Why are my rates going up? The recent 2014 health insurance rates ranging in 15-20% increase is having a profound impact especially on small businesses. Benefits are furthermore deteriorating with new deductibles adding a 10% to the out of pocket costs for a net total 25-30% rate increase.

No pre-existing condition. Several new cost contributors aside from Essential Health Benefits Mandate are assigned. Recent articles such as Kaiser’s Popular Provision Of Obamacare Is Fueling Sticker Shock For Some Consumers attributes new Pre-Existing condition waiver as a factor. Starting Jan 1, 2014 anyone with or without prior health insurance can get immediate treatment without a 12 month waiting period. “But the provision also adds costs. To a larger degree than other requirements of the law, it is fueling the “sticker shock” now being voiced by some consumers about premiums for new policies, say industry experts.” With the guaranteed issue there are unknown costs that cannot be accounted for just yet. Example: An uninsured individual we know is delaying needed surgeries until January for this reason. The member will pay a $250/month premium and get a $40,000 surgery paid for immediately. How many young healthy members are needed to offset this cost?

Transitional reinsurance fee. This is paid by fully insured and self-funded plans. The goal of the fee is to stabilize the individual markets by reimbursing companies who insure a disproportionately large number of individuals who are high utilizers of health care services. Fees will be collected between 2014, 2015, and 2016.

Health insurance providers’ fee, also referred to as a health insurance tax, annual fee, and insurer fee. This will be assessed annually beginning in 2014 on health insurance carriers. The total amount to be collected in 2014 is $8 billion. The tax is based on premiums and by some estimates is expected to have a cost impact of 2 to 2.5 percent in 2014, and higher in subsequent years.

Exchange fee. For 2014, our state’s online exchange marketplace is funded through federal start-up grants. But states that run their own exchange, such as Washington, have been tasked with implementing a funding mechanism after 2014. In the session that ended in June, the Washington State Legislature approved a funding plan for our exchange that authorizes the use of a current insurance premium tax for the qualified health plans (QHPs) sold in the exchange and, if necessary, an additional assessment on carriers who sell QHPs through the exchange.

Patient-Centered Outcome Research Institute (PCORI) fee (also known as comparative-effectiveness fee). Health insurance issuers and sponsors of self-funded group health plans will be assessed this annual fee beginning in 2012 and ending in 2019. It funds patient-centered outcomes research. PCORI is a nonprofit corporation whose mission is to help people make informed health care decisions, and improve health care delivery and outcomes. The Group Health Research Institute has received two research awards from PCORI to study ways to improve care for back pain, and connect patients with community resources.

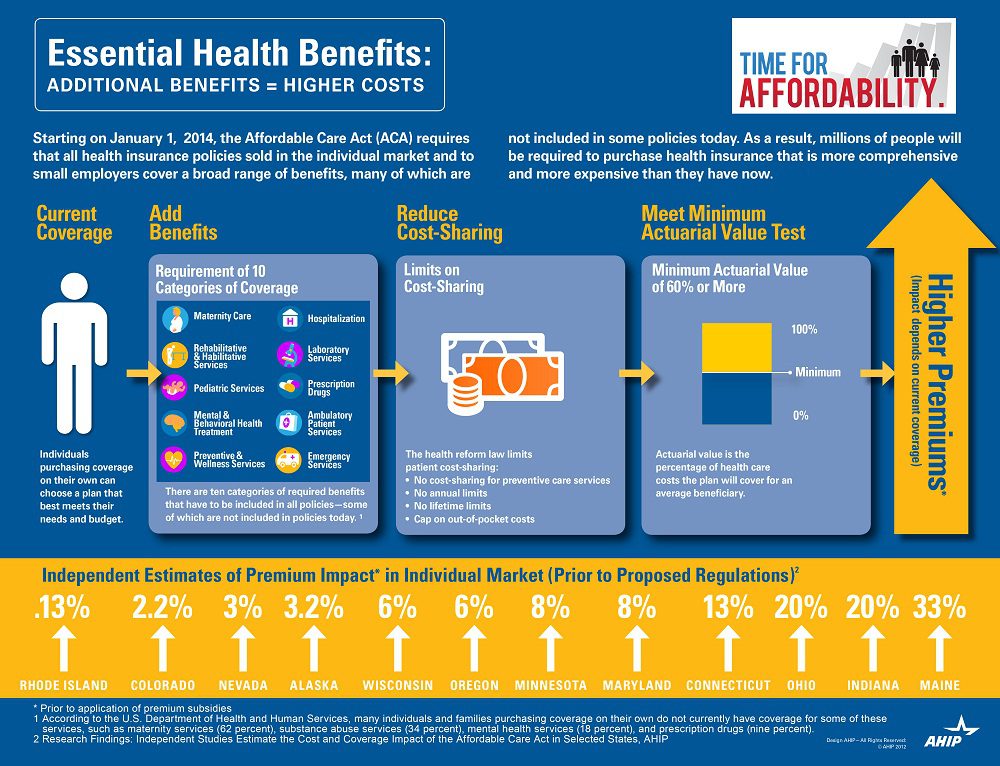

Essential Health benefits. The quintessential question asked is why are my rates going up so much this year has multiple answers with new Essential Health Benefits leading the way. The Essential Health Benefits Not Delayedarticle explains that The Affordable Care Act mandates that the plans include ten essential benefits, from care for pregnant mothers to substance abuse treatment. Popular local plans such as Healthy NY and Brooklyn Healthworks have afforded coverage for over a decade are are missing Mental Health, Chiropractic, and have a $3,000 Rx limit. All Individual Healthy NY and Sole Proprietors are terminating this year . Existing small businesses must buy the full version with Essential Health Benefits.

CASE: A Healthy Ny client just had an increase for singles from $412 to $519. She is a successful generous Caterer who is covering majority of a staff of 10 employees which is unusual for that industry. Her staff had an affordable benefits as well. They loved paying only $20, her Rx copay was only $10/generic and $20/brand for providers she did not have any deductibles. Hospitalization had full coverage with a modest copay. Statistically nearly 90% do not use more than $3,000 Rx. her new plan rolls automatically into the GOLD PLAN increasing her premium 25% along with a new $600 deductible on all benefits and a $40 copay for Specialist. She asked me I thought the new tax was only .9% medicare tax but evidently this IS HER NEW TAX.

So much for if you like your plan you can keep it promise. Even supporters such as Former President ClintonWeighs in on Obamacare. “Obama should honor his health-care promise: Pres. Clinton”, He personally believes President Barack Obama should honor his promise that people who have and like their insurance can keep it.

Do not under estimate the power of the Bill. The President is reviewing ways to allow some to keep their health plan but this would only apply to policyholders losing coverage. Stay tuned.

You can download the complete Essential Health Benefits NYS. Also, for a downloadable guide on self-insuring and secondary market reinsurance for your group please send contact form below. In the meantime, please visit to view past blogs and Legislative Alerts at https://360peo.com/feed.

The Health Exchange also known as The Health Marketplace or Obamacare Exchanges are set to open in less than 12 hours. Are you ready or aye you like most asking What is an Exchange? Starting Oct 1 you can enroll until March 31, 2014, though you’ll generally need to sign up by Dec. 15 of this year, to be covered as of Jan. 1. You can find your state’s marketplace at healthcare.gov. The prices for the marketplace plans are likely to be similar to those sold privately. A plan that is also available on the exchange may be eligible for subsidies. Heres an easy top 10 list of what you need to know.

10. Locate your State Exchange

Look up your state’s exchange here and Healthcare.gov. Some states are running their own exchange, others are running it through the federal government see www.healthcare.gov. For NY Tri-State the sites are:

NYS – http://info.nystateofhealth.ny.gov See rates here

CT – https://www.accesshealthct.com See rates here

9. Individual Mandate Penalty

For 2014, the annual penalty is $95 or 1% of your income, whichever is greater. The penalty will increase over the first three years. Coverage can include employer-provided insurance, individual health insurance, Medicare or Medicaid.

Health Insurance Individual Penalty for Not Having Insurance Pay the greater of the two amounts

Year

Percentage of Income

Set Dollar Amount

2014

1%

$95 & $285/family max

2015

2%

$325 & $975/family max

2016

2.5%

$695 & $2,085/family max

8. Individual Subsidies

Individuals who do not have affordable minimum essential coverage from their employer will be eligible for tax credit subsidies for their health insurance purchase on a state exchange if their income is below 400 percent of federal poverty level.

If you make under $45,960 or your family makes under $94,200, you could get a real break on health insurance costs More low-income people will also be eligible for free coverage under Medicaid For those eligible, the subsidies will cap the amount you pay for your exchange policy at between 2% and 9.5% of your income (on a sliding scale, based on your income). To find out how much you would pay, estimate your income for this year and plug it into any health subsidy calculator. You can also see estimate subsidies with these “health subsidy charts”.

7. Small Business Subsidy – SHOP Exchange

A key change is that the small business health care tax credits will only be available ONLY through the SHOP Exchange marketplace in 2014. Small businesses with 25 or fewer employees who receive less than $50,000 a year in wages may be eligible for tax credits if they purchase the plan through the SHOP marketplace. These credits will cover up to 50% of the employer’s cost (35% for non-profits) for the first two years of coverage. Click here to read more about the small business health care tax credits.

6. Your income

not your assets, such as your house, stocks or retirement accounts – will count toward determining whether you can get tax credits. When you buy your plan, you estimate your income for next year, and your tax credit is based on that estimate. The next year, your tax returns will be checked by the IRS and compared against your estimate.

5. Pre-Existing Conditions Eliminated

Your insurer generally can’t drop you, as long as you keep up with your insurance premiums and don’t lie on your application. Generally, people will be able to enroll in or change plans once a year during the annual open enrollment period. This first year, open enrollment on the exchanges will run for six months, from Oct. 1 through March of next year. But in subsequent years the time period will be shorter, running from October 15 to December 7.

4. Essential Health Benefits Covered

Each plan covers 10 “essential health benefits,” which include prescription drugs, emergency and hospital care, doctor visits, maternity and mental health services, rehabilitation and lab services, among others. In addition, recommended preventive services, such as mammograms, must be covered without any out-of-pocket costs to you. More info here.

3. Ninety-Day Maximum Waiting Period

Group health plans and health insurance issuers may not impose waiting periods of more than ninety days before coverage becomes effective. This also applies to grandfathered plans.

2. Annual or Lifetime Limits

Group health plans, including grandfathered plans, may no longer include more than restricted annual or any lifetime dollar limits on essential health benefits for participants. Limits may exist in and after 2014 for non-essential benefits.

1. Not Everyone is Eligible

Immigrants who are in the country illegally will be barred from buying insurance on the exchanges. However, legal immigrants are permitted to use the marketplaces and may qualify for subsidies if their income is no more than 400 percent of the federal poverty level (about $46,000 for an individual and $94,200 for a family of four).

members of certain religious groups and Native American tribes

incarcerated individuals

people whose incomes are so low they don’t have to file taxes (currently $9,500 for individuals and $19,000 for married couples)

Conclusion:

There has been a lot of news about individual Obamacare provisions getting delayed – Obamacare Employer mandate Delayed. Some people may assume that means the health law is being slowly dismantled, or put off for an additional several years. .The Affordable Care Act is an extremely complicated law with a lot of moving parts, but ultimately, the biggest provisions are still moving forward. There will likely be more hiccups along the way. As the enrollment period opens for Obamacare’s new exchanges, industry experts predict there will probably be other issues that need to be ironed out — but that doesn’t mean the whole law is collapsing

Still confused?

Don’t be. These are the common questions that we are working through with our clients daily. Am I better off going SHOP Exchange vs. Individual for my business? Am I better off going off Exchanges or onto Private Exchanges? Whats my minimum employer contribution? Do I have to cover employee and dependents? Is dental and vision included? What happens to my Healthy NY when it shuts down Jan 1, 2014? What employer notices must I be posting?

Please contact our team at Millennium Medical Solutions Corp if you have additional questions regarding how SHOP Exchanges and Individual Exchanges can benefit you Stay tuned to our site for updates as more information gets released. Sign up for latest news updates.

Health Exchange Notification Due Oct 1 – Employers Must Distribute Required Exchange Notice

If your organization hasn’t done so already, you have until October 1 to inform employees about their option to enroll in a public health exchange under theAffordable Care Act.

Notice Must Be Provided to Current and New Employees. Following a delay in the original effective date, employers will need to comply with the new requirement to provide each employee a written notice with information about a Health Insurance Exchange (also known as a Marketplace) beginning this Fall.

Employers are required to provide the written notice to each current employee not later than October 1, 2013, and to each new employee at the time of hiring (within 14 days of the employee’s start date) beginning October 1, 2013. Two model notices are available from the U.S. Department of Labor:

Model Notice for Employers Who Offer a Health Plan Model Notice for Employers Who Do Not Offer a Health Plan

Employers must provide the notice to each employee regardless of plan enrollment status (if applicable) or of part-time or full-time status. Employers are not required to provide a separate notice to dependents or other individuals who are or may become eligible for coverage under the plan but who are not employees.

The notice may be provided by first-class mail, or, alternatively, it may be provided electronically if certain requirements are met. More information on the notice requirement is available from the U.S. Department of Labor.

IMPORTANT: The model notice contains an optional section about employer-sponsored coverage details. The model notice is three pages long and contains an optional section on page three (questions 13 though 16). An employer is in no way obligated to provide the optional information requested on the model notice. Also, an employer may modify the notice as long as the end result corresponds to the overall basic content guidelines. However, the employer should carefully weigh the value of providing additional information about the cost and value of the employee’s group health plan options.

Technically, the law does not impose any fines for failing to provide the notices. However, the Affordable Care Act is intertwined with other laws (this particular provision is embedded in the FLSA in a new section, 8A), so it is considered a good idea to comply to avoid possible legal complications.

Who Must Receive the Notices?

Notices must be given to all employees, whether or not they work full time, and regardless of whether they are currently receiving health benefits. The October 1 deadline is to give these notices to all employees. After October 1, the notices must be given to new hires within two weeks of coming on board.

The notices must “be provided in writing in a manner calculated to be understood by the average employee,” says the Department of Labor (DOL) in Technical Release 2013-02. They can also be provided via e-mail, but only to employees for whom accessing e-mail is “an “integral part of the employee’s duties” and who can access the system easily.

Which Employers Must Send the Notices?

The notice requirement must be met by employers that must comply with theFair Labor Standards Act (FLSA). In general, the FLSA applies to employers with one or more employees who are engaged in, or produce goods for, interstate commerce. For most firms, a test of not less than $500,000 in annual dollar volume of business applies.

The FLSA also specifically covers the following: hospitals; institutions primarily engaged in the care of the sick, the aged, mentally ill, or disabled who reside on the premises; schools for children who are mentally or physically disabled or gifted; preschools, elementary and secondary schools, and institutions of higher education; as well as federal, state and local government agencies.

Model Notices

The DOL has issued a pair of model notices you can use. One is for employers which currently offer health benefits and another for those which do not. On Part B of the forms, you will see information the employees will need if they plan to purchase coverage on the exchange, assuming they are eligible.

The Part B information would allow employees who apply to their state’s exchange (or the federal version, if no state-run exchange exists) to complete a required questionnaire to determine their eligibility for the program.

The model notice for employers that do currently offer health coverage features a lot of slots for information about your health plan in Part B. Since the law doesn’t actually require you to provide the information, and because some of the information may be hard to dig up employers may decide to disregard some or all of Part B, especially if the information is uncertain or likely to change, employers to be “cautious about volunteering too much information.”

Ask us about our Online Notification Tool developed by our payroll partner. Be sure to visit our section on Health Care Reform for information on other notices required to be provided and to download additional model notices available for employers and group health plans.

[tab_item title=”Reminder PCORI Research Fees Due by July 231st”]

Posted on July 24 2013

Fees Apply to Employers Sponsoring Certain Self-Insured Plans

Effective for plan years ending on or after October 1, 2012, and before October 1, 2019, employers that sponsorcertain self-insured plans are responsible for new fees to fund the Patient-Centered Outcomes Research Institute (also known as PCORI). HRAs and health FSAs that are not treated as excepted benefits are generally subject to the fees.

Fees are due no later than July 31st of the year following the last day of the plan year. The IRS has revised Form 720for affected employers to report and pay the required fees.

Review our Health Care Reform Checklist for information on other requirements impacting employers and group health plans this year.

[/tab_item]

[tab_item title=”Affordable Care Act Weekly Webinar Series”]

Posted on July 23 2013

Free Series for Small Business Owners to Help Understand the Law

The U.S. Small Business Administration (SBA), together with the Small Business Majority (a national nonprofit advocacy organization), has launched the Affordable Care Act 101 Weekly Webinar Series. The webinars feature guidance on key pieces of the law for small business owners provided by SBA representatives, followed by a question and answer period.

Topics being discussed in the webinars include:

Small business tax credits—who is eligible and how to claim the credit;

Shared responsibility (also known as “pay or play”);

Cost containment; and

Tools and resources available for small businesses to learn more about the law.

The free series will take place every Thursday from now through the opening of the Health Insurance Exchanges (Marketplaces) in October. The first series of webinars will cover the same content; a second round of webinars featuring new content will be held later this fall.

The registration links for the first series of webinars can be found by clicking here. After registering, you will receive a confirmation email with all of the information needed to access the webinar either by telephone or online.

Visit our Health Care Reform Blog section to stay on top of the latest Affordable Care Act updates.

[/tab_item]

[tab_item title=”4 Things Employers Should Know About Providing the Health Insurance Exchange Notice”]

Posted on July 19 2013

Notice Must Be Distributed to Current Employees No Later Than October 1, 2013

Following a delay in the original effective date, employers will need to comply with the new requirement to provide each employee a written notice with information about a Health Insurance Exchange (also known as a Marketplace) beginning this fall. Below are four important reminders about the notice.

The notice requirement applies to employers covered by the federal Fair Labor Standards Act (FLSA). In general, the FLSA applies to employers that employ one or more employees who are engaged in, or produce goods for, interstate commerce. For most firms, a test of not less than $500,000 in annual dollar volume of business applies. The FLSA also specifically covers certain entities such as hospitals, educational institutions, and government agencies.

Employers must provide the notice to each employee, regardless of plan enrollment status (if applicable) or of part-time or full-time status. Employers are not required to provide a separate notice to dependents or other individuals who are or may become eligible for coverage under the plan but who are not employees.

The U.S. Department of Labor has provided two sample notices employers may use to comply with this requirement. The law requires that specific information be included in each notice. One model notice is available for employers that offer a health plan to some or all employees, and another model notice may be used by employers that do not offer a health plan.

Notices must be provided to each current employee no later than October 1, 2013, and to each new employee at the time of hiring beginning October 1, 2013. In general, a notice will be considered provided at the time of hiring if it is provided within 14 days of an employee’s start date. The notice is required to be provided automatically and free of charge. Employers may distribute the notice by first-class mail, or electronically if certain requirements are met.

Visit our section on Health Reform Resource for information on other notices required to be provided and to download additional model notices available for employers and group health plans.

[/tab_item][tab_item title=”5 Q and As on Individual Shared Responsibility”]

Posted on July 12 2013

Employer-Sponsored Coverage Considered “Minimum Essential Coverage”

The individual shared responsibility provision, which goes into effect on January 1, 2014, requires individuals of all ages (including children) to have minimum essential health coverage for each month, qualify for an exemption, or make a payment when filing his or her federal income tax return. Below are five questions and answers related to the mandate that may be of interest to employers and employees.

1. What counts as minimum essential coverage? Minimum essential coverage includes employer-sponsored coverage (including COBRA coverage and retiree coverage), coverage purchased in the individual market, Medicare Part A coverage and Medicare Advantage, Children’s Health Insurance Program (CHIP) coverage, and certain other types of coverage.

Minimum essential coverage does not include coverage providing only limited benefits, such as coverage only for vision care or dental care, workers’ compensation, or disability policies.

2. If an employee receives coverage from a spouse’s employer, will that employee have minimum essential coverage? Yes. Employer-sponsored coverage is generally minimum essential coverage. If an employee enrolls in employer-sponsored coverage for himself and his family, the employee and all of the covered family members have minimum essential coverage.

3. Does an employee’s spouse and dependent children have to be covered under the same policy or plan that covers the employee? No. An employee, his or her spouse, and dependent children do not have to be covered under the same policy or plan. However, the employee, spouse, and each dependent child for whom the employee may claim a personal exemption on his or her federal income tax return must have minimum essential coverage or qualify for an exemption, or a payment will be owed.

4. A company’s health plan is “grandfathered.” Does the employer’s plan provide minimum essential coverage? Yes. Grandfathered group health plans provide minimum essential coverage.

5. Is transition relief available in certain circumstances? Yes. Notice 2013-42 provides transition relief from the shared responsibility payment for individuals who are eligible to enroll in employer-sponsored health plans with a plan year other than a calendar year (non-calendar year plans) if the plan year begins in 2013 and ends in 2014. The transition relief applies to an employee, or an individual having a relationship to the employee, who is eligible to enroll in a non-calendar year eligible employer-sponsored plan with a 2013-2014 plan year. The transition relief begins in January 2014 and continues through the month in which the 2013-2014 plan year ends.

For More Information You may review additional questions and answers in their entirety on the IRS website.

[/tab_item][tab_item title=”IRS Guidance on Delay of Pay or Play Requirements”]

Posted on July 10 2013

No Penalties Will Be Assessed for 2014

Formal guidance released by the IRS provides additional details regarding the delay of the Health Care Reform “pay or play” requirements. Under those provisions, certain large employers (generally those with at least 50 full-time employees) who do not offer full-time employees affordable health insurance that provides a minimum level of coverage may be subject to a penalty tax.

According to the guidance, no penalties (also known as employer shared responsibility payments) will be assessed for 2014. The “pay or play” requirements will be fully effective for 2015 and employers are encouraged to maintain or expand health coverage in 2014 in preparation for compliance.

The delay is a result of transition relief being provided for 2014 with respect to certain employer and insurer reporting requirements. Such reporting will be necessary for the IRS to determine whether a penalty may be due, and, consequently, the transition relief makes it impractical to determine which employers owe shared responsibility payments for 2014. Once the information reporting rules are issued, employers are encouraged to voluntarily comply with the reporting requirements in 2014.

The delay does not affect the application or effective dates of other Health Care Reform provisions, including the individual shared responsibility requirements and employees’ access to premium tax credits for enrolling in qualified health plans through the Health Insurance Exchanges.

The pre-July 4th news of Obamacare Employer Mandate Delayed until 2015 decision may have started early fireworks. The administration did not, however, delay the larger new requirements facing employers who choose to offer health insurance in the small group market––employers with less than 50 workers. The biggest requirement – Essential Health Benefits not delayed.

Whether the rationale was to alleviate business pressure to meet new mandates by Jan 2014 or the real fear that Employers have already begun making necessary employment hours cut backs to avoid the $2,000 penalty. A $3,000/employee penalty was also looming for Employers offering unaffordable insurance.

Keep in mind that this limited delay does not affect other provisions of the Affordable Care Act slated to go into effect in or before 2014, such as:

Individual mandate which requires most individuals to purchase insurance by January 1, 2014, or pay a tax penalty.

a 90-day maximum on eligibility waiting periods;

monetary caps on annual out-of-pocket maximums;

total elimination of lifetime and annual limits (including expiration of waivers that permitted certain “mini-med” plans and stand-alone Health Reimbursement Arrangements to stay in place through plan years beginning in 2013);

Patient Centered Outcomes Research Institute (PCORI) excise taxes and transitional reinsurance program fees; HRA/HSA/FSA clients also pay a monthly $1/employee tax.

a notice informing employees of the availability of the new health insurance Exchanges (a model notice is available on the U. S. Department of Labor website); and insurance market reforms.

The biggest impact is the Essential Health Benefits (EHB) which will not be delayed and this affects fully insured or ALL Small Businesses. While small employers are not required to offer coverage, if they do then they come under that large number of new essential health benefit mandates and group rating rules that won’t apply to large employers. These small group requirements are expected to increase the cost of small group coverage by an average of 15%––with wide variation by state and the average age of the group.

An employer sponsoring a Healthy NY or Brooklyn Healthworks Plan today for example would be disqualified as this does not carry all Essential Health Benefits. The very popular Healthy NY is slated to shut down for Jan 2014 and most Employers have just received this transition letter last week. Individual and Sole Prop Healthy NY is terminating and small business Healthy NY must be reapplied under a new higher cost version. While the plan did not carry Ambulance and had a $3,000 limited Pharmacy plan it is priced 35% below market and did manage to capture hundreds of thousands that would otherwise had been uninsured. The same is true for those on Hospital Only or high deductible catastrophic plans.

So what are these Essential Health Benefits?

All individual and small group policies on and off-Exchangemust cover ten categories of minimum essential health benefits.

Under the ACA, each state must choose one plan from among popular health insurance plans offered statewide to serve as a benchmark for EHBs. The benchmark plan will act as the model for how plans must define and include EHBs in their coverage — in both the individual and small group markets. New York selected the benefits of the State’s largest small group plan as its EHB benchmark. There is also a Minimum Value requirement, See NYS Minimum Value STANDARD BENEFIT DESIGN COST SHARING DESCRIPTION CHART (5-6-2013) Some of the plan’s components include:

No cost-sharing for routine preventive services

Pediatric dental and vision coverage

Habilitative and rehabilitative services, including physical therapy, speech therapy and occupational therapy

Rich mental/behavioral health services

No annual or lifetime dollar limits on benefits

Conversely, a shift to self- insurance is underway as self-insureds can avoid many taxes and instead ONLY cover the Minimum Essential Coverage which is different than the Essential Health Benefits. The strategy coupled with reinsurance is a great sophisticated model usually reserved for larger groups. This segment will be able to avoid local additional State mandates which in States like NY account for 14-16%% of the costs. Thats a total swing of 30% for a fully insured NY group. Also, self-insured groups do NOT pay added taxes such as the health insurance tax of $9 Billion annually over the next 10 years.

The administration has shown their sensitivity to larger groups. This segment already covers 94% of its employees at least in some fashion while small businesses cover less than 50%.

Why not do the same for small employers as well? And while they are at it, use the time to reconsider the impact many of these regulations are likely to have on the number of small employers continuing to offer coverage.

For a downloadable guide on self-insuring and secondary market reinsurance for your group please send contact form below. In the meantime, please visit to view past blogs and Legislative Alerts at https://360peo.com/feed.

Usually, you can take care of your bites and stings at home with your parents’ help. Here’s what to do:

Mosquitoes, fleas and other small bugs

Wash the bite with soap and water.

Use calamine (rhymes with “pal–of–mine”) lotion or another cream that will help you stop the itch.

Don’t scratch the bites, even though that’s hard because they itch a lot!

Put ice on a swollen bite.

See a doctor if your bite looks worse or you just can’t stop scratching. Talk to your mom, dad, or another adult about it.

Bees and wasps

Tell a grown-up right away that you’ve been stung.

Take out the stinger if it’s still in your skin – ask a grown-up for help.

Gently wash the sting with soap and water. You might have to do this a few times a day.

Put an icepack on the sting.

Apply a paste made with baking soda and water. Baking soda is something people cook with, but it also can make stings feel a lot better. Ask an adult to help you do this.

Ask your mom or dad if you can take some pain medicine.

Use some lotion or cream to stop the itch if it’s bothering you.

Sometimes, stings can be dangerous. To learn if you might have an allergic reaction to the sting, visit Reactions to bites and stings.

Spiders

Wash the bite with soap and water.Most spider bites can be treated by a grown-up.

Put on an ice pack to make it less puffy.

If you think a black widow or brown recluse spider bit you, tell a grown-up right away. You might need to see a doctor and go to the hospital.

Ticks

Don’t pull off a tick if you find one on your skin, but tell your mom, dad or another adult right away.

An adult should grab the tick with a tweezers close to your skin and pull straight up to remove the tick.

Treating Bites and Stings

Carefully look over the rest of your body. With your parents’ help, check all over, including behind the ears, to be sure there are no other ticks.

Never squeeze or crush a tick, because that can cause more venom to enter your body.

Save the tick in a jar of alcohol in case your doctor wants to see it later. The doctor might be able to tell you if this is the kind of tick that can cause Lyme disease, which can feel like the flu. To learn more, visit Reactions to bites and stings.

In Time magazine’s March issue Bitter Pill: Why Medical Bills Are Killing Us Steven Brill gets to work on answering the ever elusive Why are Medical Costs So High? The 21,000 word article is longest article in Time Magazine history that can boiled down to simply there is no free marketplace in health care. We think everything in this country is a free market but is there a free market when one needs to got to an emergency room or a free market when one must take a cancer pill? According to Howard Dean the singular reason is to get away form the current fee for service system where providers get paid per procedure and not per patient.

Here’s an eye opener: “Insurance Companies are not really the problem they run pretty terribly. They process claims, a lot of us think they process claims and fairly consistently but they are increasingly at the mercy of hospitals which are consolidating buying a doctors practices. We should tax profits on so-called nonprofit hospitals and put that money back into the system. We should control all the prices for prescription drugs because if I have a monopoly a cancer wonder drug I can charge anything I want for them that’s obviously not a free market and it’s completely two different uses you see this article once you follow the money.”

Transcript of the video:

“This is not a free-market. You don’t get health care because you want it. You don’t wake up in the morning and gee I love to go down to the emergency room today. You enter that market and will you know nothing about the products of you being asked by no choice of those products. Hi I am Steve Brill I’ve got the cover story this week in TIME Magazine looking at the health care debate from a very different perspective. Everybody focuses on who should pay for the exorbitant cost of health care and that I decided to do was ask for more fundamental question which is why does health care cost so much.

I look behind the bills and trace the bills all the way back to who’s getting what money is making what profits and the results are really surprised one of the things I found that everybody in the healthcare industry knows about that that nobody else knows his something called the charge-master. The charge master is a internal listing each hospital of the thousands of different items that they charge and nobody could explain it to me. Indeed would be hard to explain for example why would you charge $77 for a box of gauze pads? You can buy for a dollar at the drugstore. why would you charge thousands of dollars for CAT scan it really isn’t cost you anything?

It’s emblematic if you will, of the irrationality of the higher healthcare system because no one can explain the cost no one tries to and the only people who are guaranteed surefire to pay to be asked to pay the charge-master prices are the poorest people who don’t have health insurance.

Real profit makers are way hospitals markup very expensive drugs that you get. If you have cancer to have pneumonia but they’re making thousands of dollars on these drugs and drug companies in turn making still more thousands of dollars.

Obamacare does very little to solve any of these problems and just probably why you got to Congress I’m it doesn’t do anything to control the prices of prescription drugs or medical devices CAT scan. In fact if anything it will increase the profitable the players in the market by making equal insurance and therefore more people are in the marketplace with the funds from insurance companies to buy all these products.

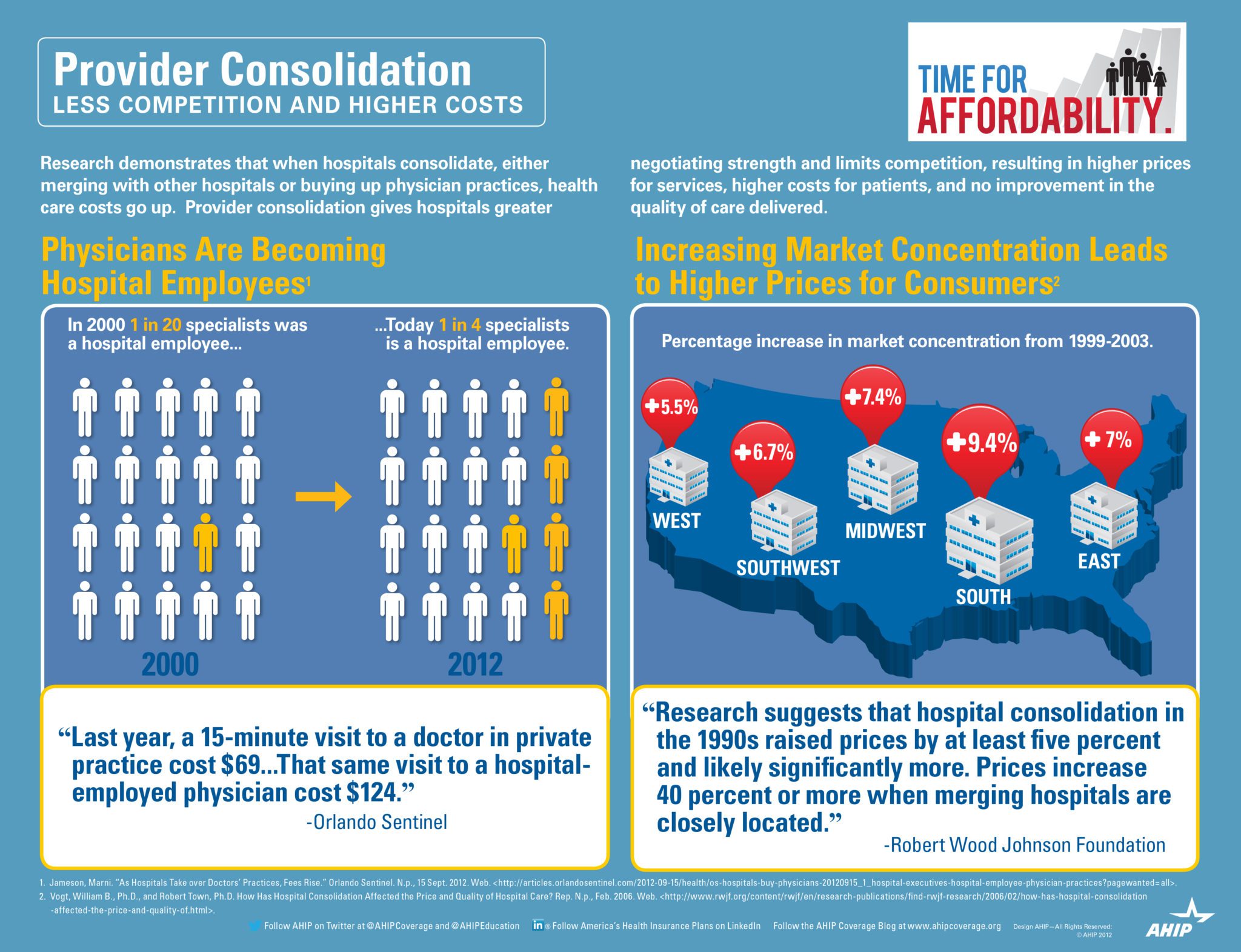

Insurance Companies are not really the problem they run pretty terribly. They process claims, a lot of us think they process claims and fairly consistently but they are increasingly at the mercy of hospitals which are consolidating buying a doctors practices. See Provider Consolidation Info-graph– “The proliferation of hospital mergers and hospitals’ appetite for buying doctors’ practices—in part to assure a steady stream of patients to fill hospital beds—could create local monopolies that raise prices without increasing efficiency. ‘Historically,’ says Deloitte’s Mr. Keckley, ‘hospital consolidation hasn’t reduced costs.’”

We should tax profits on so-called nonprofit hospitals and put that money back into the system. We should control all the prices for prescription drugs because if I have a monopoly a cancer wonder drug I can charge anything I want for them that’s obviously not a free market and it’s completely two different uses you see this article once you follow the money.”

The ACO (Accountable Care Organization) referenced in our post NYU Beth Israel Merger and ACOs are models encouraged in Obamacare in fact as examples of Provider capitated reimbursement that Howard Dean is in favor of. An ACOI cordiantes patient care and provide the full range of health care services for patients. The health reform law provides incentives for providers who join together to form such organizations and who agree to be accountable for the quality, cost, and overall care of Medicarebeneficiaries who are enrolled in the traditional fee-for-service program who are assigned to the ACO.

The fee-for-service system has evidentially driven costs by incentivizing volumes of added procedures. The ACO model is built on par excellence hospitals such as Mayo Clinic where there is team of providers are financially incentivized for patient care coordination outcomes and high quality of care. The ACO’s payment would be tied to achieving goals that improve health care and save money. Members of the ACO would divvy up that payment. Today’s payment system, investments in providing better care are doubly penalized. If a hospital hires a nurse to follow up with patients after they are discharged in order to reduce readmissions — for example, to help patients with diabetes improve blood sugar control — it must pay for the nurse, which is typically not reimbursed by insurance companies or Medicare, and it loses revenue by preventing the readmission.

Congress included ACOs in the health care law as a way to rein in Medicare spending. That federal program pays for health care for people 65 and older and the disabled. The federal government estimates ACOs could save the Medicare program up to $940 million over four years. Medicare recently began testing this system with 32 pilot ACOs in 18 states, including one in the New York City area – Bronx Accountable Healthcare Network.

Some have pointed to ACO Model just as a pro-merger supporting argument with the FTC. These significant mergers create market dominance and therefore limit competition and drive up health care dollars. And yet Hospitals operate on thin profit margins and cannot afford to lose market share therein lies is the conundrum.

Note: At time of this article MVP and Hudson Valley Health Plans announced a merger –Hudson Health Plans joins MVP. Hudson Health Plan, the Medicaid managed care organization based in Tarrytown, will join the MVP Health Care group of companies, the two nonprofit health plans jointly announced today.

“Size and diversity of offerings are important for health plans in the new world of the health insurance marketplaces. A 55-year-old person would like to join a health plan that can continue to cover him when he turns 65. Likewise, if someone is no longer eligible for Medicaid, she might prefer to buy a commercial product from that same insurer. Together, MVP and Hudson now can cover people through all of life’s stages and changing needs.

In the coming months, Millennium Medical Solutions Inc will host seminars and will share information you’ll need to know as the countdown continues to October 1st. Please contact us for immediate information on how to implement these initiatives for your group-specific needs at info@medicalsolutionscorp.com or Call (855) 667-4621.

Health Insurance Mandates 2012. The Councel for Affordable Health Insurance in VA released their annual “Health Insurance Mandates in the States” for 2012 last week. While NYS did not crack the top 5 they did come close at number 7 this year.

NYS Mandates were discussed in our posting Empire Leaving Small Groups Nov 2011. ” Today, we have so many State mandates that many of the mandates(overage dependents coverage, preventive care, pre-existing for kids) in PPACA didnt even affect NY since they were already in place. Mandates account for approx 17% of the costs of which Small Businesses pay more than fair share. Large corporations and Unions can self insure and avoid some mandates as they are governed by ERISA and not State. To the relief of of our struggling clients on subsidized Healthy NYthe State doesn’t play by their own rules and instead opts out of its very own mandates.”

According to the study CAHI Identifies 2,271 State Health Insurance Mandates “The sheer number of state mandates will make it difficult for states to deliver on one of the key promises repeatedly made by supporters of Obamacare: it would provide all Americans with affordable health coverage. The essential health benefit plan design was supposed to give states the flexibility to craft benefit packages which would be suitable and affordable for their unique populations. But HHS shackled the states to the full load of mandated benefits on their books, and the prices of next year’s offerings in the health insurance exchanges are going to bear witness to the free-wheeling mandate craze of the last twenty years. Recent studies have predicted double digit increases in health insurance premiums next year — the mandates are coming home to roost,” said Roy Ramthun, CAHI’s Director of Federal Affairs.”

The United Hospital Fun estimates that approximately 2.2 million New Yorkers lacked insurance coverage in 2009, (Health Insurance Coverage in New York 2009.)

The collective cost of paying for New York’s health insurance mandates equates to 12.2% of overall premium cost. Based on 2008 premiums, this translates into $1,538 expense per year for an average family policy and $566 per year for a single person policy. (Employer Alliance, NYS Mandated Health Insurance Benefits, 2003)

Higher health care costs increase the number of uninsured. In New York, it is estimated that for every 1% increase in premiums, 30,000 New Yorkers lose health insurance. (Barents Group, 1999)

Mandates have a cumulative impact on premium costs. It is estimated that the cost of the 12 most common mandates can increase the cost of health insurance by as much as 30%. (Milliman and Robertson 1996)

Rising health care costs have the biggest impact on the small business sector. For every 1% increase in premium costs, small business sponsorship of health insurance drops by 2.6%. (Morrisey et al., 1994)

The percentage of US small business workers receiving insurance through their employer declined 5% between 1996 and 1998 – from 52% in 1996 to 47% in 1998. (KPMG Peat Marwick, 1999)

Nearly one of every four uninsured Americans has no health care coverage as the direct result of state mandates. (Jensen, Morrisey, 1999)

Health insurance premiums for New York’s working families skyrocketed between 2000 & 2007 increasing by 80.7 percent. (Families versus Paychecks, Families USA 2008)

Since 1999, family premiums for employer-sponsored health coverage have increased by 131 percent, placing increasing cost burdens on employers and workers. (Kaiser Family Foundation and Health Research and Educational Trust. Employer Health Benefits 2009 Annual Survey. September 2009).

the HIT is actually a hidden tax on small business. PPACA assesses a tax on all health insurance companies based on their “net premiums” written. The tax will raise $8 billion starting in 2014, $14.3 billion in 2018 and more in later years. This is [aid for by fully insured health plans which are comprised mostly by small businesses.

The AHIP infograph provides visually a great infograph describing how provider consolidation increases costs. According to Wall Street Journal Article this week –Four Key Questions for Health-Care Law “The proliferation of hospital mergers and hospitals’ appetite for buying doctors’ practices—in part to assure a steady stream of patients to fill hospital beds—could create local monopolies that raise prices without increasing efficiency. ‘Historically,’ says Deloitte’s Mr. Keckley, ‘hospital consolidation hasn’t reduced costs.’”

If we as a society ask our hospitals to behave as industries then size matters in achieving economies of scale. However, the important question we must then answer are we operating in a true free market economy when someone gets sick?

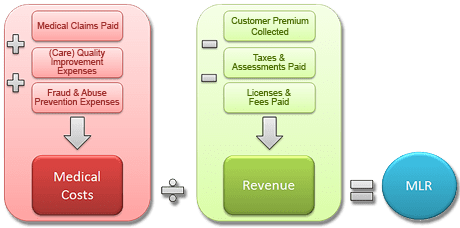

So what are are Medical Loss Ratios and why should we care?

Medical Loss Ratio (MLR) – The minimum percentage of premium dollars a commercial insurance company must spend on the reimbursement of certain medical costs. The health reform law requires insurers in the large group market to have an MLR of 85% and insurers in the small group and individual markets to have an MLR of 80% (with some waivers granted to states to reduce the threshold for certain markets).

The MLR calculation is determined on a state-by-state basis by each insurer or HMO. Rebates are calculated separately for the individual, small group and large group markets in each state.

The final regulations issued onDecember 2, 2011: • The rebate distribution processwassimplified to allowmostrebatesto be distributed to group policyholders rather than to each participantin a group plan. • Employers can distribute rebatesin a variety ofwaysincluding future premiumreductions and benefit enhancementsthatwill allowrebatesto be tax-free to recipients.

This is arguably the most significant change in Health Care Reform. In short, this is a price control on health insurers regulating profits ceilings. Unlike many industries, however, insurers must maintain a high minimum in reserves. After-all if Health Underwriters incorrectly predict unknown future costs by pricing too low there is no recovery of losses. Conversely if they priced policies too high they must return premiums to subscribers. While this is altruistically great, in today’s Oligopoly Business with an avg of 3-4 insurers in a NYC Metro Area the realities are little motivation to compete. Furthermore, health insurers in NYS have higher MLR rates and must place rate filings a year in advance. This complicates the ability of actuarial to predict future costs thus asking for higher rate increase just in case. The State then reacts by cutting increase in half which forces more insurers out of State and actually emboldens remaining health insurers to push for more aggressive cuts in benefits, challenging underwriting participation’s and limit an insurers will to go above and beyond minimum essential benefits requirements.

In full disclosure, the Benefit advisor (broker/consultant) commissions have been cut close to 50% as this cuts into insurers profits. See our interview in Crain’s regarding this https://360peo.com/p/crains-article-on-broker-commissions-cuts. Small Businesses and Sole Prop feel this the most as the resources needed to intelligently shop for benefits, reinsurance, navigate state/federal laws, employee annual open enrollments meetings have been defrayed by using a Broker. In many cases, good Brokers have become the de-facto HR.

The Federal Gov has already spent $2.2 Billion on State Exchanges. And this figures does not include remaining States as there are only 19 States working on an Exchange for 2014. The Exchanges will be built up for 2 years and then must be fully independent by 2016. If 88% of small groups coverage purchased by Brokers acc. to Boston’s Wakely Report in research study- Role of Producers and Other Third Party Assisters in New York’s Individual and SHOP Exchanges the distribution infrastructure is already there. Access to care is not the difficulty in finding a plan its the very cost of the plan! Why then does NYS decide to spend on building up new infrastructures? Agents/Brokers can easily outreach and council to uninsured as well. In fact many small businesses such as construction, consulting services and dining have many uninsured that an Agent/Broker already has a relationship with.

So where is this going? A weakened health insurer market place with the new domination of powerful large Medical groups numbering in the thousands + mega Hospital chains dictating rates. To be sure some the Hospital market is becoming close to an Oligopoly as well see: http://www.nytimes.com/2012/03/08/health/hospital-groups-will-get-bigger-moodys-report-says.html?_r=0.Still disagree? Hospital stocks have averaged 20-30% increases while insurance stocks have remained net net stagnant and down after initial spike. Ask yourself why NYS had 10 – 15 private health insurers 20 years ago while there are no rumors of new insurers or returning insurers?

If additional changes aren’t made, there could be unintended consequences including less competition, a reduction in consumer choice and higher health insurance costs. Oh I almost forgot, most clients especially NY SMB were not entitled to a rebate check with a small minority receiving avg $120.