Oxford /United Healthcare has announced last week their contract termination with the Valhalla teaching hospital, Westchester Medical Center effective May 1, 2012. The NYS “cooling off period” imposes both parties to renegotiate a contract until July 1st. The hospital will be considered in-network until that time.

This marks the second time a large health insurer has terminated their contracts with Westchester medical Center. Empire had terminated their contract on Nov 10, 2010 after a similar dispute and is still not under contract. While contractual posturing is all too common in the health industry with eleventh hour agreements, we are seeing this disturbing trend playing out in other instances now.

We will monitor the situation and keep members posted. Oxford member letters explaing this are going out. Please contact us with any questions.

We are always on the lookout for highly motivated individuals with relevant industry experience and a strong interest in our industry. We are particularly interested in people with backgrounds in hospitals, web technologies and HR consulting. A bilingual skill is also desirable. If you think your skills would be a good fit for our business, please forward your resume to info@medicalsolutionscorp.com. We look forward to hearing from you.

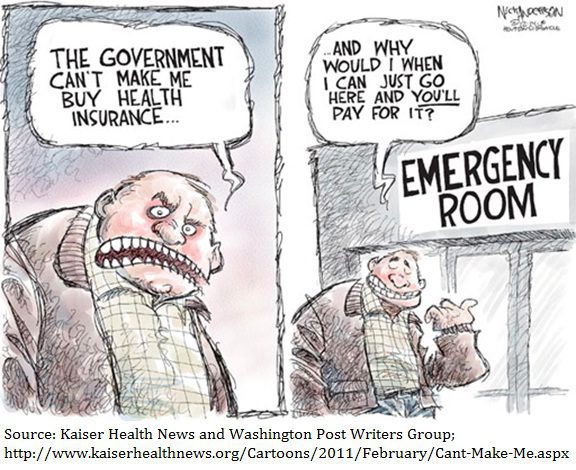

The same analogy would hold true with auto insurance where only the risky drivers would only participate making it impossible to afford coverage. Just imagine buying a health plan on the way to the hospital? Coining this as "ambulance-care" would be more fitting than "ObamaCare".

After 3 days of Health Care Reform Supreme Court Hearings, a central components debated is the constitutionality of forcing an individual to purchase health insurance. Certainly it would be costly if one could just opt out at any time and then come back in you would be left with a high risk pool.

The same analogy would hold true with auto insurance where only the risky drivers would only participate making it impossible to afford coverage. Just imagine buying a health plan on the way to the hospital? Coining this alternative as “ambulance-care” would be more fitting than “ObamaCare”.

Of course there are Individual Mandate penalties. So how does the penalty work?

In 2014, the penalty for being without health insurance is $95 per adult and $47.50 per child (up to $285 for a family) or 1.0% of family income, whichever is greater.

In 2015, the penalty for being without health insurance is $325 per adult and $162.50 per child (up to $975 for a family) or 2.0% of family income, whichever is greater.

In 2016, the penalty for being without health insurance is $695 per adult and $347.50 per child (up to $2,085 for a family) or 2.5% of family income, whichever is greater.

As of now, there are no known method to enforcing the penalty if you don’t buy insurance and you don’t pay the penalty. In fact, the law specifically states that no criminal action or liens can be imposed on you but I am certain that will change. I would also think that if a large numbers of people continue to choose not to enroll and the cost of premiums increase, the chance to revise the low penalties and increased enforcement are inevitable.

In conclusion, the Supreme Court ruling set for June is worth watching but only for legal wonks. With average health insurance single rates costing $600/month wouldnt you pay the penalty and just opt out?

Few healthcare changes have been more impacted than the out of control out of network charges billed to patients. The health care reform bill known as PPACA has for the most part been insignificant in the Northeast, in particular, as many state laws have already addressed issues such aspre-existing conditions, contraception, coverage rescissions and maximum loss ratios (MLR).

Instead, the market forces are reshaping the medical field into significant insurance & provider consolidation, larger hospital groups and flattening provider reimbursements. The problem is pointed out in Out of Network Medical Costs Affecting NY State Across investigation report commissioned by Governor Cuomo recognizing the unexpected out-of-network claim problem. Officials say that this is now “an overwhelming amount of consumer complaints.” Some examples cited in the report An Unwelcome Surprise – “a neurosurgeon charged $159,000 for an emergency procedure for which Medicare would have paid only $8,493.” Another example: ” a consumer went to an in-network hospital for gallbladder surgery with a participating surgeon. The consumer was not informed that a non-participating anesthesiologist would be used, and was stuck with a $1,800 bill. Providers are not currently required to disclose before they provide services whether they are in-network.” The average out-of-network radiology bill was 33 times what Medicare pays, officials say.

To make matters worse, Health Insurers have reduced their out of network recognized charges from private industry index UCR (usual customary and reasonable) to the Medicare Index known as RBRVS( Resource Based Relative Value Scale ). Insurers moved away from UCR after then-NYS D.A. Mario Cuomo in 2009 forced Unitedhelatcare Group (owners of Inginex) to settle $50 Million in a conflict of interest allegation. D.A. Cuomo future hopes for UCR were to that it be overseen by a non-profit entity. So much for best laid plans.

Today, 90% of SMB members have in network only benefits but the few remaining consumers are paying for eroding out of network benefits with little transparencies and necessary protection from new out of network billing practices. The NY Dept of Financial services is calling for providers in non-emergency situations to disclose whether or not all services are in-network, what out-of-network charges will be and how much insurers will cover.

In an ominous statement” “Failure to recognize this historical out-of-network avalanche will result in shocking financial disasters, as experienced by so many hospitals in 2003″

In a pleasant surprise, Empire will delay their April 2012 decision to “simplify” small group plans 1 more year from April 2012 to April 2013 instead. The Nov 4th Empire announcement to leave the NY Small Group Businesswas truly shocking after being in business for 75 years and insuring 35% of the market.

What this means for consumers is that insured members will now breath a sigh of relief and keep their contracted plan at least until their renewal. Evidentially, Empire was allowed to abruptly do a “hard shut down of their plans” for April and not allow a group to complete their 12 month contract. The negative consequence would have affected many unfairly as most members today have some kind of annual deductible and/or coinsurance on Rx plans, hospitalizations and surgeries. Example: a member signs up for a plan Oct 1 and has already met their deductible responsibilities would suddenly have to now change plans on April 2012. and start all over again.

A point needing further explanation is are they or they not exiting? Empire is stating that they are not in fact leaving but merely simplifying their offering to 6 plans but this is actually a red herring as the plans offered are not market friendly and allows Empire to stay within the market without having to really exit. Example: Their HMO monthly rate is $675/single when you can get the same plan from a leading competitor for $465/single.

So why be in the market without actually being in the market? The state’s regulation would not permit an insurer to re-enter for 3 years. With Health Care Reform changes in the subsequent years there are variables that may help NYS such as add’l federal funding. Additionally, it is an election year and with many unknown Health Care Reform variables still evolving such as Supreme Court hearing on individual mandate by June 2012 – WSJ Supreme Test for Health Law.

Either way this is welcome news to our existing clients and for the marketplace at large however short term it is.

Medicare Part A insurance helps pay for medically necessary care—care for an illness or medical condition—that involves an inpatient stay in the hospital. Part A also helps pay for a stay in a skilled nursing facility as a follow-up to a hospital stay, hospice care for the terminally ill and some skilled home health care for those who cannot leave their homes. And it helps pay for some blood transfusions.

What providers can you see?

You can choose any qualified provider in the United States who has been accepted by Medicare and who is accepting new patients. Because Part A offers the same benefits throughout the United States, you are not limited to a particular state or region for your care.

Part A is free if you or your spouse made payroll contributions to Social Security for at least 10 years (40 quarters).

If you otherwise qualify for Medicare but neither you nor your spouse contributed to Social Security for at least 10 years, you’ll pay a monthly premiums of up to $450 per month in 2011.

Important: If you don’t qualify for no-premium Part A benefits, and you don’t enroll in Part A when you first become eligible for Medicare, your Part A premium could be higher.

Before Part A begins paying a share of your costs, you must first pay a deductible. In 2011, your Part A deductible is $1,132. You’ll pay this deductible for each hospital stay, subject to certain limits.

Medicare Copay

You pay a copay after you have stayed in the hospital or in a skilled nursing facility a certain number of days. Here are the Part A copays for 2011:

For hospital stays, you’ll pay $283 per day for days 61 through 90, and $566 per day for days 91 through 150.

In a skilled nursing facility, you’ll pay $141.50 for days 21 through 100 that you stay.

You’ll also pay a copay of $5 for each outpatient drug prescription you receive in hospice care.

Medicare Coinsurance

You will pay a small coinsurance payment if you use inpatient respite care for hospice patients.

An overview of Medicare Part B

Medicare Part B insurance helps pay for a variety of medically necessary care—that is, care for an illness or medical condition. This includes services like doctor’s office visits, care in hospitals and clinics when you are not admitted for an inpatient stay, laboratory tests and some diagnostic screenings, and some skilled nursing care at home if you cannot leave your home.

Part B also covers most doctor services you receive as a hospital inpatient, although other hospital services are covered by Part A. Unlike Part A, Medicare Part B is voluntary, but most people sign up when they first become eligible.

In 2011, Medicare Part B is making it easier to get preventive care. It will now cover an annual physical exam plus additional preventive screenings at no cost to you.

What providers can you see with Medicare Part B?

You can choose any provider who is eligible to participate in Medicare and who is accepting new patients.

Most people pay a monthly premium for Medicare Part B. The premium amount depends on your yearly income. If you receive Social Security, the premium will be automatically deducted from your Social Security benefits. For 2011, premiums range from $115.40 to $369.10 per month.

Important: You may pay a penalty if you don’t sign up for Part B when you are first eligible. Your cost for Medicare Part B may go up 10% for each full 12-month period that you could have had Part B but didn’t sign up for it. You’ll pay that penalty for as long as you’re enrolled in Part B.

This penalty may not apply to you if you are still working for an employer who provides group health coverage or if you have other credible coverage when you become eligible for Medicare.

As per todays Crains article, Empire Blue Cross will be exiting the majority of small group health plans effective April 1, 2012. The news was swirling earlier this week with official Empire communication going out today.

This affects 1/3 of New York Small Businesses as defined by 50 or less FT and eligible employees. Since with large group market the insurer is allowed to rate a group based on true census and make up of a group’s sex, age and family status as well as claims experience of the prior year. In NY State where the small group market is Community rated and independent of census this becomes an important point that I will get back to.

As healthcare has become regulated by MLR(Max Loss ratios) or revenue controls its not surprising that insurers are unhappy but why does it seem that in NYS regulations run deeper than in other states? We are licensed in multiple states and we are not seeing the same pattern this quickly. Numerous companies have already exited such as CIGNA, HealthNet, Horizon, Guardian not to mention M&A of HIP/GHI, Oxford/UnitedHealthcare and Aetna/US Healthcare/NYLCare etc. I can go on.

In NYS the insurance regulations go beyond Health Care Reform (PPACA) with higher MLR than the national one. The Federal level is 80% for small groups and in NYS its 82%

There are new NYS price controls where insurers must anticipate risk a year in advance and ask for larger rate increases to protect on anticipated uncertain risks. With so many unknown variables its almost like asking one to predict who’s going to win the Super Bowl in 2013. Rate increase of 15-20% requests must be higher than usual since after all there are no State protection on the loss side. Furthermore, increases of 10%+ must now require public hearings 60 days prior.

Today, we have so many State mandates that many of the mandates(overage dependents coverage, preventive care, pre-existing for kids) in PPACA didnt even affect NY since they were already in place. Mandates account for approx 17% of the costs of which Small Businesses pay more than fair share. Large corporations and Unions can self insure and avoid some mandates as they are governed by ERISAand not State. To the relief of of our struggling clients on subsidized Healthy NY the State doesn’t play by their own rules and instead opts out of its very own mandates.

So what happened with Empire? The tipping point evidently was rate increase denials of 5 consecutive quarters and that Empire quite frankly got caught with great pricing and products just when healthcare reform came around. Many insurers raised their rates in advance of the law. Emblem (GHI) raised rates 25% on average and even as high as 60% on HSA. Granted they have also removed many plans recently.

Much like in the 70’s its a regulaed oligipoly with insurers too too big to fail. Our clients will have access to only 3 insurer – Aetna, Emblem and Oxford. Just imagine how high your Auto Insurance would cost in the same scenario? This remarkable in a 25 million metropolis like NYC. Insurers do not have to be in NYS, no new carrier is looking to enter the NY market. After 75 years in business and insuring 4 generations of small businesses this should be a shock to the system and a wake up call to every politician.

We ask for greater oversight on Mergers and Acquisition of health insurers,providers and hospitals. Its begining to dawn on everyone that a too big to fail environment is poison and will be the tail that wags the dog. I can only imagine what the other remaining insurers must be thinking whats in store for next year.

Importantly, the community rating ought to be dropped as most states such as NJ, CT are census based. With Health Exchanges coming in 2014 individuals will be able to purchase health insurance on their own which will make Community Rating less relevant. This will be a positive step in allowing great competitors like Humana to enter the market.

If this is not a wake up call for small businesses to have a seat at the table I dont know what is. Anyone in for an Occupy Albany?

Medicare Advantage plans are a popular low cost alternative to Medigap coverage. These insurance policies are offered by private insurance companies with a contract from Medicare. Advantage plans will usually have a low or $0 premium in addition to your regular Part B premium. This type of plan may include Part D prescription drug coverage although health coverage only is also available.

There are many types of Medicare Advantage plans available and you should check to see which plans are offered in your county. We have included some brief descriptions and helpful tips to provide you with a better understanding. You may also contact us to speak a live representative who will answer any specific questions that you may have.

Medicare Health Maintenance Organization (HMO)

Health Maintenance Organization members are required to choose a primary care physician within the plans network. In order to see a specialist you will need to get a referral from your primary care doctor. The specialist must also be in the plans network. You must also use network providers for all other services including hospitals, lab work, and durable medical equipment suppliers. HMO plans usually offer the lowest premiums and copayments. This is a good choice if your Doctors and health providers are a part of the plan network.

HMO Point Of Service (POS)

A Point of Service (POS) plan is a type of managed health care system that combines characteristics of the HMO and the PPO. Like an HMO you pay only a minimal co-payment when you use a health care provider within your network. You also must choose a primary care physician. If you choose to go outside the network for health care, POS coverage functions similar to a PPO.

The plan will specify which benefits are available under the POS option and how much the co-payment will be for out-of-network benefit.

Medicare Preferred Provider Organization (PPO)

Preferred Provider plan members have more freedom of choice. A PPO also has a network of providers but you are free to use out of network providers if you wish. You will simply pay a slightly higher co-payment when using out of network Doctors and health care providers. These plans offer local, regional or Nationwide coverage. A good choice for those who travel or simply wish to have greater flexibility.

Private Fee For Service (PFFS)

Private Fee For Service plans do not have a network. You can use this plan at any Doctor or provider who agrees to the terms and conditions of payment from the plan. These plans include Nationwide coverage and are a good option for those who travel or live in a rural area. PFFS plans are only offered in select Counties.

Medicare is a Federal health insurance program for people 65 years or older, certain people with disabilities, and people with end-stage renal disease (ESRD). Medicare has two parts — Part A, which is hospital insurance, and Part B, which is medical insurance.

Who is eligible for Medicare?

Generally, Medicare is available for people age 65 or older, younger people with disabilities and people with End Stage Renal Disease (permanent kidney failure requiring dialysis or transplant). Medicare has two parts, Part A (Hospital Insurance) and Part B (Medicare Insurance). You are eligible for premium-free Part A if you are age 65 or older and you or your spouse worked and paid Medicare taxes for at least 10 years. You can get Part A at age 65 without having to pay premiums if:

You are receiving retirement benefits from Social Security or the Railroad Retirement Board.

You are eligible to receive Social Security or Railroad benefits but you have not yet filed for them.

You or your spouse had Medicare-covered government employment.

If you (or your spouse) did not pay Medicare taxes while you worked, and you are age 65 or older and a citizen or permanent resident of the United States, you may be able to buy Part A. If you are under age 65, you can get Part A without having to pay premiums if:

You have been entitled to Social Security or Railroad Retirement Board disability benefits for 24 months. (Note: If you have Lou Gehrig’s disease, your Medicare benefits begin the first month you get disability benefits.)

You are a kidney dialysis or kidney transplant patient.

While most people do not have to pay a premium for Part A, everyone must pay for Part B if they want it. This monthly premium is deducted from your Social Security, Railroad Retirement, or Civil Service Retirement check. If you do not get any of these payments, Medicare sends you a bill for your Part B premium every 3 months.

The retirement age for Social Security is increasing until it reaches age 67. Will I still get Medicare at age 65 if I’m not yet eligible for Social Security retirement benefits?

Although the retirement age is rising, 65 remains as the starting date for Medicare eligibility. You will be eligible to apply for Medicare if you have paid into Social Security for at least 10 years or you are eligible to receive Social Security benefits on your spouse’s earnings. If you do not meet these requirements, you can still get Medicare hospital insurance (Part A) by paying a monthly premium if you are a citizen or a lawfully admitted alien who has lived in the U.S. for at least five years. Also, anyone who is age 65 and a citizen or a lawfully admitted alien with five years of residency in the United States can sign up for Medicare Part B medical insurance and pay a monthly premium. Be sure to sign up for Medicare about three months before you reach age 65. And remember, you do not have to be retired to enroll in Medicare. For more information about retirement, visit www.socialsecurity.gov or call 1-800-772-1213 (TTY users should call 1-800-325-0778).

What is “assignment” in the Original Medicare Plan and why is it important?

Assignment is an agreement between Medicare and doctors, other health care providers, and suppliers of health care equipment and supplies (like wheelchairs, oxygen, braces, and ostomy supplies). Doctors and suppliers who agree to accept assignment accept the Medicare-approved amount as payment in full for Part B services and supplies. You pay the coinsurance and deductible amounts. In some cases (such as if you have both Medicare and Medicaid), your health care providers and suppliers must accept assignment. If assignment is not accepted, charges are often higher. This means you may pay more. In addition, you may have to pay the entire charge at the time of service. Medicare will then send you its share of the charge. There is a limit on the amount your doctors and providers can bill you. The highest amount of money you can be charged for a covered service by doctors and other health care providers who don’t accept assignment is called the limiting charge. The limit is 15% over Medicare’s approved amount. The limiting charge only applies to certain services and does not apply to supplies or equipment.

Where can I find a list of all physicians that participate in Medicare?

A list of participating physicians in your area can be found in the Participating Physician Directory section in the www.medicare.gov website. Or, your local Medicare Carrier can assist you with this question. You can find their phone number in the Helpful Contacts section of www.medicare.gov.

Why aren’t all Medicare participating healthcare professionals included in the Participating Physicians Directory?

The healthcare professionals listed in the Participating Physician Directory on www.medicare.gov is derived from the Unique Physicians Identifier Number (UPIN) directory. This directory is limited to practitioners who have the following academic credentials:

Medical Doctor (MD) Doctor of Osteopathy (DO) Doctor of Optometry (OD) Doctor of Podiatric Medicine (DPM) Doctor of Dental Medicine (DM) Doctor of Dental Surgery (DDS) Doctor of Chiropractic Medicine (DC)

We acknowledge the fact that there are several other Medicare participating healthcare professionals that have other academic credentials and are not included in the UPIN directory and subsequently are not listed in the Participating Physicians Directory at this time. The healthcare professional classifications that are not included in the UPIN directory include, but are not limited to:

Medicare uses your personal information to administer our country’s largest health insurance program for the elderly, disabled, and people with end-stage renal disease. Some of the ways Medicare uses your personal information are to:

Pay your medical bills for Medicare benefits

Make sure you get quality health care

Set the Medicare payment rates for doctors hospitals and other health care providers, and

Make sure that Medicare does not pay for health care providers or services that you did not get.

How is the privacy of my medical records protected?

You have the right to talk with health care providers in private and to have your personal health care information kept private as protected under federal and state laws. There is a new patient privacy rule that gives you more access to your own medical records and more control over how your personal health information is used by your health care provider or your health plan. This rule will be fully effective on April 14, 2003. If you have any questions about this privacy rule, look at the National Standards to Protect the Privacy of Personal Health Information on the web. If you are in a Medicare managed care plan or a Medicare Private Fee-for-Service plan, you also have the right to timely access to our medical records.

How does Medicare protect my personal information?

The Privacy Act protects the personal information about you that Medicare uses. This law requires that all federal agencies, and their contractors, follow certain rules to protect any personal information which they collect, use, or disclose. Medicare managed care plans are not required to comply with the Privacy Act, but your personal information is still protected. Medicare managed care plan materials (e.g., Evidence of Coverage) describe your privacy rights. You should contact your managed care plan directly for more information.

Source: www.medicare.gov – The official U.S. site for people with Medicare

Advantage Plans, are health plans from insurance companies that have a contract with CMS (Center for Medicare and Medicaid). Individuals who have Medicare Part A and B are eligible to choose a Medicare Advantage plan. Specialized plans exist for people with certain health conditions, but beyond that the general plans are not allowed to decline based on health except for very specific reasons.

When an individual is enrolled in the plan they do not lose their Medicare. They are entitled to cancel their Medicare Advantage plan, and the next month, they can go back to original Medicare. While enrolled in Medicare Advantage, they will have to use the insurance card provided by the Medicare Advantage plan instead of their Medicare card.

These plans may cost the participants nothing, or very little, though many still require the Part B participation amount. A Medicare Advantage plan is not free however. The plans receive a contribution from CMS every month, instead of having that tax money go to original Medicare. That is how the bulk of the plan is paid for, from tax money.

Traditionally, Medicare Advantage Plans were thought of as HMO plans were an insured person had to use the plan hospitals, doctors, and other medical providers to be covered. Many Medicare Advantage Plans are HMO plans. However, PPO Medicare Advantage plans also exist. Fee for Service Medicare Advantage Plans, or plans that will cover any medical providers who accept the insurance, are being marketed aggressively these days.

Your own medical needs and preferences will determine which plan will work out well for you. If your current medical providers contract with the plan’s HMO, then you may be very satisfied with comprehensive coverage with very little extra payments. If you like more choice, and area doctors will accept a Free For Service plan then you might consider an “Any Doctor” plan. Be aware that not all doctors work with the Fee For Service plans, even though the insurance company claims it will work with any doctor! A great compromise is provided by PPO plans. You get the greatest coverage at the lowest price inside the network, but will still be covered by other medical providers.

Most, but not all, Medicare Advantage plans also contain Part D, or prescription drug coverage. Medicare Advantage plans may have very low, or no, premium for the insured people beyond their normal Part B premium. Some plans even refund the Part B premium. Also, Medicare Advantage Plans are not allowed to do a lot of risk selection based upon health, so they may be a good choice for less healthy applicants.

A traditional Medicare Supplement is very different from Medicare Advantage. With Medicare Supplements you still use your original Medicare Card, and add your Medicare Supplement health card. These plans are also provided by insurance companies, but they simply supplement the coverage gaps and deductibles not provided by original Medicare Part A and Part B.

If you have Medicare Part A and Part B, your Medicare supplement plan will pay the portion of your medical bill that Medicare will not pay. Of course, Medicare supplement plans differ, and so you need to be aware of exactly which portions a Medicare Supplement plan will pay before you sign up. For instance, Medicare may be 80% of your hospital bill, and your supplement will pick up the other 20%.

Medicare supplements come with premiums, and also may exclude unhealthy individuals. However, they generally provide the broadest access to health care.

Choosing a Medicare health plan can be one of the most important decisions a Medicare beneficiary will make. Let us help you find the right plan to fit your needs, lifestyle, and budget.