Business Auto Insurance Whether you have two vehicles or a fleet of 200 trucks, our Business Auto Insurance policies are custom designed to meet the needs of your business and to insure your vehicles in transit and parked. Coverages and Insurance Solutions...

Commercial Insurance We create cost-effective and comprehensive insurance solutions that meet the specific needs of your industry and business. For the business around the corner, and the company around the world, we build cost-effective insurance solutions that...

Accidents happen without any notice. Life insurance helps those you leave behind pay bills, education cost, and funeral expenses among other things. Nothing can replace you in their hearts, but life insurance can make things easier for them when your gone.

This is an essential part of financial planning. One reason most people buy life insurance is to replace income that would be lost with the death of a wage earner. The cash provided can also can help ensure that your dependents are not burdened with significant debt when you die. The insurance proceeds could mean your dependents will not have to sell assets to pay outstanding bills or taxes. An important feature is that generally no income tax is payable on proceeds paid to beneficiaries. The death benefit of a life policy owned by a C corporation may be included in the calculation of the alternative minimum tax.

How much Insurance do I need?

Before buying life insurance, you should assemble personal financial information and review your family’s needs. There are a number of factors to consider when determining how much protection you should have. These include:

any immediate needs at the time of death, such as final illness expenses, burial costs and estate taxes;

funds for a readjustment period, to finance a move or to provide time for family members to find a job

ongoing financial needs, such as monthly bills and expenses, day-care costs, college tuition or retirement.

Although there is no substitute for a careful evaluation of the amount of coverage needed to meet your needs, one rule of thumb used is to buy life insurance that is equal to five to seven times annual gross income.

Sign up for latest news updates. Please contact us for immediate information on how to implement these initiatives for your group-specific needs at info@medicalsolutionscorp.com or Call (855) 667-4621.

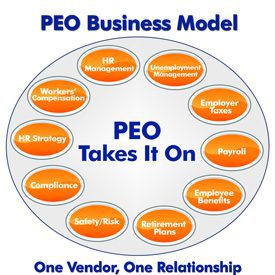

Having management done effectively can be a difficult task in the competitive business world. Professional Employer Organizations, or PEOs, help companies of clients. They do so by developing strategies in outsourcing the management of certain business factors such as payroll, workers’ compensation, employee benefits, and human resources. In fact, PEOs keep the clients’ focus in mind to optimize the competitive edge of the business as the client company can now focus on more lucrative endeavors.

When it comes to managing complex related matters, businesses need as much help as possible. It may be tedious to allow other fields to progress as businesses may need to keep records consistent and error-free for matters such as health benefits, payroll, workers’ compensation claims, unemployment insurance claims, and payroll tax compliance. With the bulk work needed for the employees to be fully satisfied, a company may sacrifice productivity for compensation. A PEO prevents this from happening and opens up the gateway to other possible management systems. A business will then benefit from the advantage of rerouting their focus on more profitable means in their business.

The PEO Advantage

You need the benefits a Professional Employer Organization (PEO) can bring to your business to make it soar. We independently work with 50+ leading PEOs in the marketplace. Our PEO Partnerships will act as more than just an addition to your Human Resources department they provide a Client Relations Partners and SHRM certified Human Capital Consultants that provides expert guidance on a host of topics relating to human resources and employee concerns. With our Client Relation Partners, you are assured of a prompt and knowledgeable response to all your human resource questions.

Business owners who use PEO services also have full and free access to additional services such as employment verification and background screening, drug testing, recruiting, professional development and continuing education instruction and seminars. With a PEO at your side, you are able to attract and keep the absolute best employees to further the growth of your business.

So what do they DO?

There are several “core” features that are offered by nearly every PEO company. They are:

HR Outsourcing – Human Resources tasks are often very detailed and technical, and it can be easy to make a mistake or miss a crucial step when filing paperwork. For a business owner, HR duties can become very time-consuming, tedious, and stressful. PEOs act as a dedicated human resources department for their clients, and will monitor employment regulations and reporting requirements. In addition, hiring, firing and interviewing assistance can typically be given by the professional employer organization. They can also provide access to HR experts that will give you advice on compliance and recruiting, and even put together employee handbooks and employment procedure manuals.

While there may be differences in the offerings and organization of different employee leasing companies, it is important to note that while the HR tasks are managed by an outside service, the business owner is still responsible for day to day management of their employees.

Payroll – PEOs process payroll, deliver checks, perform direct deposits and file payroll taxes. They ensure your workers are categorized correctly, and that you are compliant with the most up to date government rules and regulations. This service is especially useful for companies with employees in multiple states. They ensure that payroll is filed properly for each state, saving business owners time and money.

Benefit Outsourcing -To maintain a competitive edge and retain key employees, small businesses must compete with large companies that can offer extensive employee benefit programs. PEOs provide access to a broad range of medical, dental, retirement and other insurance offerings thus allowing their clients to offer a competitive, well organized package to attract talent, boost employee morale and retain their best employees. A PEO will also help insure compliance with government regulations related to benefits such as COBRA and the PPACA.

Additional Services

Though these core services are very important, there are still many other benefits to co-employment. Not all PEOs offer these same additional services, and these differences often determine which PEO is the best fit for your company. Some of these additional services are:

Worker’s Comp -This benefit is so popular that many PEOs are now offering worker’s comp as a core service. It’s worth noting that if a business is satisfied with its existing coverage, it is usually possible to find a PEO that will allow the company to keep its individual policy. However, companies can benefit from obtaining worker’s comp insurance through a PEO. PEO services are usually subject to lower rates, and these savings can offset the PEO’s cost of services. Typically, a PEO will also review and process worker’s compensation claims, saving small businesses a great deal of time.

Safety – Because the PEO’s service may be responsible for worker’s compensation, they may also provide risk and safety consultants. These consultants will review facilities, give advice, and even develop safety programs tailored exclusively to their client’s needs.

Recruiting – In addition to traditional HR services, some PEOs provide access to a recruiter or a job posting service. They may also screen applicant resumes or perform initial interviews. This helps save business owners time, and ensures that final interviews are conducted only with serious, qualified candidates. However, not all PEOs are involved in the hiring process, and employers do not have to use this service if they would rather recruit on their own.

Training Services – If offered, training may be local or web based, and is often provided at a discounted fee. Training areas can range from employee development and computer skills to sexual harassment and ethics programs.

Performance Management– Outsourced human resources departments provide guidance concerning performance reviews and methods of identifying and retaining key employees. This service helps a business owner understand which employees are doing the most for their company, and how to reward their efforts. Additional services available may include on-boarding programs, evaluation & performance tracking, goal development, compensation management, market salary data, workforce planning, and even writing tools for performance reviews.

Outplacement Services – This service helps to limit risk when performing a reduction in the workplace. With this service, downsized employees will have some assistance while searching for a new employer.

Background screening – Some PEOs offer background screening to assist in the hiring process. With sufficient background screening, employers can avoid hiring high-risk individuals who may cause concern for a small business. This service is usually discounted due to volume-based pricing.

Drug Screening – As in background screening, this step insures employers do not hire high-risk individuals. Again, this service may be discounted due to volume-based pricing.

But What Does it Cost?

Most PEOs charge a flat fee per employee per year based on a percentage of payroll. This percentage will vary depending on the number of services utilized by their client. For example, a contract to manage employee recruitment, the payroll process, medical insurance administration and employee retirement planning will pay a larger fee than one who only contracts to oversee payroll.

PEOs can also offer bundling packages to reduce overall cost – for example, Human Resources, background checks, and drug screening may be offered together for a reduced rate. Of course, businesses should take care not to pay for services they will not use, as this will increase the price of co-employment.

More Stats, Please

The nation’s largest trade association for PEOs is the TheNational Association of Professional Employer Organizations (NAPEO). With well over 400 PEO members, NAPEO operates in all 50 states. Member companies range in size from brand new companies to large, publicly held organizations with many years of experience. NAPEO describes itself as The Source for PEO Education®, bringing its members with the very best educational options and business resources, including conferences, seminars, magazines, online services, marketing resources, public relations support and more. The Voice of the PEO Industry®, NAPEO also protects the interests of its PEO members by proactive lobbying efforts and ongoing, timely communications on legislative/regulatory issues of interest. For more information on growth in the PEO industry, you may review some of NAPEO’s statistics here, www.NAPEO.org.

Is a PEO Right For My Group?

If you’re a small business owner who has concerns about payroll, filing paperwork, and complying with government regulations, co-employment may be the service you’ve been looking for. You may already have a PEO but confused as to unbundling the administration fees form the benefits component you are actually paying. In some cases, a PEO may NOT be right for you. With Health Care Reform your company may qualify for a small business tax credit or a large percent of employees may qualify for an income tax credit on the individual exchange.

For more detailed specifics and a quick comparison shop please email us at info@medicalsolutionscorp.com or cal 855-667-4621

Breaking News: NSLIJ, and Brooklyn’s Maimonides Announce Strategic Partnership on Wednesday. Both side shave been in talks since February.

Eventually North Shore-LIJ and Maimonides will fully integrate, “in a phased approach that will begin immediately,” the two jointly announced Wednesday. In the meantime, both institutions maintain their independence and separate governance structures. Lynam said there was no specific time frame for full integration.

Maimonides gets much-needed cash — tens of millions of dollars — for capital and operational investments. That will help it compete with Presbyterian-backed Methodist and Langone-backed Lutheran. North Shore-LIJ gets its first real foothold in #Brooklyn, one of the most competitive health care markets in the nation. But it does so without the commitment that a full-scale merger would entail. An affiliation agreement also protects North Shore-LIJ from unknown liabilities related to the Federation of Jewish Philanthropies, a malpractice insurer that covers Maimonides and several other hospitals

North Shore-LIJ has made strategic partnerships and acquisitions before. For North Shore-LIJ, the relationship means it has a hospital or hospitals in every borough as well as blanketing Westchester and Long Island. North Shore-LIJ, the country’s 14th largest health care system, owns 19 hospitals. In the city that includes Lenox Hill Hospital in Manhattan, Staten Island University Hospital, and, in Queens, Forest Hills Hospital, Long Island Jewish Medical Center, Cohen Children’s Medical Center and Zucker Hillside Hospital, a behavioral health center.

They are also actively insuring members today in the Downstate NY area under the CareConnect NSLIJ holding company. With important advantages under ACA and mindful of delivering value the insurance arm is priced affordably. In fact they had lowered their rates 15-20% for 2015 and and industry low 3.3% for 2016.

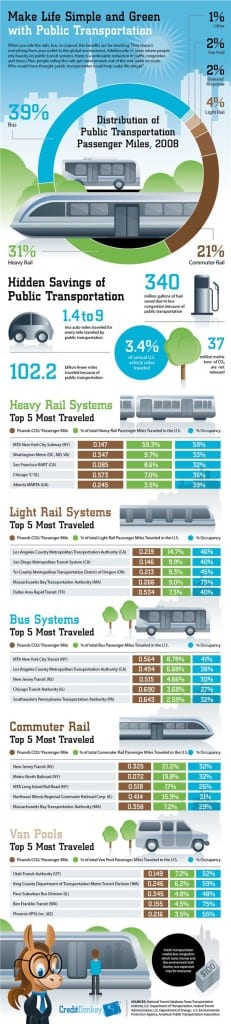

A fun visual transit infographic highlighting the benefits of public transportation by Credit Donkey. With NYC Transit Benefit Mandate for 2016 Employers with 20 or more full-time employees in New York City must sponsor for full-time employees a pre-tax qualified transportation benefit program (excluding parking subsidies). It would mean that an estimated 450,000 more New York City-based employees will have access to the commuter tax break. That’s in addition to the 700,000 who already get the break.

Despite the requirement this visual highlights the inherent win-win of riding public transit. Furthermore, Employers exempt form the mandate such as smaller Employer or outside NYC ought to consider this as a benefit per at work. IMPORTANT: The popularity of the benefit for Employers have been a budget neutral perk that is offset by payroll tax savings. After all, the Employer is not required to fund the Transit/Parking only sponsor the plan.

Tax Savings:

The way the pretax commuter tax break works is employees exclude their transit commuting costs from their taxable wages up to the $130 monthly limit (there’s a separate $250 monthly limit for parking). If you’re in the 40% combined federal and state bracket and you put away $130 a month pretax salary to use for transit, you save $624 a year. This also saves the employer money because the employer doesn’t pay payroll taxes of 7.65% on every dollar set aside by employees pre-tax.

$130 transit maximum

EE Savings @ 40% tax bracket = $624/year

ER Savings (FICA) = $119/year

$250 parking maximum

EE Savings @ 40% tax bracket = $1,200/year

ER Savings (FICA) = $230/year

Next Step:

If you want your employer to add commuter benefits—so you’re eligible for the tax break–petition your HR department, and specifically ask for the pretax commuter benefits program (why wait until 2016?). To learn more about the NYC Transit Mandate, please visit the official website of the City of New York.

To start a Transit benefit within 24 hours contact us today (855) 667-4621 or info@medicalsolutionscorp.com. Ask us about our enterprise payroll.

NYC become the 3rd U.S. City to require Employer Transit Benefits following SF and Washington, DC. Beginning in 2016, the ordinance will require employers (not including government employers) with 20 or more full-time employees in New York City to provide full-time employees a pre-tax qualified transportation benefit program (excluding parking subsidies). It would mean that an estimated 450,000 more New York City-based employees will have access to the commuter tax break. That’s in addition to the 700,000 who already get the break.

“The ordinance will require private employers with 20 or more full-time employees in New York City to provide a pretax qualified transportation benefit program for their full-time employees.” For purposes of the ordinance, a full-time employee is one who works 30 or more hours per week.

Penalties:

While the new ordinance goes into effect January 1, 2016, it provides a six-month grace period, so penalties will not begin until July 1, 2016. Penalties for a first violation will range from $100 to $250. If an employer corrects the violation within 90 days of being notified, then penalties will be waived. If correction (the steps for which have not yet been described) does not occur, penalties for the first violation will apply and an additional penalty will apply, equal to $250 for each 30-day period in which the employer continues to fail to offer the required benefits.

Tax Savings:

The way the pretax commuter tax break works is employees exclude their transit commuting costs from their taxable wages up to the $130 monthly limit (there’s a separate $250 monthly limit for parking). If you’re in the 40% combined federal and state bracket and you put away $130 a month pretax salary to use for transit, you save $624 a year. This also saves the employer money because the employer doesn’t pay payroll taxes of 7.65% on every dollar set aside by employees pre-tax.

$130 transit maximum NEW $255 transit maximum for 2016

EE Savings @ 40% tax bracket = $1200/year

ER Savings (FICA) = $230/year

$255 parking maximum

EE Savings @ 40% tax bracket = $1,200/year

ER Savings (FICA) = $230/year

Next Step:

If you want your employer to add commuter benefits—so you’re eligible for the tax break–petition your HR department, and specifically ask for the pretax commuter benefits program (why wait until 2016?). To learn more about the NYC Transit Mandate, please visit the official website of the City of New York. To start a Transit benefit within 24 hours contact us today (855) 667-4621 or info@medicalsolutionscorp.com.

Q & A about Life and Disability Insurance for Business Owners and Corporate Executives Informative Answers to Commonly Asked Questions

How can a business owner identify key personnel to insure? Without these employees, the company would lose significant revenue income. Which employee(s) should a company consider purchasing a policy for? This depends on the nature of the business. Usually “C” suite management. Additionally, there may be other management team members that are considered vital to the organization. What types of policies should be In-Force? Both life & disability policies. How much life and/or disability insurance should business owners, themselves, have to maintain proper coverage but avoid overspending on what is necessary? It is often said, “insurance always costs too much to buy, though it is never enough when needed.” As this can be a unique amount proportional to each business owner, a professional and experienced business financial advisor should be consulted. What factors should business owners take into account when determining coverage needs? There are mainly two ways to earn money in our society: people at work or money at work (interest being earned). If a person is lost to death or limited by a disability, having the right amount of insurance to compensate for lost income is crucial. Is there truth in having “too much insurance”? Could a business owner really “exceed their need”? There is no such thing as “extra” money. Proceeds from different insurance policies can be utilized for multiple reasons. When should (if ever) a business owner consider a Section 162 plan? A Section 162 plan, also know as a “bonus plan”, works for tax arbitrage when there is a difference between the personal tax rate and corporate tax rate of the business owner. It also depends on the business entity type as to whether it is applicable. It is the same for key employees. There is usually a way to accomplish, on a tax-favored basis, the financial and insurance goals of a business owner. How might an insurance policy factor into a business owner’s exit strategy? There are three possible exit strategies:

Selling the business

Retiring or quitting

Death or disability forced exits

Clearly, having the proper insurances in place should death or disability ever occur, is most vital. A retire/quit exit scenario could be funded with a cash value policy in place, where significant assets have been accumulating. Selling the business may be an opportunity to insure the life of the seller. Here, the new business owner may use this policy as a key person policy. In doing so, the new business owner may keep the business seller on file as a consultant for a period of time, until the business transitions over completely to the new owner.

Please contact us for an immediate disability insurance quote & information at info@medicalsolutionscorp.com or Call (855) 667-4621.

Great news for families with HSA and high deductible plans. Individual out of pocket maximums will apply EVEN UNDER A FAMILY POLICY. New federal health care reform law regulatory guidance ends lingering uncertainty on how much in out-of-pocket costs employers with high-deductible plans can require employees to pick up.

The guidance, leaves intact the maximum out-of-pocket expenses employers can require employees to pay before health plan coverage kicks in: $6,850 for single coverage and $13,700 for family coverage when the rules go into effect in 2016.

An example illustrates how the HHS-imposed “EMBEDDED” limit on out-of-pocket expenses will work:

An employee and his or her spouse enroll in family coverage with an annual cost sharing limit of $13,000, and during the 2016 plan year, $10,000 of cost sharing payments are attributable to the spouse and $3,000 of cost sharing payments are attributable to the employee. Prior to the HHS’s clarification, the full $13,000 would be payable by the covered individuals because the $13,000 plan limit had not been reached on an aggregate basis. However, with the new EMBEDDED self-only limitation, the cost sharing payments attributable to the spouse must be capped at the self-only limit of $6,850, with the remaining $3,150 being covered 100% by the group health plan. The employee would still be subject to cost sharing, however, until the $13,000 plan limit is reached.

The biggest impact on the new cost-sharing rules will be on employers with high-deductible plans.

For the FAQs, visit: http://www.dol.gov/ebsa/pdf/faq-aca27.pdf

For more information and a free renewal evaluation please

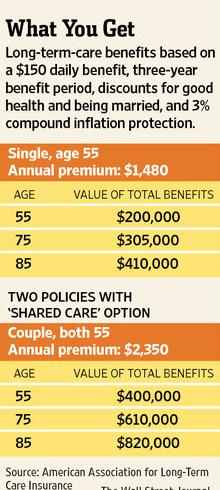

Enhance Your Group Benefits Plan with LTC Insurance

Long-term care (LTC) insurance is an option employers can include with their group health plan to provide additional benefits for their employees, which helps both employers and their workforce.

What Does LTC Insurance Cover?

Long-term care (LTC) insurance is different from traditional health insurance in that it covers long-term services and support. This coverage provides policy holders with a reimbursement for services that assist with daily living activities, such as eating, dressing, bathing, moving around, and/or getting in and out of bed. Most LTC policies that are available today are comprehensive and pay for long-term care in various settings, including:

Adult day service centers

Alzheimer’s care facilities

Assisted living facilities (also known as residential care facilities or alternate care facilities)

Nursing homes

Hospice care

Respite care

If policy holders choose to have long-term care provided in their home, comprehensive policies generally cover the following services:

Assistance with personal care, such as bathing and dressing

Who Needs LTC Insurance?

Contrary to popular belief, LTC insurance isn’t just for the elderly. It provides coverage that traditional medical plans do not provide for long-term care needs arising from accident, illness, and aging. The need for long-term care obviously increases with age, but an accident or illness can occur at any time, so all individuals can benefit from having LTC insurance.

How is the Premium Calculated?

The cost of LTC insurance depends on several factors, including:

Whether the policy is purchased on an individual basis or as part of a group plan offered by an employer

The care options and benefits that are included in the policy

The age of the policy holder when they purchase the policy

The maximum amount the policy will pay per day

The maximum number of days or years the policy will

pay benefits

Group Benefit Plans and LTC Insurance

Individuals can purchase LTC insurance on their own or, if available, through the group benefits plan at their workplace. Both the employee and the employer will realize several benefits of having LTC insurance part of the group benefits plan.

Benefits for Employees

When employees purchase LTC insurance through their group health plan, they will be able to take advantage of pricing discounts and simplified underwriting only available on a group basis. In addition, a LTC policy does the following:

Enables employees to safeguard their retirement savings.

If the need arises for long-term care, they can pay for this care through the LTC insurance rather than with their retirement savings.

Gives employees the ability to control their long-term health care decisions rather than relying on family or government for financial support.

Provides peace of mind by providing coverage for needs that are not covered by other medical benefits.

Benefits for Employers

When employers offer LTC insurance for their employees, they can choose to pay all, part, or none of the premium for employees who opt in for the coverage. Regardless of which option employers choose, they and their employees will still enjoy benefits of making this type of insurance available.

Discounts on the policy premium. Even if employers choose to simply offer the coverage as a voluntary benefit where the employee pays 100 percent of the premium, the policy will be available at a group-discounted rate.

Health underwriting concessions. Generally insurers require individuals to meet certain health standards to qualify for long-term care insurance, but when the policy is offered on a group basis the medical qualifications are often simplified.

Improve recruitment and retention of key employee talent with enhanced benefit packages that include LTC insurance.

Improve employee productivity. When an employee is dealing with a long-term care situation, either for themselves or a dependent, it can be time consuming and stressful. This can cut into employee productivity. Having access to long-term care solutions can help eliminate this problem.

the pretax commuter tax break works is employees exclude their transit commuting costs from their taxable wages up to the $130 monthly limit (there’s a separate $250 monthly limit for parking). If you’re in the 40% combined federal and state bracket and you put away $130 a month pretax salary to use for transit, you save $624 a year. This also saves the employer money because the employer doesn’t pay payroll taxes of 7.65% on every dollar set aside by employees pre-tax.

the pretax commuter tax break works is employees exclude their transit commuting costs from their taxable wages up to the $130 monthly limit (there’s a separate $250 monthly limit for parking). If you’re in the 40% combined federal and state bracket and you put away $130 a month pretax salary to use for transit, you save $624 a year. This also saves the employer money because the employer doesn’t pay payroll taxes of 7.65% on every dollar set aside by employees pre-tax.

Contrary to popular belief, LTC insurance isn’t just for the elderly. It provides coverage that traditional medical plans do not provide for long-term care needs arising from accident, illness, and aging. The need for long-term care obviously increases with age, but an accident or illness can occur at any time, so all individuals can benefit from having LTC insurance.

Contrary to popular belief, LTC insurance isn’t just for the elderly. It provides coverage that traditional medical plans do not provide for long-term care needs arising from accident, illness, and aging. The need for long-term care obviously increases with age, but an accident or illness can occur at any time, so all individuals can benefit from having LTC insurance.