Congress has voted to fully repeal the Cadillac Tax and Health Insurance Tax effective January 1, 2021. This means the Health Insurance Tax will still be in place for 2020 and will be gone in 2021.

Both unpopular taxes with bipartisan approval delayed the Cadillac Tax but put the Health Insurance Tax(HIT) back in for 2020 earlier this summer. See Cadillac Tax Out Health Insurance Tax (HIT) Back In. Below are summaries of these two taxes that are now fully repealed.

Whats is the Health Insurance Tax (HIT)?

Health Insurance Tax: This tax included in the Affordable Care Act (ACA) increased the cost of health care coverage for consumers and employers in every state. The ACA imposed a new sales tax on health insurance that started at $8 billion in 2014, increased to $14.3 billion by 2018, and continued to increase each year.

The HIT costing an estimated 2.5%-3% added surcharge or an estimated $500/family annually and $241 for Seniors. Website Stop The Hit calculates $5,000 as the average tax for a 10 man small business for example.

Whats is the Cadillac Tax?

The Cadillac Tax was to take effect in 2022 and had been twice delayed since its original inception scheduled for Jan 2014. This tax called for a 40% excise tax on the amount of the aggregate monthly premium of each primary insured individual that exceeds the year’s applicable dollar limit, which will be adjusted annually to the Consumer Price Index plus 1%.

The 40% excise tax applies to the cost of employer health plan coverage exceeding certain threshold amounts, which were originally set for 2018 at $10,200 for individuals or $27,500 for families.

Originally, the Cadillac Tax was pushed back by the behest of Unions to 2018 from the original proposed 2014 date. Most Unions with generous health care packages would not be complaint within that time frame. For average Gold Plans in regions such as NY, the widely unpopular Cadilac Tax would have been felt.

Learn more about how we are successfully helping navigate SMB for 20+ years. If you have any questions or would like additional information, please contact us at 855-667-4621 or info@360.com.

For more information on PEOs or a customized quote please submit your contact. We will be in touch ASAP.

BREAKING: HIT and Cadillac Tax Repealed

Congress has voted to fully repeal the Cadillac Tax and Health Insurance Tax effective January 1, 2021. This means the Health Insurance Tax will still be in place for 2020 and will be gone in 2021.

Both unpopular taxes with bipartisan approval delayed the Cadillac Tax but put the Health Insurance Tax(HIT) back in for 2020 earlier this summer. See Cadillac Tax Out Health Insurance Tax (HIT) Back In. Below are summaries of these two taxes that are now fully repealed.

Whats is the Health Insurance Tax (HIT)?

Health Insurance Tax: This tax included in the Affordable Care Act (ACA) increased the cost of health care coverage for consumers and employers in every state. The ACA imposed a new sales tax on health insurance that started at $8 billion in 2014, increased to $14.3 billion by 2018, and continued to increase each year.

The HIT costing an estimated 2.5%-3% added surcharge or an estimated $500/family annually and $241 for Seniors. Website Stop The Hit calculates $5,000 as the average tax for a 10 man small business for example.

Whats is the Cadillac Tax?

The Cadillac Tax was to take effect in 2022 and had been twice delayed since its original inception scheduled for Jan 2014. This tax called for a 40% excise tax on the amount of the aggregate monthly premium of each primary insured individual that exceeds the year’s applicable dollar limit, which will be adjusted annually to the Consumer Price Index plus 1%.

The 40% excise tax applies to the cost of employer health plan coverage exceeding certain threshold amounts, which were originally set for 2018 at $10,200 for individuals or $27,500 for families.

Originally, the Cadillac Tax was pushed back by the behest of Unions to 2018 from the original proposed 2014 date. Most Unions with generous health care packages would not be complaint within that time frame. For average Gold Plans in regions such as NY, the widely unpopular Cadilac Tax would have been felt.

Learn more about how we are successfully helping navigate SMB for 20+ years. If you have any questions or would like additional information, please contact us at 855-667-4621 or info@medicalsolutionscorp.com.

Last week the House voted the unpopular Obamacare Cadillac Tax to be permanently repealed 419-6. However, much like a bad cold, the Health Insurance Tax (the HIT) is back for 2020. Website Stop The Hit calculates $5,000 as the average tax for a 10 man small business for example.

Who’s affected?

No one escapes the $16 billion HIT. The return of the Health Insurance Tax (HIT) means higher costs and fewer jobs for hardworking Americans. Absent immediate Congressional action to delay the HIT, small businesses and families will face $500 on average in higher premiums for 2020. To make matters worse, the increased cost burden on small businesses from the HIT could result in the U.S. workforce being reduced by 152,000 to 286,000 jobs over a decade. Te HIT is projected to increase premiums for seniors by $241.

How much for 2020?

For Small business, this translates to an estimated 2.5%-3% added surcharge. For States like NYS where there is already approx. 16% added surcharge to high premiums, this becomes daunting. It is no surprise the unpopular HIT was suspended. In 2017, payers escaped making $13.9 billion in payments due to the moratorium, according to a 2018 analysis by Oliver Wyman, commissioned by UnitedHealth Group. This may have saved consumers billions on their insurance coverage.“The taxes on health insurance are non-deductible for federal tax purposes for health insurers,” the report explained.

In some states, such as Vermont, the price of insurance would have more than quadrupled. The payer trade group published a fact sheet on this. “Allowing a tax to resume in 2020 valued at an annual level of $16 billion, would saddle individual market consumers, small businesses, state Medicaid programs, and Medicare Advantage enrollees with higher health care costs,

Can this be repealed?

Relief from the health insurance tax would result in real savings to the American people. We strongly urge Congress to provide an additional two-year suspension of the health insurance tax by passing H.R. 1398.

Calculates how the HIT affects your State and your business, here.

Take action now: tell Congress to repeal the HIT! Join small business owners across the country in stopping the HIT. Sign the petition here.

Learn more about how we are successfully helping navigate SMB for 20+ years. If you have any questions or would like additional information, please contact us at 855-667-4621 or info@360PEO.com.

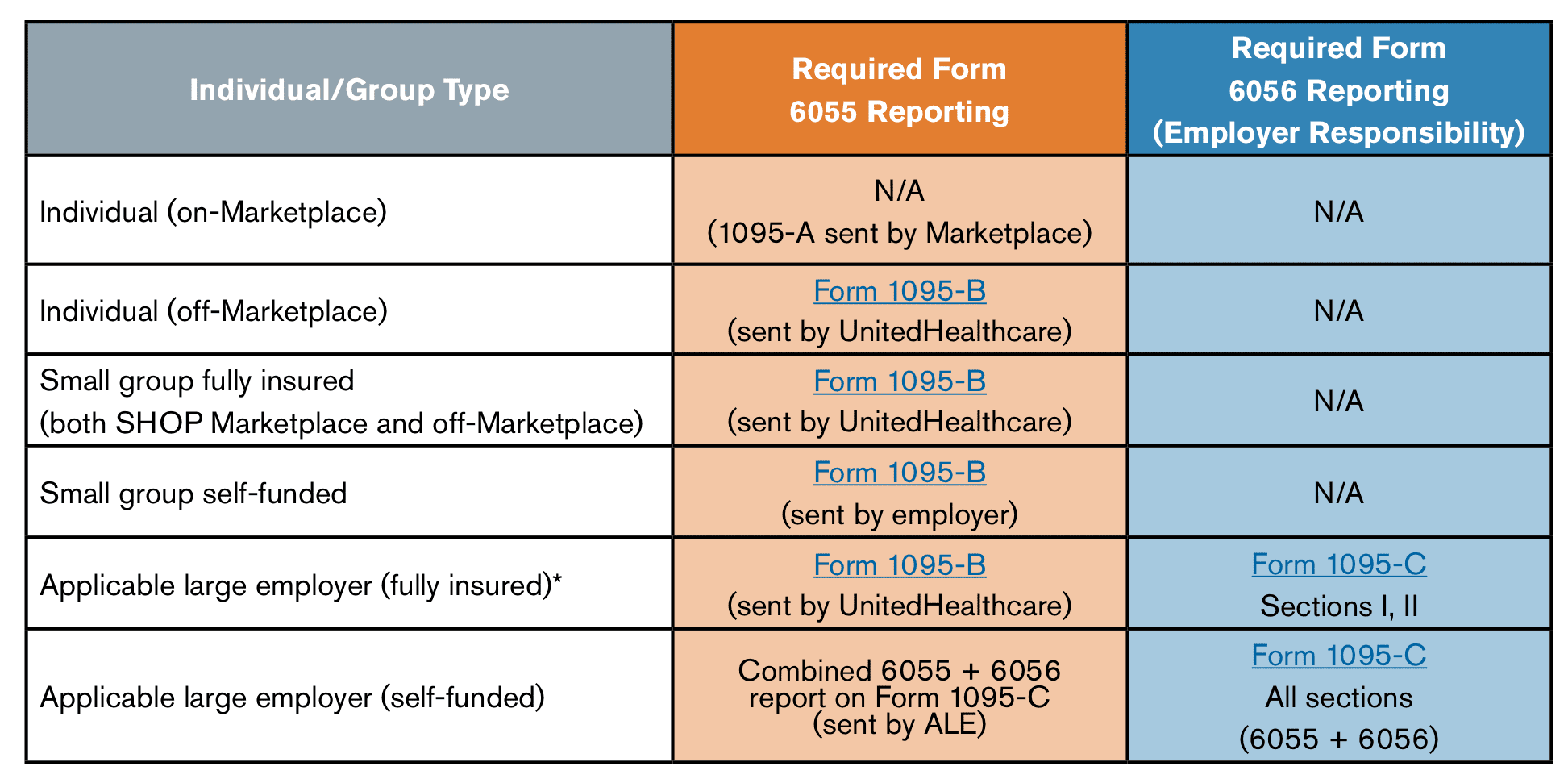

Under Obamacare, the IRS needs to know if your coverage met health care reform standards. The 1095-B is issued by Insurers on behalf of fully insured members directly to the IRS and send members a copy. In short you don’t have to do anything other than reviewing the info and confirming accuracy. 1095B and 6055 Reporting Requirements FAQ

The IRS will accept any number of items to prove that a member had insurance including:

insurance cards

explanation of benefits statements from your insurer

W-2 Form or payroll statements reflecting health insurance deductions

records of advance payments of the premium tax credit

other statements indicating that you, or a member of your family, had health care coverage

What information is on the 1095-B form?

For each person covered on your policy, the 1095-B lists:

Name

Address

Date of birth

Taxpayer identification number (most likely a Social Security number)

Months of coverage with us

If you are missing the taxpayer ID or Social Security numbers for anyone on your policy, the Insurer send you a letter. It’ll explain why they need the information and how to send it to Insurers securely.

How do I know if I should get a 1095-B form?

Insuerers send you a 1095-B form if:

You bought your coverage directly and did NOT go through healthcare.gov.

You get employer coverage and it met the health care reform standards.

6055 Reporting on Form 1095-B

6056 Reporting on Form 1095-C

Provided by Insurer for insured medical plan; by employer for a self-insured medical plan

Provided by applicable large employer (ALE)

Provided to each covered “responsible individual” (e.g., employee, COBRA QB, retiree)

Provided to each full time employee

Provided by March 31, 2016 for coverage in prior calendar year

Provided by March 31, 2016 for coverage offered in prior calendar year

Transmitted with employer’s Form 1094-B to IRS by May 31, 2016 (June 30, 2016 if filed electronically)

Transmitted with employer’s Form 1094-C to IRS by May 31, 2016 (June 30, 2016 if filed electronically)

If your organization can use a helpful audit on ACA, Payroll and HR please contact us today (855) 667-4621 or info@medicalsolutionscorp.com.

This communication is not intended, nor should it be construed, as legal or tax advice. Please contact a competent legal or tax professional for legal advice, tax treatment and restrictions. Federal and state laws and regulations are subject to change.

The IRS Notice released today December 28, 2015 extends the due dates for the 2015 information reporting requirements (both furnishing to individuals and filing with the Internal Revenue Service) for insurers, self-insuring employers, and certain other providers of minimum essential coverage, that is, all Forms 1094 & 1095.

There is no extension for individual tax filings and individual taxpayers/employees may not receive their Forms 1095-B or 1095-C before they file their income tax returns for 2015.

Because of the delay, some employees will not receive their forms until after the April 15 tax filing deadline. The IRS indicates that these employees do not have to file an amended tax return. They should simply keep their forms in a file should they need them later.

Specifically, this notice IRS extends 1094 and 1095 deadlines to:

Form 1095-C – from employer to employees – original deadline was 2/1/16, was extended to 3/31/16

Form 1094-C and 1095-C IRS filing by the employer (paper) original deadline was 2/29/16, was extended to 5/31/16

Form 1094-C and 1095-C IRS filing by employer (electronically) original deadline was 3/31/16, was extended to 6/30/16

Resource:

For a copy of the Notice 2016-4, please click on the link:

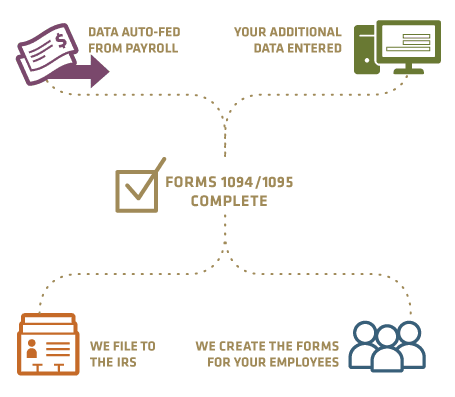

Our payroll partners offer the ability to fill out your Forms 1094 & 1095 as well as providing copies to your employees and filing them with the IRS. For additional general Payroll Support and ACA Tax filings 1094 & 1095 please contact us at 855-667-4621.

The Cadillac Tax has been delayed for two years from 2018 to 2020 by President Obama. With this delay, a repeal could be in reach for congressional leaders and business groups who oppose the Cadillac tax. The legislation also suspends the medical device tax until December 31, 2017 and delays the health insurance tax one year.

Whats a Cadillac Tax?

The 40% excise tax applies to the cost of employer health plan coverage exceeding certain threshold amounts, which were originally set for 2018 at $10,200 for individuals or $27,500 for families. These thresholds are indexed and will be higher on the delayed effective date in 2020. The Omnibus also calls for a study on how to determine adjustments to these thresholds to reflect age and gender differences between businesses. While the tax was originally non-tax deductible, the Omnibus changes that treatment and makes the tax deductible. Originally, the Cadillac Tax was pushed back by the behest of Unions to 2018 from the original proposed 2014 date. Most Unions with generous health care packages would not be complaint within that time frame.

Bipartisanship

The bipartisan vote on the Consolidated Appropriations Act was 316 to 113 in the House, and 65 – 33 in the Senate. Many employers, unions, insurers and industry groups have opposed the tax based on concerns around administrative and financial burdens for employers and adverse outcomes for employees.

Medical Device Tax

The tax bill will place a two-year moratorium on the ACA’s 2.3% tax on the sale of medical devices. The tax imposed under this provision will not apply to sales during the period beginning on January 1, 2016, and ending on December 31, 2017. This applies to sales after December 31, 2015.

Health Insurance Industry Tax

The tax bill places a one-year moratorium on the so-called HIT tax (Health Insurance Industry Tax). If passed, the industry tax will not apply for calendar year 2017, which should result in less of an increase to group health insurance premiums for 2017.

So who said Washington bipartisanship was over? There is hope going into the New Years.

HDHP Minimum Annual Deductible (No change from calendar year 2011):

Single – $1,300 (NONE, $1,300 in 2015)

Family – $2,600 (+$100, $2,500 in 2015)

HDHP Out-of-Pocket Maximum:

Single – $6,550 (+$100, $6,450 in 2015)

Family – $13,100 (+$200, $12,900 in 2015)

Age 55 Catch Up Contribution

As in 401k and IRA contributions, you are allowed to contribute extra if you are above a certain age. If you are age 55 or older by the end of year, you can contribute additional $1,000 to your HSA. If you are married, and both of you are age 55, each of you can contribute additional $1,000.

HSA/HDHP Market Growth

HSA holders own the assets in the accounts and can build up substantial sums over time. Enrollment in HSA-compatible insurance plans has increased to 10 million earlier this year, from 1 million in March 2005, according to, America’s Health Insurance Plans (AHIP), a trade group.

HSAs were authorized starting in January 2004. Since then, AHIP has conducted a periodic census of health plans participating in the HSA/HDHP market.

The number of people with HSA/HDHP coverage rose to more than 11.4 in January 2011, up from 10.0 million in January 2010, 8.0 million in January 2009, and 6.1 million in January 2008.

30 percent of individuals covered by an HSA plan were in the small group market, 50 percent were in the large-group market, and the remaining 20 percent were in the individual market.

14% of all workers in the private sector that have access to a Health Savings Account acc. to Bureau of Labor Statistics.

States with the highest levels of HSA/HDHP enrollment were California, Ohio, Florida, Texas, Illinois and Minnesota.

HSA Advantages:

Opportunity to build savings – Unused money stays in your account from year to year and earns tax-free interest. The HSA also gives you an investment opportunity.

Tax-free contributions and earnings – You don’t pay taxes on contributions or earnings.

Tax Free Money allowed for non traditional Medical coverage– As per IRS Publication 502, unused moneys can be used for dental,vision, lasik eye surgery, acupuncture, yoga, infertility etc. Popular Examples

Portability – The funds belong to you, so you keep the funds if you change jobs or retire.

Our overall experience with HSAs have been positive when employer funding is at minimum 50% using either the HSA or an HRA (Health Reimbursement Account-employer keeps unspent money). Traditional plans trend of higher copays and new in network deductibles has also led to the popularity of an HSA.

(Note that a health plan will not fail to qualify as a high deductible health plan merely because it provides certain preventive health services without a deductible, as required under Health Care Reform.)

Is your HSA compliant? Which pre-tax qualified HSA, FSA, HRA spending card is right for you? Please contact our team at Millennium Medical Solutions Corp (855)667-4621 for immediate answers.. Stay tuned for updates as more information gets released. Sign up for latest news updates.