In an unexpected announcement pre-July 4th the big news was Obamacare Employer Mandate Delayed with penalties under the Affordable Care Act (ACA) until 2015. The mandate also known as the “Employer Shared Responsibility” requires employers with 50 or more FTEs to offer affordable health insurance coverage to their workers or face financial penalties for not doing so. Those penalties would originally have been applied beginning in 2014.

There has been a follow up guidance issued last week July 9th by the IRS. According to the IRS, the delay will give employers more time to prepare for the change in how health insurance is provided and will also give the Obama Administration time to simplify the insurance-related reporting requirements that employers face. This transition relief appears to come with “no strings attached.” Although the IRS guidance encourages employers to voluntarily comply with the employer mandate and maintain or expand health care coverage in 2014, the IRS will not impose penalties for a failure to do so.

Although the IRS guidance encourages employers to voluntarily comply with the employer mandate and maintain or expand health care coverage in 2014, the IRS will not impose penalties for a failure to do so.Notably, the guidance issued on July 9th also does not require employers to make “good faith” efforts to comply. As a result of this transition year, employers will have the option of deciding to what extent (if any) they will continue efforts to comply with the employer mandate during 2014.

Employers who intended to rely on one of the transition rules previously announced for 2014 should keep in mind that the latest IRS guidance does not provide special transition rules for 2015. Other group health plan requuirements still apply as discussed in our prior blog Essential Health Benefits Not Delayed.

This means that for plan years beginning on and after January 1, 2014, all group health plans must:

Eliminate all pre-existing condition exclusions (regardless of age);

Maximum Cost Sharing Deductible to $2,000/individual ($4,000/family); limit in-network out-of-pocket maximums to $6,350/individual ($12,700/family)

Individual Mandate Still Applies. individuals will still be required to obtain health care coverage or pay a penalty for each month they do not have coverage, beginning January 1, 2014

Exchanges (Marketplaces) Open for Enrollment October 1, 2013.

The IRS notice makes it clear that individuals who enroll in coverage on the marketplaces will continue to be eligible for a premium tax credit if their household income is within a specified range and they are not eligible for other minimum essential coverage.

Employers Must Send Notice of Exchanges (Marketplaces) Before October 1, 2013. These notices must be sent to current employees by October 1, 2013. Then, beginning October 1, 2013, employers must send this notice to new hires within 14 days of their start date.

New taxes still apply – Patient Centered Outcomes Research Institute (PCORI) excise taxes and transitional reinsurance program fees;HRA/HSA/FSA clients also pay a monthly $1/employee tax.

We will continue to monitor ACA developments and will provide you relevant updated information when available. In the meantime, please visit to view past blogs and Legislative Alerts at https://360peo.com/feed.

With only 6 month away from full implementation of 2014 Patient Protection Affordability Care Act (PPACA) employers are understandably uncertain. Below are Health Care reform – five things employers can do now to prepare and take action.

UPDATE JULY 2nd: Since blog posting the President Administration has delayed 1 year Employed Shared Responsibility Mandate i.e. Pay or Play to Jan 2015.

1. Employee Communications

Employers must notify employees of the online insurance marketplace known as a Healthcare Exchange. Recently released federal guidelines require employers to notify their workers of eligibility requirements for their state exchange starting Oct. 1, 2013 Open Enrollments for Jan 2014 effective date. To the relief of many, the U.S. Labor Department also provided model notices that employers can give to their workers, which eliminates the need to develop their own notifications.

Additionally, Employers sponsoring a health plan must give employees a Summary of Benefits and Coverage (SBC). The purpose of the Summary of Benefits and Coverage, or SBC, is to present benefits and coverage information in clear language and in a consistent format. Inspired by the Nutrition Facts Label on packaged food, theSBC (pdf) includes two medical scenarios: having a baby and managing Type II diabetes. It estimates how much a patient would pay for medical care in each scenario with specific insurance plans.

It’s the employer’s responsibility to distribute the SBCs to employees.

This requirement applies to health plan renewals after Sept. 23, 2012.

Department of Labor will NOT impose penalties for non-compliance with the SBC notice during the first year as long as employers show a “good faith” effort to comply. Read the FAQ on SBC and ACA pdf here.

2. Determining which Employers must offer health care.

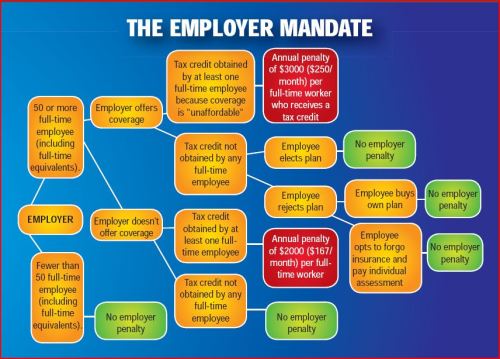

Because employers with 50 full-time equivalents face penalties for not providing affordable, minimum value insurance an employer should know whether it is subject to these requirements or not. Common law employees of the employer and any commonly controlled company must be counted. Employers with temporary or leased employees will want to discuss with their advisors whether these employees will be considered “common law employees” for purposes of determining how many FTEs an employer has. Employers with employees who are paid based on unique payment models (stipends, work product, etc) will want to discuss how to calculate these employee hours with their benefits advisors.

Employers with 50 or more employees will incur penalties of up to $2,000 per employee if they cancel their existing health care program (which up until 2014 would be considered an optional benefit to provide). They will also incur penalties if their plan is too costly, and they do not meet the affordability standards.

Employers with less than 50 employees will not incur penalties if they cancel their health care plan, and that decision will need to be made on a business by business basis. They can also choose to offer partial coverage and contribute up to the minimum 50% of single coverage not to exceed 9.5% employee

The good news is Employers can subtract 30 FT employees. This portion is known as the Employer “play or pay” option. Specific case example and details are found at Pay or Play Employer Guide.

To encourage businesses to offer health benefits to their employees, the federal government is offering tax credits to small businesses. These credits are available to an estimated 4 million small businesses, including nonprofits.The IRS has set up a web page with information: Small Business Health Care Tax Credit for Small Employers. The maximum “credit” (which offsets taxes dollar for dollar and is better than a “deduction” which reduces taxable income) is 35 percent of the amount an employer pays towards employee health insurance.

Who’s eligible?

To qualify, small employers must:

Have fewer than the equivalent of 25 full-time workers

Pay average annual wages below $50,000

Cover at least 50% of the cost of health care coverage for their workers

Because of the high wages paid in most industries in NY/NJ/CT Tri State, few small employers that provide coverage pay such a low average wage. Note, however, that the calculation of average wages and number of employees excludes the wages of an owner and his or her family members.

medicalsolutionscorp.com help clients gather the appropriate information and do a preliminary estimate of the credit amount. This information will help you and your accountant determine whether applying for the credit makes financial sense. Find out what the new tax credit could mean for your coverage. Call us at 855-667-4621.

4. Determine affordability

Beginning Jan. 1, 2014, an employer with 50 or more employees must pay a tax penalty if they either: a) Do not provide health insurance with minimum benefits or 60 percent of healthcare expenses; b) Require employees to contribute more than 9.5 percent of an employee’s household income for the health insurance and those employees obtain a government subsidy for coverage.

Companies will be required to pay $3,000 per employee without affordable coverage. (Note: there are a number of caveats that might affect the actual penalty paid, so consult your tax advisor.)

It is crucial to Understand the difference between FT and Full Time Equivalent. To determine the FTE (Full Time Equivalent) you must count FT and PT employees. Full Time Employees are those working 30 hours+/week.* The number of full-time employees excludes those full-time seasonal employees who work for less than 120 days during the year.4 The hours worked by part-time employees (i.e., those working less than 30 hours per week) are included in the calculation of a large employer, on a monthly basis, by taking their total number of monthly hours worked divided by 120.

For example, a firm has 35 full-time employees (30+ hours). In addition, the firm has 20 part time employees who all work 24 hours per week (96 hours per month). These part-time employees’ hours would be treated as equivalent to 16 full-time employees, based on the following calculation:

20 employees x 96 hours / 120 = 1920 / 120 = 16

Thus, in this example, the firm would be considered a “large employer,” based on a total full-time equivalent count of 51—that is, 35 full-time employees plus 16 full-time equivalents based on part-time hours.

In the coming months, Millennium Medical Solutions Inc will host seminars and will share information you’ll need to know as the countdown continues to October 1st.

Error: Contact form not found.

This blog is not intended to represent legal advise and one should consult with a tax and/or legal expert.

* IRC 4980H(c)(4)

Disclaimer: This blog is not intended to represent legal advise and one should consult with a tax and/or legal expert.

Many follow up questions on the postPay or Play Employer Guide have been raised. A Pay or Play FAQ hopefully adds some clarification.

Will I be required to offer health insurance coverage to my employees?

No. However, if you have at least 50 full-time employees, and you don’t offer coverage, you will owe a penalty starting in 2014 if any full time employee is eligible for and purchases subsidized coverage through an exchange. This penalty is called the “free rider” penalty.

We employ about 40 full-time employees working 30 or more hours per week and about 25 part-time or seasonal employees. So we are not subject to the employer mandate penalties, right?

You may be. The health reform law does not require you to provide coverage for employees working on average less than 30 hours per week (“part-time”). However, the hours worked by part time employees are counted to determine whether you have at least 50 full-time employee equivalents and therefore are subject to the employer mandate. This is done by taking the total number of monthly hours worked by part time employees (but not to exceed 120 hours for any one part-time employee) and dividing by 120 to get the number of “full time equivalent” employees. You would then add those “full-time equivalent” employees to your 40 full-time employees.

The hours worked by seasonal employees are also counted to determine whether you have at least 50 full-time employee equivalents and therefore are subject to the employer mandate. For purposes of determining whether you are a large employer, seasonal employees are workers who perform labor or services on a seasonal basis (i.e. exclusively performed at certain seasons or periods of the year and which, from its nature, may not be continuous or carried on throughout the year) for no more than 120 days during the taxable year and retail workers employed exclusively during holiday seasons. There is an exemption from the employer mandate that says you would not be considered to employ more than 50 full-time employees if:

Your workforce only exceeds 50 full-time employees for 120 days, or fewer, during the calendar year; and

The employees in excess of 50 who were employed during that 120-day (or fewer) period were seasonal workers.

Our workforce numbers go up and down during the year. How do we determine if we had at least 50 full-time employees on business days during the preceding calendar year?

For purposes of determining if you are a large employer, the formula requires the following steps:

1.Determine the total number of full-time employees (including any full-time seasonal workers) for each calendar month in the preceding calendar year;

2.Determine the total number of full-time equivalents (including non-full-time seasonal employees) for each calendar month in the preceding calendar year;

3.Add the number of full-time employees and full-time equivalents described in Steps 1 and 2 above for each month of the calendar year;

4.Add up the 12 monthly numbers;

5.Divide by 12. If the average per month is 50 or more, you are a large employer.

So if we offer coverage to our full-time employees, we will not have to pay a penalty?

Not necessarily. If you have at least 50 full-time employees and you offer coverage to at least 95% of your full-time employees, you are still subject to a penalty starting in 2014 if:

1.A full-time employee’s contribution for employee-only coverage exceeds 9.5% of the employee’s household income (Note: see below regarding a proposed affordability “safe harbor”) or the plan’s value is less than 60%; and

2.The employee’s household income is less than 400% of the federal poverty level; and

3.The employee waives your coverage and purchases coverage on an exchange with premium tax credits.

The penalty will be calculated separately for each month in which the above applies. The amount of the penalty for a given month equals the number of full- time employees who receive a premium tax credit for that month multiplied by 1/12 of $3,000.

We have more than 50 full-time employees so we are subject to the employer mandate penalties. How do we know which of our employees is considered “full-time” requiring us to pay a penalty if they qualify for premium tax credits at an exchange (if the employee has a variable work schedule or is seasonal)?

Through the end of 2014, for purposes of the employer mandate penalties, the guidance permits you to use a “look-back measurement period/stability period” safe harbor to determine which of your employees are considered full-time employees. You may use a standard measurement/stability period for ongoing employees, while using a different initial measurement/stability period for new variable and seasonal employees

How do the full-time employee safe harbors work for new hires?

They are generally based on the employee’s hours worked, or, the amount of hours the employee is reasonably expected to work as of their hire date.

New employee reasonably expected to work full-time (i.e. 30 or more hours per week)– If you reasonably expect an employee to work full-time when you hire them, and coverage is offered to the employee before the end of the employee’s initial 90 days of employment, you will not be subject to the employer mandate payment for that employee, if the coverage is affordable and meets the minimum required value.

New employee reasonably expected to work part-time (i.e. less than 30 hours per week)-– If you reasonably expect an employee to work part-time and the employee’s number of hours do not vary, you will not be subject to the employer mandate penalty for that employee if you don’t offer them coverage.

New variable hour and seasonal employees – If based on the facts and circumstances at the date the employee begins working (the start date), you cannot determine that the employee is reasonably expected to work on average at least 30 hours per week, then that employee is a variable hour employee. Because the term “seasonal employee” is not defined for purposes of the employer responsibility penalty, through 2014, you are permitted to use a reasonable, good faith interpretation of the term “seasonal employee”. The IRS has indicated that any interpretation of the term “seasonal” probably would not be reasonable if it included a working period of more than six months. Once hired, you have the option to determine whether a new variable hour or seasonal employee is a full-time employee using an “initial measurement period” of between three and 12 months (as selected by you).You would measure the hours of service completed by the new employee during the initial measurement period to determine whether the employee worked an average of 30 hours per week or more during this period. If the employee did work at least 30 hours per week during the measurement period, then the employee would be treated as a full-time employee during a subsequent “stability period,” regardless of the employee’s number of hours of service during the stability period, so long as he or she remained an employee. The stability period must be for at least six consecutive calendar months and cannot be shorter than the initial measurement period. If the employee then didn’t work on average at least 30 hours per week during the measurement period, you would not have to treat the employee as a full-time employee during the stability period that followed the measurement period, but the stability period could not be more than one month longer than the initial measurement period.

Example – Facts: For new variable hour employees, you use a 12-month initial measurement period that begins on the start date and apply an administrative period from the end of the initial measurement period through the end of the first calendar month beginning on or after the end of the initial measurement period.

Situation: Dianna is hired on May 10, 2014. Dianna’s initial measurement period runs from May 10, 2014, through May 9, 2015. Dianna works an average of 30 hours per week during this initial measurement period. You offer affordable coverage to Dianna for a stability period that runs from July 1, 2015 through June 30, 2016.

Conclusion: Dianna worked an average of 30 hours per week during her initial measurement period and you had (1) an initial measurement period that does not exceed 12 months; (2) an administrative period totaling not more than 90 days; and (3) a combined initial measurement period and administrative period that does not last beyond the final day of the first calendar month beginning on or after the one-year anniversary of Dianna’s start date. Accordingly, from Dianna’s start date through June 30, 2016, you are not subject to an employer mandate penalty with respect to Dianna because you complied with the standards for the initial measurement period and stability periods for a new variable hour employee. However, you must test Dianna again based on the period from October 15, 2014 through October 14, 2015 (your first standard measurement period that begins after Dianna’s start date) to see if she qualifies to continue coverage beyond the initial stability period.

Employee FT Testing Period Chart

As you can tell, there are many things to consider as you map out your plans for how your business is going to proceed with health care reform. Millennium Medical Solutions Corp hopes to be a valuable resource in the weeks and months ahead as you make these decisions. What about you? Do you have any glaring questions that we could answer for you about health care reform compliance?

For a FREE Affordable Care Act Guide leave your questions in the comments below or click the “Contact Us” button and we’ll do our best to answer your questions.

Please refer to the IRS Notice in the links below for more details and examples:

DISCLAIMER: We share this information with our clients and friends for general informational purposes only. It does not necessarily address all of your specific issues. It should not be construed as, nor is it intended to provide, legal advice. Questions regarding specific issues and application of these rules to your plans should be addressed by your legal counsel.