Clinton vs Trump Healthcare. A helpful overview from SHRM on the differences between the Candidates. They presumably agree on repealing the Cadillac Tax and well-needed price transparencies.

HILLARY CLINTON’S HEALTH CARE REFORM PLAN:

Defend the Affordable Care Act. Clinton will continue to defend the ACA against Republican efforts to repeal it.

Lower out-of-pocket costs like copays and deductibles. The average deductible for employer-sponsored health plans rose from $1,240 in 2002 to about $2,500 in 2013. Clinton believes that workers should share in slower growth of national health care spending through lower costs.

Reduce the cost of prescription drugs. Prescription drug spending accelerated from 2.5 percent in 2013 to 12.6 percent in 2014. It’s no wonder that almost three-quarters of Americans believe prescription drug costs are unreasonable. Clinton believes we need to demand lower drug costs for hardworking families and seniors.

Build on the Affordable Care Act and require plans to provide three sick visits without counting toward deductibles every year. The Affordable Care Act required nearly all plans to offer many preventive services, such as blood pressure screening and vaccines, with no cost-sharing at all. But because average deductibles have more than doubled over the past decade, many Americans would have to pay a significant cost out-of-pocket toward their deductible if they get sick and need to see a doctor. Clinton’s plan will build on the Affordable Care Act by requiring insurers and employers to provide up to three sick visits to a doctor per year without needing to meet the plan’s deductible first.

Provide a new, progressive refundable tax credit of up to $5,000 per family for excessive out-of-pocket costs. For families that still struggle with prescription drug costs even after out-of-pocket limits on drug spending and free primary care visits, Clinton’s plan will provide progressive, targeted new relief. Americans with health coverage will be eligible for a new refundable tax credit of up to $2,500 for an individual, or $5,000 for a family, available to those with substantial out-of-pocket health care costs. The credit will be available to insured Americans with qualifying out-of-pocket health expenses in excess of five percent of their income, and who are not eligible for Medicare or claiming existing deductions for medical costs. This refundable, progressive credit will help middle-class Americans who may not benefit as much from currently-available deductions for medical expenses. This tax cut will be fully paid for by demanding rebates from drug manufacturers and asking the most fortunate to pay their fair share.

Enforce and Broaden the ACA’s Transparency Provisions. Americans deserve real-time, updated, and reliable information to guide them in selecting a health plan, navigating changes to their out-of-pocket costs in their existing plan, choosing a doctor, and determining how much they will need to pay for a prescription drug. Clinton’s plan will vigorously enforce existing law under the Affordable Care Act and adopt further steps to make sure that employers, providers, and insurers provide this information through clear and accessible forms of communication so that Americans can make informed choices about their coverage and realize meaningful savings.

Repeal ACA -Modify existing law that inhibits the sale of health insurance across state lines. As long as the plan purchased complies with state requirements, any vendor ought to be able to offer insurance in any state. By allowing full competition in this market, insurance costs will go down and consumer satisfaction will go up.

Tax deductible health insurance premium payments. Allow individuals to fully deduct health insurance premium payments from their tax returns under the current tax system. -Allow individuals to use Health Savings Accounts (HSAs). Contributions into HSAs should be tax-free and should be allowed to accumulate. These accounts would become part of the estate of the individual and could be passed on to heirs without fear of any death penalty. These plans should be particularly attractive to young people who are healthy and can afford high-deductible insurance plans. These funds can be used by any member of a family without penalty. The flexibility and security provided by HSAs will be of great benefit to all who participate.

Price transparency. Require price transparency from all healthcare providers, especially doctors and healthcare organizations like clinics and hospitals. Individuals should be able to shop to find the best prices for procedures, exams or any other medical-related procedure.

Reform mental health programs. Families, without the ability to get the information needed to help those who are ailing, are too often not given the tools to help their loved ones. There are promising reforms being developed in Congress that should receive bi-partisan support.

Block-grant Medicaid to the states. Nearly every state already offers benefits beyond what is required in the current Medicaid structure. The state governments know their people best and can manage the administration of Medicaid far better without federal overhead. States will have the incentives to seek out and eliminate fraud, waste and abuse to preserve our precious resources.

Remove barriers to entry into free markets for drug providers that offer safe, reliable and cheaper products. Though the pharmaceutical industry is in the private sector, drug companies provide a public service. Allowing consumers access to imported, safe and dependable drugs from overseas will bring more options to consumers.

Add our blog & sign up for newsletter on latest in Healthcare Reform News. Please contact us for a free evaluation on your group’s benefits at 855-667-4621.

Many follow up questions on the postPay or Play Employer Guide have been raised. A Pay or Play FAQ hopefully adds some clarification.

Will I be required to offer health insurance coverage to my employees?

No. However, if you have at least 50 full-time employees, and you don’t offer coverage, you will owe a penalty starting in 2014 if any full time employee is eligible for and purchases subsidized coverage through an exchange. This penalty is called the “free rider” penalty.

We employ about 40 full-time employees working 30 or more hours per week and about 25 part-time or seasonal employees. So we are not subject to the employer mandate penalties, right?

You may be. The health reform law does not require you to provide coverage for employees working on average less than 30 hours per week (“part-time”). However, the hours worked by part time employees are counted to determine whether you have at least 50 full-time employee equivalents and therefore are subject to the employer mandate. This is done by taking the total number of monthly hours worked by part time employees (but not to exceed 120 hours for any one part-time employee) and dividing by 120 to get the number of “full time equivalent” employees. You would then add those “full-time equivalent” employees to your 40 full-time employees.

The hours worked by seasonal employees are also counted to determine whether you have at least 50 full-time employee equivalents and therefore are subject to the employer mandate. For purposes of determining whether you are a large employer, seasonal employees are workers who perform labor or services on a seasonal basis (i.e. exclusively performed at certain seasons or periods of the year and which, from its nature, may not be continuous or carried on throughout the year) for no more than 120 days during the taxable year and retail workers employed exclusively during holiday seasons. There is an exemption from the employer mandate that says you would not be considered to employ more than 50 full-time employees if:

Your workforce only exceeds 50 full-time employees for 120 days, or fewer, during the calendar year; and

The employees in excess of 50 who were employed during that 120-day (or fewer) period were seasonal workers.

Our workforce numbers go up and down during the year. How do we determine if we had at least 50 full-time employees on business days during the preceding calendar year?

For purposes of determining if you are a large employer, the formula requires the following steps:

1.Determine the total number of full-time employees (including any full-time seasonal workers) for each calendar month in the preceding calendar year;

2.Determine the total number of full-time equivalents (including non-full-time seasonal employees) for each calendar month in the preceding calendar year;

3.Add the number of full-time employees and full-time equivalents described in Steps 1 and 2 above for each month of the calendar year;

4.Add up the 12 monthly numbers;

5.Divide by 12. If the average per month is 50 or more, you are a large employer.

So if we offer coverage to our full-time employees, we will not have to pay a penalty?

Not necessarily. If you have at least 50 full-time employees and you offer coverage to at least 95% of your full-time employees, you are still subject to a penalty starting in 2014 if:

1.A full-time employee’s contribution for employee-only coverage exceeds 9.5% of the employee’s household income (Note: see below regarding a proposed affordability “safe harbor”) or the plan’s value is less than 60%; and

2.The employee’s household income is less than 400% of the federal poverty level; and

3.The employee waives your coverage and purchases coverage on an exchange with premium tax credits.

The penalty will be calculated separately for each month in which the above applies. The amount of the penalty for a given month equals the number of full- time employees who receive a premium tax credit for that month multiplied by 1/12 of $3,000.

We have more than 50 full-time employees so we are subject to the employer mandate penalties. How do we know which of our employees is considered “full-time” requiring us to pay a penalty if they qualify for premium tax credits at an exchange (if the employee has a variable work schedule or is seasonal)?

Through the end of 2014, for purposes of the employer mandate penalties, the guidance permits you to use a “look-back measurement period/stability period” safe harbor to determine which of your employees are considered full-time employees. You may use a standard measurement/stability period for ongoing employees, while using a different initial measurement/stability period for new variable and seasonal employees

How do the full-time employee safe harbors work for new hires?

They are generally based on the employee’s hours worked, or, the amount of hours the employee is reasonably expected to work as of their hire date.

New employee reasonably expected to work full-time (i.e. 30 or more hours per week)– If you reasonably expect an employee to work full-time when you hire them, and coverage is offered to the employee before the end of the employee’s initial 90 days of employment, you will not be subject to the employer mandate payment for that employee, if the coverage is affordable and meets the minimum required value.

New employee reasonably expected to work part-time (i.e. less than 30 hours per week)-– If you reasonably expect an employee to work part-time and the employee’s number of hours do not vary, you will not be subject to the employer mandate penalty for that employee if you don’t offer them coverage.

New variable hour and seasonal employees – If based on the facts and circumstances at the date the employee begins working (the start date), you cannot determine that the employee is reasonably expected to work on average at least 30 hours per week, then that employee is a variable hour employee. Because the term “seasonal employee” is not defined for purposes of the employer responsibility penalty, through 2014, you are permitted to use a reasonable, good faith interpretation of the term “seasonal employee”. The IRS has indicated that any interpretation of the term “seasonal” probably would not be reasonable if it included a working period of more than six months. Once hired, you have the option to determine whether a new variable hour or seasonal employee is a full-time employee using an “initial measurement period” of between three and 12 months (as selected by you).You would measure the hours of service completed by the new employee during the initial measurement period to determine whether the employee worked an average of 30 hours per week or more during this period. If the employee did work at least 30 hours per week during the measurement period, then the employee would be treated as a full-time employee during a subsequent “stability period,” regardless of the employee’s number of hours of service during the stability period, so long as he or she remained an employee. The stability period must be for at least six consecutive calendar months and cannot be shorter than the initial measurement period. If the employee then didn’t work on average at least 30 hours per week during the measurement period, you would not have to treat the employee as a full-time employee during the stability period that followed the measurement period, but the stability period could not be more than one month longer than the initial measurement period.

Example – Facts: For new variable hour employees, you use a 12-month initial measurement period that begins on the start date and apply an administrative period from the end of the initial measurement period through the end of the first calendar month beginning on or after the end of the initial measurement period.

Situation: Dianna is hired on May 10, 2014. Dianna’s initial measurement period runs from May 10, 2014, through May 9, 2015. Dianna works an average of 30 hours per week during this initial measurement period. You offer affordable coverage to Dianna for a stability period that runs from July 1, 2015 through June 30, 2016.

Conclusion: Dianna worked an average of 30 hours per week during her initial measurement period and you had (1) an initial measurement period that does not exceed 12 months; (2) an administrative period totaling not more than 90 days; and (3) a combined initial measurement period and administrative period that does not last beyond the final day of the first calendar month beginning on or after the one-year anniversary of Dianna’s start date. Accordingly, from Dianna’s start date through June 30, 2016, you are not subject to an employer mandate penalty with respect to Dianna because you complied with the standards for the initial measurement period and stability periods for a new variable hour employee. However, you must test Dianna again based on the period from October 15, 2014 through October 14, 2015 (your first standard measurement period that begins after Dianna’s start date) to see if she qualifies to continue coverage beyond the initial stability period.

Employee FT Testing Period Chart

As you can tell, there are many things to consider as you map out your plans for how your business is going to proceed with health care reform. Millennium Medical Solutions Corp hopes to be a valuable resource in the weeks and months ahead as you make these decisions. What about you? Do you have any glaring questions that we could answer for you about health care reform compliance?

For a FREE Affordable Care Act Guide leave your questions in the comments below or click the “Contact Us” button and we’ll do our best to answer your questions.

Please refer to the IRS Notice in the links below for more details and examples:

DISCLAIMER: We share this information with our clients and friends for general informational purposes only. It does not necessarily address all of your specific issues. It should not be construed as, nor is it intended to provide, legal advice. Questions regarding specific issues and application of these rules to your plans should be addressed by your legal counsel.

Fiscal Cliff Deal: Doc Cuts Spared. Happy 2013 Fiscal Cliff averted! At least for another year the dreaded 27% Medicare reimbursement have been spared. The so-called “doc fix” would boost the deficit by $31 billion. The President stood firm against any proposed Republican cuts to the Affordable Care Act.

The fear in provider cuts is grounded. According to The Lewin Report Patient Protection and Affordable Care Act (PPACA): Long Term Costs for Governments, Employers, Families and Providers “About half of program costs will be funded with reductions in payments to providers and health plans under the Medicare and Medicaid programs, which the CBO estimates will amount to $498 billion over the ten year period“. The new cost estimate has been updated to $1.4445 trillion from original estimate $938 billion over 10 years.

With millions of new uninsured patients slated to enter the system this would help providers recover reimbursement losses. Additionally, the President was firmly against any Provider cuts in 2013.

The Lewin Report predicts in fact that Provider Reimbursement will recover losses long term and in fact increase gross payments to $129.8 billion under the Act.

“..estimate that utilization of physician services will increase by about $102.7 billion under the Act. This estimate reflects Medicaid the payment levels for the portion of newly insured people covered under that program and commercial payment levels for those who become covered under private insurance. As discussed above, our key assumption is that utilization of services for newly insured people adjusts to the levels reported by insured individuals with similar age, gender, health status and income characteristics. Physicians also will be paid for services formerly provided free to uninsured people resulting in revenues of $8.4 billion. There will be an increase in reimbursement for people who shift from Medicaid to private coverage, and payment rates for Medicare primary care services will be increased for a three year period under the Act. These factors will add 18.7 billion in revenues for physicians.

While there was large Senate consensus 89-8 approval for the American Taxpayer Relief Act the health care debate is far from over. With rising health care costs, combined with the aging of the baby boomers, means the entitlement programs will remain at the heart of the tax-and-spending battles to come.

The Con Ed lockout this Summer couldn’t come at a more heady time. I’m not referring to the obvious temperature swelter but more to the employee health benefits that are at the back bone of virtually every recent Labor dispute. With the Con Ed dispute, Management’s has acquiesced on the health insurance . “Con Ed did accede to “public pressure” on Sunday by reinstating health insurance for the 8,500 members of Local 1-2 of the Utility Workers Union of America, a company spokesman said. The workers have been collecting unemployment benefits for two weeks but had to pay for their own prescription medicine and doctor visits because the company cut off health coverage when the old contract expired, at midnight June 30.”

Interestingly, Unions are major stakeholders in Healthcare as their benefits have been traditionally rich incentives attracting to workers. However, with A.C.A. (Affordable Care Act) otherwise known as Obamacare their health programs are very much in danger of additional taxation or member withdrawal. Unions estimate these provisions will raise the cost of health coverage by an additional $1,000 a year. In fact, a Union members may fare better on the Individual Mandated Exchange with projected individual direct insurance dropping 70% things will open up. A lower/middle income member will likely qualify for an additional discount credit. A more affordable health plan just may be a possibility.

There are other reasons the Individual Health Plan may be better:

Unions as other self insured group must now comply with added benefits for preventive care, maternity care, Age 26 dependent care, pre-existing condition waivers.

No Annual Limits on essential benefits by 2014

No Lifetime Limits

No more mini-med plans – discount health plans are prohibited. The movie John Q , based on a true story, where a father is told his son’s transplant will not be covered based on th elicited mini-med plan covering him up to $20,000. Large companies such as McDonald’s have also sponsored mini meds.

Cadillac Tax – By 2018 a 40% excise tax on health plans that exceed $10,200(single) and $27,500 (family).

The original Cadillac Tax was pushed back by the behest of Unions to 2018 from the original proposed 2014 date. Most Unions with generous health care packages would not be complaint within that time frame.

However, not all is grim for Unions. HHS has issued waivers to 1,625 plans covering 3,914,356 individuals were exempt from these mandates through 2014. According to Heartland “More than half of the approximately four million individuals receiving waivers are union members, including 82.9 percent of those covered in the most recently updated list of waivers.”

With current administration posts coming from Union there wouldn’t be much surprise if these allowances continue. Would it be that bold to predict for Union Members in 2014 will be allowed to use their Individual Exchange income tax credits for their Union benefits packages? Small businesses may not be as lucky.

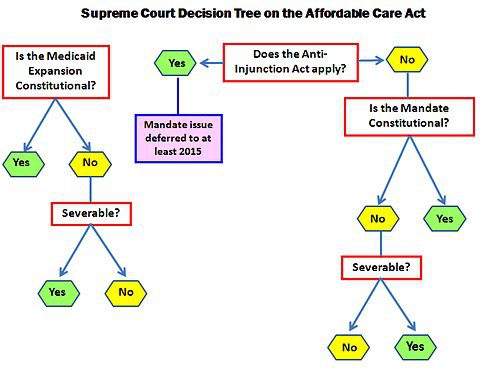

At 10 AM today the Supreme Court in a 5-4 decision upheld the Patient Protection and Affordable Health Care Act’s individual mandate as constitutional.

Imposition of a tax “leaves an individual with a lawful choice to do or not do a certain act, so long as he is willing to pay a tax levied on that choice,” Roberts says. “The Affordable Care Act’s requirement that certain individuals pay a financial penalty for not obtaining health insurance may reasonably be characterized as a tax. Because the Constitution permits such a tax, it is not our role to forbid it, or to pass upon its wisdom or fairness.”

According to Footnote 11, which is on page 44 of the slip opinion: Those subject to the individual mandate may lawfully forgo health insurance and pay higher taxes, or buy health insurance and pay lower taxes. The only thing that they may not lawfully do is buy health insurance and not pay the resulting tax.With this decision finalized, New York State (and the rest of the country) can now move forward with implementing the law. We embrace the much-needed clarity and looking forward to working with our clients moving ahead.Millennium Medical Solutions Corp will be planning health care seminars to review the decision and overview to help understand the impact on employers, plan benefits, and providers. We welcome your suggestions on specific topics or questions you want us to focus on. Please join us!

Our office will continue to monitor events and inform our members of any other important news.

The biggest Supreme Court Ruling in a decae is expected this Thursday before the Summer recess. Yet thats when the fun begins.Possible outcomes:

Delay hearing the legal issues associated with case for several years due to the Tax Issue.

Invalidate the Individual Mandate.

Invalidate all or part of the Medicaid Expansion requirements.

Uphold PPACA as is.

Declare the entire Act unconstitutional due to the lack of a Severability Clause if any of the key provisions such as the Individual Mandate overturned.

If individual mandate is repealed but leave other PPACA provisions in place, this outcome could greatly limit the coverage goals underpinning the Affordable Care Act and cause significant problems in the health insurance markets. For example, MIT economist Jonathan Gruber said, “Without a mandate the law is a lot less effective. The market will not collapse, but it will be a ton more expensive and cover many fewer people.”

While States such as NY may follow Massachusetts and set up their own Individual Mandate this becomes challenging with less Federal funding. Funding for the individual market place subsidy with subsidies could collapse. See subsidy calculator here.

Eliminating the mandate would increase premiums and mean that far fewer of the uninsured would be covered. This is known as adverse selection where the sick population would be willing to pay higher premiums and forcing the healthy population to opt out of exchange. States such as NY in fact have seen the Individual Market spiral out of control as they are high risk adverse group in order to supplement the preferred guaranteed non-preexisting condition group marketplace. Furthermore, NYS requires guaranteed issue for pre-existing condition for individual members with prior coverage. If the court invalidates the individual mandate and leave rest of Act in tact it may lead to a death spiral. Popular reforms such as overage 26 dependent coverage and expected pre-existing condition waiver in 2014 would possibly be dismantled.

The decision would punt health-care reform back to Congress, which “isn’t doing anything this year” and thus create major uncertainty going into the November elections. Taxes on pharma and medical devices would remain, while managed-care and hospital companies would suffer big losses. Insurers would be forced to take on sick patients without benefitting from the healthy ones who would have been enrolled under the mandate.

In this scenario, a lot of companies would simply cut their losses and leave the individual insurance market altogether; the law would essentially “run them out of business.

Either way the lack of uncertainty has delayed hospitals and insurers from new hires and taking decisive actions. Same time next week we hope to celebrate July 4th with certainty.

This month on April 12th, 2011 marked the five-year anniversary of Massachusetts 2006 State Health Care Reform. The reform was signed into law by then-governor Mitt Romney with the goal of providing affordable health insurance coverage to the estimated 6% of Massachusetts residents that were uninsured at the time.

Massachusetts State Health Care Reform and the Affordable Care Act are virtuallyidentical.Both reforms rely heavily on state-based health insurance exchanges, subsidies for qualifying individuals, and mandates for employers and individuals. As a result, Massachusetts presents the most appropriate example of what to expect from federal health care reform.

So, what have we learned from Massachusetts state reform? The 2006 Massachusetts State Health Care Reform:

Created the MAHealthConnector(a state health insurance exchange) to provide guaranteed issue health insurance to MA residents;

Mandated that every resident of the state obtain a minimum level of health insurance or face penalties;

Mandated that employers provide a “fair and reasonable contribution” to their employees’ health insurance premiums or face penalties; and

Provided free health insurance and partially-subsidized insurance to qualifying residents based on income.

Proponents of the law argue that Massachusetts Health Reform:

Has increased the percentage of private companies that offer health insurance from 70% in 2005 to greater than 77% today.

Has lowered the cost of individual health insurance premiums in Mass. due to the fact that primarily healthy people have moved to the individual market.

Opponents of the law argue that Massachusetts Health Reform:

Was setup for failure from the start due to its reliance on employer-sponsored health plans, plans that employers cannot afford due to rising costs.

Has resulted in more than half of the newly-insured residentsreceiving health insurance that is partially or completely subsidized by Massachusetts’ taxpayers.

Has Massachusetts health care reform been properly utilized as a test bed for Federal Reform? Will the costs associated with Massachusetts health care reform be sustainable over the long term?