Disability

Intro to Disability Insurance

DISABILITY INSURANCE – FAQ

Executive Disability Insurance- FAQ

Disability Insurance Employers Guide

NYS Statutory Disability Insurance

Get a Disability Quote

Disability Needs Calculator

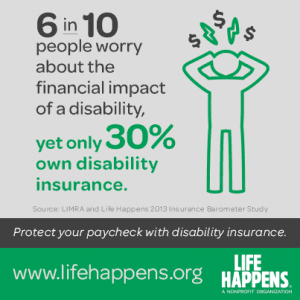

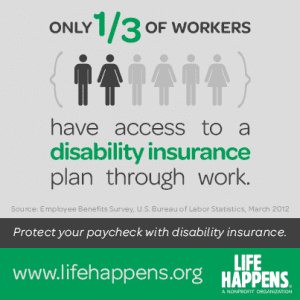

Protects your most valuable asset and your ability to earn an income.

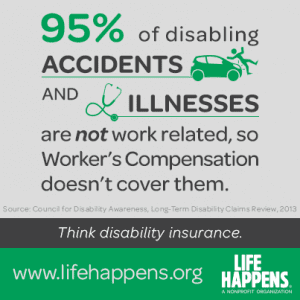

Disability insurance pays cash benefits to the policyholder in the event the insured is unable to work due to sickness or injury. That cash benefit ranges from 50% to 70% of income. The insurance company will not pay more than 70% of income because there must be an incentive to return to work.

If you pay the premium the benefits are normally received free from income tax, if the premiums are paid by an employer, the benefits are taxable as ordinary income.

A disability policy is composed of various elements. Please be advised that the terms used below are not universal and that they vary among the various policie available in the marketplace.

Elimination Period

– It is the period of time the insured must wait after becoming disabled to receive benefits. Typical waiting periods are 30, 60, 90,120,180, and 360 days. The longer the elimination period the less expensive the policy.

Benefit Period

– It is the period of time the benefits will be paid following the elimination period. The benefit period could be from 2 years to age 65 to lifetime. The longer the benefit period the more expensive the policy.

The Amount of Benefit

– The larger the pay-out the more expensive the policy. The benefit will not normally exceed 70% of income.

Residual Benefit

– If you return to work and are still partially disabled and cannot return to work full time or cannot earn your full income, if this coverage is individual it will often pay a benefit proportional to the amount of income lost due to the disability.

Own-Occupation

– A policy with this language included will consider you to be totally disabled i you are unable to perform the material and substantial duties of your occupation.

Reasonable or Any Occupation

– Pays a benefit while disabled, but stops when you are able to return to work at a job that matches your education and experience. This policy is less expensive than an Own-Occupation policy.

- Occupation

– Occupation is a factor used in determining rates. For example, a doctor’s rate would be much lower than a blue-collar worker.

Guaranteed Renewable

– Guaranteed Renewable policies cannot be cancelled by the insurance company even if a change in the insured’s circumstances would make him or her a greater risk. Plus, the insurance company cannot make any changes to the provisions of the policy, or add restrictions. When purchasing an individual disability policy it should be Guaranteed Renewable.

Non-Cancelable

– Guarantees future premiums will not be increased. When purchasing an individual policy it should be Non-Cancelable.

Presumptive Disability

– Presumptive disability often means that you are considered total disabled and eligible for benefits for the loss of sight in both eyes or the loss of two limbs. The better contracts also presume total disability for the loss of hearing in both ears, loss of the power of speech, or the loss of the use of two limbs.

Other Benefits that can be added to an individual disability policy, but could also increase the cost:

Protection Against Inflation – A benefit that can be added that offers a cost-of-living adjustment for inflation during a long-term claim.

Automatic Increase Rider

– Automatically increases monthly benefits for a specified period of time. A typical increase is between 3%-5% compound.

Future Increase Options

– Allows the insured to purchase additional benefit amounts without proof of medical insurability. The availability of additional coverage is subject to financial underwriting taking into consideration the insured’s income and other disability insurance.

Capital Sum Benefit

– Typically pays the insured a lump sum benefit up to several times the monthly benefit if the insured lost the sight of one eye with no possibility of recovery or has a hand or foot severed. This benefit is paid in addition to the other benefits.

Rehabilitation Benefit

– To help a disabled insured return to work, this benefit will pay some of the expenses incurred when the insured enrolls in an approved rehabilitation center. This benefit is paid in addition to the other benefits.

Transplant & Cosmetic Surgery Benefit

– Under this benefit, any disability arising from donating a transplant organ, improving your appearance or correcting a disfigurement will be covered by the policy.

Types of Coverage

Types of Coverage

More information click here

Social Security Disability Calculator

Please contact us for an immediate disability insurance quote & information at info@medicalsolutionscorp.com or Call (855) 667-4621.