It’s not about a number … The North Shore-LIJ CareConnect network is built around the North Shore–LIJ Health System, its employed physicians and thousands of select affiliated community providers.

This network is designed to provide you access to the highest quality doctors, so choosing the right provider is worry free.

-17 hospitals, 8,000 providers, and an additional 12,000 contracted providers

-Future expansion includes network in northern NJ, Western CT, and Westchester.

-Partnership with CVS/MinuteClinic to provide basic care outside of the service area.

-New “Tradition” plans put the co-pay first, like we’re used to.

What makes CareConnect unique:

Concierge style service.

Call their customer support, speak with a real person empowered to help.

They’ll even find a doctor, and schedule an appointment, for a time that works for you.

Integrated care.

Low denial rate.

Integrated medical management.

Customer care centers for those who want to stop in and ask questions on their plan, their care, or even payment assistance.

Voluntary Dental,Vision, Life, Accident and Disability

Dental

HealthPass offers four great dental options; Guardian Managed DentalGuard (DMO),Guardian Managed DentalGuard Plus, (DMO), Guardian DentalGuard Preferred (DMO/PPO, and Guardian DentalGuard Preferred Plus (DMO/PPO)). Managed DentalGuard provides you and your family with accessible, quality care. The DentalGuard network is comprised of carefully selected dentists dedicated to delivering personalized In-Network services, with an emphasis on preventive treatment. DentalGuard Preferred combines the freedom of choice of In-Network or Out-of-Network care, although you will typically receive a higher level of benefits and save on out-of-pocket costs if you visit an In-Network dentist.

Guardian VisionGuard provides access to the Davis Vision network. Exams and materials are covered and members can visit any doctor they wish using both In and Out-of-Network benefits. Members have access to to generous discounts including up to 25% off laser vision correction, discounts on glasses and cosmetic enhancements such as tints, special lenses and scratch-resistant coating.

HealthPass makes it easy for employers to offer EverGuard, EverGuard Plus and now the EverGuard Dual Option. Personal protection from Guardian offers Term Life, AD&D and Long Term Disability. The coverage is available on a guaranteed basis, no medical examination and no industry will be excluded. These complete benefit packages are offered with low monthly premiums based on ages.

All employees enrolled in medical coverage have access to this advocacy and assistance company. Registered nurses can help guide members through questions regarding claims, healthcare bills, authorizations, finding doctors and hospitals as well as scheduling specialists. Click herefor additional information.

** Healthpass Renewal Enrollment/Change Form ** – need this form to make changes such as switching plans, insurers, dental, vision, life insurance/disability package before your renewal. You cannot make plan changes midyear.

It’s not about a number … The North Shore-LIJ CareConnect network is built around the North Shore–LIJ Health System, its employed physicians and thousands of select affiliated community providers.

This network is designed to provide you access to the highest quality doctors, so choosing the right provider is worry free.

-17 hospitals, 8,000 providers, and an additional 12,000 contracted providers

-Future expansion includes network in northern NJ, Western CT, and Westchester.

-Partnership with CVS/MinuteClinic to provide basic care outside of the service area.

-New “Tradition” plans put the co-pay first, like we’re used to.

What makes CareConnect unique:

Concierge style service.

Call their customer support, speak with a real person empowered to help.

They’ll even find a doctor, and schedule an appointment, for a time that works for you.

Integrated care.

Low denial rate.

Integrated medical management.

Customer care centers for those who want to stop in and ask questions on their plan, their care, or even payment assistance.

Employers incentivizing fitness by lowering lower insurance premiums in exchange for wearing fitness tracking bracelets. Bloomberg reports that BP Plc drive for occupational wellness offered an employee’s spouse the option “to wear a fitness-tracking bracelet from FitBit Inc. to earn points toward cheaper health insurance,” which is “an example of how companies, facing rising health expenses, are increasingly buying or subsidizing fitness-tracking devices to encourage employees and their dependents to be more fit.

” The article notes that UnitedHealth Group Inc. (UNH), Humana Inc. (HUM), Cigna Corp. (CI) and Highmark Inc. have developed similar programs, in which “consumers wear the device and the activity data is uploaded to an online system so it can be verified to give a person their reward.” The article notes, however, that “the moves also let employers and insurers gather more data about people’s lives, raising questions from privacy advocates,” one of whom notes that “when financial incentives are involved, Dixon said it forces employees’ hands and narrows the question of whether or not they should participate.”

Wear This Device So the Boss Knows You’re Losing Weight

To fight rising medical costs, oil company BP Plc (BP) last year offered Cory Slagle — a 260-pound former football lineman — an unusual way to trim $1,200 from his annual insurance bill.

One option was to wear a fitness-tracking bracelet from Fitbit Inc. to earn points toward cheaper health insurance. With the gadget, the 51-year-old walked more than 1 million steps over several months, wirelessly logging the activity on the device. Twelve months later, Slagle has added to his new exercise regimen by trading burgers for salads and soda for water, dropping 70 pounds (31.8 kilograms) and 10 pant sizes in the process.

“I can see my toes now,” said Slagle, a middle-school administrator whose wife, Kristi, works for BP in Houston. The company’s program, he said, is “pushing me to get off the couch and make the right decisions.”

Slagle’s wife is thrilled with his thinner frame — as is BP. His once-high blood pressure and cholesterol are now in a normal range, significantly lowering BP’s risk of covering treatments related to heart trouble or other medical problems.

Slagle’s experience is an example of how companies, facing rising health expenses, are increasingly buying or subsidizing fitness-tracking devices to encourage employees and their dependents to be more fit. The tactic may reduce corporate health-care costs by encouraging healthier lifestyles, even as companies must overcome a creepy factor and concerns from privacy advocates that employers are prying too deeply into workers’ personal lives.

Source: Cory Slagle via Bloomberg

Cory Slagle wore a fitness-tracking bracelet from FitBit Inc. to earn points toward… Read More

Insurers Too

Apart from BP, insurers includingUnitedHealth Group Inc. (UNH),Humana Inc. (HUM), Cigna Corp. (CI) and Highmark Inc. have also created programs to integrate wearable gadgets into their policies. The aim is to get people more invested in taking care of themselves. Consumers wear the device and the activity data is uploaded to an online system so it can be verified to give a person their reward.

“What employers want is the person to take an active role in their health,” said Dee Brock, who has incorporated wearable devices into wellness programs for Pittsburgh-based HighMark.

Privacy Flags

The adoption of wearable devices by companies and insurers is increasing as spending on corporate wellness incentives has doubled to $594 per employee since 2009, according to a study by Fidelity Investments and National Business Group on Health. Technology is creating new forms of wellness programs to measure whether employees are making improvements, similar to a trend in the car-insurance industry where drivers who put a monitoring sensor on their vehicle can earn lower rates based on how well they are driving, instead of their driving history.

Source: Cory Slagle via Bloomberg

Cory Slagle lost 70 pounds after starting to wear a FitBit given to him by energy…Read More

Yet the moves also let employers and insurers gather more data about people’s lives, raising questions from privacy advocates. Wearable gadgets are advancing beyond tracking steps, with sensors to monitor heart rates, glucose levels, body temperature and other functions.

“The focus on preventive health at the expense of privacy is dangerous,” said Pam Dixon, founder of the World Privacy Forum in San Diego, which focuses on health privacy issues. “Right now it’s tracking steps per day, and the reach isn’t that far with these devices, but in time it will be quite sophisticated.”

When financial incentives are involved, Dixon said it forces employees’ hands and narrows the question of whether or not they should participate. The gathering of health data also opens the door for people to eventually be charged more or less based on the information, she said.

Security Requirements

These are among the ethical questions still to be addressed about the appropriateness of companies tracking the physical activity of employees, said Harry Wang, a researcher for Parks Associates who has been studying the market. With wearable devices, collecting more sensitive information is likely to bring tougher government oversight, he said.

“There will be high levels of privacy, security and compliance requirements,” Wang said. “There will be high expectations from consumers about how the data will be used.”

Companies and insurers said they protect the privacy of people using wearable gadgets, and comply with federal laws that prevent employers from seeing certain health information about employees without consent. The wearable programs are voluntary and often administered by third-party vendors like StayWell, which works with BP.

Aggregated Only

As part of the BP program, employees who use a Fitbit to log 1 million steps earn half of the 1,000 points needed each year to qualify for lower co-pays, deductibles and out-of-pocket health expenses. BP bought 25,000 Fitbit devices for North American employees, including those at refineries and drilling rigs. Points can also be earned by getting an annual physical, taking an online health class and other initiatives.

“We think the device is easy to use, gets people aware of how little they are walking and helps trigger people to get active,” said Karl Dalal, director of health and wellness benefits at BP. “BP doesn’t see any of the data except in the aggregate.”

The market for wearable devices is small — about 2 percent of the 1 billion smartphones shipped globally last year — so creating interest from employers and insurance companies is key to growth. Some 22 million fitness-tracking devices will be sold this year, and 66 million by 2018, with about a third coming from corporate-wellness programs, according to Parks Associates. The incentives an employer or insurance company can offer is a way to keep people using the gadget, instead of throwing it in a drawer once the novelty wears off.

Targeting Businesses

Under the Affordable Care Act, the new national health-care law, companies can spend as much as 30 percent of annual insurance premiums on rewards for healthy behavior.

Technology companies are taking note. Apple Inc. (AAPL), which has new health-tracking software called HealthKit that will be released this year and is said to be developing its own wearable device, has talked with UnitedHealth, the biggest U.S. insurer, and Humana, about its health initiatives, executives at the insurance providers said. The companies wouldn’t provide specifics about the conversations. Apple declined to comment.

Fitbit has a sales force dedicated to pitching employers and insurance companies, and touts software to make it easier to log the activity of workers, down to specific individuals if a company wants, said Amy McDonough, who coordinates deals for Fitbit with companies. Other makers of wearable devices, including Jawbone, Samsung Electronics Co. (005930) and iHealth Lab Inc., have also targeted businesses.

Samsung leads the smart wearable-band market, according to a report today from Canalys. The researcher estimated the wearable band market grew almost eightfold in the first half of 2014 from a year ago.

Insurance Link

Some employers are encouraging the use of wearables without the gadgets being tied to lower insurance rates. Houston Methodist, owner of a chain of hospitals in the Houston area, got about 6,000 Fitbits this year and is offering employees the chance to win $10,000 if they walk more steps than the company’s top executives. Fitbit said it also works with Time Warner Inc. (TWX) and Autodesk Inc. (ADSK)

“Walking alone isn’t going to beat diabetes, but it’s certainly going to help,” said Marc Boom, chief executive officer of Houston Methodist. “Being more active results in better health. That’s indisputable.”

Scotty’s Brewhouse

At Scotty’s Brewhouse in Indianapolis, where the $15 “Big Ass Brewhouse Burger” includes four quarter-pound beef patties and American cheese, owner Scott Wise offers an extra day of vacation for managers at his 11 restaurants who use a Jawbone UP device to log an average of 10,000 steps a day for three months. That has some managers like Brian Winnie exercising more to earn time off for a trip he wants to take to Memphis, Tennessee.

“Outside of work, I picked up riding my bike to add extra steps that way,” Winnie said in an interview.

Despite some early enthusiasm, many companies are waiting to see whether the use of wearables is a fitness fad. No major research has been done that shows the use of these devices leads to lower health-care costs and many employers want to know “if this is something that’s a passing trend or something that has staying power and can have proven results,” said Eric Herbek, who runs digital engagement for Cigna.

The gadgets have been worthwhile for Chris Barbin, CEO of Appirio Inc. in San Francisco. He said about 40 percent of his staff, which numbers around 1,000, participates in a voluntary fitness program that includes uploading their activity with Fitbit.

$300,000 Discount

While health costs weren’t the priority for the program, Barbin said that by sharing the data with the company’s health care provider he negotiated $300,000 off his company’s roughly $5 million in annual insurance costs by showing his staff is getting healthier. He said privacy protections are in place for those who want to keep the data secret. The program has become one of the most popular forums on Appirio’s internal social network, he said.

“We had an initial batch of data about people who had lost weight, and people who had moved from high risk to moderate risk,” he said. “When we could show all that information to our insurer, that’s pretty powerful.”

Kristi Slagle, whose husband slimmed down through BP’s program, isn’t concerned about privacy with the gadgets. She said the program injects more fairness into the system because those who are healthier currently end up shouldering more costs for those who aren’t.

“I like that BP is making people more accountable,” she said.

OK so this may not be the catatonic movie of our favorite State starring Zach Braff and Natalie Portman but just the same Oxford couldn’t resist using the same logical name for the new network. Starting Sept 1, 2014 Oxford will be offering the Oxford Garden State Network on all size NJ group business. The 18,000 Doctor and 65 hospitals network will answer the call for a flexible lower cost plan option.

Judging by the #1 selling plan – Oxford Liberty HMO the market supports a smaller lower cost quality network. Taking the same playbook Oxford unveiled their plan last Friday. The plan will cover members outside NJ only on emergencies. Unlike the Liberty HMO some plans options are non-gated plans not needing referrals to for access to a Specialist Doctor.

The Garden State Network provides access to the 21 New Jersey counties only.The Garden State Network does not provide national access to the UnitedHealthcare Choice Plus network. For NJ 1-50, up to 4 plan options can be selected and the Garden State products can be paired with Liberty and Freedom network options. With this network, employers can select which of the 13, in-network only plan designs available will work best for their needs and for the needs of their employees.

Oxford/United has been purchasing Provider groups since 2011 , see our post UnitedHealthcare Buying Medical Groups? This strategy of late is by no means exclusive to this Insurer but it is worth pointing them out as they are a national leading health Provider and worth paying attention to.

Some highlights of the plan designs available with the Oxford Garden State Network are below:

∙ Routine, in-network preventive care covered at 100 percent

∙ In-network only coverage

∙ Choice between 11 non-gated and two gated plan designs (gated plan designs will require a referral)

∙ Plan designs with copayments, deductible and coinsurance, and Health Savings Accounts (HSA) are available.

Sign up for latest news updates. Please contact us for immediate information on how to implement these initiatives for your group-specific needs at info@medicalsolutionscorp.com or Call (855) 667-4621.

Painful wait times at the doctor’s office… It’s an old story with few exceptions.

As a dad, I have to deal with many of the same issues of parenting that you deal with: sleepless nights , fevers and holding my kids down for shots (My wife did it once, I think, then she promptly retired from this job.). However, waiting at the pediatrician is not something I have to do. So, I can’t truly empathize with you on this one….

Because you guys know me and know I’m not one to defend the status quo…I’m going to go ahead and defend the status quo a little bit. Or, at least, sound like I am (whether I am or not).

Here are some (in my mind) acceptable reasons why wait times are long:

Scheduling – Doctors, pediatricians specifically, are often over-scheduled. We generally come out of school with the same amount of debt as our doctor friends who have entered more “lucrative” specialties. The only way to make up some of the difference (and pay back our loans) is to see more patients. Thus, patients are scheduled closer together. This normally does not cause problems…but stuff happens.

Emergencies – If you have a doctor with hospital privileges (especially one who goes to deliveries), emergencies will happen. Getting called to a C-section can ruin an entire afternoon for a busy pediatrician. Great partners (like the ones I had in Abilene) will try to pick up the slack while you are gone but it is a strain on the whole system. What about other little “emergencies”? The teenager who reveals during their well child exam that they are depressed and suicidal. The 6-year old getting an MRI for headaches that turn out to have been caused by a brain tumor. Yes, I could assign those conversations to someone else by referring to the ER or the specialist, but wouldn’t you want it to be your pediatrician walking you through that?

Here are some (in my mind) unacceptable reasons why wait times are long:

Too Much Time Out-of-Room for the Doctors – I heard a story once about a doctor whose patients complained that his wait times were too long. He in turn complained to his staff that they were too slow. Come to find out, every morning, before he saw any patients, he sat down at his desk and read the entire paper, cover to cover. He had patients waiting 15 minutes completely ready for him to see but was sitting in the back office. 15 minutes might not be terribly inconvenient but that 15 minutes, on a bad day, will turn into 30-45-60 minutes that could have been avoided. Reading the paper may not be much of a temptation these days, but spending time on the computer doing other stuff is huge. I have to make a point not to be on Facebook, Twitter and other social media during patient care time. I do my social media and blogging before patients arrive and at lunch.

Poor Work-Flow in the Office – In Abilene, I had a very hard working MA and LVN (shout out to Nikea and Beth!) that understood how important this issue was to me. There are other ways to know if work-flow is the problem but one thing is certain: if you can’t see your first patient of the day in time, then there’s something wrong.

Chronic Over-Scheduling – While I do understand the issues related to scheduling, I don’t excuse the doctor for always having a schedule such that they run behind every day. Something can be done.

Now, you can read over this and take it however you want, but keep this in mind: you almost always have a choice in medical care. Unless your child needs a specialist for which there is only one in town or you live in such a rural area that there is only one provider, you have a choice. When we make any choice, we prioritize what’s important…someone might choose to see a doctor they love and tolerate the fact that their wait times are longer (but continue to complain on Facebook about it-I get it, it’s ok). Other people might drive more miles to see one they love. The choice still lies in the hands of the parents.

Ultimately, waiting anywhere is hard. Waiting in the doctor’s office is especially hard when you have a sick child, no one slept the night before, and the only appointment available was right in the middle of nap time.

I promise to keep working on those things that I can do in order to shorten your wait time and you can stay tuned for tomorrow’s post:

Justin Smith is a pediatrician who blogs at DoctorJSmith. He can be reached on Twitter @TheDocSmitty.

Congratulations – you just signed up successfully for Obamacare! You made it right before the March 31st deadline and avoided the individual penalty and getting blocked out for 2014. Don’t relax just yet. If you’re one of the many people who applied on the first open enrollment it’s smart to expect some bumps over the next few weeks. Shifting deadlines and technical glitches have left many insurance companies scrambling to catch up to the flood of requests. To make sure you start things right, here are some easy ways to stay vigilant:

Pay the premium –Until you pay for the plan you do not truly have a plan just yet. Some states and insurance companies have extended the deadline to pay, but its best to do this as soon as possible. For maximum peace of mind, get written confirmation from your new insurance company. If you go to the doctor before you pay your premium, you may end up footing that medical bill if the insurance company doesn’t have a record of your premium payment.

Member ID Cards –in about 1–2 weeks after you receive your first bill you will receive your Member ID card from your carrier after you’ve made your first premium payment. This is the card you’ll share with medical providers and pharmacies when you receive service. Your carrier may allow you to print a temporary ID card if you need care prior to receiving your Member ID card(s). Your insurance card will (hopefully) arrive in your mailbox in early January. You’ll present it wherever you need services: at the pharmacy, doctor’s office or hospital. Since insurance companies had a very short turnaround time to process new members, you may see a delay. Don’t panic! Go to the insurance company’s website to see if you can print a temporary ID card. (This is a lifesaver!) If you turn up empty, call the company’s customer service number to confirm that you are in their system as an enrolled member.

Don’t rush to the doctors – If you have an immediate need for a prescription or an appointment, by all means take care of it asap. But if you can, wait a few weeks before scheduling your doctor’s visit. This will give time for the insurance companies and doctors to update their systems with all the new plans and enrollees. This way, you help ensure that the medical claim for your doctor’s visit will be processed accurately – and that you dodge some of the early-stage craziness.

Double check – that your doctor is in your new plan’s network . Most of the new insurance plans also came with new provider networks. Its smart to double check that your favorite doctor is in the network for the exact plan you just enrolled in. There are specific networks for different insurance products, so make sure you are checking the right one. If your doctor is not in the network, keep in mind that you may have to pay significantly more money to see an out-of-network doctor, so you may consider switching. See States Pushing Back Against Smaller Networks

Keep records – Keep a record of your payments, calls, emails with your insurance company and physicians. Just in case of a technical glitch in the insurance or doctor’s computer systems, you can show evidence of your payment or confirmations from your insurance company.

Obamacare 2014 Deadline Nearing. You are now more knowledgable than most after reading this article. Given all the new changes thanks to the new insurance plans, new enrollees, and changing deadlines, being aware of these simple tips will help you avoid unnecessary headaches. And remember, if you are still shopping for insurance, you only have until March 31st to enroll in a plan.

For enrollment help before the deadline information please contact our team at Millennium Medical Solutions Corp (855)667-4621. We have Spanish, Russian, and Hebrew speakers available. Quotes can also be viewed on our site.

Officials in at least a half dozen states are pushing back against health plans in the new insurance markets that limit choice of doctors and hospitals in a bid to control medical costs.

The plans don’t start offering coverage until January but they’re facing regulatory action, possible legislation, and in at least one case involving a high-profile children’s hospital, litigation.

The pushback against “narrow” provider networks recalls the backlash against managed care and health maintenance organizations in the 1990s. Protests from consumers and hospitals eroded those attempts to restrain expenses by narrowing provider networks.

Now criticism of limited networks has risen as consumers realize that, despite President Barack Obama’s pledge that they could keep their doctors, their Affordable Care Act insurance may not include the physicians or hospitals they’ve been seeing.

The critique feeds into the politically damaging outcry over the millions of people whose health plans were cancelled. It’s unclear whether the limited choice of doctors and other providers will be as much of a concern to uninsured people who will be gaining subsidized coverage through the state-based marketplaces.

Still regulators and elected officials in a few states have already forced changes. Others are weighing legislation that could expand the networks. Legal fights are brewing. In some cases, the officials are responding to complaints of health care systems or providers that were excluded.

In Maine, state regulators prohibited Anthem BlueCross BlueShield from switching some customers to a network sold through the Affordable Care Act’s marketplace that excluded six of the state’s hospitals.

In Washington State, the insurance commissioner initially banned several health plans from the online exchange for what he called inadequate caregiver networks. Some of the plans have broadened networks; the dispute continues with others.

In New Hampshire Anthem’s 2014 marketplace plans exclude more than a third of the state’s hospitals. Lawmakers have written legislation that would force insurers to expand choice.

Anthem will “use the excuse, ‘Well, we’re going to save money by having a narrow network,’” said State Rep. Bill Nelson, a Republican who sponsored the bill pendingin the New Hampshire legislature. “Sure that could happen for some people, but other people are going to be losers. Imagine having to change the doctor you’ve had for years.”

South Dakota, Pennsylvania and Mississippi are discussing measures similar to Nelson’s, known as “any-willing-provider” laws that would force insurers to accept more participants in the networks.

Broader choice comes with a price. The ability to sell less-expensive plans with limited choices of doctors and hospitals helps contain medical inflation, health economists argue. Looser networks could. mean higher prices.

“We had narrow networks in the ‘90s. Health-care prices not only moderated, but actually there was one year where they fell,” said Northwestern University professor David Dranove, who specializes in the health care industry. “Then we had the HMO backlash and we had broad networks [again], and health care prices went through the roof.”

In a typical narrow network, offered in many states under the new ACA rules, caregivers agree to lower prices in expectation of more patients. Insurers pass some of the savings to consumers. Done correctly, limited networks can also save money because family doctors, specialists and hospitals who are all part of the same network do a better job of coordinating care, many health policy experts believe.

Excluding certain hospitals from Anthem’s New Hampshire narrow plan would allow premiums to be 25 percent lower than they otherwise would have been, a company spokesman said. Anthem’s narrow Maine plan would save 12 percent, he said.

Insurers are supposed to compete side-by-side in the health law’s subsidized, online exchanges. Under the ACA, they must all now offer certain basic health benefits and they must cover anyone, regardless of pre-existing conditions.

On this new legal terrain, they compete by offering their best combination of price and providers directly to individuals and families who lack other coverage. Adjusting caregiver rosters is one of the few remaining ways insurers can lower costs, limited-network advocates say.

But others argue that these narrow networks can force patients to switch doctors or drive long distances for care if a key hospital is left out of the plan, especially in states such as Maine and New Hampshire with few insurers selling through the ACA marketplace.

“Whenever you have an extremely narrow network there are potential problems for patients with cancer and for patients with any chronic condition, particularly when it requires the patient to go out of network,” said Kirsten Sloan, senior director of policy for the American Cancer Society Cancer Action Network.

Leaving a network to seek specialized care can lead to enormous out-of-pocket bills, she said.

In extreme cases networks could be too small to serve all the plan members they sign up.

“It’s no good making a narrow network that nobody can get in to see,” said Sander Domaszewicz, a senior benefits consultant at Mercer.

Insurers began unveiling ACA marketplace plans with narrow networks in recent months for coverage that starts in January 2014. Policymakers soon challenged them in several states, often pushed by excluded hospitals and their patients.

Maine Insurance Superintendent Eric Cioppa blocked Anthem from switching several thousand existing subscribers to a plan that excluded Central Maine Medical Center and partner doctors and hospitals. Anthem argued that shrinking its network would provide less-expensive but still high-quality care.

This summer Washington Insurance Commissioner Mike Kreidler blocked five insurers from selling through the exchange, in several cases because of network problems. One plan, he said, would have required people to drive nearly 50 miles to see a cardiologist and more than 100 miles to see a gastroenterologist.

Four plans protested Kreidler’s ban. Three reached settlements, some by adjusting networks. An administrative judge ruled in favor of another, Coordinated Care, whose network doesn’t include a children’s hospital.

Seattle Children’s Hospital, left out of networks including Coordinated Care’s, then sued Kreidler, alleging he failed to ensure adequate access to care.

In New Hampshire, Anthem’s decision to leave hospitals out of its network has prompted at least one to threaten litigation, and Nelson to introduce his bill. Anthem’s network could force some patients in his district to drive a dozen of miles or more to get routine care, he said

In few places has the fight over networks been fiercer than in Mississippi. BlueCross Blue Shield of Mississippi cancelled in-network contracts over the summer with Health Management Associates, a for-profit chain with 10 hospitals in the state.

Blue Cross isn’t selling insurance in 2014 through Mississippi’s federally run ACA marketplace, but many expect it to come on board later.

In response HMA took to the airwaves in protest and pitted the insurance commissioner, who wanted only four hospitals reinstated, against the governor, who ordered the insurer to take back all 10.

“I’ve been practicing law for 36 years and I have never seen as aggressive an effort to sway public opinion as these guys engaged in,” said David Kaufman, an outside lawyer for BlueCross BlueShield of Mississippi said of the hospital chain. “You could not go to your mailbox, pick up a newspaper, watch TV, listen to the radio or answer your home phone without hearing that Blue Cross is the devil.”

Blue Cross sued Gov. Phil Bryant, arguing the order was unconstitutional, noting that his daughter works for HMA’s law firm and pointing out that HMA is one of his top campaign contributors. Bryant backed off but ordered Insurance Commissioner Mike Chaney to hold hearings. He refused. Bryant and Cheney, both Republicans, have clashed repeatedly over the federal health law.

Now Mississippi, too, is talking about an any-willing-provider law, which typically requires insurers to take any hospital, clinic or doctor under terms accepted by other participants.

Such a rule would tell Blue Cross that “it can’t kick somebody out of the hospital of their choice,” HMA executive Paul Hurst told WFMN radio’s Paul Gallo on a show broadcast statewide.

But in any state, making every insurer accept every hospital, “is going to throttle competition,” said Dranove, the Northwestern professor who specializes in the health industry. “And this is a healthcare reform that depends entirely on competition. So the people who are fighting for broad networks… are ultimately fighting for the demise of Obamacare.”

Millennium Medical Solutions Inc. will continue to monitor and report on narrow net- work plans and other efforts by insurers to control costs in the PPACA environment.

Health Republic Insurance of New York, a new not-for-profit Consumer Operated and Oriented Plan (CO-OP) offering health insurance coverage in New York State, New jersey and Oregon. In NYS Health Republic Insurance is offering new competitive options for individuals and small businesses both on and off the New York State of Health Benefit Exchange. In partnership with MagnaCare, its network comprises more than 70,000 providers in 32 counties, including New York City, Long Island, the Hudson Valley, the Capital District, parts of North County, Syracuse, and parts of Western New York.

Health Republic Insurance is now offering three health insurance plans on the Exchange: EssentialCare (the New York State mandated “standard plan”), PrimarySelect (an alternative plan where members can access better outpatient benefits when they select a primary care physician), and PrimarySelect EPO (a plan similar to PrimarySelect, but members must choose their primary physician from a menu of primary care medical homes).

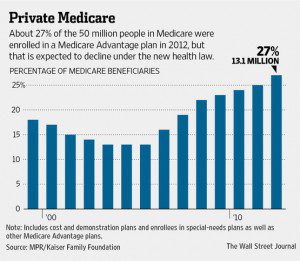

United Healthcare Dropping Medicare Docs. United Healthcare has notified 10-15% of its Medicare Advantage Providers that they will be dropped from their network this February.

Providers are calling the move by the insurer to increase their star rating in order to increase Medicare (CMS) reimbursements. Quality-incentive payments to insurers under CMS’ five-star rating system for health plans will get stricter in 2014, eliminating payments to any plan earning fewer than four stars. Over the past two years, plans with 3 or 3.5 stars received payments.

According to today’s WSJ article UnitedHealth Culls Doctors From Medicare Advantage Plans – The company said it is managing its network, in part, to provide more value for members, particularly given Medicare’s new five-star rating system that ties bonus payments for insurers to certain measures of cost and quality.”That’s what’s driving our actions,” said Austin Pittman, president of UnitedHealth’s networks. He also said, “It’s no secret that we are under substantial funding pressure from the federal government.”

According to a study by the Kaiser family Foundation, United received $540 million in bonus payments in 2012 — the largest share for any single carrier. United had a CMS rating of 3.17 stars that year, according to the study.

This is important as AARP endorses the popular AARP Medicare Advantage Insurance Plans, insured by UnitedHealthcare Insurance Company. According to WSJ article AARP issued a

statement saying it “has heard from a small number of our members regarding this decision” and was encouraging anyone with concerns to contact UnitedHealth directly.

The article points out “Medicare Advantage, an alternative to traditional Medicare, combines hospital and doctor coverage and often includes prescription drugs and perks like gym memberships. Enrollment has more than doubled since 2004 to 13 million in 2012, which represents about 27% of Americans on Medicare.” Also worth noting, “providers have the right to an appeal within 30 days.”

2014 Medicare Open Enrollment is here. Medicare Open Enrollment for 2014 ends Dec 7th. We, at Millennium Medical Solutions Inc, are working closely with affected members to help them find new providers and that patients enrolled in its commercial, Medicaid and Medicare supplement plans are not affected by the changes. Some members may turn back to original Medicare as a result of possibly losing their Doctors.

Download a Copy Of The Medicare and You 2014 Handbook Here.

Is your Doctor still in the network? Is Medicare Advantage still right for you? Please contact us for immediate review at (855) 667-4621. Please visit our https://360peo.com/about-us/blog to view past blogs and Legislative Alerts.

Voluntary Dental,Vision, Life, Accident and Disability

Voluntary Dental,Vision, Life, Accident and Disability