Essential Health Benefits Not Delayed

Essential Health Benefits

Essential Health Benefits Not Delayed

The pre-July 4th news of Obamacare Employer Mandate Delayed until 2015 decision may have started early fireworks. The administration did not, however, delay the larger new requirements facing employers who choose to offer health insurance in the small group market––employers with less than 50 workers. The biggest requirement – Essential Health Benefits not delayed.

Whether the rationale was to alleviate business pressure to meet new mandates by Jan 2014 or the real fear that Employers have already begun making necessary employment hours cut backs to avoid the $2,000 penalty. A $3,000/employee penalty was also looming for Employers offering unaffordable insurance.

Keep in mind that this limited delay does not affect other provisions of the Affordable Care Act slated to go into effect in or before 2014, such as:

- Individual mandate which requires most individuals to purchase insurance by January 1, 2014, or pay a tax penalty.

- a 90-day maximum on eligibility waiting periods;

- monetary caps on annual out-of-pocket maximums;

- total elimination of lifetime and annual limits (including expiration of waivers that permitted certain “mini-med” plans and stand-alone Health Reimbursement Arrangements to stay in place through plan years beginning in 2013);

- new wellness plan rules;

- revised Summary of Benefits and Coverage templates;

- Patient Centered Outcomes Research Institute (PCORI) excise taxes and transitional reinsurance program fees; HRA/HSA/FSA clients also pay a monthly $1/employee tax.

- a notice informing employees of the availability of the new health insurance Exchanges (a model notice is available on the U. S. Department of Labor website); and insurance market reforms.

See NYS specific Essential Health Benefits chart.

The biggest impact is the Essential Health Benefits (EHB) which will not be delayed and this affects fully insured or ALL Small Businesses. While small employers are not required to offer coverage, if they do then they come under that large number of new essential health benefit mandates and group rating rules that won’t apply to large employers. These small group requirements are expected to increase the cost of small group coverage by an average of 15%––with wide variation by state and the average age of the group.

An employer sponsoring a Healthy NY or Brooklyn Healthworks Plan today for example would be disqualified as this does not carry all Essential Health Benefits. The very popular Healthy NY is slated to shut down for Jan 2014 and most Employers have just received this transition letter last week. Individual and Sole Prop Healthy NY is terminating and small business Healthy NY must be reapplied under a new higher cost version. While the plan did not carry Ambulance and had a $3,000 limited Pharmacy plan it is priced 35% below market and did manage to capture hundreds of thousands that would otherwise had been uninsured. The same is true for those on Hospital Only or high deductible catastrophic plans.

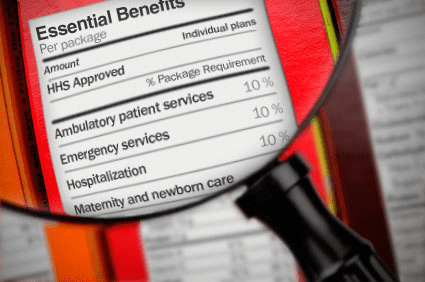

So what are these Essential Health Benefits?

All individual and small group policies on and off-Exchange must cover ten categories of minimum essential health benefits.

— Ambulatory services

— Emergency services

— Hospitalization

— Maternity and newborn care

— Mental health & substance abuse services

— Prescription drugs

— Rehabilitative and habilitative

— Laboratory services

— Preventive/wellness services, disease management

— Pediatric oral and vision car

Under the ACA, each state must choose one plan from among popular health insurance plans offered statewide to serve as a benchmark for EHBs. The benchmark plan will act as the model for how plans must define and include EHBs in their coverage — in both the individual and small group markets. New York selected the benefits of the State’s largest small group plan as its EHB benchmark. There is also a Minimum Value requirement, See NYS Minimum Value STANDARD BENEFIT DESIGN COST SHARING DESCRIPTION CHART (5-6-2013) Some of the plan’s components include:

- No cost-sharing for routine preventive services

- Pediatric dental and vision coverage

- Habilitative and rehabilitative services, including physical therapy, speech therapy and occupational therapy

- Rich mental/behavioral health services

- No annual or lifetime dollar limits on benefits

Conversely, a shift to self- insurance is underway as self-insureds can avoid many taxes and instead ONLY cover the Minimum Essential Coverage which is different than the Essential Health Benefits. The strategy coupled with reinsurance is a great sophisticated model usually reserved for larger groups. This segment will be able to avoid local additional State mandates which in States like NY account for 14-16%% of the costs. Thats a total swing of 30% for a fully insured NY group. Also, self-insured groups do NOT pay added taxes such as the health insurance tax of $9 Billion annually over the next 10 years.

The administration has shown their sensitivity to larger groups. This segment already covers 94% of its employees at least in some fashion while small businesses cover less than 50%.

Why not do the same for small employers as well? And while they are at it, use the time to reconsider the impact many of these regulations are likely to have on the number of small employers continuing to offer coverage.

For a downloadable guide on self-insuring and secondary market reinsurance for your group please send contact form below. In the meantime, please visit to view past blogs and Legislative Alerts at https://360peo.com/feed.