What is Long Term care? Insurance is an important tool for protecting yourself against risk. For instance, health insurance pays your doctor and hospital bills if you get sick or injured. But how can you protect yourself against the significant financial risk posed by the potential need for long-term care services, either in a nursing home or in your own home?

Long-term care goes beyond medical care and nursing care to include all the assistance you could need if you ever have a chronic illness or disability that leaves you unable to care for yourself for an extended period of time. You can receive long-term care in a nursing home, assisted living facility, or in your own home. Though older people use the most long-term care services, a young or middle-aged person who has been in an accident or suffered a debilitating illness might also need long-term care.

Beyond nursing homes, there is a range of services available in the community to help meet long-term care needs. Visiting nurses, home health aides, friendly visitor programs, home-delivered meals, chore services, adult daycare centers, and respite services for caregivers who need a break from daily responsibilities can supplement care given by family members.

Are you likely to need long-term care? You may never need long-term care. But about 19 percent of Americans aged 65 and older experience some degree of chronic physical impairment. Among those aged 85 or older, the proportion of people who are impaired and require long-term care is about 55 percent. By the year 2020, 12 million older Americans will need long-term care. Most will be cared for at home; family members and friends are the sole caregivers for 70 percent of elderly people. But a study by the U.S. Department of Health and Human Services indicates that people age 65 face at least a 40 percent lifetime risk of entering a nursing home. About 10 percent will stay there five years or longer.

The American population is growing older, and the group over age 85 is now the fastest-growing segment of the population. The odds of entering a nursing home, and staying for longer periods, increase with age. In fact, statistics show that at any given time, 22 percent of those age 85 and older are in a nursing home. Because women generally outlive men by several years, they face a 50 percent greater likelihood than men of entering a nursing home after age 65.

While certainly older people are more likely to need long-term care, your need for long-term care can come at any age. In fact, the U.S. Government Accountability Office estimates that 40 percent of the 13 million people receiving long-term care services are between the ages of 18 and 64.

What do policies cost? The cost of long-term care insurance varies widely, depending on the options you choose. For example, inflation adjustments can add between 40 and more than 100 percent to your premium. However, this option can keep benefits in line with the current cost of care.The actual premium you will pay depends on many factors, including your age, the level of benefits, and the length of time you are willing to wait until benefits begin. A licensed long-term care insurance agent or a financial advisor can help in balancing policy features and premium cost.

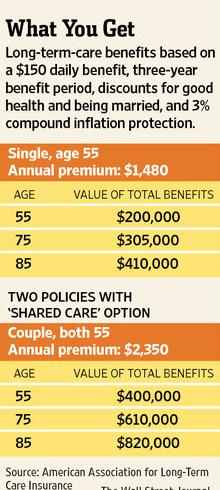

- Age In 2002, a policy offering a $150 per day long-term care benefit for four years, with a 90-day deductible, cost a 50-year-old a national average of $564 per year. For someone who was 65 years old, the national average cost was $1,337, and for a 79-year-old, the national average cost was $5,330. The same policy with an inflation protection feature cost, on average nationally, $1,134 at age 50, $2,346 at age 65, and $7,572 at age 79. Please note that these are only national averages. The cost of long-term care varies significantly by state. For the cost of care and coverage in your area, check with a representative of a long-term care insurer, an insurance agent, or financial adviser.Premiums generally remain the same each year (unless they are increased for an entire class of policyholders at once). That means that the younger you are when you first buy a policy, the lower your annual premium will be.

- Benefits The amount of your premium also depends on the amount of the daily benefit and how long you wish that benefit to be paid. For example, a policy that pays $100 a day for up to five years of long-term care costs more than a policy that pays $50 a day for three years.

- Elimination or deductible periods Elimination or deductible periods are the number of days you must be in residence at a nursing home or the number of home care visits you must receive before policy benefits begin. For instance, with a 20-day elimination period your policy will begin paying benefits on the twenty-first day. Most policies offer a choice of deductible ranging from zero to 180 days. The longer the elimination or deductible period, the lower the premium. However, longer elimination periods also mean higher out-of-pocket costs. For instance, if have a policy with a 100-day waiting period and you go to a nursing home for a year, you must pay for 100 days of care. If your stay costs $150 a day, your total cost would be $15,000. With a 30-day elimination period, your cost would be only $4,500.

When you’re considering a long-term care policy, you should determine, not just how much you can pay for premiums but also how long you could pay for your own care. Bear in mind that while 45 percent of nursing home stays last three months or less, more than one-third last one year or longer. The more costly longer stay may be the devastating financial blow that you may want to insure against.

Where can I get long-term care coverage? Although long-term care insurance is relatively new, more than 100 companies now offer coverage.Long-term care insurance is generally available through groups and to individuals. Group insurance is typically offered through employers, and this type of coverage is becoming a more common benefit. By the end of 2002, more than 5,600 employers were offering a long-term care insurance plan to their employees, retirees, or both.

Individual long-term care insurance coverage is a good option if you are not employed, work for a small company that doesn’t offer a plan, or are self-employed. Choosing a policy requires careful shopping because coverage and costs vary from company to company and depend on the benefit levels you choose.

New York Long Term Care Insurance Partnership Program

TheNew York State Partnership for Long Term Care is a partnership program between private insurance companies and Medicaid to finance Long Term Care of the people of the State of New York. Medicaid program under the Partnership is known as Medicaid Extended Coverage. Under the Partnership program, New Yorkers may be able to apply for Medicaid assistance without exhausting their assets and resources. Medicaid Extended Coverage allows eligible policyholders to protect all of their assets through Total Asset Protection Plan, or some, through Dollar for Dollar Asset Protection Plan. With these alternatives, New Yorkers are assured of their continued care after using up the benefits provided by their private insurance policies, without losing their life savings and their dignity.

| Region | Home Health Aide Hourly Rate (Medicare Certified) | Assisted Living Facility Monthly Rate (Private room) | Nursing Home Daily Rate (Semi-private room) | Nursing Home Daily Rate (Private room) |

| Albany – Schenectady – Troy | $23 | $3,723 | $304 | $315 |

| Binghamton | $21 | $5,078 | $280 | $290 |

| Bronx | $16 | $2,045 | $382 | $382 |

| Brooklyn | $18 | $1,850 | $340 | $343 |

| Buffalo – Niagara Falls | $23 | $3,633 | $301 | $305 |

| Elmira | $21 | $2,965 | $313 | $317 |

| Glens Falls | $23 | $2,828 | $270 | $281 |

| Ithaca | $22 | $5,440 | $250 | $263 |

| Kingston | $20 | $3,231 | $354 | $362 |

| Long Island | $22 | $3,800 | $398 | $388 |

| Manhattan | $19 | $1,720 | $438 | $459 |

| Outer New York City Area | $21 | $6,000 | $325 | $358 |

| Poughkeepsie – Newburgh – Middletown | $24 | $3,800 | $357 | $367 |

| Queens | $17 | $4,000 | $331 | $336 |

| Rochester | $24 | $3,788 | $305 | $325 |

| Staten Island | $19 | $2,225 | $310 | $325 |

| Syracuse | $20 | $2,750 | $270 | $270 |

| Utica – Rome | $19 | $2,344 | $235 | $250 |

| Rest of State | $23 | $2,200 | $251 $258 | |

Long Term Care Partnership Policies

All insurance companies participating in the Partnership program must include the following basic benefits in the policies that they offer:

- Nursing home care

- Nursing home bed reservation of 20 days per year

- Skilled nursing care

- Assisted living care

- Adult care

- Home care

- Personal care

- Respite care (14 nursing home equivalent days per year)

- Hospice care

- Alternate level of care – in-patient services received in a hospital while waiting to be placed in a nursing home, or while waiting for arrangements for home care.

- Care management – minimum of 2 consultations per calendar year. This is a face-to-face care management consultation done by independent healthcare professionals, to assess the services received by a policyholder and give recommendations to optimize utilization of insurance benefits. Care management benefits depend on the amount of the nursing home daily benefit. For instance, if a policyholder has a $300 nursing home daily benefit, his care management benefits would amount to $600 for one calendar year. If one care management consultation costs $200, then a total of three consultations can be accessed for a year. However, care management benefits, if used, are deducted from the maximum lifetime benefits that a policyholder may receive.

- Inflation protection of 5% compounded annually – Partnership policies issued to qualified policyholders aged 79 and below include a 5% annual compounded inflation protection. This benefit is optional to those aged 80 and above.

- Guaranteed renewable – the insurance company cannot decline should a policyholder wishes to renew a policy, provided that the policyholder pays the premium on time and makes no changes in the provision of the Partnership policy while it is in force.

- Partnership Independent Assessment Benefit – a unique feature of Partnership policies. This allows policyholders who are denied by their Partnership insurance company of benefits (due to failure to meet disability standards) to request for an independent review by the New York State Partnership office.

Additional benefits may be offered by some participating insurance companies but with additional costs in policy premiums. Examples are waiver of premium (payment of premium is waived after care has started), combined home care benefit, independent provider benefit, etc.

Types of Partnership Policies in the New York Long Term Care Partnership Program

1. Total Asset 50 – minimum 3 years Nursing home care OR 6 years Home care with a minimum daily benefit of $218 for Nursing home and $109 for Home care.

2. Total Asset 100 – minimum 4 years Nursing Home care OR 4 years Home care OR 4 years Residential Care Facility. The minimum daily benefit of $218 is provided for Nursing Home and $218 for Home care.

Both Total Asset 50 and Total Asset 100 can have unlimited maximum policy duration and 100 days maximum elimination period.

3. Dollar for Dollar 50 – minimum 1.5 years Nursing home care OR 3 years Home care and maximum 2.5 years Nursing Home or 5 years Home Care. Minimum daily benefits are $218 for Nursing home and $109 for Home care.

4. Dollar for Dollar 100 – minimum 2 years Nursing Home care OR 2 years Home care OR 2 years Residential Care Facility and maximum of 2.5 years for the aforementioned care settings. The minimum daily benefit of $218 is provided for Nursing Home and $218 for Home care.

Both Dollar for Dollar 50 and Dollar for Dollar 100 Plans have 60 days elimination period.

Obtaining a Partnership Policy in New York

Applicants go through an assessment process and must satisfy requirements in order to qualify to the Partnership program. The New York State office does not sell Partnership policies. The New York State Department of Insurance authorizes private insurance companies to market Partnership policies. Below is a list of participating insurance companies:

For individual policies:

- Genworth Life Insurance Company of New York

- John Hancock Life Insurance Co.

- MedAmerica Insurance Co. of New York

- Metropolitan Life Insurance Company

- New York Life Insurance Company

For group policies:

- CNA Insurance Companies (NYC Employees Only)

- MedAmerica Insurance Co. of NY

- MedAmerica Insurance Co. of NY (NYS Employees and Retirees Only)

- Metropolitan Life Insurance Company (NYSUT Members Only)

- Prudential Insurance Company (AICPA Members Only)

The New York State Partnership for Long Term Care has no reciprocity agreement. Therefore if you move to another state, you must come back to New York State and be a resident to be eligible for the Medicaid Extended Coverage part of your Partnership policy.

For more information, you may contact the toll-free New York State Medicaid Helpline at 1-800-541-2831 or the Human Resources Administration at 1-877-472-8411 for NYC residents (5 Boroughs).

Can I move out of NY and use this? Your Partnership policy has two components: a private insurance component and the Medicaid Extended Coverage component. During the private component, you can use your policy’s benefits wherever you choose (in accordance with the policy contract conditions). During the Medicaid Extended Coverage component, you must be a New York State resident in order to receive New York State Medicaid Extended Coverage.

Millennium Medical Solutions Corp is trained and certified to offer NYS Partnership for LTC.

Fill out this short form to get your free quotes from all providers