The New FSA Carry Over. U.S. loosens FSA rules and will allow a carry over of up to $500 to the next year. The use-it-or-lose-it rule scared off many workers, with just 25 percent of eligible workers participating in healthcare FSAs.

According to a WSJ article “Consumers Can Roll Over $500 in an FSA”, about 14 million families use FSA accounts and the new plan would be a welcome relief for them. That’s because until now any unused funds used to go the employer, so people were forced to use up the funds, especially toward the end of the year by spending on frivolous things. Moreover, many were fearful of signing up, lest they lose any unused amount.

The most recent prior change to FSA this year was a limit of $2,500 that a worker can set aside.

The health care Flexible Savings Account (FSA) can reimburse you or help you pay for eligible health care expenses not covered by your health plan. The portion of your paycheck you put into your FSA is taken out before you pay federal income taxes, Social Security taxes and most state taxes. It’s a great way to save money.

Generally, contributions you make to your FSA are not subject to federal income taxes or social security taxes. In most instances, there are no state taxes taken out either. The amount you may save depends upon:

The amount you put into your FSA

The tax percentage you would normally pay on that money (tax bracket)

Let’s say you want $2,000 taken out of your paycheck this year to put into your FSA. The money you direct to your FSA is taken out of your check before taxes are taken out. That reduces your taxable income by $2,000.

Let’s say you normally pay 30 percent in federal, social security and state taxes on your income. In this example, you would enjoy a tax savings of 30 percent of the $2,000. In other words, you could get a $600 tax savings on the $2,000 you directed to your FSA.

This example should not be taken as tax advice. See a tax advisor to seek the best advice for your situation. To see how much you may save, check out Aetna’s FSA Savings Calculator.

Is your FSA compliant? Which pre-tax qualified HSA, FSA, HRA spending card is right is right for you ? Please contact our team at Millennium Medical Solutions Corp (855)667-4621 for immediate answers.. Stay tuned for updates as more information gets released. Sign up for latest news updates.

In an unexpected announcement pre-July 4th the big news was Obamacare Employer Mandate Delayed with penalties under the Affordable Care Act (ACA) until 2015. The mandate also known as the “Employer Shared Responsibility” requires employers with 50 or more FTEs to offer affordable health insurance coverage to their workers or face financial penalties for not doing so. Those penalties would originally have been applied beginning in 2014.

There has been a follow up guidance issued last week July 9th by the IRS. According to the IRS, the delay will give employers more time to prepare for the change in how health insurance is provided and will also give the Obama Administration time to simplify the insurance-related reporting requirements that employers face. This transition relief appears to come with “no strings attached.” Although the IRS guidance encourages employers to voluntarily comply with the employer mandate and maintain or expand health care coverage in 2014, the IRS will not impose penalties for a failure to do so.

Although the IRS guidance encourages employers to voluntarily comply with the employer mandate and maintain or expand health care coverage in 2014, the IRS will not impose penalties for a failure to do so.Notably, the guidance issued on July 9th also does not require employers to make “good faith” efforts to comply. As a result of this transition year, employers will have the option of deciding to what extent (if any) they will continue efforts to comply with the employer mandate during 2014.

Employers who intended to rely on one of the transition rules previously announced for 2014 should keep in mind that the latest IRS guidance does not provide special transition rules for 2015. Other group health plan requuirements still apply as discussed in our prior blog Essential Health Benefits Not Delayed.

This means that for plan years beginning on and after January 1, 2014, all group health plans must:

Eliminate all pre-existing condition exclusions (regardless of age);

Maximum Cost Sharing Deductible to $2,000/individual ($4,000/family); limit in-network out-of-pocket maximums to $6,350/individual ($12,700/family)

Individual Mandate Still Applies. individuals will still be required to obtain health care coverage or pay a penalty for each month they do not have coverage, beginning January 1, 2014

Exchanges (Marketplaces) Open for Enrollment October 1, 2013.

The IRS notice makes it clear that individuals who enroll in coverage on the marketplaces will continue to be eligible for a premium tax credit if their household income is within a specified range and they are not eligible for other minimum essential coverage.

Employers Must Send Notice of Exchanges (Marketplaces) Before October 1, 2013. These notices must be sent to current employees by October 1, 2013. Then, beginning October 1, 2013, employers must send this notice to new hires within 14 days of their start date.

New taxes still apply – Patient Centered Outcomes Research Institute (PCORI) excise taxes and transitional reinsurance program fees;HRA/HSA/FSA clients also pay a monthly $1/employee tax.

We will continue to monitor ACA developments and will provide you relevant updated information when available. In the meantime, please visit to view past blogs and Legislative Alerts at https://360peo.com/feed.

The pre-July 4th news of Obamacare Employer Mandate Delayed until 2015 decision may have started early fireworks. The administration did not, however, delay the larger new requirements facing employers who choose to offer health insurance in the small group market––employers with less than 50 workers. The biggest requirement – Essential Health Benefits not delayed.

Whether the rationale was to alleviate business pressure to meet new mandates by Jan 2014 or the real fear that Employers have already begun making necessary employment hours cut backs to avoid the $2,000 penalty. A $3,000/employee penalty was also looming for Employers offering unaffordable insurance.

Keep in mind that this limited delay does not affect other provisions of the Affordable Care Act slated to go into effect in or before 2014, such as:

Individual mandate which requires most individuals to purchase insurance by January 1, 2014, or pay a tax penalty.

a 90-day maximum on eligibility waiting periods;

monetary caps on annual out-of-pocket maximums;

total elimination of lifetime and annual limits (including expiration of waivers that permitted certain “mini-med” plans and stand-alone Health Reimbursement Arrangements to stay in place through plan years beginning in 2013);

Patient Centered Outcomes Research Institute (PCORI) excise taxes and transitional reinsurance program fees; HRA/HSA/FSA clients also pay a monthly $1/employee tax.

a notice informing employees of the availability of the new health insurance Exchanges (a model notice is available on the U. S. Department of Labor website); and insurance market reforms.

The biggest impact is the Essential Health Benefits (EHB) which will not be delayed and this affects fully insured or ALL Small Businesses. While small employers are not required to offer coverage, if they do then they come under that large number of new essential health benefit mandates and group rating rules that won’t apply to large employers. These small group requirements are expected to increase the cost of small group coverage by an average of 15%––with wide variation by state and the average age of the group.

An employer sponsoring a Healthy NY or Brooklyn Healthworks Plan today for example would be disqualified as this does not carry all Essential Health Benefits. The very popular Healthy NY is slated to shut down for Jan 2014 and most Employers have just received this transition letter last week. Individual and Sole Prop Healthy NY is terminating and small business Healthy NY must be reapplied under a new higher cost version. While the plan did not carry Ambulance and had a $3,000 limited Pharmacy plan it is priced 35% below market and did manage to capture hundreds of thousands that would otherwise had been uninsured. The same is true for those on Hospital Only or high deductible catastrophic plans.

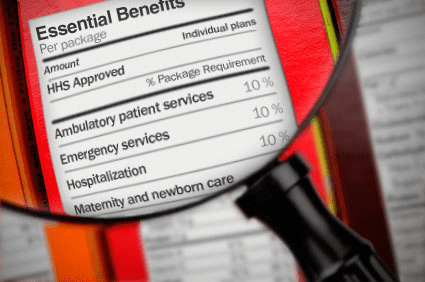

So what are these Essential Health Benefits?

All individual and small group policies on and off-Exchangemust cover ten categories of minimum essential health benefits.

Under the ACA, each state must choose one plan from among popular health insurance plans offered statewide to serve as a benchmark for EHBs. The benchmark plan will act as the model for how plans must define and include EHBs in their coverage — in both the individual and small group markets. New York selected the benefits of the State’s largest small group plan as its EHB benchmark. There is also a Minimum Value requirement, See NYS Minimum Value STANDARD BENEFIT DESIGN COST SHARING DESCRIPTION CHART (5-6-2013) Some of the plan’s components include:

No cost-sharing for routine preventive services

Pediatric dental and vision coverage

Habilitative and rehabilitative services, including physical therapy, speech therapy and occupational therapy

Rich mental/behavioral health services

No annual or lifetime dollar limits on benefits

Conversely, a shift to self- insurance is underway as self-insureds can avoid many taxes and instead ONLY cover the Minimum Essential Coverage which is different than the Essential Health Benefits. The strategy coupled with reinsurance is a great sophisticated model usually reserved for larger groups. This segment will be able to avoid local additional State mandates which in States like NY account for 14-16%% of the costs. Thats a total swing of 30% for a fully insured NY group. Also, self-insured groups do NOT pay added taxes such as the health insurance tax of $9 Billion annually over the next 10 years.

The administration has shown their sensitivity to larger groups. This segment already covers 94% of its employees at least in some fashion while small businesses cover less than 50%.

Why not do the same for small employers as well? And while they are at it, use the time to reconsider the impact many of these regulations are likely to have on the number of small employers continuing to offer coverage.

For a downloadable guide on self-insuring and secondary market reinsurance for your group please send contact form below. In the meantime, please visit to view past blogs and Legislative Alerts at https://360peo.com/feed.

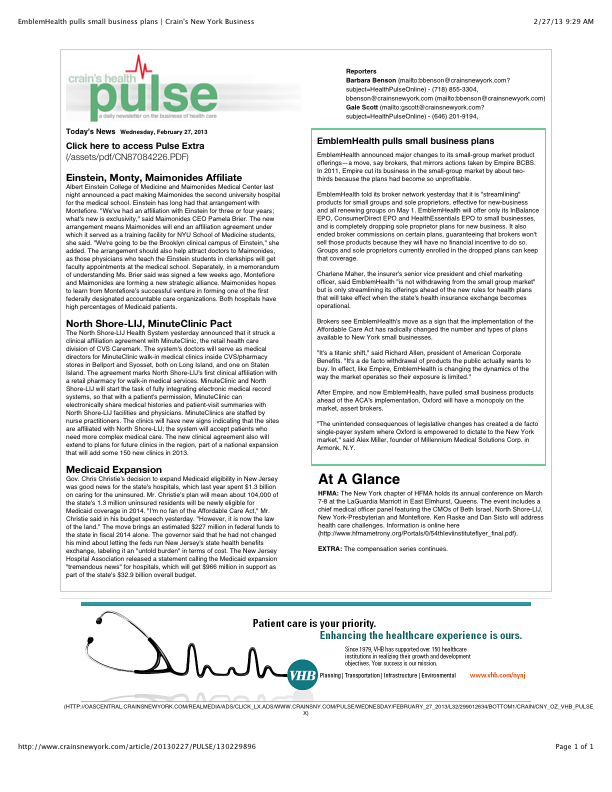

Is EmblemHealth (GHI formerly) leaving the small business market? Yes and no. The popular traditional EPO is slated to be chopped up for new business May 1 pending State approval. The remaining consumer driven health plans which have deductibles and coinsurance (a %) will stay in tact. With that Broker compensation commissions will be significantly cut as well. The family popular 2-tier rating is also phased out and new groups must submit everything clean within 30 days.

Our quote in todays Crains Health Pulse Crains EmblemHealth pulls small business plans Feb 2013 | Crain’s New York Businessreflects our deep concerns on market consolidations. “The unintended consequences of legislative changes has created a de facto single-payer system where Oxford is empowered to dictate to the New York market,” said Alex Miller, founder of Millennium Medical Solutions Corp. in Armonk, N.Y. To be fair Emblem has been steadily streamlining plans with in network only plan offerings and lowest HSA (Health Savings Account) family deductible starting out at $11,600. They are not the first insurer to do this as Empire Blue Crossissued a broader exit back in Nov 2011.

A healthy health insurance marketplace depends on competition as we all agree. From approximately 12 insurers 15 years ago we are today down to 2 active insurers Aetna and Oxford with Oxford claiming approx 2/3 of the small business marketplace. In NYS theMLR(Minimum Loss Ratios) are higher than any other state with additional state taxes. See NYS Surcharge on Health Insurance. The tight State Regulators allowing for razor thin margins while requiring insurers to maintain high reserves makes a burden many insurers are not excited. This resembles more of a utility company environment except ConEd realizes a 10% operating profit and do not have to have insurance reserves to prove solvency. Is there any surprise why there is no rush by outside insurers to compete here?

While on topic of ConEd we all know how customer care was in the aftermath of Hurricane Sandy. When was the last time an independent veteran consultant (not an ESCO) worked with you on your utility bill, servicing, negotiating, educating, and maximizing savings? Sure you can use a different supplier or ESCO but its still the local singular utility company that you are using. In comparison, same is happening in the health insurance field and the consequential exit of Health Insurance Brokers. Sadly, this is precisely the time when their training is most in demand and the most in need will be least likely to afford them.

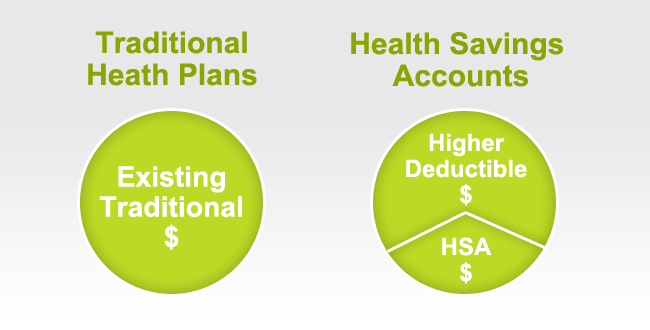

HSA holders own the assets in the accounts and can build up substantial sums over time. Enrollment in HSA-compatible insurance plans has increased to 10 million earlier this year, from 1 million in March 2005, according to, America’s Health Insurance Plans (AHIP), a trade group.

HSAs were authorized starting in January 2004. Since then, AHIP has conducted a periodic census of health plans participating in the HSA/HDHP market.

The number of people with HSA/HDHP coverage rose to more than 11.4 in January 2011, up from 10.0 million in January 2010, 8.0 million in January 2009, and 6.1 million in January 2008.

30 percent of individuals covered by an HSA plan were in the small group market, 50 percent were in the large-group market, and the remaining 20 percent were in the individual market.

14% of all workers in the private sector that have access to a Health Savings Account acc. to Bureau of Labor Statistics.

States with the highest levels of HSA/HDHP enrollment were California, Ohio, Florida, Texas, Illinois and Minnesota.

HSA Advantages:

Opportunity to build savings – Unused money stays in your account from year to year and earns tax-free interest. The HSA also gives you an investment opportunity.

Tax-free contributions and earnings – You don’t pay taxes on contributions or earnings.

Tax Free Money allowed for non traditional Medical coverage– As per IRS Publication 502, unused moneys can be used for dental,vision, lasik eye surgery, acupuncture, yoga, infertility etc. Popular Examples

Portability – The funds belong to you, so you keep the funds if you change jobs or retire.

Our overall experience with HSAs have been positive when employer funding is at minimum 50% using either the HSA or an HRA (Health Reimbursement Account-employer keeps unspent money). Traditional plans trend of higher copays and new in network deductibles has also led to the popularity of an HSA.

Please contact us for more customized information and how to incorporate this into your employee benefits.

HDHP Minimum Annual Deductible (No change from calendar year 2011):

Single – $1200

Family – $2400

HDHP Out-of-Pocket Maximum:

Single – $6050

Family – $12,100

HSA Maximum Contribution Limit:

Single – $3100

Family – $6250

HSA/HDHP Market Growth

HSA holders own the assets in the accounts and can build up substantial sums over time. Enrollment in HSA-compatible insurance plans has increased to 10 million earlier this year, from 1 million in March 2005, according to, America’s Health Insurance Plans (AHIP), a trade group.

HSAs were authorized starting in January 2004. Since then, AHIP has conducted a periodic census of health plans participating in the HSA/HDHP market.

• Between January 2009 and January 2010, the fastest growing market for HSA/HDHP products was large-group coverage, which rose by 33 percent, followed by small-group coverage, which grew by 22 percent.

• 30 percent of individuals covered by an HSA plan were in the small group market, 50 percent were in the large-group market, and the remaining 20 percent were in the individual market.

• States with the highest levels of HSA/HDHP enrollment were California, Ohio, Florida, Texas, Illinois and Minnesota

HSA Advantages:

Opportunity to build savings – Unused money stays in your account from year to year and earns tax-free interest. The HSA also gives you an investment opportunity.

Tax-free contributions and earnings – You don’t pay taxes on contributions or earnings.

Tax Free Money allowed for non traditional Medical coverage– As per IRS Publication 502, unused moneys can be used for dental,vision, lasik eye surgery, acupuncture, yoga, infertility etc. Popular Examples

Portability – The funds belong to you, so you keep the funds if you change jobs or retire.

Our overall experience with HSAs have been positive when employer funding is at minimum 50% using either the HSA or an HRA (Health Reimbursement Account-employer keeps unspent money). Traditional plans trend of higher copays and new in network deductibles has also led to the popularity of an HSA.

For more customized information and how to navigate this please contact us: