Many follow up questions on the postPay or Play Employer Guide have been raised. A Pay or Play FAQ hopefully adds some clarification.

Will I be required to offer health insurance coverage to my employees?

No. However, if you have at least 50 full-time employees, and you don’t offer coverage, you will owe a penalty starting in 2014 if any full time employee is eligible for and purchases subsidized coverage through an exchange. This penalty is called the “free rider” penalty.

We employ about 40 full-time employees working 30 or more hours per week and about 25 part-time or seasonal employees. So we are not subject to the employer mandate penalties, right?

You may be. The health reform law does not require you to provide coverage for employees working on average less than 30 hours per week (“part-time”). However, the hours worked by part time employees are counted to determine whether you have at least 50 full-time employee equivalents and therefore are subject to the employer mandate. This is done by taking the total number of monthly hours worked by part time employees (but not to exceed 120 hours for any one part-time employee) and dividing by 120 to get the number of “full time equivalent” employees. You would then add those “full-time equivalent” employees to your 40 full-time employees.

The hours worked by seasonal employees are also counted to determine whether you have at least 50 full-time employee equivalents and therefore are subject to the employer mandate. For purposes of determining whether you are a large employer, seasonal employees are workers who perform labor or services on a seasonal basis (i.e. exclusively performed at certain seasons or periods of the year and which, from its nature, may not be continuous or carried on throughout the year) for no more than 120 days during the taxable year and retail workers employed exclusively during holiday seasons. There is an exemption from the employer mandate that says you would not be considered to employ more than 50 full-time employees if:

Your workforce only exceeds 50 full-time employees for 120 days, or fewer, during the calendar year; and

The employees in excess of 50 who were employed during that 120-day (or fewer) period were seasonal workers.

Our workforce numbers go up and down during the year. How do we determine if we had at least 50 full-time employees on business days during the preceding calendar year?

For purposes of determining if you are a large employer, the formula requires the following steps:

1.Determine the total number of full-time employees (including any full-time seasonal workers) for each calendar month in the preceding calendar year;

2.Determine the total number of full-time equivalents (including non-full-time seasonal employees) for each calendar month in the preceding calendar year;

3.Add the number of full-time employees and full-time equivalents described in Steps 1 and 2 above for each month of the calendar year;

4.Add up the 12 monthly numbers;

5.Divide by 12. If the average per month is 50 or more, you are a large employer.

So if we offer coverage to our full-time employees, we will not have to pay a penalty?

Not necessarily. If you have at least 50 full-time employees and you offer coverage to at least 95% of your full-time employees, you are still subject to a penalty starting in 2014 if:

1.A full-time employee’s contribution for employee-only coverage exceeds 9.5% of the employee’s household income (Note: see below regarding a proposed affordability “safe harbor”) or the plan’s value is less than 60%; and

2.The employee’s household income is less than 400% of the federal poverty level; and

3.The employee waives your coverage and purchases coverage on an exchange with premium tax credits.

The penalty will be calculated separately for each month in which the above applies. The amount of the penalty for a given month equals the number of full- time employees who receive a premium tax credit for that month multiplied by 1/12 of $3,000.

We have more than 50 full-time employees so we are subject to the employer mandate penalties. How do we know which of our employees is considered “full-time” requiring us to pay a penalty if they qualify for premium tax credits at an exchange (if the employee has a variable work schedule or is seasonal)?

Through the end of 2014, for purposes of the employer mandate penalties, the guidance permits you to use a “look-back measurement period/stability period” safe harbor to determine which of your employees are considered full-time employees. You may use a standard measurement/stability period for ongoing employees, while using a different initial measurement/stability period for new variable and seasonal employees

How do the full-time employee safe harbors work for new hires?

They are generally based on the employee’s hours worked, or, the amount of hours the employee is reasonably expected to work as of their hire date.

New employee reasonably expected to work full-time (i.e. 30 or more hours per week)– If you reasonably expect an employee to work full-time when you hire them, and coverage is offered to the employee before the end of the employee’s initial 90 days of employment, you will not be subject to the employer mandate payment for that employee, if the coverage is affordable and meets the minimum required value.

New employee reasonably expected to work part-time (i.e. less than 30 hours per week)-– If you reasonably expect an employee to work part-time and the employee’s number of hours do not vary, you will not be subject to the employer mandate penalty for that employee if you don’t offer them coverage.

New variable hour and seasonal employees – If based on the facts and circumstances at the date the employee begins working (the start date), you cannot determine that the employee is reasonably expected to work on average at least 30 hours per week, then that employee is a variable hour employee. Because the term “seasonal employee” is not defined for purposes of the employer responsibility penalty, through 2014, you are permitted to use a reasonable, good faith interpretation of the term “seasonal employee”. The IRS has indicated that any interpretation of the term “seasonal” probably would not be reasonable if it included a working period of more than six months. Once hired, you have the option to determine whether a new variable hour or seasonal employee is a full-time employee using an “initial measurement period” of between three and 12 months (as selected by you).You would measure the hours of service completed by the new employee during the initial measurement period to determine whether the employee worked an average of 30 hours per week or more during this period. If the employee did work at least 30 hours per week during the measurement period, then the employee would be treated as a full-time employee during a subsequent “stability period,” regardless of the employee’s number of hours of service during the stability period, so long as he or she remained an employee. The stability period must be for at least six consecutive calendar months and cannot be shorter than the initial measurement period. If the employee then didn’t work on average at least 30 hours per week during the measurement period, you would not have to treat the employee as a full-time employee during the stability period that followed the measurement period, but the stability period could not be more than one month longer than the initial measurement period.

Example – Facts: For new variable hour employees, you use a 12-month initial measurement period that begins on the start date and apply an administrative period from the end of the initial measurement period through the end of the first calendar month beginning on or after the end of the initial measurement period.

Situation: Dianna is hired on May 10, 2014. Dianna’s initial measurement period runs from May 10, 2014, through May 9, 2015. Dianna works an average of 30 hours per week during this initial measurement period. You offer affordable coverage to Dianna for a stability period that runs from July 1, 2015 through June 30, 2016.

Conclusion: Dianna worked an average of 30 hours per week during her initial measurement period and you had (1) an initial measurement period that does not exceed 12 months; (2) an administrative period totaling not more than 90 days; and (3) a combined initial measurement period and administrative period that does not last beyond the final day of the first calendar month beginning on or after the one-year anniversary of Dianna’s start date. Accordingly, from Dianna’s start date through June 30, 2016, you are not subject to an employer mandate penalty with respect to Dianna because you complied with the standards for the initial measurement period and stability periods for a new variable hour employee. However, you must test Dianna again based on the period from October 15, 2014 through October 14, 2015 (your first standard measurement period that begins after Dianna’s start date) to see if she qualifies to continue coverage beyond the initial stability period.

Employee FT Testing Period Chart

As you can tell, there are many things to consider as you map out your plans for how your business is going to proceed with health care reform. Millennium Medical Solutions Corp hopes to be a valuable resource in the weeks and months ahead as you make these decisions. What about you? Do you have any glaring questions that we could answer for you about health care reform compliance?

For a FREE Affordable Care Act Guide leave your questions in the comments below or click the “Contact Us” button and we’ll do our best to answer your questions.

Please refer to the IRS Notice in the links below for more details and examples:

DISCLAIMER: We share this information with our clients and friends for general informational purposes only. It does not necessarily address all of your specific issues. It should not be construed as, nor is it intended to provide, legal advice. Questions regarding specific issues and application of these rules to your plans should be addressed by your legal counsel.

Accountable Care Organization (ACO) – These organizations coordinate patient care and provide the full range of health care services for patients. The health reform law provides incentives for providers who join together to form such organizations and who agree to be accountable for the quality, cost, and overall care of Medicare beneficiaries who are enrolled in the traditional fee-for-service program who are assigned to the ACO. Annual Benefit Limit – In the past, some insurance plans have placed a limit on the dollar amount of claims they will pay in a given year for an individual. Beginning in 2010, annual benefit limits on certain “essential health benefits” are restricted on a graduated basis, and annual limits will eventually be prohibited in 2014. Basic Health Plan – Beginning in 2014, states will have the option of creating a basic health plan to provide coverage to individuals with incomes between 133 and 200 percent of poverty instead of enrolling in the health insurance exchange and receiving premium subsidies. The federal government will provide states that choose to offer this plan with 95 percent of what it would have paid to subsidize these enrollees in the health insurance exchange. Benefit Package – The set of health services, such as physician visits, hospitalizations, and prescription drugs, that are covered by a member’s insurance policy or group health plan. Capitation – Under a capitation system health care providers are paid a set amount for each enrolled person assigned to that physician or group of physicians, whether or not that person seeks care. Case Management – The coordination of medical care for patients with specific diagnoses or high health care needs, performed by case managers who can include medical directors or nurses. Catastrophic Coverage – A coverage option with a limited benefit plan design accompanied by a high Deductible. The plan design is intended to protect primarily against the cost for unforeseen and expensive illnesses or injuries. These plans are attractive to young adults in relatively good health. CHIP – The Children’s Health Insurance Program (CHIP) is a program administered by the United States Department of Health and Human Services that provides matching funds to states for health insurance to low income families with children. The program was designed with the intent to cover uninsured children in families with incomes that are modest but too high to qualify for Medicaid. Chronic Care Management – The coordination of health care and supportive services to improve the health status of patients with chronic conditions, such as diabetes and asthma. The goals of these programs are to improve the quality of care and manage costs. COBRA – Consolidated Omnibus Budget Reconciliation Act of 1985 (COBRA) applies to employers who generally employ 20 or more full time equivalent employees. Employees who lose their jobs are able to continue their employer-sponsored coverage for a set period of time. For example, employees are typically entitled to extend coverage for 18 months, however if they are deemed disabled by the Social Security Administration, coverage may continue for up to 29 months. Co-insurance – The amount or percentage of the reimbursed amount of covered expenses a plan member must pay for health services after the Deductible has been met. Community Living Assistance Services and Supports (CLASS) Program – The CLASS program establishes a national voluntary long-term care insurance program for the purchase of non-medical services and support necessary for enrollees who have paid premiums into the program and become eligible (due to disability or chronic illnesses). Enrollees would receive benefits that help pay for assistance in the home or in a facility in future years. Enrollment begins January 1, 2011 (targeting working adults who can make voluntary premium contributions through payroll deductions or directly). The first benefits will be paid out to enrollees in 2016. Community Rating – A method of pricing health insurance plans, where all policyholders are charged the same premium, regardless of health status, age or other factors. “Modified community rating” generally refers to a method where health insurers may vary premiums based on specified demographic characteristics (e.g. age, gender, location), but cannot vary premiums based on the health status or claims history of policyholders. Comparative Effectiveness Research – Research is federally sponsored to compare existing health care interventions to determine which work best for which patients and which pose the greatest benefits and harms. The research also aims to improve the quality of care and to control costs. Consumer-Directed Health Plans – These health plans seek to increase consumer awareness about health care costs and provide incentives for consumers to consider costs when making health care decisions. These plans usually have a high Deductible accompanied by a savings account for health care services. There are two types of savings accounts – Health Savings Accounts (HSAs) and Health Reimbursement Accounts (HRAs). Co-payment – A fixed dollar amount paid by an individual receiving a health care service covered by the member’s plan. Cost-Sharing – Health plan members are required to pay a portion of the costs of their care. Examples of these costs include Co-payments, Co-insurance and annual Deductibles. Deductible – The dollar amount that a plan member must pay for health care services each year before the insurer begins to reimburse for health care services. Beginning in 2014, deductibles for small group insurance plans will be limited to $2,000 for individual policies and $4,000 for family policies. Disease Management – The coordination of care for the entire disease treatment process, including preventive care, patient education and outpatient care in addition to inpatient and acute care. The process is intended to reduce costs and improve the quality of life for an individual with a chronic condition. Donut Hole – A gap in prescription drug coverage under Medicare Part D, where beneficiaries pay 100% of their prescription drug costs after their total drug costs exceed an initial coverage limit until they qualify for a second tier of coverage. Under the standard Part D benefit, Medicare covers 75% of drug costs below the initial coverage limit ($2,830 in 2010), and 95% of spending within the second tier level ($6,440 in 2010). The “donut hole” specifically refers to the range between these two levels. Health care reform also provides a $250 rebate for all Medicare Part D enrollees who enter the donut hole in 2010, increases discounts in subsequent years and completely closes the donut hole by 2020. Dual Eligibles – A term used to describe an individual who is eligible for Medicare and for some Medicaid benefits. Electronic Health Record/Electronic Medical Records – Computerized patient health records, including medical, demographic, and administrative information. These records can be created and stored within one organization or shared across multiple health care organizations and sites. Employee Retirement Income Security Act of 1974 (ERISA) – Enacted in 1974 to provide minimum Federal standards for welfare benefit plans in private industry, and protect the interests of employee benefit plan participants and their beneficiaries by requiring the disclosure to them of financial and other information concerning the plan; by establishing standards of conduct for plan fiduciaries; and by providing for appropriate remedies and access to the Federal courts. Employer Mandate – Beginning in 2014 pursuant to the health reform law, employers meeting size or revenue thresholds will be required to offer minimum essential health benefit packages or pay a set portion of the cost of those benefits for use in the Exchanges. Episode of Care – Refers to all the health services related to the treatment of a condition. For acute conditions (such as a concussion or a broken bone), the episode includes all treatment and services from the onset of the condition to its resolution. For chronic conditions (such as diabetes), the episode refers to all services and treatments received over a given period of time. Some payment reform proposals involve basing provider payment on episodes of care instead of paying on a Fee-for-Service basis. Essential Health Benefits – The health reform law placed certain coverage requirements on essential health benefits, and provides a broad set of benefit categories that would be considered essential to a health benefits package — including hospitalization, outpatient services, emergency care, prescription drugs, maternity care, preventive services and other benefits. The Secretary of HHS will, in the future, define what constitutes “Essential Health Benefits” and this will be guided by the current scope of benefits provided under a typical employer plan. For plan years beginning in 2010 the only requirement for “Essential Health Benefits” is that if they are included in the plan they may not be subject to a lifetime limit and until 2014 can only be subject to a “restricted annual limit”. Exchange or Health Insurance Exchange – The health care reform law creates Health Benefit Exchanges (competitive insurance marketplaces) in each state, where individuals and employers can shop for health plans. External Review – Health care reform requires all health plans (except Grandfathered plans) to provide an external review appeal process that meets minimum standards. With the exception of a few state processes currently in existence, external review has typically been limited to appeals of clinical decisions. The health reform law has expanded the scope of external review for self-funded health plans to non-eligibility administrative appeals as well. Administrative appeals deal with such issues as benefit exclusions, benefit limits and disputes over member financial responsibility for payments such as Co-payments, Co-insurance and Deductibles. Fee-for-Service – A traditional method of paying for medical services where doctors and hospitals are paid a fee for each service they provide.

FTE – Full Time Equivalent -The percent of time worked is based on a standard of 100% or 1.0. For example, an employee who is working 60% and employee who is working 40% of the time would equal 100% or an FTE of 1.0.

For example, a firm has 35 full-time employees (30+ hours). In addition, the firm has 20 part time employees who all work 24 hours per week (96 hours per month). These part-time employees’ hours would be treated as equivalent to 16 full-time employees, based on the following calculation: 20 employees x 96 hours / 120 = 1920 / 120 = 16

Grandfathered Plan – A health plan that was in place on March 23, 2010, when the health reform law was enacted, is exempt from complying with some parts of the health reform law, so long as the plan does not make certain changes (such as eliminating or reducing benefits, increasing cost-sharing, or reducing the employer contribution toward the premium). Once a health plan makes such a change, it becomes subject to other health reform provisions (e.g., appeals and cost sharing restrictions on preventive services).

Group Health Plan – Health insurance that is offered by a plan sponsor, typically an employer on behalf of its employees. Guarantee Issue/Guarantee Renewability – Beginning in 2014, the health reform law requires insurers to offer and renew coverage to non-Grandfathered plans, without regard to health status, use of services, or pre-existing conditions. Health Insurance Portability and Accountability Act of 1996 (HIPAA) – This law sets standards for the security and privacy of personal health information. In addition, the law makes it easier for individuals to change jobs without the risk of extended waiting periods due to pre-existing conditions. Health Maintenance Organization (HMO) – A health plan that provides coverage through a network of hospitals, physicians and other health care providers. HMOs usually require the selection of a primary care physician who is responsible for managing and coordinating all health care. Usually, referrals to specialist physicians are required, and the HMO pays only for care provided by an in-network provider. Health Reimbursement Account (HRA) – A tax-exempt account that can be used to pay for qualified health expenses. HRAs are usually paired with a high-Deductible health plan and are funded solely by employer contributions. Health Savings Account (HSA) – A tax-exempt savings account that can be used to pay for qualified medical expenses. Individuals can obtain HSAs from most financial institutions, or through their employer. Both employers and employees can contribute to the plan. To open an HSA, an individual must have health coverage under an HSA-qualified high-Deductible health plan which has Deductibles of at least $1,200 for an individual and $2,400 for a family in 2010. High-Deductible Health Plan – These health insurance plans have higher Deductibles and lower premiums than traditional insurance plans. High-Risk Pool – The health reform law expands upon the current state-based high-risk pool system. The law requires the government to establish or issue contracts to establish a temporary high risk pool (through 2013) to provide coverage for eligible individuals with pre-existing conditions by appropriating $5 billion to subsidize premiums. Eligibility is limited to individuals who have been uninsured for at least six months prior to applying for pool coverage, and who have a pre-existing condition. Individual Mandate – A requirement that most individuals obtain health insurance or pay a penalty beginning in 2014. Massachusetts was the first state to impose an individual mandate that all adults have health insurance. Interim Final Rule (IFR) – A final rule that has the full force and effect of law; thus, affected parties have an obligation to comply with its requirements. An IFR allows interested parties to submit comments during a public comment period and prior to issuing revised guidance. Internal Review – An internal review of an adverse claim determination. Lifetime Benefit Maximum – A limit on the amount an insurer will pay toward the cost of health care services over the lifetime of the policy. Health care reform prohibits lifetime dollar limits on “essential health benefits” effective for plan/policy years beginning on or after September 23, 2010. Long-Term Care – Services needed for an individual to live independently in the community, such as home health and personal care, as well as services provided in institutional settings such as nursing homes. Many of these services are not covered by Medicare or private insurance (see also the Community Living Assistance Services and Supports program defined above). Managed Care – A health care delivery system that seeks to reduce the cost of providing health benefits and improve the quality of care. These arrangements often rely on primary care physicians to manage the care their patients receive. Mandatory Benefits – A state or federal requirement that health plans provide coverage for certain benefits, treatment or services. Medicaid – A federal and state funded program that provides medical and health related services to certain low-income Americans. The health reform law expands Medicaid eligibility to non-Medicare eligible individuals with incomes up to 133% of the Federal poverty level, establishing uniform eligibility for adults and children across all states by 2014. Medical Loss Ratio (MLR) – The minimum percentage of premium dollars a commercial insurance company must spend on the reimbursement of certain medical costs. The health reform law requires insurers in the large group market to have an MLR of 85% and insurers in the small group and individual markets to have an MLR of 80% (with some waivers granted to states to reduce the threshold for certain markets). Medicare – A federal program that provides health care coverage to people age 65 and older, and to those who are under 65 and are permanently physically disabled or who have a congenital physical disability; or to those who meet other special criteria such as end-stage renal disease. Eligible individuals can receive coverage for hospital services (Medicare Part A), physician based medical services (Medicare Part B) and prescription drugs (Medicare Part D). Medicare Advantage – Also referred to as Medicare Part C, the Medicare Advantage program allows Medicare beneficiaries to receive their Medicare benefits through a private insurance plan. Out-of-Pocket Costs – Health care costs that are not covered by insurance, such as Deductibles, Co-payments, and Co-insurance. Out-of-pocket costs do not include premium costs. Out-of-Pocket Maximum – An annual limit on the amount of money individuals are required to pay out-of-pocket for health care costs, excluding premiums. The health reform law, beginning in 2014, prevents an employer from imposing cost sharing in amounts greater than the current out-of-pocket limits for high-Deductible health plans ($5,950 for an individual policy or $11,900 for a family policy in 2010). These amounts will be adjusted annually. Patient Centered Medical Home – A term defining a health care setting where patients receive comprehensive primary care services, have an ongoing relationship with a primary care provider who directs and coordinates their care; and have enhanced access to non-emergent care. Patient Protection and Affordable Care Act (PPACA) – Also referred to as the “health reform law,” this Act begins the implementation of a staged set of rules with an initial effective date of March 23, 2010. The law is intended to increase access to health care for more Americans, and includes many changes that impact the commercial health insurance market, Medicare and Medicaid. Pay for Performance – A payment system where health care providers receive incentives for meeting or exceeding quality and cost benchmarks. Some systems also penalize providers who do not meet established benchmarks. The goal of pay for performance programs is to improve the quality of care over time. Pre-existing Condition – An illness or medical condition for which a person is diagnosed or treated within a specified period of time prior to becoming insured in a new plan. The heath reform law prohibits the denial of coverage due to a pre-existing condition for plan and policy years beginning after September 23, 2010 for children under 19, and for all others beginning in 2014. Preferred Provider Organization (PPO) – A type of managed care organization that provides health care coverage through a network of providers. Plan members typically pay higher costs when they seek care from out-of-network providers. Premium – The amount paid, often on a monthly basis, for health insurance. The cost of the premium may be shared between employers or government purchasers, and individuals. Premium Subsidies – A fixed amount of money, or a designated percentage of the premium cost, that is provided to help people purchase health insurance. The health reform law provides premium subsidies to individuals with incomes between 133% and 400% of the federal poverty level who purchase policies through the health insurance Exchanges, beginning in 2014. Preventive Care Services – Health care that emphasizes the early detection and treatment of disease. The health reform law requires certain health plans (excludes Grandfathered plans) to provide coverage without member cost-sharing for certain preventive services. Primary Care Provider – A provider, usually a physician, specializing in internal medicine, family practice, or pediatrics, who is responsible for providing primary care and coordinating other necessary health care services for patients. Qualified Health Plan – Insurance plans that are sold through a Health Insurance Exchange must have been certified as meeting a minimum benchmark of benefits (i.e., essential health benefits) under the health reform law. Rate Review – Review by insurance regulators of a health plan’s proposed premium and premium increases. Rates are reviewed to ensure they are sufficient to pay claims, are not unreasonably high in relation to the medical claim costs and the benefits provided, and are not discriminatorily applied. Reinsurance – Insurance purchased by insurance companies and employers that self-insure their employees’ medical costs, to limit liability or exposure to high claims or increased cost trends. The health reform law includes a temporary federal reinsurance program for employers that insure early retirees over age 55 who are not eligible for Medicare. Rescission – Refers to a practice where an approved policy is voided from its inception by the insurer, usually on the grounds of material misrepresentation or omission on the initial application. Under health reform, rescissions are prohibited except in cases of fraud or intentional misrepresentation. Risk Adjustment – The process of increasing or reducing payments to health plans to reflect higher or lower than expected spending. Risk adjusting is designed to compensate health plans that enroll a sicker population as a way to discourage plans from selecting only healthier individuals. Section 125 Plan – These plans are otherwise known as a “cafeteria plan” offered pursuant to Section 125 of the Internal Revenue Code. Its name comes from a set of benefit plans that allows employees to choose between different types of benefits, similar to the ability of a customer to choose among available items in a cafeteria, and the employees’ pretax contributions are not subject to federal, state, or Social Security taxes. Self-Insured Plan – The employer assumes the financial responsibility of health care benefits for its employees in a self-insured or self-funded plan. Employer sponsored self-insured plans typically contract with a third-party administrator to provide administrative services for the plan. Small Business Tax Credit – The health reform law includes a tax credit equal to 50 percent (35 percent in the case of tax-exempt eligible small employers) for qualified small employers that provide health coverage to their employees. The tax credit is available to employers with 25 or fewer employees with average annual wages of less than $50,000. Small Group Market – Businesses with typically 2-50 employees, or eligible employees depending on applicable state law, can purchase health insurance for their employees through this market, which is regulated by states. Tax Credit – An amount that a person or business can subtract from the income tax that they owe. If a tax credit is refundable, the taxpayer can receive a payment from the government to the extent that the credit is greater than the amount of tax they would otherwise owe. Tax Deduction – An amount that a person can subtract from adjusted gross income when calculating the taxes that they owe. Generally, people who itemize deductions can deduct the portion of medical expenses, including health insurance premiums, that exceeds 7.5% of their adjusted gross income. Under health reform, the threshold for deducting medical expenses increases to 10% in 2013 (this increase is waived for individuals 65 and older for tax years 2013-2016). Value-Based Purchasing – A payment reform which provides bonuses to hospitals and other providers based upon their performance against quality measures. Wellness Plan/Program – An employer program to improve health and prevent disease

The President earlier today has signed The Health Care and Education Affordability Reconciliation Act of 2010, a historic health care reform that’s been 14 months in the making. This is after Sunday’s Congressional passage by the slim margins of 219-212.

The Bill for the most part follows the President’s version of the Reform Health Bill which tweaked measures such as elimination of Nebraska’s politically wrangled special Medicaid deal, delays on Cadillac Tax enactment and the establishment of a new Health Insurance Rate Authority to give guidance and oversight to states and monitor insurance market behavior. “If a rate increase is unreasonable and unjustified, health insurers must lower premiums, provide rebates, or take other actions to make premiums affordable.” The 21% Medicare cuts to providers were rescinded.

Children under 19 with certain pre-existing conditions could not be barred from coverage.

Dependent children will be allowed to continue coverage on their parents’ plans until age 26 as long as they are not eligible for coverage from an employer. Previously, this applied only to full-time students usually up to the age of 23. Dependents previously dropped because they no longer met the old coverage requirements can be picked up by parents’ plans. At least some insurers will be charging adult children the full rate for an individual rather than including them in the family or employee and child rate. This may or may not be beneficial depending on the situation.

Subsidies for Medicare Advantage will be cut but the so called donut hole under the Medicare Drug Plan would be closed. Seniors getting a prescription drug benefit under Medicare will get $250 later this year under the reconciliation bill. And starting this year, Medicare beneficiaries can get some free preventive services like routine cancer screenings.

The bill creates a temporary pool for “high risk” uninsured. That is, individuals who currently have no coverage due to a pre-existing condition, and who have been uninsured for at least six months, would qualify for coverage under a government plan until the other provisions regulating coverage for pre-existing conditions kick in.

There will be no lifetime limits on coverage paid out under insurance plans.

Certain tax credits will also go into effect for small businesses.

Long Term Changes:

Some medical devices will be newly taxed. Same with drug makers.

Beginning in 2013, income over $200,000 for individuals and $250,000 a year for couples would be hit with a 2.35 percent Medicare payroll tax instead of the existing 1.45 percent rate. Those upper incomes would also see 3.8 percent more in taxes on unearned income such as stock dividends and interest income above the thresholds.

By 2013, employers will have to redesign their flexible spending accounts to impose a $2,500 annual limit on contributions. There is no limit now, though employers typically impose limits between $4,000 and $5,000.

In 2014, citizens will be required to have acceptable coverage or pay a penalty of $95, $325 in 2015, $695 (or up to 2.5 percent of income) in 2016. Families will pay half the amount for children, up to a cap of $2,250 per family. After 2016, penalties are indexed to Consumer Price Index.

in 2014, a new affordability test will kick in that could result in employers facing assessments unless they redesign their plans. If the premium paid by an employee exceeds 9.5% of their income and the employee uses federal health insurance premium subsidies to purchase coverage through new state health insurance exchanges, the employer would have to pay an assessment of $3,000 for that employee.

In 2014, employers with at least 50 employees that do not offer coverage will pay a tax of $2,000 for each employee without coverage. However, in determining the assessment, an employer’s first 30 employees would be excluded from the calculation. Taking the case of an employer with 100 employees that did not offer coverage, for example, its assessment would be 70 times $2,000.

So-called Cadillac health plans would also get dinged. Employer-sponsored plans worth $10,200 for individuals and $27,500 for families would be hit with a 40% excise tax starting in 2018.

Individual Mandate:

All individuals will be required to have health insurance, with some exceptions, beginning in 2014. Those who do not have coverage will be required to pay a yearly financial penalty of the greater of $695 per person (up to a maximum of $2,085 per family), or 2.5% of household income, which will be phased-in from 2014-2016. Exceptions will be given for financial hardship and religious objections; and to American Indians; people who have been uninsured for less than three months; if the lowest cost health plan exceeds 8% of income; and if the individual has income below the poverty level ($10,830 for an individual and $22,050 for a family of four in 2009).

Premium subsidies will be provided to families with incomes between 100-400% of the poverty level (or $22,050 to $88,200 for a family of four in 2009) to help them purchase insurance through the Exchanges. These subsidies will be offered on a sliding scale basis and will limit the cost of the premium to between 2% of income for those between 100-133% of the poverty level to 9.8% of income for those between 300- 400% of the poverty level.

Employer Requirements: There is no employer mandate but employers with more than 50 employees will be assessed a fee of $2000 per full-time employee (excluding the first 30 employees from the assessment)

Employers that offer coverage will be required to provide a free choice voucher to employees with incomes below 400% of the poverty level if their share of the premium cost is between 8-9.8% of income and who choose to enroll in a plan in an Exchange. Employers that offer a free choice voucher will not be subject to the above penalty.

Large employers (more than 200 employees) that offer coverage will be required to automatically enroll employees into the employer’s lowest cost premium plan if the employee does not sign up for employer coverage or does not opt out of coverage.

No employer may impose a waiting period that exceeds 90 days

Small Business Tax Credit

Provides a two year tax credit to small businesses (less than 25 employees) with aver annual wages of less than $40,000 that purchase health insurance with the tax credit.

For tax years 2010 to 2013, the tax credit would be up to 35% of the employer’s contribution toward the employee’s health insurance premium if the employer contributes at least 50% of the total premium cost.

For tax years 2014 and later, for eligible businesses that purchase through the Exchanges, the tax credit would be up to 50% of the employer’s contribution toward the employee’s premium if the employer contributes at least 50% of the employee’s total premium cost.

The full credit will be available to employers with 10 or few employees and average annual wages of $25,000 and less, the credit phases out as firm size and wages increase.

American Health Benefit Exchanges

States will create the American Health Benefits Exchanges where individuals can purchase insurance and separate exchanges for small employers to purchase insurance. These new marketplaces will provide consumers with information to enable them to choose among plans. Premium and cost-sharing subsidies will be available to make coverage more affordable.

subsidies will only be available to those without other coverage or whose share of the premium for coverage offered by an employer exceeds 9.8% of their income. Small businesses with up to 100 employees can purchase coverage through the Exchange.

the Office of Personnel Management, which administers the Federal Employees Health Benefit Program, will contract with private insurers to offer at least two multi-state plans in each Exchange, including at least one offered by a non-profit entity. In addition, funds will be made available to establish non-profit, member-run health insurance CO-OPs in each state

Plans in the Exchanges will be required to offer benefits that meet a minimum set of standards. Insurers will offer four levels of coverage that vary based on premiums, out-of-pocket costs, and benefits beyond the minimum required plus a catastrophic coverage plan.

Premium subsidies will be provided to families with incomes between 100-400% of the poverty level (or $22,050 to $88,200 for a family of four in 2009) to help them purchase insurance through the Exchanges. These subsidies will be offered on a sliding scale basis and will limit the cost of the premium to between 2% of income for those between 100-133% of the poverty level to 9.8% of income for those between 300- 400% of the poverty level.

Cost-sharing subsidies will also be available to people with incomes between 100-200% of the poverty level to limit out-of-pocket spending.

Broker Role – HHS Secretary is required to “establish procedures under which a State may allow agents and brokers to enroll individuals” in Exchanges.

Beginning in 2014, the legislation allows states the option of merging the individual and small group markets within the Exchanges.

A more comprehensive chart is available through NAHU (National Association of health Underwriters).

Several states have already challenged this law as an over extension of Federal powers. Additionally, the requirement of mandating an individual to buy insurance is not so clear.

Many additional questions will arise such as:

-How will plans with Federal minimum standards reconcile with progressive states like NY that have numerous state mandates already? -Afterall, a Healthy NY plan can operate commercially without mandates that an ordinary group plan must comply with? -What happens to community rated states like NY? -Will they drop this rating methodology altogether? -Since there will be no longer pre-existing conditions is it just cheaper for an individual to just withdraw pay the penalty and then hop in when in need of coverage?

Lastly and importantly, the bending of the cost curve is weak. There is language, however, on attacking fraud & billing abuses as well successful Pharmaceutical concession for Medicare Part D. But Rome was not built in a day and this lays the foundation for a path of extending coverage to as many people as possible. Heavy topics such as Tort Reform, exorbitant malpractice insurance, federal medical reimbursements cuts must wait for another day.

To prepare for 2024 open enrollment, health plan sponsors should be aware of the legal changes affecting the design and administration of their plans for plan years beginning on or after Jan.

A little-known requirement but most important under the Affordable Care Act (ACA) is for Health Insurers must waive their minimum employer contribution and employee-participation rules once a year. ACA requires a one-month Special Open Enrollment Window for January 1st coverage. FEDERAL JAN 1st SMALL GROUP ANNUAL OPEN ENROLLMENT WAIVER. For more help w/Special Open Enrollment Window info@360peo.com or (855)667-4621

A little-known requirement but most important under the Affordable Care Act (ACA) is for Health Insurers must waive their minimum employer-contribution and employee-participation rules once a year. ACA requires a one-month Special Open Enrollment Window for January 1st coverage. FEDERAL JAN 1st SMALL GROUP ANNUAL OPEN ENROLLMENT WAIVER. For more help w/Special Open Enrollment Window info@360peo.com or (855)667-4621

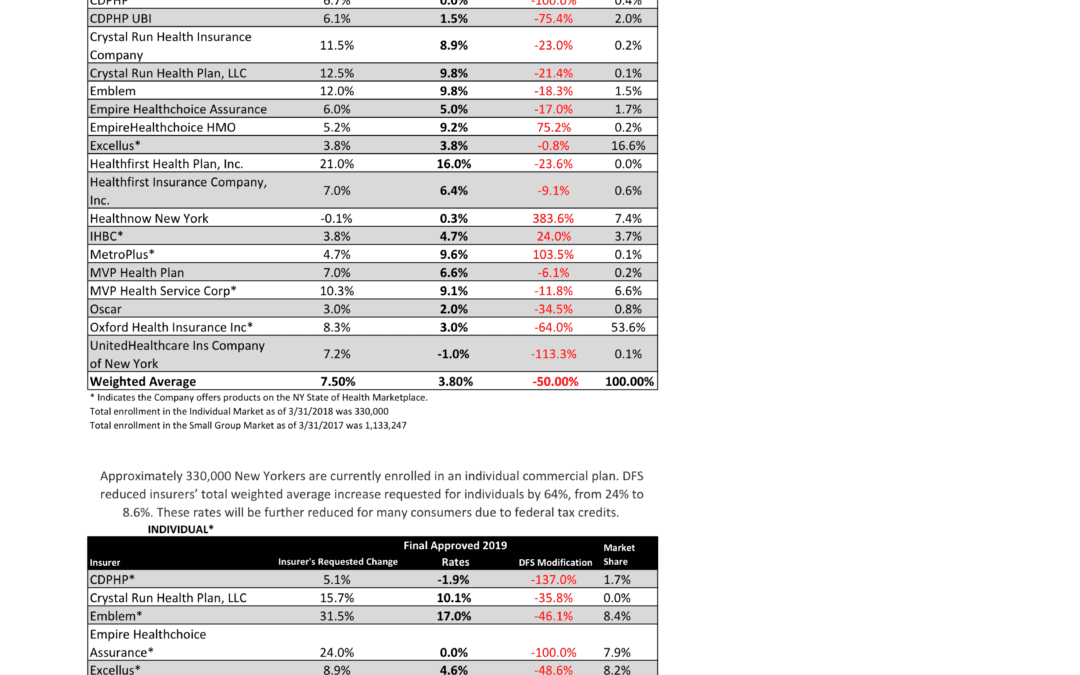

NYS has approved 2019 Final Rates last Friday. Small group rates will increase 3.8% and 8.6% for individuals.

As per NY State Law, Health Insurers are required to send out early notices of rate request filings to groups and subscribers see original –NYS 2019 Rate Requests. Despite only 3 months of mature claims data experience for 2018 health insurers’ original requests were noticeably below average 7.5% for small group and 24% for individuals. Ultimately NYS reduced this request substantially by approximately 50%.

Experts are concerned over the long term effects. Example, the Individual mandate was removed last December by Presidential order. Without the Mandate anyone can drop insurance without penalty. A comparable take away for similar auto insurance industry would be something like this -Drivers ought not be mandated to buy auto insurance as its a profit scheme by Insurers. While a popular decision this will hardly bend the curve long term and reduce competition. Furthermore, the new order of Selling Across State lines makes NYS most unwelcoming.

OTHER STATES

Insurers have been filing to sell Obamacare plans that will go into effect in 2019, and in some states they appear to be pricing in for the fact that the mandate is going away next year. Other states are seeing mild increases, but that is in part because they saw significant hikes for the previous year.

Insurers have concluded that fewer people will enroll without the mandate than otherwise, so in some places they are pricing their plans higher based on the assumption that sicker people will be left behind, which will increase medical costs for those left. It is well worth pointing out that in recent years the loss federal risk reinsurance corridor funds account for 5.5 percent of the rate increase.

How are neighboring States doing?

In NJ, not that bad. Last year the average increase were 5.5% for small groups and some popular plans such as Horizon Blue Cross Blue Shield’s OMINA increasing only 4.8% increase. This year the increase is only 5.2. Other insurers offering EPO and HMO plans in the individual market for 2019 include Oscar Health and Oxford Health Plans.

With individual mandate repeal fewer people will buy health insurance raising the prices for those who do. NJ Banking and Insurance Department officials said premium prices would have increased, on average, by 12.6 percent.

For CT market, on the other hand, things are much worse at least for the individual marketplace with average 25% rate increases last year. The 2019 proposed rate increases for both the individual and small group market are, on average lower, than last year: The proposed average small group rate increase request is a 10.22 percent and ranges from -5.0 percent to 21.1 percent. This compares to the average increase request of 18.06 percent requested last year.The proposed average individual rate increase request is 12.3 percent and ranges from -10.9 percent to 31.0 percent. This compares to the average increase request of 25.51 percent requested last year.

Final plan rates in New Jersey & CT will be finalized and released in the fall, state officials said. ACA open enrollment begins Nov. 1

Trend: Trend is a factor that accounts for rising health care costs, including the cost of prescription drugs, and the increased demand for medical services.

Uncertainty in Washington:

Removal of penalty for individual mandate: The elimination of the penalty means that individuals who are typically younger and healthier would have no inducement to participate in the insurance pool, which could further destabilize the market. Lack of participation shrinks the pool and increases the cost of insurance to the remaining members.

Short-duration health plans and Association Health Plans: Still pending are final federal regulations on non-ACA compliant short-duration plans, which may have implications for the ACA risk pool. Also, Connecticut along with other state insurance regulators, are awaiting clarification from the federal government on new federal regulations allowing association health plans, which could further shrink the ACA risk pool.

A bipartisan group of congressional representatives has discussed an agreement to extend and guarantee the payments, but it’s unclear whether they could do so by the new filing deadline of Sept. 5. A lawsuit filed by Congress against the Obama administration to challenge the payments is still pending. In addition, Trump has repeatedly threatened to withhold payments to insurers that reduce cost-sharing – deductibles, copays and coinsurance – paid by low-income customers. More than half of New Jersey’s marketplace customers receive that assistance, and without it, most would be unable to afford coverage.

Finally, a tax on health insurance premiums has been reinstated in 2018 after a one-year “tax holiday” approved by Congress for 2017. That contributed 2.3 percent to the rate hikes that insurers requested for 2019 and for 2019

SMALL GROUP MARKET VS. INDIVIDUAL MARKET

Importantly, small group market is still more advantageous than individual markets unless one gets a sizable low-income tax credit. Overall, about 350,000 individual plan consumers will be affected by the price hike, while more than a million users will be hit by higher small group fees. Last year, Blue Cross Blue Shield released a study showing Obamacare user costs were 22 percent higher than people with employer-sponsored health plans, while UnitedHealthplans to exit most Exchanges see – Breaking: Oxford Exits Metro Indiv & Oxford Liberty HMO 2017.

The correct approach for a small business in keeping with simplicity is a Private Exchange and with our large buying group PEO partnerships. This is a true defined contribution empowering employees with a choice of leading insurers offering paperless technologies integrating HRIS/Benefits/Payroll. Both employee and employers still gain tax advantage benefits under the business. Also, the benefits, rates and network size are superior under a group plan as the risk are lower for small group plans than individual markets.

Learn how a PEO Partnership can help your group please contact us at info@360PEO.com or (855)667-4621.

President Trump signed an Executive Order on Jan 20 Minimizing the Economic Burden of the Patient Protection and Affordable Care Act Pending Repeal. As a practical matter, he can’t repeal it “line-by-line on day one” of his Presidency. So he did the next best thing: sign an Executive Order.

While lawmakers work on a repeal and replacement plan, here are 5 things you should know. The executive order will:

End the individual mandate.

Expand Medicaid waivers and provide states more flexibility to implement healthcare programs.

Encourage the creation of interstate insurance markets to “the maximum extent permitted by the law.”

Remove ACA taxes, including some placed on health insurance and pharmaceutical companies, in addition to waiving PPACA taxes, fees, and penalties.

Grant leaders of the Department of Health and Human Services (HHS) and other agencies to exercise greater discretion. This includes the ability to waive, defer, or grant an exception to any provision that would impose a fiscal burden on a state or place a financial or regulatory burden (cost, fee tax, penalty) on individuals, families, healthcare providers, and patients.

We will soon know whether the Executive Order is more symbolic or has practical effects. Employers should continue to comply with the provisions in current law, until official guidance provides otherwise.

On Tuesday The 21st Century Cures Act Passed and signed by President Obama. The ‘Act” has numerous components but the the greatest impact on small business is the HRA ( health reimbursement arrangement) component.

The Cures Act allows small employers to reimburse individual health coverage premiums up to a dollar limit through HRAs called “Qualified Small Employer Health Reimbursement Arrangements” (QSE HRA). This provision will go into effect on January 1, 2017.

The IRS previously limited Employer reimbursement of individual premiums in light of the requirements of the Patient Protection and Affordable Care Act (ACA). For many years, employers had been permitted to reimburse premiums paid for individual coverage on a tax-favored basis, and many smaller employers adopted this type of an arrangement instead of sponsoring a group health plan. However, these “employer payment plans” are often unable to meet all of the ACA requirements that took effect in 2014, and in a series of Notices and frequently asked questions (FAQs) the IRS made it clear that an employer may not either directly pay premiums for individual policies or reimburse employees for individual premiums on either an after-tax or pre-tax basis. This was the case whether payment or reimbursement is done through an HRA, a Section 125 plan, a Section 105 plan, or another mechanism.

Who is eligible?

The Cures Act now allows employers with less than 50 FT employees (under ACA counting methods) who do not offer group health plans to use QSE HRAs that are fully employer funded to reimburse employees for the purchase of individual health care.

What are the funding limits?

The reimbursement cannot exceed $4,950 annually for single coverage, and $10,000 annually for family coverage. The amount is prorated by month for individuals who are not covered by the arrangement for the entire year. Practically speaking, the monthly limit for single coverage reimbursement is $412, and the monthly limit for family coverage reimbursement is $833. The limits will be updated annually.

Impact on Individual Subsidy Eligibility?

For any month an individual is covered by a QSE HRA/individual policy arrangement, their subsidy eligibility would be reduced by the dollar amount provided for the month through the QSE HRA if the QSE HRA provides “unaffordable” coverage under ACA standards.

Employees applying for coverage on federal or state health insurance exchanges will need to disclose the amount that the employer is making available via the HRA. That amount will be used by the exchange in calculating whether an employee’s household income exceeds ACA affordability thresholds (2017 – 9.69 % of household income), as well as determining subsidy amounts for those that meet the eligibility requirements. Those employees eligible for a subsidy will have their monthly amount reduced by the monthly HRA amount available through their employer.

If the QSE HRA provides affordable coverage, individuals would lose subsidy eligibility entirely. Caution should be taken to fully education employees on this impact.

COBRA and ERISA Implications?

QSE HRAs are not subject to COBRA or ERISA.

Annual Notice Requirement?

The new QSE HRA benefit has an annual notice requirement for employers who wish to implement it. Written notice must be provided to eligible employees no later than 90 days prior to the beginning of the benefit year that contains the following:

A statement to the employee that it is their responsibility to provide the federal or state health insurance exchangewith the amount being provided in HRA funds, as this amount will be used by the exchange when calculating need based premium assistance.

A statement that if the employee is not covered by minimum essential coverage for any month of the tax year, they could be subject to a penalty under the Individual Mandate provisions of the ACA.

Failure to provide this notice will result in a penalty to the employer of $50 per applicable employee, up to a $2,500 maximum per calendar year. Transition relief is available for plans starting in the first quarter 2017 – they will have until April 1, 2017 to provide notices to employees.

Record-keeping, IRS Reporting?

Because QSE HRAs can only provide reimbursement for documented healthcare expense, employers with QSE HRAs should have a method in place to obtain and retain receipts or confirmation for the premiums that are paid with the account. Employers sponsoring QSE HRAs would be subject to ACA related reporting with Form 1095-B as the sponsor of MEC. Money provided through a QSE HRA must be reported on an employee’s W-2 under the aggregate cost of employer-sponsored coverage. It is unclear if the existing safe harbor on reporting the aggregate cost of employer-sponsored coverage for employers with fewer than 250 W-2s would apply, as arguably many of the small employers eligible to offer QSE HRA’s would have fewer than 250 W-2s.

Individual Premium Reimbursement Prohibitions

Outside of the exception for small employers using QSE HRAs for reimbursement of individual premiums, all of the prior prohibitions from IRS Notice 2015-17 remain. There is no method for an employer with 50 or more full time employees to reimburse individual premiums, or for small employers with a group health plan to reimburse individual premiums. There is no mechanism for employers of any size to allow employees to use pre-tax dollars to purchase individual premiums. Reimbursing individual premiums in a non-compliant manner will subject an employer to a penalty of $100 a day per individual they provide reimbursement to, with the potential for other penalties based on the mechanism of the non-compliant reimbursement.

For analysis if this works for your small business? Please contact our payroll and reimbursement team on your HR/Payroll/Compliance needs at Millennium Medical Solutions Corp (855)667-4621 for immediate answers.