HSA 2013 Limits

The IRS has released the 2013 Health Savings Account (HSA) inflation adjustments.

In 2013 HSA limits are as follows:

HSA Annual Contribution Limit:

Single – $3,250 (up from $3,100 in 2012)

Family – $6,450 (up from $6,250 in 2012)

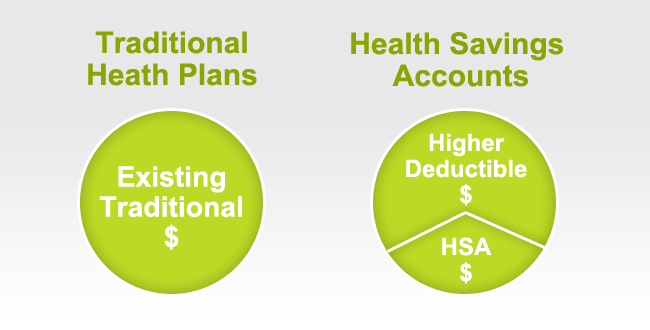

HDHP Minimum Annual Deductible (No change from calendar year 2011):

Single – $1250 (up from $1,200 in 2012)

Family – $2500 (up from $2,400 in 2012)

HDHP Out-of-Pocket Maximum:

Single – $6250 (up from $6,050 in 2012)

Family – $12,500 (up from $12,100 in 2012)

HSA/HDHP Market Growth

HSA holders own the assets in the accounts and can build up substantial sums over time. Enrollment in HSA-compatible insurance plans has increased to 10 million earlier this year, from 1 million in March 2005, according to, America’s Health Insurance Plans (AHIP), a trade group.

HSAs were authorized starting in January 2004. Since then, AHIP has conducted a periodic census of health plans participating in the HSA/HDHP market.

- The number of people with HSA/HDHP coverage rose to more than 11.4 in January 2011, up from 10.0 million in January 2010, 8.0 million in January 2009, and 6.1 million in January 2008.

- 30 percent of individuals covered by an HSA plan were in the small group market, 50 percent were in the large-group market, and the remaining 20 percent were in the individual market.

- 14% of all workers in the private sector that have access to a Health Savings Account acc. to Bureau of Labor Statistics.

- States with the highest levels of HSA/HDHP enrollment were California, Ohio, Florida, Texas, Illinois and Minnesota.

HSA Advantages:

Opportunity to build savings – Unused money stays in your account from year to year and earns tax-free interest. The HSA also gives you an investment opportunity.

Tax-free contributions and earnings – You don’t pay taxes on contributions or earnings.

Tax Free Money allowed for non traditional Medical coverage– As per IRS Publication 502, unused moneys can be used for dental,vision, lasik eye surgery, acupuncture, yoga, infertility etc. Popular Examples

Portability – The funds belong to you, so you keep the funds if you change jobs or retire.

Our overall experience with HSAs have been positive when employer funding is at minimum 50% using either the HSA or an HRA (Health Reimbursement Account-employer keeps unspent money). Traditional plans trend of higher copays and new in network deductibles has also led to the popularity of an HSA.

Please contact us for more customized information and how to incorporate this into your employee benefits.