Today, health care costs are high, and getting higher. Who will pay your bills if you have a serious accident or a major illness? You buy health insurance for the same reason you buy other kinds of insurance, to protect yourself financially. With health insurance, you protect yourself and your family in case you need medical care that could be very expensive. You can’t predict what your medical bills will be. In a good year, your costs may be low. But if you become ill, your bills could be very high. If you have insurance, many of your costs are covered by a third-party payer, not by you. A third-party payer can be an insurance company or, in some cases, it can be your employer.

Sign up for latest news updates. Please contact us for immediate information on how to implement these initiatives for your group-specific needs at info@medicalsolutionscorp.com or Call (855) 667-4621.

Get NY/NJ Individual Insurance:

National:

Please complete the following information if you would like to obtain an individual health insurance quote. Please understand this is not an application for insurance. An application will be sent to you if coverage is desired. All information provided on this information sheet is confidential and will be used solely for the purpose of developing a quote for you.

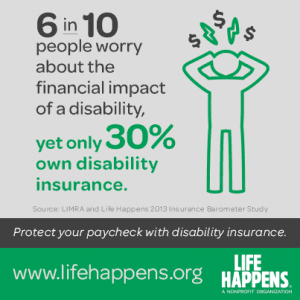

Protects your most valuable asset and your ability to earn an income.

Disability insurance pays cash benefits to the policyholder in the event the insured is unable to work due to sickness or injury. That cash benefit ranges from 50% to 70% of income. The insurance company will not pay more than 70% of income because there must be an incentive to return to work.

If you pay the premium the benefits are normally received free from income tax, if the premiums are paid by an employer, the benefits are taxable as ordinary income.

A disability policy is composed of various elements. Please be advised that the terms used below are not universal and that they vary among the various policie available in the marketplace.

Elimination Period

– It is the period of time the insured must wait after becoming disabled to receive benefits. Typical waiting periods are 30, 60, 90,120,180, and 360 days. The longer the elimination period the less expensive the policy.

Benefit Period

– It is the period of time the benefits will be paid following the elimination period. The benefit period could be from 2 years to age 65 to lifetime. The longer the benefit period the more expensive the policy.

The Amount of Benefit

– The larger the pay-out the more expensive the policy. The benefit will not normally exceed 70% of income.

Residual Benefit

– If you return to work and are still partially disabled and cannot return to work full time or cannot earn your full income, if this coverage is individual it will often pay a benefit proportional to the amount of income lost due to the disability.

Own-Occupation

– A policy with this language included will consider you to be totally disabled i you are unable to perform the material and substantial duties of your occupation.

Reasonable or Any Occupation

– Pays a benefit while disabled, but stops when you are able to return to work at a job that matches your education and experience. This policy is less expensive than an Own-Occupation policy.

Occupation

– Occupation is a factor used in determining rates. For example, a doctor’s rate would be much lower than a blue-collar worker.

Guaranteed Renewable

– Guaranteed Renewable policies cannot be cancelled by the insurance company even if a change in the insured’s circumstances would make him or her a greater risk. Plus, the insurance company cannot make any changes to the provisions of the policy, or add restrictions. When purchasing an individual disability policy it should be Guaranteed Renewable.

Non-Cancelable

– Guarantees future premiums will not be increased. When purchasing an individual policy it should be Non-Cancelable.

Presumptive Disability

– Presumptive disability often means that you are considered total disabled and eligible for benefits for the loss of sight in both eyes or the loss of two limbs. The better contracts also presume total disability for the loss of hearing in both ears, loss of the power of speech, or the loss of the use of two limbs.

Other Benefits that can be added to an individual disability policy, but could also increase the cost:

Protection Against Inflation – A benefit that can be added that offers a cost-of-living adjustment for inflation during a long-term claim.

Automatic Increase Rider

– Automatically increases monthly benefits for a specified period of time. A typical increase is between 3%-5% compound.

Future Increase Options

– Allows the insured to purchase additional benefit amounts without proof of medical insurability. The availability of additional coverage is subject to financial underwriting taking into consideration the insured’s income and other disability insurance.

Capital Sum Benefit

– Typically pays the insured a lump sum benefit up to several times the monthly benefit if the insured lost the sight of one eye with no possibility of recovery or has a hand or foot severed. This benefit is paid in addition to the other benefits.

Rehabilitation Benefit

– To help a disabled insured return to work, this benefit will pay some of the expenses incurred when the insured enrolls in an approved rehabilitation center. This benefit is paid in addition to the other benefits.

Transplant & Cosmetic Surgery Benefit

– Under this benefit, any disability arising from donating a transplant organ, improving your appearance or correcting a disfigurement will be covered by the policy.

Sign up for latest news updates. Please contact us for immediate information on how to implement these initiatives for your group-specific needs at info@medicalsolutionscorp.com or Call (855) 667-4621.

Protects your most valuable asset and your ability to earn an income.

Disability insurance pays cash benefits to the policyholder in the event the insured is unable to work due to sickness or injury. That cash benefit ranges from 50% to 70% of income. The insurance company will not pay more than 70% of income because there must be an incentive to return to work.

If you pay the premium the benefits are normally received free from income tax, if the premiums are paid by an employer, the benefits are taxable as ordinary income.

A disability policy is composed of various elements. Please be advised that the terms used below are not universal and that they vary among the various policie available in the marketplace.

Elimination Period

– It is the period of time the insured must wait after becoming disabled to receive benefits. Typical waiting periods are 30, 60, 90,120,180, and 360 days. The longer the elimination period the less expensive the policy.

Benefit Period

– It is the period of time the benefits will be paid following the elimination period. The benefit period could be from 2 years to age 65 to lifetime. The longer the benefit period the more expensive the policy.

The Amount of Benefit

– The larger the pay-out the more expensive the policy. The benefit will not normally exceed 70% of income.

Residual Benefit

– If you return to work and are still partially disabled and cannot return to work full time or cannot earn your full income, if this coverage is individual it will often pay a benefit proportional to the amount of income lost due to the disability.

Own-Occupation

– A policy with this language included will consider you to be totally disabled i you are unable to perform the material and substantial duties of your occupation.

Reasonable or Any Occupation

– Pays a benefit while disabled, but stops when you are able to return to work at a job that matches your education and experience. This policy is less expensive than an Own-Occupation policy.

Occupation

– Occupation is a factor used in determining rates. For example, a doctor’s rate would be much lower than a blue-collar worker.

Guaranteed Renewable

– Guaranteed Renewable policies cannot be cancelled by the insurance company even if a change in the insured’s circumstances would make him or her a greater risk. Plus, the insurance company cannot make any changes to the provisions of the policy, or add restrictions. When purchasing an individual disability policy it should be Guaranteed Renewable.

Non-Cancelable

– Guarantees future premiums will not be increased. When purchasing an individual policy it should be Non-Cancelable.

Presumptive Disability

– Presumptive disability often means that you are considered total disabled and eligible for benefits for the loss of sight in both eyes or the loss of two limbs. The better contracts also presume total disability for the loss of hearing in both ears, loss of the power of speech, or the loss of the use of two limbs.

Other Benefits that can be added to an individual disability policy, but could also increase the cost:

Protection Against Inflation – A benefit that can be added that offers a cost-of-living adjustment for inflation during a long-term claim.

Automatic Increase Rider

– Automatically increases monthly benefits for a specified period of time. A typical increase is between 3%-5% compound.

Future Increase Options

– Allows the insured to purchase additional benefit amounts without proof of medical insurability. The availability of additional coverage is subject to financial underwriting taking into consideration the insured’s income and other disability insurance.

Capital Sum Benefit

– Typically pays the insured a lump sum benefit up to several times the monthly benefit if the insured lost the sight of one eye with no possibility of recovery or has a hand or foot severed. This benefit is paid in addition to the other benefits.

Rehabilitation Benefit

– To help a disabled insured return to work, this benefit will pay some of the expenses incurred when the insured enrolls in an approved rehabilitation center. This benefit is paid in addition to the other benefits.

Transplant & Cosmetic Surgery Benefit

– Under this benefit, any disability arising from donating a transplant organ, improving your appearance or correcting a disfigurement will be covered by the policy.

Types of Coverage

Social Security

Social Security does not just provide for retirement income but disability income as well.

In 2009, the average monthly payment for a disabled worker was $1064; the average monthly payment for a family of a male disabled worker, young spouse and 2 or more children was $1670.

You are eligible for benefits after you have been disabled for 5 months and if the disability is expected to last 12 months. See Waiting Period Question

Social Security disability payments are subject to federal income tax if your income exceeds $25,000 individually or $32,000 jointly.

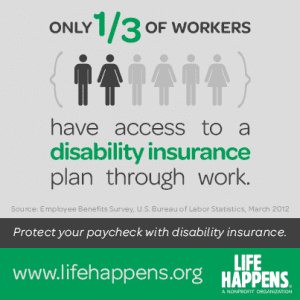

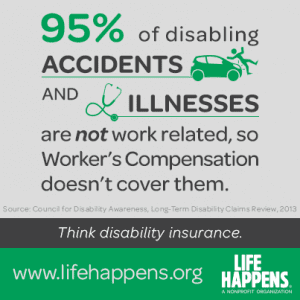

Most employers are required to provide this coverage. The amount and duration varies by state. Workers Compensation only pays if the disability occurs on the job, and usually lasts for only a few years and the payments are low. Individual Policies

For individual policies, the applicant needs to qualify and go through an underwriting process, similar to the process required for life insurance. The applicant could be subject to a higher premium or even be declined based on his or her occupation, medical history, or lifestyle. Individual policies are usually purchased by high income professionals because of the cost.

Group Policies

Some states require employers to carry group disability insurance anywhere from 26 to 52 weeks. New York State Statutory Disability Insurance is a mandatory benefits, Rates and Form are available immediately on site.

Group Long Term Disability (LTD) Group LTD is carried by almost half of mid-size to large employers and provides long term benefits for at least 5 years covering about 60% of salary. The premium is usually very low, does not require proof of insurability, and often is fully paid by the employer.

Protects your most valuable asset and your ability to earn an income.

Disability insurance pays cash benefits to the policyholder in the event the insured is unable to work due to sickness or injury. That cash benefit ranges from 50% to 70% of income. The insurance company will not pay more than 70% of income because there must be an incentive to return to work.

If you pay the premium the benefits are normally received free from income tax, if the premiums are paid by an employer, the benefits are taxable as ordinary income.

A disability policy is composed of various elements. Please be advised that the terms used below are not universal and that they vary among the various policie available in the marketplace.

Elimination Period

– It is the period of time the insured must wait after becoming disabled to receive benefits. Typical waiting periods are 30, 60, 90,120,180, and 360 days. The longer the elimination period the less expensive the policy.

Benefit Period

– It is the period of time the benefits will be paid following the elimination period. The benefit period could be from 2 years to age 65 to lifetime. The longer the benefit period the more expensive the policy.

The Amount of Benefit

– The larger the pay-out the more expensive the policy. The benefit will not normally exceed 70% of income.

Residual Benefit

– If you return to work and are still partially disabled and cannot return to work full time or cannot earn your full income, if this coverage is individual it will often pay a benefit proportional to the amount of income lost due to the disability.

Own-Occupation

– A policy with this language included will consider you to be totally disabled i you are unable to perform the material and substantial duties of your occupation.

Reasonable or Any Occupation

– Pays a benefit while disabled, but stops when you are able to return to work at a job that matches your education and experience. This policy is less expensive than an Own-Occupation policy.

Occupation

– Occupation is a factor used in determining rates. For example, a doctor’s rate would be much lower than a blue-collar worker.

Guaranteed Renewable

– Guaranteed Renewable policies cannot be cancelled by the insurance company even if a change in the insured’s circumstances would make him or her a greater risk. Plus, the insurance company cannot make any changes to the provisions of the policy, or add restrictions. When purchasing an individual disability policy it should be Guaranteed Renewable.

Non-Cancelable

– Guarantees future premiums will not be increased. When purchasing an individual policy it should be Non-Cancelable.

Presumptive Disability

– Presumptive disability often means that you are considered total disabled and eligible for benefits for the loss of sight in both eyes or the loss of two limbs. The better contracts also presume total disability for the loss of hearing in both ears, loss of the power of speech, or the loss of the use of two limbs.

Other Benefits that can be added to an individual disability policy, but could also increase the cost:

Protection Against Inflation – A benefit that can be added that offers a cost-of-living adjustment for inflation during a long-term claim.

Automatic Increase Rider

– Automatically increases monthly benefits for a specified period of time. A typical increase is between 3%-5% compound.

Future Increase Options

– Allows the insured to purchase additional benefit amounts without proof of medical insurability. The availability of additional coverage is subject to financial underwriting taking into consideration the insured’s income and other disability insurance.

Capital Sum Benefit

– Typically pays the insured a lump sum benefit up to several times the monthly benefit if the insured lost the sight of one eye with no possibility of recovery or has a hand or foot severed. This benefit is paid in addition to the other benefits.

Rehabilitation Benefit

– To help a disabled insured return to work, this benefit will pay some of the expenses incurred when the insured enrolls in an approved rehabilitation center. This benefit is paid in addition to the other benefits.

Transplant & Cosmetic Surgery Benefit

– Under this benefit, any disability arising from donating a transplant organ, improving your appearance or correcting a disfigurement will be covered by the policy.

No business can afford to be unprepared for a lawsuit.

Liability insurance protects your business assets when the business is sued for something the business did (or failed to do) that contributed to injury or property damage to someone else.

Liability coverage extends not only to paying damages but also to the attorneys’ fees and other costs involved in defending against the lawsuit, whether valid or not.

The standard business owners policy provides liability coverage, as does a separate policy known as a commercial general liability (CGL) insurance policy.

Generally, commercial liability insurance, whether purchased in a separate policy, or as part of a standard business owners policy, will cover bodily injury, property damage, personal injury or advertising injury. The medical expenses of a person (other than an employee) injured at the business or as a direct result of the operations of the business are also covered.

Usually excluded from both types of liability insurance policies are suits by customers against a business for nonperformance of a contract and by employees charging wrongful termination or racial or gender discrimination or harassment.

Business Group Plans

Types & Uses of Retirement Plans for Business/Group/Employees*

Simplified Employee Pension (SEP) Plan: For self-employed people and small business owners who wish to make tax-deductible contributions of up to $40,000 or 25% of their income, whichever is less, and that of their eligible employees.

Simple IRA Plan: For firms of 100 or fewer employees to establish an employee savings program for pre-tax contributions of up to $7,000 per year.

Profit Sharing Plan (Keogh** Plan): For business owners who wish to make tax-deductible contributions of up to 15% of each participant’s pay, and have vesting and loan schedules not available with a SEP.

Money Purchase Pension Plan (Keogh** Pension Plan): For business owners with predictable incomes who wish to make pre-determined tax-deductible contributions of up to 25% of each Participant’s pay.

Age-Weighted or Comparability Plan: For business owners who are older and more highly paid than most of their employees and wish to allocate contributions under a formula based on both age and salary.

Defined Benefit Pension Plan: For business owners who wish to contribute enough money each year to provide a specific benefit upon retirement. This may be beneficial to older employees with a high, stable income who need a rapid accumulation of assets over a short period of time.

401(k) Plan: For employers who wish to allow employees to make pre-tax contributions through payroll deductions of up to $11,000 per year or 25% of their pay, whichever is less.

Safe Harbor or DASH 401(k) Plan: For business owners who wish to give their employees the advantages of a 401(k) plan, while maximizing the amount they can put away for themselves.

403(b) Plan: For employees of public schools, non-profit hospitals and other certain tax-exempt organizations. Also known as a Tax-Sheltered Account.

Our agency does not provide legal or tax advice. For specific legal or tax advice based on your situation, please contact your attorney of tax advisor.

** The term “Keogh” or “HR-10” describes any type of retirement plan established by an unincorporated business – whether it be a profit sharing, money purchase or defined benefit plan.

Sign up for latest news updates. Please contact us for immediate information on how to implement these initiatives for your group-specific needs at info@medicalsolutionscorp.com or Call (855) 667-4621.

An annuity is a contract issued by an insurance company. It is a unique financial product that provides tax deferral of interest and capital gains and the option (if funds are annuitized) of a guaranteed monthly income for life.

Although annuities can serve various needs, the primary purpose of an annuity is that of a retirement vehicle for the annuitant, the person who will usually receive the annuity benefits. The annuity is an attractive retirement vehicle because the money accumulating in an annuity, grows on a tax deferred basis. There are two parts to an annuity: the accumulation phase and the distribution phase.

After accumulating money in an annuity it is not mandatory that the annuitant exercise the annuitization option and relinquish control of his or her cash value and enter into the annuity distribution phase, the annuitant can simply cash out of his or her annuity. Click here for more info.

Sign up for latest news updates. Please contact us for immediate information on how to implement these initiatives for your group-specific needs at info@medicalsolutionscorp.com or Call (855) 667-4621.

Other Benefits that can be added to an individual disability policy, but could also increase the cost:

Other Benefits that can be added to an individual disability policy, but could also increase the cost: