. They loved paying only $20, her Rx copay was only $10/generic and $20/brand for providers she did not have any deductibles. Hospitalization had full coverage with a modest copay. Statistically nearly 90% do not use more than $3,000 Rx. her new plan rolls automatically into the GOLD PLAN increasing her premium 25% along with a new $600 deductible on all benefits and a $40 copay for Specialist. She asked me I thought the new tax was only .9% medicare tax but evidently this IS HER NEW TAX.

So much for if you like your plan you can keep it promise. Even supporters such as Former President ClintonWeighs in on Obamacare. “Obama should honor his health-care promise: Pres. Clinton”, He personally believes President Barack Obama should honor his promise that people who have and like their insurance can keep it.

Do not under estimate the power of the Bill. The President is reviewing ways to allow some to keep their health plan but this would only apply to policyholders losing coverage. Stay tuned.

You can download the complete Essential Health Benefits NYS. Also, for a downloadable guide on self-insuring and secondary market reinsurance for your group please send contact form below. In the meantime, please visit to view past blogs and Legislative Alerts at https://360peo.com/feed.

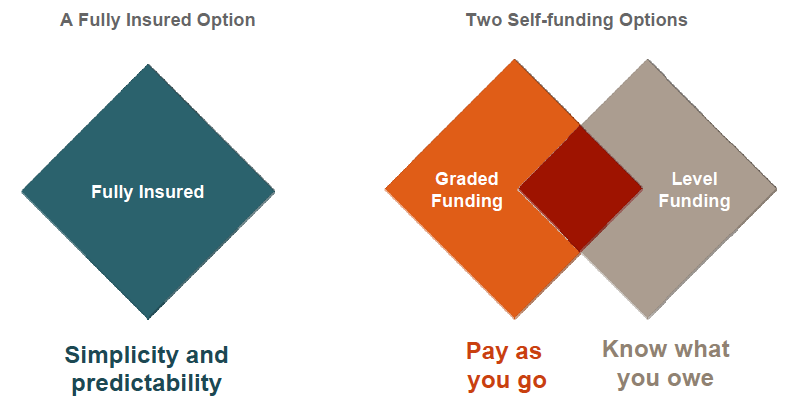

Most employers search for methods of lowering their company’s spending on their health benefit plans. A Self Funded, or Self-Insured plan, is one in which the employer assumes the financial risk for providing health care benefits to its employees. In practical terms, Self-Insured employers pay for claims out-of-pocket as they are presented instead of paying a pre-determined premium to an insurance carrier for a Fully Insured plan. Typically, a self-insured employer will set up a special trust fund to earmark money (corporate and employee contributions) to pay incurred claims.

In a self-funded — also known as self-insured — health plan, the employer takes on direct financial responsibility for employees’ health care costs. Rather than being part of a larger risk pool, an employer that self-funds takes on the risk for its employee group alone. All of a health plan may be self-funded, or an insurance contract might be purchased to cover certain types of claims. Most self-funded employers buy stop-loss insurance to cover catastrophic claims

Being exempt from state insurance laws and mandates and not having to pay premiums on a regular basis to an insurance company can result in substantial cost savings. Yet, many employers, especially smaller employers, shy away from self-funding, perceiving it as too risky.

According to a Kaiser Family Foundation Health Benefits Survey, about 55 percent of all employees covered for health care are in self-funded plans. Among employers with 200 or more workers, 77 percent of employees are in self-funded health plans, compared to 12 percent of employees in firms with 3–199 workers.

What is a TPA?

A third party administrator (TPA) is an entity that processes or adjudicates claims for an employee benefit plan. A TPA may provide additional services to an employee benefit plan or employer, such as collecting premiums, contracting for PPO services, providing utilization review of claims, and similar ancillary services to the operation of the employee benefit plan. Self-insured employers can either administer the claims in-house, or subcontract this service to a TPA.

Why do employers self fund their health plans?

There are several reasons why employers choose the self-insurance option. The following are the most common reasons:

The employer can customize the plan to meet the specific health care needs of its workforce, as opposed to purchasing a ‘one-size-fits-all’ insurance policy.

The employer maintains control over the health plan reserves, enabling maximization of interest income – income that would be otherwise generated by an insurance carrier through the investment of premium dollars.

The employer does not have to pre-pay for coverage, thereby providing for improved cash flow.

The employer is not subject to conflicting state health insurance regulations/benefit mandates, as self-insured health plans are regulated under federal law (ERISA).

The employer is not subject to state health insurance premium taxes, which are generally 2-3 percent of the premium’s dollar value.

The employer is free to contract with the providers or provider network best suited to meet the health care needs of its employees.

Is self-insurance the best option for every employer?

No. Since a self-insured employer assumes the risk for paying the health care claim costs for its employees, it must have the financial resources (cash flow) to meet this obligation, which can be unpredictable. Therefore, small employers and other employers with poor cash flow may find that self-insurance is not a viable option. It should be noted, however, that there are companies with as few as 25 employees that do maintain viable self-insured health plans.

Can self-insured employers protect themselves against unpredicted or catastrophic claims?

Yes. While the largest employers have sufficient financial reserves to cover virtually any amount of health care costs, most self-insured employers purchase what is known as stop-loss insurance to reimburse them for claims above a specified dollar level.

With what laws must self-insured group health plans comply?

Self-insured group health plans come under all applicable federal laws, including the Employee Retirement Income Security Act (ERISA), Health Insurance Portability and Accountability Act (HIPAA), Consolidated Omnibus Budget Reconciliation Act (COBRA), the Americans with Disabilities Act (ADA), the Pregnancy Discrimination Act, the Age Discrimination in Employment Act, the Civil Rights Act, and various budget reconciliation acts such as Tax Equity and Fiscal Responsibility Act (TEFRA), Deficit Reduction Act (DEFRA), and Economic Recovery Tax Act (ERTA).

How can your organization benefit from self insurance or level funding? Are there Self-Insurance advantages of avoiding Essential Health Benefits and using the lower cost Minimum Actuarial Value in Health Care Reform?

For additional information on self-funding please contact us at 1-855-667-4621 or e-mail us at info@medicalsolutionscorp.com.

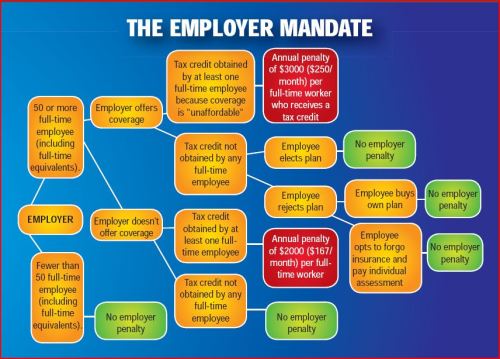

In an unexpected announcement pre-July 4th the big news was Obamacare Employer Mandate Delayed with penalties under the Affordable Care Act (ACA) until 2015. The mandate also known as the “Employer Shared Responsibility” requires employers with 50 or more FTEs to offer affordable health insurance coverage to their workers or face financial penalties for not doing so. Those penalties would originally have been applied beginning in 2014.

There has been a follow up guidance issued last week July 9th by the IRS. According to the IRS, the delay will give employers more time to prepare for the change in how health insurance is provided and will also give the Obama Administration time to simplify the insurance-related reporting requirements that employers face. This transition relief appears to come with “no strings attached.” Although the IRS guidance encourages employers to voluntarily comply with the employer mandate and maintain or expand health care coverage in 2014, the IRS will not impose penalties for a failure to do so.

Although the IRS guidance encourages employers to voluntarily comply with the employer mandate and maintain or expand health care coverage in 2014, the IRS will not impose penalties for a failure to do so.Notably, the guidance issued on July 9th also does not require employers to make “good faith” efforts to comply. As a result of this transition year, employers will have the option of deciding to what extent (if any) they will continue efforts to comply with the employer mandate during 2014.

Employers who intended to rely on one of the transition rules previously announced for 2014 should keep in mind that the latest IRS guidance does not provide special transition rules for 2015. Other group health plan requuirements still apply as discussed in our prior blog Essential Health Benefits Not Delayed.

This means that for plan years beginning on and after January 1, 2014, all group health plans must:

Eliminate all pre-existing condition exclusions (regardless of age);

Maximum Cost Sharing Deductible to $2,000/individual ($4,000/family); limit in-network out-of-pocket maximums to $6,350/individual ($12,700/family)

Individual Mandate Still Applies. individuals will still be required to obtain health care coverage or pay a penalty for each month they do not have coverage, beginning January 1, 2014

Exchanges (Marketplaces) Open for Enrollment October 1, 2013.

The IRS notice makes it clear that individuals who enroll in coverage on the marketplaces will continue to be eligible for a premium tax credit if their household income is within a specified range and they are not eligible for other minimum essential coverage.

Employers Must Send Notice of Exchanges (Marketplaces) Before October 1, 2013. These notices must be sent to current employees by October 1, 2013. Then, beginning October 1, 2013, employers must send this notice to new hires within 14 days of their start date.

New taxes still apply – Patient Centered Outcomes Research Institute (PCORI) excise taxes and transitional reinsurance program fees;HRA/HSA/FSA clients also pay a monthly $1/employee tax.

We will continue to monitor ACA developments and will provide you relevant updated information when available. In the meantime, please visit to view past blogs and Legislative Alerts at https://360peo.com/feed.

The pre-July 4th news of Obamacare Employer Mandate Delayed until 2015 decision may have started early fireworks. The administration did not, however, delay the larger new requirements facing employers who choose to offer health insurance in the small group market––employers with less than 50 workers. The biggest requirement – Essential Health Benefits not delayed.

Whether the rationale was to alleviate business pressure to meet new mandates by Jan 2014 or the real fear that Employers have already begun making necessary employment hours cut backs to avoid the $2,000 penalty. A $3,000/employee penalty was also looming for Employers offering unaffordable insurance.

Keep in mind that this limited delay does not affect other provisions of the Affordable Care Act slated to go into effect in or before 2014, such as:

Individual mandate which requires most individuals to purchase insurance by January 1, 2014, or pay a tax penalty.

a 90-day maximum on eligibility waiting periods;

monetary caps on annual out-of-pocket maximums;

total elimination of lifetime and annual limits (including expiration of waivers that permitted certain “mini-med” plans and stand-alone Health Reimbursement Arrangements to stay in place through plan years beginning in 2013);

Patient Centered Outcomes Research Institute (PCORI) excise taxes and transitional reinsurance program fees; HRA/HSA/FSA clients also pay a monthly $1/employee tax.

a notice informing employees of the availability of the new health insurance Exchanges (a model notice is available on the U. S. Department of Labor website); and insurance market reforms.

The biggest impact is the Essential Health Benefits (EHB) which will not be delayed and this affects fully insured or ALL Small Businesses. While small employers are not required to offer coverage, if they do then they come under that large number of new essential health benefit mandates and group rating rules that won’t apply to large employers. These small group requirements are expected to increase the cost of small group coverage by an average of 15%––with wide variation by state and the average age of the group.

An employer sponsoring a Healthy NY or Brooklyn Healthworks Plan today for example would be disqualified as this does not carry all Essential Health Benefits. The very popular Healthy NY is slated to shut down for Jan 2014 and most Employers have just received this transition letter last week. Individual and Sole Prop Healthy NY is terminating and small business Healthy NY must be reapplied under a new higher cost version. While the plan did not carry Ambulance and had a $3,000 limited Pharmacy plan it is priced 35% below market and did manage to capture hundreds of thousands that would otherwise had been uninsured. The same is true for those on Hospital Only or high deductible catastrophic plans.

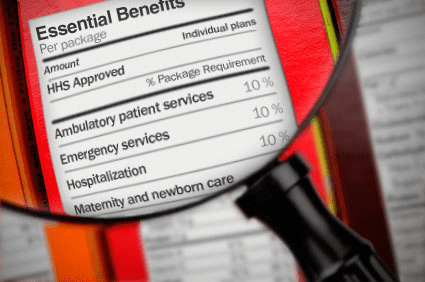

So what are these Essential Health Benefits?

All individual and small group policies on and off-Exchangemust cover ten categories of minimum essential health benefits.

Under the ACA, each state must choose one plan from among popular health insurance plans offered statewide to serve as a benchmark for EHBs. The benchmark plan will act as the model for how plans must define and include EHBs in their coverage — in both the individual and small group markets. New York selected the benefits of the State’s largest small group plan as its EHB benchmark. There is also a Minimum Value requirement, See NYS Minimum Value STANDARD BENEFIT DESIGN COST SHARING DESCRIPTION CHART (5-6-2013) Some of the plan’s components include:

No cost-sharing for routine preventive services

Pediatric dental and vision coverage

Habilitative and rehabilitative services, including physical therapy, speech therapy and occupational therapy

Rich mental/behavioral health services

No annual or lifetime dollar limits on benefits

Conversely, a shift to self- insurance is underway as self-insureds can avoid many taxes and instead ONLY cover the Minimum Essential Coverage which is different than the Essential Health Benefits. The strategy coupled with reinsurance is a great sophisticated model usually reserved for larger groups. This segment will be able to avoid local additional State mandates which in States like NY account for 14-16%% of the costs. Thats a total swing of 30% for a fully insured NY group. Also, self-insured groups do NOT pay added taxes such as the health insurance tax of $9 Billion annually over the next 10 years.

The administration has shown their sensitivity to larger groups. This segment already covers 94% of its employees at least in some fashion while small businesses cover less than 50%.

Why not do the same for small employers as well? And while they are at it, use the time to reconsider the impact many of these regulations are likely to have on the number of small employers continuing to offer coverage.

For a downloadable guide on self-insuring and secondary market reinsurance for your group please send contact form below. In the meantime, please visit to view past blogs and Legislative Alerts at https://360peo.com/feed.

With only 6 month away from full implementation of 2014 Patient Protection Affordability Care Act (PPACA) employers are understandably uncertain. Below are Health Care reform – five things employers can do now to prepare and take action.

UPDATE JULY 2nd: Since blog posting the President Administration has delayed 1 year Employed Shared Responsibility Mandate i.e. Pay or Play to Jan 2015.

1. Employee Communications

Employers must notify employees of the online insurance marketplace known as a Healthcare Exchange. Recently released federal guidelines require employers to notify their workers of eligibility requirements for their state exchange starting Oct. 1, 2013 Open Enrollments for Jan 2014 effective date. To the relief of many, the U.S. Labor Department also provided model notices that employers can give to their workers, which eliminates the need to develop their own notifications.

Additionally, Employers sponsoring a health plan must give employees a Summary of Benefits and Coverage (SBC). The purpose of the Summary of Benefits and Coverage, or SBC, is to present benefits and coverage information in clear language and in a consistent format. Inspired by the Nutrition Facts Label on packaged food, theSBC (pdf) includes two medical scenarios: having a baby and managing Type II diabetes. It estimates how much a patient would pay for medical care in each scenario with specific insurance plans.

It’s the employer’s responsibility to distribute the SBCs to employees.

This requirement applies to health plan renewals after Sept. 23, 2012.

Department of Labor will NOT impose penalties for non-compliance with the SBC notice during the first year as long as employers show a “good faith” effort to comply. Read the FAQ on SBC and ACA pdf here.

2. Determining which Employers must offer health care.

Because employers with 50 full-time equivalents face penalties for not providing affordable, minimum value insurance an employer should know whether it is subject to these requirements or not. Common law employees of the employer and any commonly controlled company must be counted. Employers with temporary or leased employees will want to discuss with their advisors whether these employees will be considered “common law employees” for purposes of determining how many FTEs an employer has. Employers with employees who are paid based on unique payment models (stipends, work product, etc) will want to discuss how to calculate these employee hours with their benefits advisors.

Employers with 50 or more employees will incur penalties of up to $2,000 per employee if they cancel their existing health care program (which up until 2014 would be considered an optional benefit to provide). They will also incur penalties if their plan is too costly, and they do not meet the affordability standards.

Employers with less than 50 employees will not incur penalties if they cancel their health care plan, and that decision will need to be made on a business by business basis. They can also choose to offer partial coverage and contribute up to the minimum 50% of single coverage not to exceed 9.5% employee

The good news is Employers can subtract 30 FT employees. This portion is known as the Employer “play or pay” option. Specific case example and details are found at Pay or Play Employer Guide.

To encourage businesses to offer health benefits to their employees, the federal government is offering tax credits to small businesses. These credits are available to an estimated 4 million small businesses, including nonprofits.The IRS has set up a web page with information: Small Business Health Care Tax Credit for Small Employers. The maximum “credit” (which offsets taxes dollar for dollar and is better than a “deduction” which reduces taxable income) is 35 percent of the amount an employer pays towards employee health insurance.

Who’s eligible?

To qualify, small employers must:

Have fewer than the equivalent of 25 full-time workers

Pay average annual wages below $50,000

Cover at least 50% of the cost of health care coverage for their workers

Because of the high wages paid in most industries in NY/NJ/CT Tri State, few small employers that provide coverage pay such a low average wage. Note, however, that the calculation of average wages and number of employees excludes the wages of an owner and his or her family members.

medicalsolutionscorp.com help clients gather the appropriate information and do a preliminary estimate of the credit amount. This information will help you and your accountant determine whether applying for the credit makes financial sense. Find out what the new tax credit could mean for your coverage. Call us at 855-667-4621.

4. Determine affordability

Beginning Jan. 1, 2014, an employer with 50 or more employees must pay a tax penalty if they either: a) Do not provide health insurance with minimum benefits or 60 percent of healthcare expenses; b) Require employees to contribute more than 9.5 percent of an employee’s household income for the health insurance and those employees obtain a government subsidy for coverage.

Companies will be required to pay $3,000 per employee without affordable coverage. (Note: there are a number of caveats that might affect the actual penalty paid, so consult your tax advisor.)

It is crucial to Understand the difference between FT and Full Time Equivalent. To determine the FTE (Full Time Equivalent) you must count FT and PT employees. Full Time Employees are those working 30 hours+/week.* The number of full-time employees excludes those full-time seasonal employees who work for less than 120 days during the year.4 The hours worked by part-time employees (i.e., those working less than 30 hours per week) are included in the calculation of a large employer, on a monthly basis, by taking their total number of monthly hours worked divided by 120.

For example, a firm has 35 full-time employees (30+ hours). In addition, the firm has 20 part time employees who all work 24 hours per week (96 hours per month). These part-time employees’ hours would be treated as equivalent to 16 full-time employees, based on the following calculation:

20 employees x 96 hours / 120 = 1920 / 120 = 16

Thus, in this example, the firm would be considered a “large employer,” based on a total full-time equivalent count of 51—that is, 35 full-time employees plus 16 full-time equivalents based on part-time hours.

In the coming months, Millennium Medical Solutions Inc will host seminars and will share information you’ll need to know as the countdown continues to October 1st.

Error: Contact form not found.

This blog is not intended to represent legal advise and one should consult with a tax and/or legal expert.

* IRC 4980H(c)(4)

Disclaimer: This blog is not intended to represent legal advise and one should consult with a tax and/or legal expert.

In Time magazine’s March issue Bitter Pill: Why Medical Bills Are Killing Us Steven Brill gets to work on answering the ever elusive Why are Medical Costs So High? The 21,000 word article is longest article in Time Magazine history that can boiled down to simply there is no free marketplace in health care. We think everything in this country is a free market but is there a free market when one needs to got to an emergency room or a free market when one must take a cancer pill? According to Howard Dean the singular reason is to get away form the current fee for service system where providers get paid per procedure and not per patient.

Here’s an eye opener: “Insurance Companies are not really the problem they run pretty terribly. They process claims, a lot of us think they process claims and fairly consistently but they are increasingly at the mercy of hospitals which are consolidating buying a doctors practices. We should tax profits on so-called nonprofit hospitals and put that money back into the system. We should control all the prices for prescription drugs because if I have a monopoly a cancer wonder drug I can charge anything I want for them that’s obviously not a free market and it’s completely two different uses you see this article once you follow the money.”

Transcript of the video:

“This is not a free-market. You don’t get health care because you want it. You don’t wake up in the morning and gee I love to go down to the emergency room today. You enter that market and will you know nothing about the products of you being asked by no choice of those products. Hi I am Steve Brill I’ve got the cover story this week in TIME Magazine looking at the health care debate from a very different perspective. Everybody focuses on who should pay for the exorbitant cost of health care and that I decided to do was ask for more fundamental question which is why does health care cost so much.

I look behind the bills and trace the bills all the way back to who’s getting what money is making what profits and the results are really surprised one of the things I found that everybody in the healthcare industry knows about that that nobody else knows his something called the charge-master. The charge master is a internal listing each hospital of the thousands of different items that they charge and nobody could explain it to me. Indeed would be hard to explain for example why would you charge $77 for a box of gauze pads? You can buy for a dollar at the drugstore. why would you charge thousands of dollars for CAT scan it really isn’t cost you anything?

It’s emblematic if you will, of the irrationality of the higher healthcare system because no one can explain the cost no one tries to and the only people who are guaranteed surefire to pay to be asked to pay the charge-master prices are the poorest people who don’t have health insurance.

Real profit makers are way hospitals markup very expensive drugs that you get. If you have cancer to have pneumonia but they’re making thousands of dollars on these drugs and drug companies in turn making still more thousands of dollars.

Obamacare does very little to solve any of these problems and just probably why you got to Congress I’m it doesn’t do anything to control the prices of prescription drugs or medical devices CAT scan. In fact if anything it will increase the profitable the players in the market by making equal insurance and therefore more people are in the marketplace with the funds from insurance companies to buy all these products.

Insurance Companies are not really the problem they run pretty terribly. They process claims, a lot of us think they process claims and fairly consistently but they are increasingly at the mercy of hospitals which are consolidating buying a doctors practices. See Provider Consolidation Info-graph– “The proliferation of hospital mergers and hospitals’ appetite for buying doctors’ practices—in part to assure a steady stream of patients to fill hospital beds—could create local monopolies that raise prices without increasing efficiency. ‘Historically,’ says Deloitte’s Mr. Keckley, ‘hospital consolidation hasn’t reduced costs.’”

We should tax profits on so-called nonprofit hospitals and put that money back into the system. We should control all the prices for prescription drugs because if I have a monopoly a cancer wonder drug I can charge anything I want for them that’s obviously not a free market and it’s completely two different uses you see this article once you follow the money.”

The ACO (Accountable Care Organization) referenced in our post NYU Beth Israel Merger and ACOs are models encouraged in Obamacare in fact as examples of Provider capitated reimbursement that Howard Dean is in favor of. An ACOI cordiantes patient care and provide the full range of health care services for patients. The health reform law provides incentives for providers who join together to form such organizations and who agree to be accountable for the quality, cost, and overall care of Medicarebeneficiaries who are enrolled in the traditional fee-for-service program who are assigned to the ACO.

The fee-for-service system has evidentially driven costs by incentivizing volumes of added procedures. The ACO model is built on par excellence hospitals such as Mayo Clinic where there is team of providers are financially incentivized for patient care coordination outcomes and high quality of care. The ACO’s payment would be tied to achieving goals that improve health care and save money. Members of the ACO would divvy up that payment. Today’s payment system, investments in providing better care are doubly penalized. If a hospital hires a nurse to follow up with patients after they are discharged in order to reduce readmissions — for example, to help patients with diabetes improve blood sugar control — it must pay for the nurse, which is typically not reimbursed by insurance companies or Medicare, and it loses revenue by preventing the readmission.

Congress included ACOs in the health care law as a way to rein in Medicare spending. That federal program pays for health care for people 65 and older and the disabled. The federal government estimates ACOs could save the Medicare program up to $940 million over four years. Medicare recently began testing this system with 32 pilot ACOs in 18 states, including one in the New York City area – Bronx Accountable Healthcare Network.

Some have pointed to ACO Model just as a pro-merger supporting argument with the FTC. These significant mergers create market dominance and therefore limit competition and drive up health care dollars. And yet Hospitals operate on thin profit margins and cannot afford to lose market share therein lies is the conundrum.

Note: At time of this article MVP and Hudson Valley Health Plans announced a merger –Hudson Health Plans joins MVP. Hudson Health Plan, the Medicaid managed care organization based in Tarrytown, will join the MVP Health Care group of companies, the two nonprofit health plans jointly announced today.

“Size and diversity of offerings are important for health plans in the new world of the health insurance marketplaces. A 55-year-old person would like to join a health plan that can continue to cover him when he turns 65. Likewise, if someone is no longer eligible for Medicaid, she might prefer to buy a commercial product from that same insurer. Together, MVP and Hudson now can cover people through all of life’s stages and changing needs.

In the coming months, Millennium Medical Solutions Inc will host seminars and will share information you’ll need to know as the countdown continues to October 1st. Please contact us for immediate information on how to implement these initiatives for your group-specific needs at info@medicalsolutionscorp.com or Call (855) 667-4621.

In a self-funded — also known as self-insured — health plan, the employer takes on direct financial responsibility for employees’ health care costs. Rather than being part of a larger risk pool, an employer that self-funds takes on the risk for its employee group alone. All of a health plan may be self-funded, or an insurance contract might be purchased to cover certain types of claims. Most self-funded employers buy stop-loss insurance to cover catastrophic claims

In a self-funded — also known as self-insured — health plan, the employer takes on direct financial responsibility for employees’ health care costs. Rather than being part of a larger risk pool, an employer that self-funds takes on the risk for its employee group alone. All of a health plan may be self-funded, or an insurance contract might be purchased to cover certain types of claims. Most self-funded employers buy stop-loss insurance to cover catastrophic claims