The IRS has released the 2022 Health Savings Account (HSA) inflation adjustments. To be eligible to make HSA contributions, an individual must be covered under a high deductible health plan (HDHP) and meet certain other eligibility requirements.

New HSA 2022 limits are as follows:

2022

2021

HSA Annual Contribution Limit

$3,650; $7,300

$3,600 – Single; $7,200 – Family

HDHP Minimum Annual Deductible

$1,400; $2,800

$1,400 – Single; $2,800 – Family

HDHP Out-of-Pocket Maximum

$7,050; $14,100

$7,000 – Single; $14,000 – Family

Age 55+ Catch-Up Provision

$1,000; $2,000

$1,000- Single; $2,000 – H/W

Age 55 Catch Up Contribution

As in 401k and IRA contributions, you are allowed to contribute extra if you are above a certain age. If you are age 55 or older by the end of the year, you can contribute an additional $1,000 to your HSA. If you are married, and both of you are age 55, each of you can contribute an additional $1,000. A savvy strategy for high-income earners is to invest the money in your HSA for the long haul. Once you’re 65, you can take out tax-free distributions to cover Medicare premiums. If you withdraw money at that point for non-medical uses, you pay the same tax as you would on withdrawals from a pretax 401(k). But you can also take money out tax-free to reimburse yourself for prior years’ out-of-pocket medical expenses if you have the old receipts.

COVId-19 Update:

You can even use an HSA to save on a typical trip to the CVS. Thanks to a tax relief provision tucked in the last Covid-19 stimulus package, you can use the money you stash in an HSA or FSA (more on those later) for over-the-counter medications like Tylenol or Flonase as well as menstrual products like tampons and pads. That reverses Obamacare restrictions on OTC meds requiring a doctor’s prescription for them to be eligible for reimbursement.

HSA/HDHP Market Growth

HSA holders own the assets in the accounts and can build up substantial sums over time. Enrollment in HSA-compatible insurance plans has increased to 10 million earlier this year, from 1 million in March 2005, according to, America’s Health Insurance Plans (AHIP), a trade group.

HSAs were authorized starting in January 2004. Since then, AHIP has conducted a periodic census of health plans participating in the HSA/HDHP market.

The number of people with HSA/HDHP coverage rose to more than 11.4 in January 2011, up from 10.0 million in January 2010, 8.0 million in January 2009, and 6.1 million in January 2008.

30 percent of individuals covered by an HSA plan were in the small group market, 50 percent were in the large-group market, and the remaining 20 percent were in the individual market.

14% of all workers in the private sector have access to a Health Savings Account acc. to the Bureau of Labor Statistics.

States with the highest levels of HSA/HDHP enrollment were California, Ohio, Florida, Texas, Illinois, and Minnesota.

HSA Advantages:

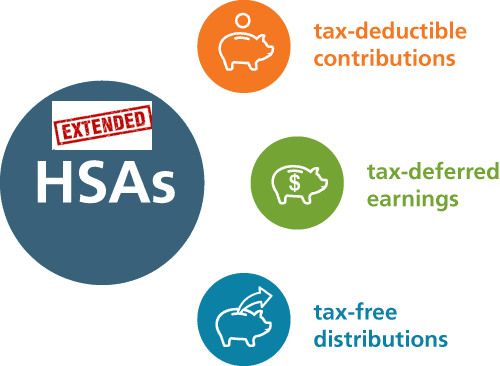

Opportunity to build savings – Unused money stays in your account from year to year and earns tax-free interest. The HSA also gives you an investment opportunity.

Tax-free contributions and earnings – You don’t pay taxes on contributions or earnings.

Tax-Free Money allowed for non-traditional Medical coverage– As per IRS Publication 502, unused money can be used for dental, vision, Lasik eye surgery, acupuncture, yoga, infertility, etc. Popular Examples

Portability – The funds belong to you, so you keep the funds if you change jobs or retire.

Our overall experience with HSAs has been positive when employer funding is at a minimum 50% using either the HSA or an HRA (Health Reimbursement Account-employer keeps unspent money). Traditional plans trend of higher copays and new in-network deductibles has also led to the popularity of an HSA.

Next Steps

Plan sponsors should update payroll and plan administration systems for the 2022 cost-of-living adjustments and should incorporate the new limits in relevant participant communications, such as open enrollment and communication materials, plan documents, and summary plan descriptions.

Is your HSA compliant? Which pre-tax qualified HSA, FSA, HRA spending card is right for you? Please contact our team at Millennium Medical Solutions Corp (855)667-4621 for immediate answers. Stay tuned for updates as more information gets released. Sign up for the latest news updates.

PPE Expenses May Be Reimbursable Under Health Spending Accounts – Video

During the COVID-19 pandemic, you may have purchased masks or PPE for the purpose of preventing the spread of the COVID-19. Now, according to a recent announcement from the IRS, those purchases may be deductible from your income for tax purposes and eligible to be paid or reimbursed under certain savings accounts. This video explains further:

If you’re interested in hearing more about the advantages of partnering with a PEO, we’d love to talk to you. Fill out the form below or email info@medicalsolutionscorp.com for a FREE Consultation Today!

The information provided on this website is intended for informational purposes only. Millennium Medical Solutions Corp. does not offer legal or medical guidance. Those with legal or medical questions should seek appropriate assistance from a licensed professional. Stay up to date by signing up for Newsletter and Coronavirus Dashboard below.

The IRS & SSA announced the 2021 dollar limits for various benefits and compensation levels for retirement plans and IRAs. There are incremental changes but nonetheless worth bookmarking.

The contributions and retirement benefits for qualified retirement plans and individuals. Retirement Arrangements (IRAs) are subject to certain limits that are adjusted by the Secretary of the Treasury annually subject to cost-of-living.Highlightedbelow are the various 2020 and 2021 limits that impact IRA and retirement plans.

The limit on contributions to a traditional. or Roth IRA will remain unchanged in 2021 at $6,000. The limit that applies to IRA catch-up contributions (contributions for individuals age 50 and older) remains at $1,000.

Social Security

The Social. Security Administration (SSA) announced an increase in the taxable wage base (TWB) for 2021 to $142,800 (was $137,700 in 2020). Workers pay Social. Security tax on wages up to the TWB and some retirement plans use the TWB when allocating contributions or calculating benefits.

Although not a formal. retirement plan, health savings accounts (HSA) often factor into retirement savings. The IRS announced the following 2021 limits. These apply to individuals under a high-deductible-health-plan (HDHP). The minimum deductibles and maximum out-of-pocket expenses the IRS uses to define HDHPs are outlined below, as well.

Is your HSA compliant? Which pre-tax qualified HSA, FSA, HRA spending card is right for you? Please contact our team at 360PEO (855)667-4621 for immediate answers. Stay tuned for updates as more information gets released. Sign up for the latest news updates.

The subject matter in this communication is educational only and not rendering legal, accounting, investment advice, or tax advice. You should consult with appropriate counsel or other professionals on all matters pertaining to legal, tax, investment, or accounting obligations and requirements.

The IRS has released the 2021 Health Savings Account (HSA) inflation adjustments. To be eligible to make HSA contributions, an individual must be covered under a high deductible health plan (HDHP) and meet certain other eligibility requirements.

New HSA 2021 limits are as follows:

2021

2020

HSA Annual Contribution Limit

$3,600; $7,200

$3,550 – Single; $7,100 – Family

HDHP Minimum Annual Deductible

$1,400; $2,800

$1,400 – Single; $2,800 – Family

HDHP Out-of-Pocket Maximum

$7,000; $14,000

$6,900 – Single; $13,800 – Family

Age 55+ Catch-Up Provision

$1,000; $2,000

$1,000- Single; $2,000 – Husband/Wife

Age 55 Catch Up Contribution

As in 401k and IRA contributions, you are allowed to contribute extra if you are above a certain age. If you are age 55 or older by the end of the year, you can contribute an additional $1,000 to your HSA. If you are married, and both of you are age 55, each of you can contribute an additional $1,000. A savvy strategy for high-income earners is to invest the money in your HSA for the long haul. Once you’re 65, you can take out tax-free distributions to cover Medicare premiums. If you withdraw money at that point for non-medical uses, you pay the same tax as you would on withdrawals from a pretax 401(k). But you can also take money out tax-free to reimburse yourself for prior years’ out-of-pocket medical expenses if you have the old receipts.

COVId-19 Update:

You can even use an HSA to save on a typical trip to the CVS. Thanks to a tax relief provision tucked in the last Covid-19 stimulus package, you can use the money you stash in an HSA or FSA (more on those later) for over-the-counter medications like Tylenol or Flonase as well as menstrual products like tampons and pads. That reverses Obamacare restrictions on OTC meds requiring a doctor’s prescription for them to be eligible for reimbursement.

HSA/HDHP Market Growth

HSA holders own the assets in the accounts and can build up substantial sums over time. Enrollment in HSA-compatible insurance plans has increased to 10 million earlier this year, from 1 million in March 2005, according to, America’s Health Insurance Plans (AHIP), a trade group.

HSAs were authorized starting in January 2004. Since then, AHIP has conducted a periodic census of health plans participating in the HSA/HDHP market.

The number of people with HSA/HDHP coverage rose to more than 11.4 in January 2011, up from 10.0 million in January 2010, 8.0 million in January 2009, and 6.1 million in January 2008.

30 percent of individuals covered by an HSA plan were in the small group market, 50 percent were in the large-group market, and the remaining 20 percent were in the individual market.

14% of all workers in the private sector have access to a Health Savings Account acc. to the Bureau of Labor Statistics.

States with the highest levels of HSA/HDHP enrollment were California, Ohio, Florida, Texas, Illinois, and Minnesota.

HSA Advantages:

Opportunity to build savings – Unused money stays in your account from year to year and earns tax-free interest. The HSA also gives you an investment opportunity.

Tax-free contributions and earnings – You don’t pay taxes on contributions or earnings.

Tax-Free Money allowed for non-traditional Medical coverage– As per IRS Publication 502, unused money can be used for dental, vision, Lasik eye surgery, acupuncture, yoga, infertility, etc. Popular Examples

Portability – The funds belong to you, so you keep the funds if you change jobs or retire.

Our overall experience with HSAs has been positive when employer funding is at a minimum 50% using either the HSA or an HRA (Health Reimbursement Account-employer keeps unspent money). Traditional plans trend of higher copays and new in-network deductibles has also led to the popularity of an HSA.

Next Steps

Plan sponsors should update payroll and plan administration systems for the 2021 cost-of-living adjustments and should incorporate the new limits in relevant participant communications, such as open enrollment and communication materials, plan documents, and summary plan descriptions.

Is your HSA compliant? Which pre-tax qualified HSA, FSA, HRA spending card is right for you? Please contact our team at Millennium Medical Solutions Corp (855)667-4621 for immediate answers. Stay tuned for updates as more information gets released. Sign up for the latest news updates.

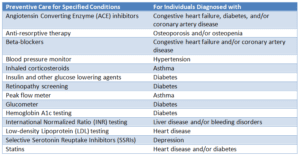

Last week, the IRS added care for a range of chronic conditions to the list of preventive care benefits that may be provided by an HSA compatible high deductible health plans (HDHP). Notice 2019-45, lists the new types of medical care that may be treated as preventive care for this purpose.

Individuals covered by an HSA compatible HDHP generally may establish and deduct contributions to a Health Savings Account (HSA) as long as they have no disqualifying health coverage or not enrolled in Medicare. To qualify as a high deductible health plan, an HDHP generally may not provide benefits for any year until the Federal (not health plan) minimum deductible for that year is satisfied.

The IRS together with the Department of Health and Human Services, has determined that certain medical care services received and items purchased, including prescription drugs, for certain chronic conditions should be classified as preventive care. The following services and items for individuals with the specified chronic conditions listed are treated as preventive care.

Learn how our Agency is helping businesses thrive in today’s economy. Please contact us at info@360PEO.com or (855)667-4621.

The IRS has released the 2020 Health Savings Account (HSA) inflation adjustments. To be eligible to make HSA contributions, an individual must be covered under a high deductible health plan (HDHP) and meet c ertain other eligibility requirements.

New HSA 2020 limits are as follows:

2020

2019

HSA Annual Contribution Limit

$3,550 $7,100

$3,500 – Single $7,000 – Family

HDHP Minimum Annual Deductible

$1,400 $2,800

$1,350 – Single $2,700 – Family

HDHP Out-of-Pocket Maximum

$6,900 $13,800

$6,750 – Single $13,300 – Family

Age 55+ Catch-Up Provision

$1,000 $2,000

$1,000- Single $2,000 – Husband/Wife

Age 55 Catch Up Contribution-As in 401k and IRA contributions, you are allowed to contribute extra if you are above a certain age. If you are age 55 or older by the end of year, you can contribute additional $1,000 to your HSA. If you are married, and both of you are age 55, each of you can contribute additional $1,000

HSA/HDHP Market Growth

HSA holders own the assets in the accounts and can build up substantial sums over time. Enrollment in HSA-compatible insurance plans has increased to 10 million earlier this year, from 1 million in March 2005, according to, America’s Health Insurance Plans (AHIP), a trade group.

HSAs were authorized starting in January 2004. Since then, AHIP has conducted a periodic census of health plans participating in the HSA/HDHP market.

The number of people with HSA/HDHP coverage rose to more than 11.4 in January 2011, up from 10.0 million in January 2010, 8.0 million in January 2009, and 6.1 million in January 2008.

30 percent of individuals covered by an HSA plan were in the small group market, 50 percent were in the large-group market, and the remaining 20 percent were in the individual market.

14% of all workers in the private sector that have access to a Health Savings Account acc. to Bureau of Labor Statistics.

States with the highest levels of HSA/HDHP enrollment were California, Ohio, Florida, Texas, Illinois and Minnesota.

HSA Advantages:

HSA plans are one of the most tax-effective ways to reduce health insurance costs. The amounts contributed are allowed as a full deduction on your tax return and as long as any amounts taking out of the account are used for medical costs, they are completely tax-free including any earnings.

Opportunity to build savings – Unused money stays in your account from year to year and earns tax-free interest. The HSA also gives you an investment opportunity.

Tax-free contributions and earnings – You don’t pay taxes on contributions or earnings.

Tax Free Money allowed for non-traditional Medical coverage– As per IRS Publication 502, unused moneys can be used for dental, vision, lasik eye surgery, acupuncture, yoga, infertility, etc. Popular Examples

Portability – The funds belong to you, so you keep the funds if you change jobs or retire.

Our overall experience with HSAs have been positive when employer funding is at minimum 50% using either the HSA or an HRA (Health Reimbursement Account-employer keeps unspent money). Traditional plans trend of higher copays and new in network deductibles has also led to the popularity of an HSA.

Is your HSA compliant? Which pre-tax qualified HSA, FSA, HRA spending card is right for you? Please contact our team at Millennium Medical Solutions Corp (855)667-4621 for immediate answers. Stay tuned for updates as more information gets released. Sign up for latest news updates.