HDHP Minimum Annual Deductible (No change from calendar year 2011):

Single – $1,300 (NONE, $1,300 in 2015)

Family – $2,600 (+$100, $2,500 in 2015)

HDHP Out-of-Pocket Maximum:

Single – $6,550 (+$100, $6,450 in 2015)

Family – $13,100 (+$200, $12,900 in 2015)

Age 55 Catch Up Contribution

As in 401k and IRA contributions, you are allowed to contribute extra if you are above a certain age. If you are age 55 or older by the end of year, you can contribute additional $1,000 to your HSA. If you are married, and both of you are age 55, each of you can contribute additional $1,000.

HSA/HDHP Market Growth

HSA holders own the assets in the accounts and can build up substantial sums over time. Enrollment in HSA-compatible insurance plans has increased to 10 million earlier this year, from 1 million in March 2005, according to, America’s Health Insurance Plans (AHIP), a trade group.

HSAs were authorized starting in January 2004. Since then, AHIP has conducted a periodic census of health plans participating in the HSA/HDHP market.

The number of people with HSA/HDHP coverage rose to more than 11.4 in January 2011, up from 10.0 million in January 2010, 8.0 million in January 2009, and 6.1 million in January 2008.

30 percent of individuals covered by an HSA plan were in the small group market, 50 percent were in the large-group market, and the remaining 20 percent were in the individual market.

14% of all workers in the private sector that have access to a Health Savings Account acc. to Bureau of Labor Statistics.

States with the highest levels of HSA/HDHP enrollment were California, Ohio, Florida, Texas, Illinois and Minnesota.

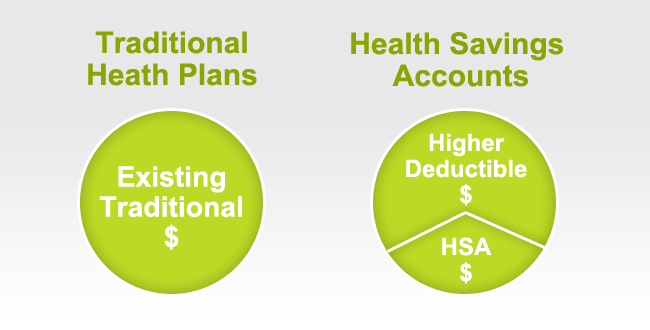

HSA Advantages:

Opportunity to build savings – Unused money stays in your account from year to year and earns tax-free interest. The HSA also gives you an investment opportunity.

Tax-free contributions and earnings – You don’t pay taxes on contributions or earnings.

Tax Free Money allowed for non traditional Medical coverage– As per IRS Publication 502, unused moneys can be used for dental,vision, lasik eye surgery, acupuncture, yoga, infertility etc. Popular Examples

Portability – The funds belong to you, so you keep the funds if you change jobs or retire.

Our overall experience with HSAs have been positive when employer funding is at minimum 50% using either the HSA or an HRA (Health Reimbursement Account-employer keeps unspent money). Traditional plans trend of higher copays and new in network deductibles has also led to the popularity of an HSA.

(Note that a health plan will not fail to qualify as a high deductible health plan merely because it provides certain preventive health services without a deductible, as required under Health Care Reform.)

Is your HSA compliant? Which pre-tax qualified HSA, FSA, HRA spending card is right for you? Please contact our team at Millennium Medical Solutions Corp (855)667-4621 for immediate answers.. Stay tuned for updates as more information gets released. Sign up for latest news updates.

Anyone who has moved has been confronted with the question “How to Order Your Medical Records?”. Requesting your medical records may seem complex at first its simpler than one thinks.

1. Get a HIPAA release form. The federal law known as HIPAA entitles every person the right to access his or her medical records, receive copies of them, and request amendments to them.

2, Select your records. I would make this at least one month no more than 2 months This will give the office plenty of time to get you the records together. Specify the effective date, medical providers name, address, your name, address, medical record number ( you can get this from the staff) any identification numbers; i.e., Social Security Number or insurance ID number.

3. Submit forms. Fill out an authorization form giving one medical provider permission to share your records with another.Mark on that form which types of records you want included. Pay any fees that result.

4. Wait. The turnaround time under HIPAA can be 30 days. Most facilities, however, do not require that much time—many can fulfill a request in five to 10 days. Individual state laws may also dictate how quickly a facility must fulfill a request.

5. Follow up. In an imperfect world things can go wrong. What to do?

If your doctor has moved, you should be able to find your records at the practice she left. If that practice was affiliated with a hospital, the records may be housed within the hospital’s records system.

If your old provider says the records have been sent, but your new doctor’s office hasn’t received them, ask that they be re-sent. Doublecheck to make sure the old provider has the right contact information for your new one. You may find getting someone from your new doctor’s office involved could help. Having a nurse advocate for you, for instance, could put you in a better position.

If you’ve tried everything and are getting nowhere, offer to pick up the records yourself (but be aware that this may cost you), ask to speak with a manager or your doctor directly, or, as a final resort, contact your state medical board to file a complaint. This step is rarely necessary, but even suggesting you’ll have to go this route could get things moving on your request.

The Value of Requesting Your Records

There are many good reasons to request a copy of your medical records. Physicians don’t always share complete patient information or exchange a patient’s health records, so if a patient is seeing a new provider it is beneficial to ensure a copy of their record is sent to the new physician.. Also, it is beneficial for patients or caregivers dealing with multiple doctors and facilities to have all medical records in one place, which can then be used by providers to ensure thorough care.

Reviewing your record is an important way to ensure your provider has complete, correct, and up-to-date information, such as your known allergies. If you find information in your record that is incorrect or that you disagree with, contact the provider’s Health Info Management department.

Finally, it can be good for your health to keep a copy of your medical records, . Keeping an up-to-date copy of your health information will prevent redundant care, like repeat tests, and give all your physicians essential information about your health.

HDHP Minimum Annual Deductible (No change from calendar year 2011):

Single – $1,300 (up from $1,250 in 2014)

Family – $2,600 (up from $2,500 in 2014)

HDHP Out-of-Pocket Maximum:

Single – $6,450 (up from $6,350 in 2014)

Family – $12,900 (up from $12,900 in 2014)

HSA/HDHP Market Growth

HSA holders own the assets in the accounts and can build up substantial sums over time. Enrollment in HSA-compatible insurance plans has increased to 10 million earlier this year, from 1 million in March 2005, according to, America’s Health Insurance Plans (AHIP), a trade group.

HSAs were authorized starting in January 2004. Since then, AHIP has conducted a periodic census of health plans participating in the HSA/HDHP market.

The number of people with HSA/HDHP coverage rose to more than 11.4 in January 2011, up from 10.0 million in January 2010, 8.0 million in January 2009, and 6.1 million in January 2008.

30 percent of individuals covered by an HSA plan were in the small group market, 50 percent were in the large-group market, and the remaining 20 percent were in the individual market.

14% of all workers in the private sector that have access to a Health Savings Account acc. to Bureau of Labor Statistics.

States with the highest levels of HSA/HDHP enrollment were California, Ohio, Florida, Texas, Illinois and Minnesota.

HSA Advantages:

Opportunity to build savings – Unused money stays in your account from year to year and earns tax-free interest. The HSA also gives you an investment opportunity.

Tax-free contributions and earnings – You don’t pay taxes on contributions or earnings.

Tax Free Money allowed for non traditional Medical coverage– As per IRS Publication 502, unused moneys can be used for dental,vision, lasik eye surgery, acupuncture, yoga, infertility etc. Popular Examples

Portability – The funds belong to you, so you keep the funds if you change jobs or retire.

Our overall experience with HSAs have been positive when employer funding is at minimum 50% using either the HSA or an HRA (Health Reimbursement Account-employer keeps unspent money). Traditional plans trend of higher copays and new in network deductibles has also led to the popularity of an HSA.

Is your HSA compliant? Which pre-tax qualified HSA, FSA, HRA spending card is right is right for you? Please contact our team at Millennium Medical Solutions Corp (855)667-4621 for immediate answers.. Stay tuned for updates as more information gets released. Sign up for latest news updates.

(Note that a health plan will not fail to qualify as a high deductible health plan merely because it provides certain preventive health services without a deductible, as required under Health Care Reform.)

New Proposed Rules for Wellness ProgramsIn another step forward to ncentivize wellness new proposal can give discounts for managing good health much like good drivers with auto insurance.Newproposed rules issued under Health Care Reform address certain amendments to the nondiscrimination requirements for group health plans offering a wellness program to comply with the federal Health Insurance Portability and Accountability Act(HIPAA).Specifically, the proposed rules would increase the maximum permissible reward under a wellness program that requires an individual to satisfy a standard based on a health factor in order to obtain a reward, from 20% to 30% of the cost of coverage (and to 50% for programs designed to prevent or reduce tobacco use). The rules also include other proposed clarifications regarding the requirements for such wellness programs to avoid prohibited discrimination, including reasonable design and reasonable alternatives that must be offered for individuals to obtain the reward.Other Proposed Rules Released Under Health Care Reform Separately, new proposed rules have been issued for health insurance companies regarding the law’s requirements related to guaranteed availability of coverage and essential health benefits.

Under one set of proposed rules, issuers offering non-grandfathered health insurance coverage in the individual or group market would be required to accept every individual and employer that applies for coverage, with limited exceptions. Issuers in the individual and small group markets would be allowed to vary premiums within limits, only based on age, tobacco use, family size, and geography.

Another set of proposed rules outline issuer standards related to coverage of “essential health benefits.” Essential health benefits are a core set of items and services that must be covered by non-grandfathered plans in the individual and small group markets beginning in 2014.

While its always been known a healthy livingfor employees makes a productive employee. Large businesses have benefited from a healthy work force as they can better afford programs and have a direct rate reduction in rates.

Although employers continue to use cost shifting to control health insurance expenses, many companies are also making wellness programs part of the overall strategy to keep costs down by keeping staff members healthy.“Our entire health care system is organized around treating diseases after they occur, not preventing them before they occur. We need a paradigm shift that places prevention at the center of our health priorities.” – Lynn C. Swann, Chairman, President’s Council on Physical Fitness and Sports

The new proposed rules would apply for plan years beginning on or after January 1, 2014. An overview of the proposed rules is available on Healthcare.gov. Our Summary by Year offers updates on other requirements related to Health Care Reform.

First, and most importantly, we hope that you and your families are safe and sound.

An office status for Health Insurance Carrier post Hurricane Sandy for your information. Millennium medical Solutions Corp is up and running and the offices are open until 2:00 PM today, Friday November 2nd.

Our building has power but we are having on and off phone/internet trouble but some calls are able to come through so you can call if you have any issues.

Carrier Update

• EmblemHealth still closed • Horizon still closed • AmeriHealth still had no power as of yesterday • Oxford Update – see below

A few changes to business as usual in response to the storm:

1. The deadline for payment of October premiums has been extended. We’ve extended the deposit date for payments to November 9th. Customers should make their payments online, however, as we cannot guarantee that our overnight mailing facilities will be open and available to accept mail.

https://www.payerexpress.com/billmail/EBPP/Sites/Oxford/ 2. The deadline for November renewals has been extended from the 1st to the 6th. This includes renewals run through our IDEA portal. As we get any additionalupdates, we will reach out to you.