Congratulations – you just signed up successfully for Obamacare! You made it right before the March 31st deadline and avoided the individual penalty and getting blocked out for 2014. Don’t relax just yet. If you’re one of the many people who applied on the first open enrollment it’s smart to expect some bumps over the next few weeks. Shifting deadlines and technical glitches have left many insurance companies scrambling to catch up to the flood of requests. To make sure you start things right, here are some easy ways to stay vigilant:

Pay the premium –Until you pay for the plan you do not truly have a plan just yet. Some states and insurance companies have extended the deadline to pay, but its best to do this as soon as possible. For maximum peace of mind, get written confirmation from your new insurance company. If you go to the doctor before you pay your premium, you may end up footing that medical bill if the insurance company doesn’t have a record of your premium payment.

Member ID Cards –in about 1–2 weeks after you receive your first bill you will receive your Member ID card from your carrier after you’ve made your first premium payment. This is the card you’ll share with medical providers and pharmacies when you receive service. Your carrier may allow you to print a temporary ID card if you need care prior to receiving your Member ID card(s). Your insurance card will (hopefully) arrive in your mailbox in early January. You’ll present it wherever you need services: at the pharmacy, doctor’s office or hospital. Since insurance companies had a very short turnaround time to process new members, you may see a delay. Don’t panic! Go to the insurance company’s website to see if you can print a temporary ID card. (This is a lifesaver!) If you turn up empty, call the company’s customer service number to confirm that you are in their system as an enrolled member.

Don’t rush to the doctors – If you have an immediate need for a prescription or an appointment, by all means take care of it asap. But if you can, wait a few weeks before scheduling your doctor’s visit. This will give time for the insurance companies and doctors to update their systems with all the new plans and enrollees. This way, you help ensure that the medical claim for your doctor’s visit will be processed accurately – and that you dodge some of the early-stage craziness.

Double check – that your doctor is in your new plan’s network . Most of the new insurance plans also came with new provider networks. Its smart to double check that your favorite doctor is in the network for the exact plan you just enrolled in. There are specific networks for different insurance products, so make sure you are checking the right one. If your doctor is not in the network, keep in mind that you may have to pay significantly more money to see an out-of-network doctor, so you may consider switching. See States Pushing Back Against Smaller Networks

Keep records – Keep a record of your payments, calls, emails with your insurance company and physicians. Just in case of a technical glitch in the insurance or doctor’s computer systems, you can show evidence of your payment or confirmations from your insurance company.

Obamacare 2014 Deadline Nearing. You are now more knowledgable than most after reading this article. Given all the new changes thanks to the new insurance plans, new enrollees, and changing deadlines, being aware of these simple tips will help you avoid unnecessary headaches. And remember, if you are still shopping for insurance, you only have until March 31st to enroll in a plan.

For enrollment help before the deadline information please contact our team at Millennium Medical Solutions Corp (855)667-4621. We have Spanish, Russian, and Hebrew speakers available. Quotes can also be viewed on our site.

Qualifying Events for Marketplace Special Enrollment Period

After March 31, 2014, what are considered qualifying events for individuals to buy coverage from the Exchange Marketplace outside of the annual enrollment period?

Please note that the open enrollment for Marketplace coverage ends March 31, 2014. See more at: Obamacare 2014 Deadline Nearing. The next proposed open enrollment period is November 15, 2014 – January 15, 2015. According to the Healthcare.gov site, most special enrollment periods last 60 days from the date of the qualifying life event.

Whats is a Qualifying Event?

A Special Enrollment Period (SEP) is the time outside of Open Enrollment that allows individuals and families facing special circumstances (Qualifying Life Events) to enroll in a Qualified Health Plan. Eligible individuals have 60 days to enroll after their Qualifying Life Event.

Individual or dependent loses minimum essential coverage due to: job loss; employer no longer offers coverage; divorce; death of a spouse; becoming ineligible for Medicaid or Child Health Plus; expiration of COBRA; or health plan is decertified

Marriage, birth, adoption, or placement for adoption

Gaining status as a citizen, national, or lawfully present individual

Consumer is newly eligible or ineligible for tax credits and/or cost sharing reductions

Permanent move to an area that has different health plan options

Marketplace staff or contractor enrollment error

Qualified Health Plan violated a provision of its contract

American Indians can enroll or change plans one time per month throughout the year

Other exceptional circumstances, as defined by HHS

Approximately 50% of all enrollments occur outside of Open Enrollment due to Qualifying Life Events. If you are uninsured do not miss your chance to enroll before March 31!

When do I need to complete my application to avoid a federal tax penalty?

You need to complete your application by 11:59pm on Monday, March 31, 2014 to avoid a federal tax penalty. However, if you give us your word that you tried to apply for health insurance and were not able to enroll through no fault of your own, you will have until 11:59pm on Tuesday, April 15, 2014 to complete your enrollment.

I forgot about the enrollment deadline. Can I still buy health insurance through the Marketplace this year?

No. Unless you are Medicaid eligible or you are buying insurance for a child, you must have a major life-changing event called a qualifying life event to be eligible to buy insurance through the Marketplace this year after the deadline. If you don’t have a qualifying life event, you must wait for the next open enrollment period that begins on November 15, 2014 for coverage that starts on January 1, 2015.

When is my next chance to buy insurance through the Marketplace if I am not eligible for Medicaid?

The next open enrollment period for individuals and families begins on November 15, 2014 for coverage that starts on January 1, 2015.

Are there any exceptions to the open enrollment period?

Enrollment in Medicaid, Child Health Plus and the Small Business Marketplace continues all year.

Have a Qualifying Event?

Enroll Now using our online shopping tool

where you can compare plans and prices and enroll

Find us on the Health Insurance Marketplace where you may qualify for help to pay for your health insurance. Qualifying Events for Exchange Marketplace. 76 percent of the uninsured are unaware of the looming March 31 sign-up deadline. Contact us at (855)667-4621.

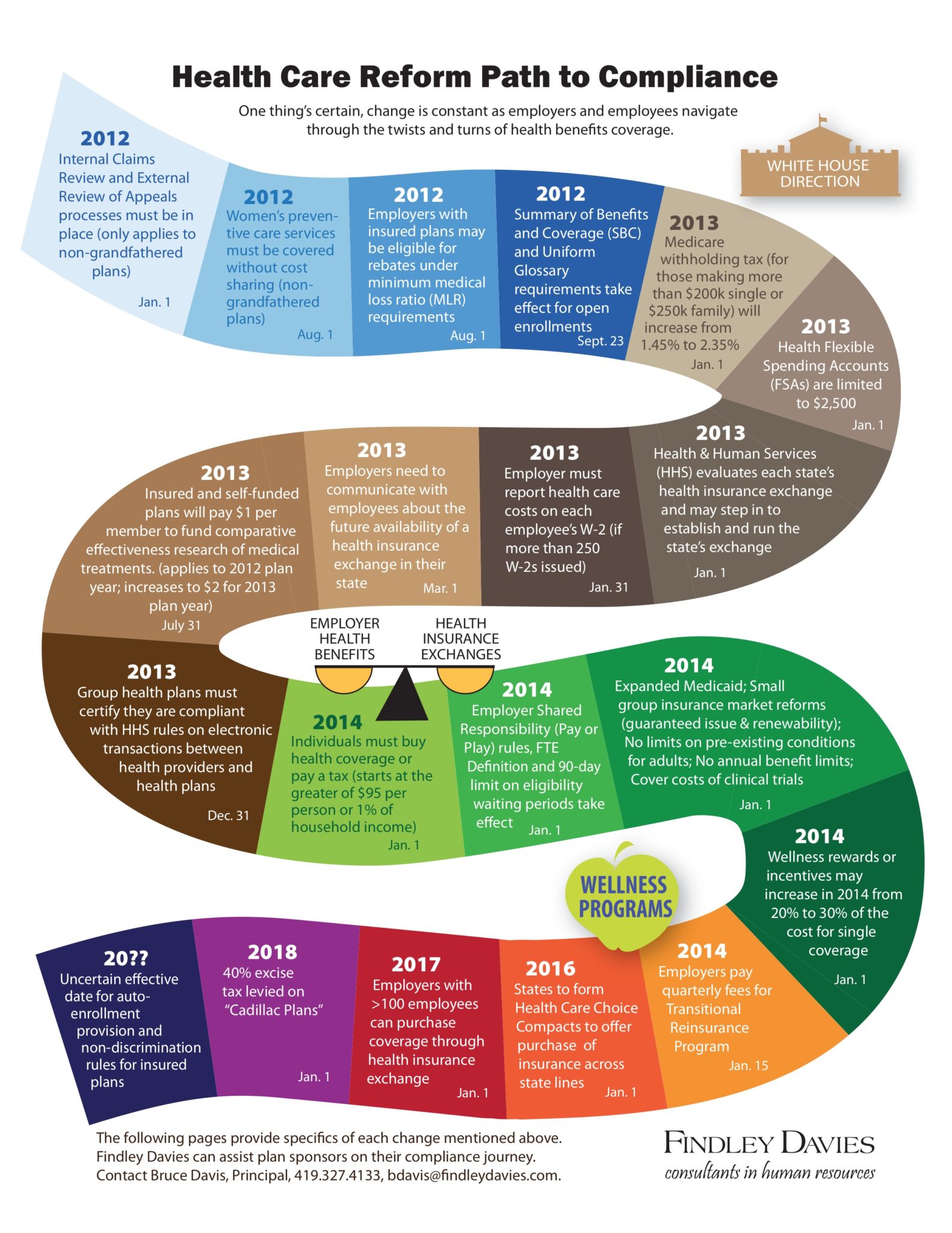

Obamacare Midsize Employer Mandate Delayed Till 2016.

For small businesses employing 50-99 the Treasury Dept is not requiring compliance of the Employer Mandate until 2016. Companies with 100 workers or more could avoid penalties in 2015 if they showed they were offering coverage to at least 70 percent of their full-time workers, the Treasury said.

The large group employer mandate had been originally delayed until 2015 in July 2013 see- Obamacare Employer Mandate Delayed, More Guidance. Employers with the equivalent of 50 full-time workers or more had to originally offer coverage or pay a penalty starting at $2,000 per worker beginning in 2014.

Employers with 100 or more full-time employers will have to comply with the Internal Revenue Code Section 4980H “play or pay” provision Jan. 1, 2015. Companies with 100 workers or more could avoid penalties in 2015 if they showed they were offering coverage to at least 70 percent of their full-time workers, the Treasury said.

Under the new rules, companies would be allowed during the phasing-in year to offer coverage specifically to a subset of employees, such as those working 35 hours or more a week, the Treasury said.

Treasury also set new rules for how the requirement would apply to workers such as volunteers and seasonal employees, saying that employers wouldn’t be penalized for failing to offer those people coverage, regardless of the number of hours they were working. Teachers, however, wouldn’t be considered part-time workers even if they were away over the summer, and adjunct faculty would have a special arrangement for how their classroom hours should be counted.

The penalty the employer pays would be based on the number of full-time workers that the employer employs. For purposes of calculating the penalty, the employer would not have to include part-time and seasonal workers in the calculations. Under PPACA, only workers who are not offered group health coverage are eligible to apply for exchange coverage.

The coverage must encompass a core set of benefits and be affordable – which the law defines as premiums costing no more than 9.5 percent of an employee’s income – and the employer must pay for the equivalent of 60 percent of the cost of coverage for workers but not their dependents.

As reported in Washington Post: “Administration officials said that organizations with a large number of volunteer employees – such as firefighters and first responders – would not have to provide coverage, along with those hiring seasonal employers who work six months or less in a given year. Teachers will not be considered part-time just because they do not work for three months during the summer, officials added, while the status of adjunct faculty will be calculated on a formula where they would receive credit for 2¼ hours of service per week for each hour they spent teaching or in the classroom.”

Many Employers are asking for flexibilities of defining FT as higher than 30 hours. The law has already had unintended consequences with shift in employment hours especially in industries such as dining, entertainment, services and construction.

Other transitional relief contained in the regulations include:

For employers with between 50 and 99 employees, the employer mandate is delayed until 2016. Note that an employer must provide a certification to take advantage of this relief.

Employees in positions for which the customary annual employment is six months or less generally will be considered seasonal employees and not full-time employees.

When employers are first subject to the employer mandate, they can determine whether they had at least 100 full-time employees in the previous year by referencing a period of six consecutive months, rather than an entire year.

For purposes of determining coverage in 2015 only, employers may use a measurement period (the period used to determine whether a variable-hour employee is a full-time employee) of six months, with respect to a stability period (the period following the measurement period, during which the variable-hour employee must be offered coverage) of up to 12 months.

Employers with non-calendar year plans must comply with the employer mandate at the start of their 2015 plan year, rather than on January 1, 2015.

For more information regarding both Exchanges – Individual Exchanges or SHOP please contact our team at Millennium Medical Solutions Corp (855)667-4621. We work in coordination with Navigators to assist with medicaid, CHIP Child Health Plus, Family Health Plus and Medicare Dual Eligibles. We have Spanish, Russian, and Hebrew speakers available. Quotes can also be viewed on our site.

Jan 1 Deadline is Today. Attention last minute health insurance shoppers you have until midnight to purchase a policy on the Health Exchange.

NYS Health Exchange is down again. Not surprisingly a large volume of late comers trying to beat t0morrows deadline for Jan 1, 2014. Last week a 34% enrollment spike in 1 week alone. Despite the 1 week extension the enrollments are still falling short of the original 600,000 projection. A significant percentage have instead been qualified under expanded Medicaid in NYS. At the same time many New Yorkers have had sole prop and husband/wife groups shut out of the small group market place. In addition, popular programs such as Healthy NY have been increased by 25-35% and new $600/single or $1200/family deductibles.

Facts:

Some people mistakenly believe they have until Dec. 31 to enroll in a plan that takes effect on Jan. 1. Others don’t realize they could pay a federal tax penalty if they don’t have health insurance in place by March 31.

Under the Affordable Care Act, most adults will pay a $95 penalty — or 1 percent of income — in 2014 if they don’t have health insurance coverage. The penalty rises to $695 — or 2 percent of income — by 2016.

To avoid the penalty, people must enroll in a plan by Feb. 15 or qualify for an exemption from the penalty.

Consumers who sign up by Dec. 23 and pay the first month’s premium by Jan. 10 will have coverage on Jan. 1, the industry group America’s Health Insurance Plans announced Wednesday.

If you make under $45,960 or your family makes under $94,200, you could get a real break on health insurance costs More low-income people will also be eligible for free coverage under Medicaid For those eligible, the subsidies will cap the amount you pay for your exchange policy at between 2% and 9.5% of your income (on a sliding scale, based on your income). To find out how much you would pay, estimate your income for this year and plug it into any health subsidy calculator. You can also see estimate subsidies with these ”health subsidy charts”.

Important: If the web site is down we can sign up via paper application to avoid the penalty. A surge of 34% enrollments in one week caused some technical delays last week.

For more information regarding both Exchanges – Individual Exchanges or SHOP please contact our team at Millennium Medical Solutions Corp (855)667-4621. We have Spanish, Russian, and Hebrew speakers available. Quotes can also be viewed on our site.

NYS Health Exchange 100,000 Enrolled. According to a USA Today article More than 100,000 enroll in N.Y. health exchange, up a third in less than two weeks according to the state Health Department .

According to the NYS Exchange site www.nystateofhealth.ny.gov– As of today, 100,881 state residents had enrolled in a health insurance plan through the state’s exchange. Additionally, 314,146 people had “completed applications” for coverage. The state did not break down the latest data based on the number of people enrolling in private insurance versus Medicaid. The state’s already “vast” Medicaid system “has been credited with having an easier transition to the health exchange.” New York state plans to enroll a total of 1.1 million people by the end of 2016

New York already has a vast Medicaid program, at an annual cost of $50 billion, it has been credited with having an easier transition to the health exchange. Reuters reported Dec. 4 that about 29,000 people signed up for health insurance through the federal HealthCare.gov website on Dec. 1 and Dec. 2 – eclipsing the 26,000 for all of October.

According to sources and our experience half of the Exchange applicants were to determined not be Medicaid eligible. The article Federal exchange sends unqualified people to Medicaid points out that some qualified Medicaid may not in fact be eligible. “The federal health care exchange is incorrectly determining that some people are eligible for Medicaid when they clearly are not, leaving them with little chance to get the subsidized insurance they are entitled to as the Dec. 23 deadline for enrollment approaches.”

New York State, unlike 36 states, runs its own exchange. The NYS website has had less issues than the troubled Federal health Exchange www.healthcare.gov. Our blog NYS Approves Health Insurance Exchange Rates describes how the new rates lower individual insurance market by 50%.

New York has various tiers of health insurers, and customers can pick from 16 insurers and 10 dental insurers. Quotes can also be viewed on our site. The program also has a small-business marketplace that offers health insurance to businesses with 50 or fewer employees. Large businesses that do not offer employees health insurance could be hit with a fine in 2015.

The exchange also offers tax credits to those who earn less than $45,960 as an individual or $94,200 as a family of four.People without health insurance would be hit with a fine on their income taxes for 2014, starting at about $95 or 1 percent of gross income. The fine can grow to as much as $695 a year , then double in 2015 and grow over time.

For more information regarding both Exchanges – Individual Exchanges or SHOP please contact our team at Millennium Medical Solutions Corp. We have Spanish, Russian, and Hebrew speakers available. Quotes can also be viewed on our site.

The following companies had health insurance plan rates for the health benefits exchange approved today by DFS. The rates approved today are subject to final certification of the insurers’ participation in the exchange.

Affinity Health Plan, Inc.

American Progressive Life & Health Insurance Company of New York

The Health Exchange also known as The Health Marketplace or Obamacare Exchanges are set to open in less than 12 hours. Are you ready or aye you like most asking What is an Exchange? Starting Oct 1 you can enroll until March 31, 2014, though you’ll generally need to sign up by Dec. 15 of this year, to be covered as of Jan. 1. You can find your state’s marketplace at healthcare.gov. The prices for the marketplace plans are likely to be similar to those sold privately. A plan that is also available on the exchange may be eligible for subsidies. Heres an easy top 10 list of what you need to know.

10. Locate your State Exchange

Look up your state’s exchange here and Healthcare.gov. Some states are running their own exchange, others are running it through the federal government see www.healthcare.gov. For NY Tri-State the sites are:

NYS – http://info.nystateofhealth.ny.gov See rates here

CT – https://www.accesshealthct.com See rates here

9. Individual Mandate Penalty

For 2014, the annual penalty is $95 or 1% of your income, whichever is greater. The penalty will increase over the first three years. Coverage can include employer-provided insurance, individual health insurance, Medicare or Medicaid.

Health Insurance Individual Penalty for Not Having Insurance Pay the greater of the two amounts

Year

Percentage of Income

Set Dollar Amount

2014

1%

$95 & $285/family max

2015

2%

$325 & $975/family max

2016

2.5%

$695 & $2,085/family max

8. Individual Subsidies

Individuals who do not have affordable minimum essential coverage from their employer will be eligible for tax credit subsidies for their health insurance purchase on a state exchange if their income is below 400 percent of federal poverty level.

If you make under $45,960 or your family makes under $94,200, you could get a real break on health insurance costs More low-income people will also be eligible for free coverage under Medicaid For those eligible, the subsidies will cap the amount you pay for your exchange policy at between 2% and 9.5% of your income (on a sliding scale, based on your income). To find out how much you would pay, estimate your income for this year and plug it into any health subsidy calculator. You can also see estimate subsidies with these “health subsidy charts”.

7. Small Business Subsidy – SHOP Exchange

A key change is that the small business health care tax credits will only be available ONLY through the SHOP Exchange marketplace in 2014. Small businesses with 25 or fewer employees who receive less than $50,000 a year in wages may be eligible for tax credits if they purchase the plan through the SHOP marketplace. These credits will cover up to 50% of the employer’s cost (35% for non-profits) for the first two years of coverage. Click here to read more about the small business health care tax credits.

6. Your income

not your assets, such as your house, stocks or retirement accounts – will count toward determining whether you can get tax credits. When you buy your plan, you estimate your income for next year, and your tax credit is based on that estimate. The next year, your tax returns will be checked by the IRS and compared against your estimate.

5. Pre-Existing Conditions Eliminated

Your insurer generally can’t drop you, as long as you keep up with your insurance premiums and don’t lie on your application. Generally, people will be able to enroll in or change plans once a year during the annual open enrollment period. This first year, open enrollment on the exchanges will run for six months, from Oct. 1 through March of next year. But in subsequent years the time period will be shorter, running from October 15 to December 7.

4. Essential Health Benefits Covered

Each plan covers 10 “essential health benefits,” which include prescription drugs, emergency and hospital care, doctor visits, maternity and mental health services, rehabilitation and lab services, among others. In addition, recommended preventive services, such as mammograms, must be covered without any out-of-pocket costs to you. More info here.

3. Ninety-Day Maximum Waiting Period

Group health plans and health insurance issuers may not impose waiting periods of more than ninety days before coverage becomes effective. This also applies to grandfathered plans.

2. Annual or Lifetime Limits

Group health plans, including grandfathered plans, may no longer include more than restricted annual or any lifetime dollar limits on essential health benefits for participants. Limits may exist in and after 2014 for non-essential benefits.

1. Not Everyone is Eligible

Immigrants who are in the country illegally will be barred from buying insurance on the exchanges. However, legal immigrants are permitted to use the marketplaces and may qualify for subsidies if their income is no more than 400 percent of the federal poverty level (about $46,000 for an individual and $94,200 for a family of four).

members of certain religious groups and Native American tribes

incarcerated individuals

people whose incomes are so low they don’t have to file taxes (currently $9,500 for individuals and $19,000 for married couples)

Conclusion:

There has been a lot of news about individual Obamacare provisions getting delayed – Obamacare Employer mandate Delayed. Some people may assume that means the health law is being slowly dismantled, or put off for an additional several years. .The Affordable Care Act is an extremely complicated law with a lot of moving parts, but ultimately, the biggest provisions are still moving forward. There will likely be more hiccups along the way. As the enrollment period opens for Obamacare’s new exchanges, industry experts predict there will probably be other issues that need to be ironed out — but that doesn’t mean the whole law is collapsing

Still confused?

Don’t be. These are the common questions that we are working through with our clients daily. Am I better off going SHOP Exchange vs. Individual for my business? Am I better off going off Exchanges or onto Private Exchanges? Whats my minimum employer contribution? Do I have to cover employee and dependents? Is dental and vision included? What happens to my Healthy NY when it shuts down Jan 1, 2014? What employer notices must I be posting?

Please contact our team at Millennium Medical Solutions Corp if you have additional questions regarding how SHOP Exchanges and Individual Exchanges can benefit you Stay tuned to our site for updates as more information gets released. Sign up for latest news updates.