by admin | May 1, 2015 | Health Care Reform, healthcare

Order Your Medical Records 5 Steps

Anyone who has moved has been confronted with the question “How to Order Your Medical Records?”. Requesting your medical records may seem complex at first its simpler than one thinks.

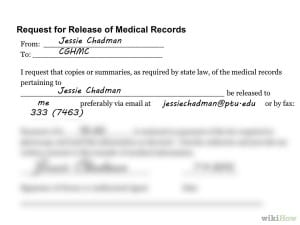

1. Get a HIPAA release form. The federal law known as HIPAA entitles every person the right to access his or her medical records, receive copies of them, and request amendments to them.

2, Select your records. I would make this at least one month no more than 2 months This will give the office plenty of time to get you the records together. Specify the effective date, medical providers name, address, your name, address, medical record number ( you can get this from the staff) any identification numbers; i.e., Social Security Number or insurance ID number.

3. Submit forms. Fill out an authorization form giving one medical provider permission to share your records with another.Mark on that form which types of records you want included. Pay any fees that result.

4. Wait. The turnaround time under HIPAA can be 30 days. Most facilities, however, do not require that much time—many can fulfill a request in five to 10 days. Individual state laws may also dictate how quickly a facility must fulfill a request.

5. Follow up. In an imperfect world things can go wrong. What to do?

If your doctor has moved, you should be able to find your records at the practice she left. If that practice was affiliated with a hospital, the records may be housed within the hospital’s records system.

If your old provider says the records have been sent, but your new doctor’s office hasn’t received them, ask that they be re-sent. Doublecheck to make sure the old provider has the right contact information for your new one. You may find getting someone from your new doctor’s office involved could help. Having a nurse advocate for you, for instance, could put you in a better position.

If you’ve tried everything and are getting nowhere, offer to pick up the records yourself (but be aware that this may cost you), ask to speak with a manager or your doctor directly, or, as a final resort, contact your state medical board to file a complaint. This step is rarely necessary, but even suggesting you’ll have to go this route could get things moving on your request.

The Value of Requesting Your Records

There are many good reasons to request a copy of your medical records. Physicians don’t always share complete patient information or exchange a patient’s health records, so if a patient is seeing a new provider it is beneficial to ensure a copy of their record is sent to the new physician.. Also, it is beneficial for patients or caregivers dealing with multiple doctors and facilities to have all medical records in one place, which can then be used by providers to ensure thorough care.

Reviewing your record is an important way to ensure your provider has complete, correct, and up-to-date information, such as your known allergies. If you find information in your record that is incorrect or that you disagree with, contact the provider’s Health Info Management department.

Finally, it can be good for your health to keep a copy of your medical records, . Keeping an up-to-date copy of your health information will prevent redundant care, like repeat tests, and give all your physicians essential information about your health.

by admin | Jul 2, 2013 | Health Care Reform, Health Exchanges, individual health insurance, MEDICARE, Obamacare, State Exchanges

Obamacare 1.0: Rolling Brown Outs?

The sheer technological volume of it all could bring “rolling brown outs” similar to electrical grids. Try to imagine a scenario of credit union Experien working with IRS then Social Security & Center for Medicare & Medicaid Services’s dated mainframe computer system while balancing HIPAA and privacy sensitive information. All this while millions of people converge simultaneously onto the information highway. Visualize all of the U.S. Daily Commuters driving into Manhattan today. As reported below by Reuters’ Sharon Begley Obamacare 1.0: States brace for Web barrage when reform goes live: “Obamacare, formally known as the Patient Protection and Affordable Care Act (ACA), could fail for many reasons, including participation by too few of the uninsured and a shortage of doctors to treat those who do sign up. But because its core is government-run marketplaces selling health insurance online, the likeliest reason for failure at the opening bell is information technology snafus, say experts who are helping with the rollout.” By Sharon Begley

NEW YORK | Sun Jun 30, 2013 7:03am EDT

(Reuters) – About 550,000 people in Oregon do not have health insurance, and Aaron Karjala is confident the state’s new online insurance exchange will be able to accommodate them when enrollment under President Barack Obama’s healthcare reform begins on October 1.

What Karjala, the chief information officer at “Cover Oregon,” does worry about, however, is what will happen if the entire population of Oregon – 3.9 million – logs on that day “just to check it out,” he said. Or if millions of curious souls elsewhere, wondering if Oregon’s insurance offerings are better than their states’, log on, causing Cover Oregon to crash in a blur of spinning hourglasses and color wheels and an epidemic of frozen screens.

Multiply that by another 49 states and the District of Columbia, all of which will open health insurance exchanges under “Obamacare” that same day, and you get some idea of what could go publicly and disastrously wrong.

Obamacare, formally known as the Patient Protection and Affordable Care Act (ACA), could fail for many reasons, including participation by too few of the uninsured and a shortage of doctors to treat those who do sign up. But because its core is government-run marketplaces selling health insurance online, the likeliest reason for failure at the opening bell is information technology snafus, say experts who are helping with the rollout.

Although IT is the single most expensive ingredient of the exchanges, with eight-figure contracts to build them, experts expect bugs, errors and crashes. In April, Obama himself predicted “glitches and bumps” when the exchanges open for business.

“This is a 1.0 implementation,” said Dan Maynard, chief executive of Connecture, a software developer that is providing the shopping and enrollment functions for several states’ insurance exchanges. “From an IT perspective, 1.0’s come out with a lot of defects. Everyone is waiting for something to go wrong.”

Two states that intended to build their own exchanges, Idaho and New Mexico, announced this spring that because of the tight timeline and daunting challenges they would have the federal government operate their IT systems.

“Nothing like this in IT has ever been done to this complexity or scale, and with a timeline that put it behind schedule almost before the ink was dry,” said Rick Howard, research director at the technology advisory firm Gartner.

WHAT COLOR WAS YOUR VOLVO?

The potential for problems will begin as soon as would-be buyers log onto their state exchange. They’ll enter their name, birth date, address and other identifying information. Then comes the first IT handoff: Is this person who she says she is?

To check that, credit bureau Experian will check the answers against its voluminous external databases, which include information from utility companies and banks on people’s spending and other history, and generate questions. The customer will be asked which of several addresses he previously lived at, for example, whether his car has one of several proffered license plate numbers, and what color his old Volvo was.

It’s similar to the system that verifies identity for accessing personal Social Security information. If someone gets a question wrong, he will be referred to Experian’s help desk, and if that fails may be asked to submit documentation to prove he is who he claims to be.

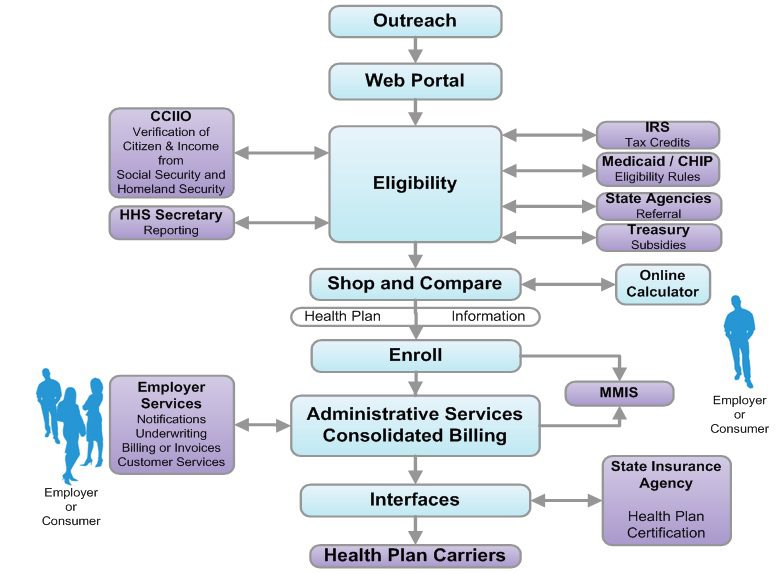

The next step is determining if the customer is eligible for federal subsidies to pay for insurance. She is if she is a citizen and her income, which she will enter, is less than four times the federal poverty level. To verify this, the exchange pings the “federal data services hub,” which is being built by Quality Software Services Inc under a $58 million contract with the Centers for Medicare & Medicaid Services (CMS).

The query arrives at the hub, which does not actually store information, and is routed to online servers at the Internal Revenue Service for income verification and at the Department of Homeland Security for a citizenship check.

The answers must be returned in real time, before the would-be buyer loses patience and logs off. If the reported income doesn’t match the IRS’s records, the applicant may have to submit pay stubs.

These federal computer systems have never been connected before, so it’s anyone’s guess how well they’ll communicate.

“The challenge for states,” said Jinnifer Wattum, director of Eligibility and Exchange Solutions at Xerox’s government healthcare unit, is that they have to build “the interfaces needed with the federal data services hub without knowing what this system will look like.” That makes the task akin to making a key for a lock that doesn’t exist yet.

CMS’s contractors are working to finish the hub, but “much remains to be accomplished within a relatively short amount of time,” concluded a report from the Government Accountability Office (GAO), the investigative arm of Congress, in June. CMS spokesman Brian Cook said the hub would be ready by September, and that the beta version had been tested for its ability to interact with the exchanges Oregon and Maryland are building.

The federal hub has to verify even more arcane data, such as whether the insurance offered to a buyer through his job is unaffordable, in which case he may qualify for federal subsidies, and whether the buyer is in prison, in which case she is exempt from the mandate to purchase insurance.

If someone’s income qualifies him for Medicaid, or his children for the Children’s Health Insurance Program (CHIP), software has to divert him from the ACA exchange and into those systems. Many of the computers handling Medicaid and CHIP enrollment are, as IT people diplomatically put it, “legacy systems,” meaning old, even decades old.

Many are mainframes, lacking the connectivity of cloud computing. They typically process eligibility requests in days, not seconds.

The legacy systems “rely on daily or weekly batch files to pass information back and forth,” and often require follow-up phone calls, said Wattum of Xerox, which is working to configure Nevada’s exchange so it can interface with the federal hub.

‘NO WRONG DOOR’

A “we’ll call you” message is unacceptable under Obamacare, which has a “no wrong door” goal: A buyer must never come to a dead end. If she is diverted to Medicaid, for instance, she must not be required to resubmit information, let alone wait a week for an answer about whether she’s now enrolled.

State IT systems must therefore “be interoperable and integrated with an exchange, Medicaid, and CHIP to allow consumers to easily switch from private insurance to Medicaid and CHIP,” said an April report from the Government Accountability Office (GAO), the investigative arm of Congress.

To make all those systems communicate, the state exchanges must either develop entirely new systems or use application programming interfaces (APIs) that work with the legacy systems to exchange data in real time. APIs are programming instructions for accessing Web-based software applications.

GAO’s Stan Czerwinski compares the necessary connectivity to adapters that let Americanelectronics work with European outlets.

State officials told the GAO that verifying eligibility, enrolling buyers and interfacing with legacy systems are the most “onerous” aspects of developing their exchanges, “given the age and limited functionality of current state systems.”

A key goal for exchange officials is keeping would-be buyers in the portal so they don’t give up and use a state’s ACA call center, which could quickly be swamped.

To avoid this, Oregon brought in potential users to test design prototypes, recorded what people did and where they had trouble, and tweaked the consumer interface to make it as user-friendly as possible, said Karjala.

“Even with that, if you have a family of four and you’re eligible for a tax credit to offset your premium,” he said, “you could be sitting at the computer for a long time.”

What everyone hopes to avoid is a repeat of the early days of the Medicare prescription-drug program in 2006. Some seniors who tried to sign up for a plan were mistakenly enrolled in several, while others had the wrong premium amounts deducted from their Social Security checks.

Another challenge is capacity. Websites regularly crash when too many people try to access them.

“I had no choice but to be extremely conservative” in estimates of how many simultaneous users Cover Oregon has to be prepared for, Karjala said. “Building capacity is the only way to avoid the spinning hourglass or the site freezing, so in our performance testing we’re seeing what happens if the whole U.S. population came to Cover Oregon to check it out.”

This summer, state exchanges will test their ability to communicate with the federal data hub, whose security frameworks and connectivity protocols are still works in progress. But whether Obamacare 1.0 flies won’t be known until the new health plans take effect on January 1. Robert Laszewski, president of Health Policy and Strategy Associates Inc, a consulting firm, said he wouldn’t be surprised if some patients showing up at doctors’ offices next year with Obamacare policies are told their insurers never heard of them.

(Additional reporting by Caroline Humer; Editing by Michele Gershberg and Prudence Crowther)