Recently, UHC/Oxford and Mt Sinai Health System had split effective January 1, 2024. Since that time there have been a state-required cooling-off period and ongoing talks on resolution but that has not yielded a positive outcome yet. The Mount Sinai Hospital, Mount Sinai Queens, and their related hospital outpatient locations will remain in-network for all patients until at least Friday, March 1.

According to UnitedHealthcare/Oxford:

People enrolled in UnitedHealthcare fully insured commercial plans have continued network access to all of Mount Sinai’s hospitals through Feb. 29, 2024, due to New York cooling-off requirements.

Unless they obtain admitting privileges to another in-network hospital, the majority of Mount Sinai’s physicians will no longer participate in our network for employer-sponsored and individual plans, including the Oxford Health Plan, effective March 22, 2024.

This negotiation only impacts our relationship with Mount Sinai for employer-sponsored and individual commercial plans, including Oxford. All other active contracts, including Medicare Advantage and the Empire Plan, remain in place with no change.

The two organizations had a three-year agreement that took effect on Jan. 1, 2022, which was canceled before it was supposed to expire amid a dispute over payment rates. Both institutions are blaming one another for the standoff.

Mount Sinai claims UnitedHealthcare compensates it an average of 30% less for care than other health systems in New York. The insurer pays New York-Presbyterian $25,911 for a normal vaginal birth, and Mount Sinai $15,989, Mount Sinai said.

“Mount Sinai must be paid fairly,” spokeswoman Lucia Lee said in a statement. “As Mount Sinai costs substantially less than our peers, UHC/Oxford will actually end up paying more for patients to get care at other systems in New York. This cost — estimated to be at least $140 million more over the course of a year — will be passed on to employers and patients.”

UnitedHealthcare says Mount Sinai sought “outlandish price hikes” that would increase costs for services an average of 50% over three years or $600 million — an estimate disputed by Mount Sinai. For example, a regular, outpatient colonoscopy at South Nassau costs about $6,000 and would be about $8,700 in three years under Mount Sinai’s proposal, according to UnitedHealthcare.

Mt Sinai Hospitals & Health System

Facility Name

County

Mount Sinai Beth Israel

NYC

The Mount Sinai Hospital

NYC

Mount Sinai Morningside

NYC

The Mount Sinai West

NYC

Mount Sinai-Union Square

NYC

Mount Sinai Kravis Children’s Hospital

NYC

Mount Sinai-Behavioral Health Center (MSBHC)

NYC

Blavatnik Center, Medical Center

NYC

New York Eye and Ear Infirmary of Mount Sinai

NYC

Mount Sinai Brooklyn

Brooklyn

Mount Sinai Queens

Queens

Mount Sinai South Nassau

Long Island

Neighboring Hospitals

Bellevue Hospital Center

NYC

New York Presbyterian Queens

Queens

Elmhurst Hospital Center

Queens

New York Presbyterian Weill Cornell

NYC

Flushing Hospital Medical Center

Queens

North Shore University Hospital Manhasset

Long Island

Lenox Hill Hospital

NYC

NYU Langone Hospital Brooklyn

Brooklyn

Long Island Jewish Medical Center

Brooklyn

NYU Langone Hospital Long Island

Long Island

Maimonides Medical Center

Brooklyn

St. Francis Hospital

Long Island

Mercy Medical Center

Long Island

St. Johns Episcopal Hospital

Queens

New York Presbyterian Columbia

NYC

St. Joseph Hospital

Queens

New York Presbyterian Lower Manhattan Hospital

NYC

Wyckoff Heights Medical Center

Brooklyn

Both sides need each other as both are market leaders in their fields. It is our hope and most of our clients that they get this resolved soon. In the meantime, please bookmark our site for the latest updates. And do reach out to us and learn the steps that you can take to smoothen this temporary roadblock.

We already love Professional Employer Organizations (PEO)– our clients do too. Today we’re counting down our top 5 reasons why we love PEO:

1. National Capabilities: It ensures your compliance with local and federal laws, even if your business has locations in different states. Access to a national provider healthcare plan, not single state carriers

2. Liability Protections: Some liability moves to the PEO service instead of your company.

3. It saves you money on HR staff. Being part of a PEO gives you a clear-cut idea of what your costs are going to be a year in and year out. The PEOs work tirelessly to keep their insurance renewals down, so their clients won’t leave. Every year they work with the insurance carriers to introduce new plans and ways to reduce the costs of insurance to their clients. This gives you the ability to forecast and know precisely what your costs will be.

4. Technologies: Online HR resources for self-service issues Ability for employees to make personal changes on their own, online. Ability to track PTO (paid-time off).

5. One Vendor: It streamlines HR tasks like payroll, taxes, employee benefits, worker’s compensation, 401K, and HR administrative tasks.

Our PEO Quoting Tool ensures that we have first-hand insight as to what the small business owner needs to be successful. Click below for a quote.

Healthcare is constantly evolving, shaping how people view their health and well-being. The complexities of managing rising healthcare costs, the continuous evolution of the modern workplace, and a heightened focus on employee wellbeing highlight the necessity for a broader perspective on the concept of “workplace wellbeing.”

To be successful, organizations must construct a future that works for everyone, including individuals, the workforce, and the organization.

How will employers invest in workplace well-being?

According to aGreat Place to Workand Johns Hopkins survey in 2023, employee well-being is a key predictor of employee retention and referrals. It identifies that:

Promoting employee well-being requires consistent listening and regular communication with employees.

Employees who experience high levels of well-being in the workplace are three times more likely to stay with their employer.

Employees who experience high levels of well-being in the workplace are three times more likely to recommend their employer to others.

It’s safe to say that providing a culture of health and well-being within your organization significantly impacts more than just healthcare costs and physical health.

Think about every aspect of your life where support is needed—and how everyone’s list differs. Wellbeing at work should be addressed by supporting the “whole person.” This means employers should support not only physical health but also the following:

Mental health

Digital wellbeing

A work-life balance

Financial wellbeing

Family support services

Although this list is not exhaustive, it highlights the complex and interdependent nature of workplace wellbeing needs.

5 trends that will shape the future of employee wellbeing:

Mental Health and Emotional Wellbeing:

Emotional wellbeing has taken center stage in the post-pandemic years. One positive outcome of the pandemic is the awareness and need for greater mental health resources and the de-stigmatization of mental health in the workplace. According to aGallup poll, 19% of U.S. workers rate their mental health as fair or poor.

Here are some of the things that are being implemented as they relate to mental wellbeing at work:

“Safe Space” communities:Employees can access mental health resources and learn to support others while sharing personal stories.

Manager’s Training:Leaders can access training to learn how to be effective listeners, identify, and respond swiftly to the mental health needs of their teams. These training courses also help inform company policy needs and provide a framework to be developed within all areas of the organization.

Mindfulness Resources:Incorporating relaxation solutions into the workplace with on-the-go apps, online platforms, calm spaces, or meditation rooms involves integrating mindfulness tools into communication platforms.

The Continued Rise of Technology – Driven Solutions

The intersection of convenience, privacy, and adaptability is crucial for digital wellbeing tools. Integrating technology into employee wellbeing programs not only improves accessibility and convenience but also enhances data collection and analysis, which helps organizations gain insight into health trends and potential interventions. Finding a way to tie these different technology systems together will be instrumental when it comes to the interconnectedness of data and programs.

Some solutions are determined to stick around, and ones that you might consider include:

Personalized Wellness Platforms: Artificial Intelligence (AI) is inspired to adapt to individual preferences and circumstances with constantly evolving algorithms that adjust real-time recommendations based on new user data, behavioral patterns, personalized content, and customized plans.

Telehealth Solutions: With multi-modal consultation formats and interactive platforms, integrated health allows individual solutions to be consolidated into more holistic platforms, bringing together everything someone needs in one place.

Wearable Technology: Fitness trackers and smartwatches are being used to monitor physical activity, sleep patterns, and overall health. Wearables that adapt their tracking based on user lifestyle algorithms will be instrumental in personalization and customization.

Flexibility and Work/Life Balance:

The COVID-19 pandemic forced organizations to adopt remote work arrangements on an unprecedented scale. Whether your office now promotes a worksite that is hybrid, in-office, or remote, having flexible work arrangements helps accommodate employees, enhance work-life balance, and make companies more attractive.

Develop strategies to support employees wherever they are:

Virtual Wellness and Fitness Classes:Allow employees to participate in their health and wellbeing wherever they are.

Telehealth Visits:Offers flexibility to talk with a doctor from the comfort of their home.

Virtual Team-building Activities:Allow employees to connect even though they are not physically together.

Invest in Technology Tools:Facilitating seamless collaboration among remote and in-office teams or multiple locations.

Financial Wellbeing

A recentstudy by PwCfound that57%of employees say finances are the top cause of stress in their lives. When people have money worries, it impacts morale and productivity, not to mention overall physical and mental health. Businesses have a responsibility to help their employees by investing in financial wellbeing, education, and resources, but also to help retain top talent in this ever-changing job market.

Here are some services to consider offering:

Financial Wellness Coaching:Such as one-on-one coaching, workshops, webinars, and online tools

Financial Education:Literacy opportunities on topics such as budgeting, saving, investing, debt management, and overall financial planning.

Financial Wellness Benefits:Such as tuition reimbursement, employer-sponsored retirement plans, or home-buying assistance programs.

Family Support Services:

Balancing the roles of parent, caregiver, and employee can feel like juggling two full-time jobs. Having a supportive employer makes all the difference.Caregiver responsibilitiesfor both children and aging parents put a strain on mental and physical health. Having programs and support for a range of needs helps employees feel supported.

How do you invest in caregivers?

Financial support, such as childcare subsidies or discounts for daycare centers

Flex spending accounts for dependent care expenses

Backup care services

Eldercare resources

Caregiver leave/paid time off

Maternity and paternity leave

Mental health benefits for caregivers

Return to work programs

Wellbeing investments in the workplace are retention boosters and help secure top talent. According to anotherGallup poll, 63% of workers say that having work-life balance and better personal wellbeing opportunities is very important when considering a new job. Organizations should look to provide more inclusive, equitable benefits and wellbeing programs across their workforce. In the future, organizations will intensify their focus on human-centric wellbeing, aiming to enhance the employee experience and drive concrete business results by evolving from the appearance of personalization to genuine personalization.

The wellness landscape is changing daily. Employers should research the options by seeking guidance with a PEO. We have multiple wellness programs and initiatives that can be implemented and offer comprehensive ACA compliance/reporting services to clients.

This Compliance Overview is not intended to be exhaustive nor should any discussion or opinions be construed as legal advice. Readers should contact legal counsel for legal advice.

In preparation for open enrollment, Employers should review their plan documents in light of changes for the plan year beginning Jan 1, 2024. Below is an Employer 2024 Open Enrollment Checklist including some administrative items to prepare for in 2024.

Change has been constant for employer plans in the last few years. Unfortunately, 2023 was no exception. As they prepare for 2024 open enrollment, employers must incorporate new requirements affecting the design and administration of their health plans for plan years beginning on or after Jan. 1, 2024. Those changes include items that are adjusted for cost of living changes each year, – e.g., the cost-sharing limits for high deductible health plans (HDHPs), contribution limits to health savings accounts (HSAs), as well as new requirements due to legislative and regulatory updates, such as the expiration of COVID-19 mandates, to name a few.

Employers should ensure their health plan is updated and communicate benefit changes to participants through an updated summary plan description (SPD) or a summary of material modifications (SMM) for the 2024 plan year.

As a general best practice, employers should confirm that their open enrollment materials contain certain required participant notices and consider including some periodic notices, such as the Medicare Part D creditable/non-creditable coverage notice, in their open enrollment materials.

PLAN DESIGN CHANGES

ACA Mandates

Affordability Requirements

Under the ACA’s employer shared responsibility rules (the “pay or play” rules), applicable large employers (ALEs) (those with 50 or more full-time employees or the equivalent) are required to offer affordable, minimum value health coverage to their full-time employees (and dependent children) or risk paying a penalty.

Under the ACA, an ALE’s health coverage is considered affordable if the employee’s required contribution to the plan does not exceed 9.5% of the employee’s household income for the taxable year (as adjusted each year). The adjusted percentage is 9.12% for 2023.

The affordability percentage for plan years that begin on or after Jan. 1, 2024, will be 8.39%. That is another reduction demonstrating the need for ALEs to monitor the affordability percentage each year so they can confirm that at least one of the health plans offered to full-time employees satisfies the ACA’s affordability standard (typically by the use of one of the optional safe harbors – federal poverty level, W-2 or rate of pay).

Out-of-pocket Maximum

Under the ACA, non-grandfathered health plans (which apply to almost all employer plans) are subject to limits on cost sharing for essential health benefits. Confirm that out-of-pocket maximum limits for your health plan comply with the ACA’s limits for the 2024 plan year.

Plan years beginning on or after Jan. 1, 2024:

$9,450for self-only coverage

$18,900for family coverage

Note, the out-of-pocket maximum limits for HDHPs compatible with HSAs must be lower than the ACA’s limits. For the 2024 plan year, the out-of-pocket maximum limits for HDHPs are $8,050 for self-only coverage and $16,100 for family coverage.

Preventive Care Benefits

The ACA requires non-grandfathered health plans to cover certain preventive health services without imposing cost-sharing requirements (e.g., deductibles, copayments, or coinsurance) when in-network healthcare providers supply the services. The preventive care services covered by the requirements are based on the following:

Evidence-based items or services that have a rating of A or B in the current recommendations of the United States Preventive Services Task Force (USPSTF).

Immunizations for routine use in children, adolescents, and adults that are currently recommended by the Centers for Disease Control and Prevention.

Evidence-informed preventive care and screenings are included in the Health Resources and Services Administration (HRSA) guidelines for infants, children, and adolescents.

Evidence-informed preventive care and screenings are included in HRSA-supported guidelines for women.

There needs to be some clarity. An ongoing court case has raised some uncertainty about using the USPSTF recommendations. However, guidance from federal agencies will permit employers to use those factors without the risk of penalties for the time being. Therefore, employers should monitor future developments regarding the ACA’s preventive care mandate, which is expected by the end of 2023.

Coverage For COVID-19 Vaccines, Testing And Treatment

Because the COVID-19 public health emergency has ended (seeAlert here), health plans are no longer required to cover COVID-19 diagnostic tests and related services without cost sharing or other medical management requirements. Health plans are still required to cover recommended preventive services (under the ACA requirements), including COVID-19 immunizations, without cost sharing, but this coverage requirement can now be limited to in-network providers.

For plan years ending after Dec. 31, 2024, an HSA-compatible HDHP is no longer permitted to provide COVID-19 testing and treatment benefits without a deductible (or with a deductible below the minimum deductible for an HDHP). Therefore, employers should

Determine whether health plans will impose cost-sharing requirements, prior authorization, or other medical management requirements on COVID-19 testing for the upcoming plan year.

Determine whether health plans will continue covering COVID-19 immunizations without cost sharing from all healthcare providers or whether this first-dollar coverage will be limited to in-network providers.

Confirm that HDHPs that do not have a calendar year as the plan year will not pay benefits for COVID-19 testing and treatment before the annual minimum deductible has been met for plan years ending after Dec. 31, 2024.

Notify plan participants of any changes for the 2024 plan year regarding COVID-19 testing and vaccines through an updated SPD or SMM.

The IRS issued a memorandum on claims substantiation (see Article here) for health FSAs. The memorandum clarifies that health FSA expenses are not considered properly substantiated if employees self-certify expenses, if the plan uses sampling, if only amounts over a certain level are substantiated, or if charges from favored providers are not substantiated. Employers should, therefore, review the health FSA substantiation procedures to make sure they comply with IRS rules.

If you offer an HDHP to your employees that is compatible with an HSA, you should confirm that the HDHP’s minimum deductible and out-of-pocket maximum comply with the 2020 limits. The IRS limits for HSA contributions and HDHP cost-sharing increase for 2024. The HSA contribution limits will increase effective Jan. 1, 2024, while the HDHP limits will increase effective for plan years beginning on or after Jan. 1, 2024.

Check whether your HDHP’s cost-sharing limits need to be adjusted for the 2024 limits.

If you communicate the HSA contribution limits to employees as part of the enrollment process, these enrollment materials should be updated to reflect the increased limits that apply for 2024.

The following table contains the HDHP and HSA limits for 2024 as compared to 2023. It also includes the catch-up contribution limit that applies to HSA-eligible individuals who are age 55 or older, which is not adjusted for inflation and stays the same from year to year.

Type of Limit

2024

2023

Change

HSA Contribution Limit

Self-only

$4,150

$3,850

Up $300

Family

$8,300

$7,750

Up $550

HSA Catch-up Contributions (not subject to adjustment for inflation)

Age 55 or older

$1,000

$1,000

No change

HDHP Minimum Deductible

Self-only

$1,600

$1,500

Up $100

Family

$3,200

$3,000

Up $200

HDHP Maximum Out-of-pocket Expense Limit (deductibles, copayments and other amounts, but not premiums)

Self-only

$8,050

$7,500

Up $550

Family

$16,100

$15,000

Up $1,100

HDHP Design Option – Telehealth

At the beginning of the COVID-19 pandemic, Congress temporarily relaxed the rules for HDHPs to allow them to provide benefits for telehealth or other remote care services before plan deductibles were met without jeopardizing HSA eligibility. That relaxed rule currently applies for plan years beginning before Jan. 1, 2025.

Determine whether HDHPs will waive the deductible for telehealth services for the plan year beginning in 2024

Communicate plan changes for the upcoming year to participants through an updated SPD or SMM

Mental Health Parity – Required Comparative Analysis For NQTLs

The Mental Health Parity and Addiction Equity Act (MHPAEA) requires parity between a group health plan’s medical/surgical benefits and its mental health or substance use disorder (MH/SUD) benefits. These parity requirements apply to financial requirements and treatment limits for MH/SUD benefits. In addition, any nonquantitative treatment limitations (NQTLs) placed on MH/SUD benefits must comply with MHPAEA’s parity requirements. For example, NQTLs include prior authorization, step therapy protocols, network adequacy, and medical necessity criteria.

MHPAEA requires health plans and issuers to conduct comparative analyses of the NQTLs used for medical/surgical benefits compared to MH/SUD benefits. This analysis must contain a detailed, written, and reasoned explanation of the specific plan terms and practices and include the basis for the plan or issuer’s conclusion that the NQTLs comply with MHPAEA. Plans and issuers must make their comparative analyses available to specific federal agencies or applicable state authorities upon request.

Employers should request that health plan issuers (or third-party administrators) confirm that comparative analyses of NQTLs will be updated, if necessary, for the plan year beginning in 2024 and make the analysis available to the employee.

Open Enrollment Notices

Employers who sponsor group health plans should provide certain benefits notices in connection with their open enrollment periods. Some of these notices must be provided at open enrollment time, such as the Summary of Benefit and Coverage (SBC). Other notices, such as the WHCRA notice, must be distributed annually. Although these annual notices may be provided at different times throughout the year, employers often include them in their open enrollment materials for administrative convenience.

In addition, employers should review their open enrollment materials to confirm that they accurately reflect the terms and cost of coverage. In general, any plan design changes for 2024 should be communicated to plan participants through an updated SPD or an SMM.

Summary Of Benefits And Coverage

The ACA requires health plans and health insurance issuers to provide an SBC to applicants and enrollees each year at open enrollment or renewal. Federal agencies have provided atemplatefor the SBC, which health plans must use.

Note that for self-funded plans, the plan administrator is responsible for providing the SBC. For insured plans, the issuer usually prepares the SBC. If the issuer prepares the SBC, an employer is not required to also prepare an SBC for the health plan, although the employer may need to distribute the SBC prepared by the issuer.

Medicare Part D Notices

Group health plan sponsors must provide a notice of creditable or non-creditable prescription drug coverage to Medicare Part D-eligible individuals covered by, or who apply for, prescription drug coverage under the health plan. The notice alerts the individuals about whether their prescription drug coverage is at least as good as Medicare Part D coverage. The notice generally must be provided at various times that cannot always be anticipated, including when an individual enrolls in the plan and each year before Oct. 15 (when the Medicare annual open enrollment period begins). Therefore, the best practice is to provide it annually at open enrollment, as that will ensure timely compliance. Model notices are available on the Centers for Medicare and Medicaid Services’website.

Annual CHIP Notices

Group health plans covering residents in a state that provides a premium subsidy to low-income children and their families to help pay for employer-sponsored coverage must send an annual Children’s Health Insurance Program (CHIP) notice about the available assistance to all employees in that state. The U.S. Department of Labor (DOL) has provideda model notice.

Initial COBRA Notices

COBRA applies to employers with 20 or more employees who sponsor group health plans. Group health plan administrators must provide an initial COBRA notice to new participants and certain dependents within 90 days after plan coverage begins. The initial COBRA notice may be incorporated into the plan’s SPD. Because the COBRA election-period will not start until this notice is provided, it is helpful to many employers to include a copy in the open enrollment materials as a backup.

Notices Of Patient Protections

Under the ACA, group health plans and issuers that require the designation of a participating primary care provider must permit each participant, beneficiary, and enrollee to designate any available participating primary care provider (including a pediatrician for children). Additionally, plans and issuers that provide obstetrical/gynecological care and require a designation of a participating primary care provider may not require preauthorization or referral for such care. If a health plan requires participants to designate a participating primary care provider, the plan or issuer must provide a notice of these patient protections whenever the SPD or similar description of benefits is provided to a participant. If an employer’s plan is subject to this notice requirement, they should confirm that it is included in the plan’s open enrollment materials. This notice may be included in the plan’s SPD.Model languageis available from the DOL.

Grandfathered Plan Notices

If an employer has a grandfathered plan, they should include information about its grandfathered status in plan materials describing the coverage under the plan, such as SPDs and open enrollment materials. Model language is available from the DOL.

Notices Of HIPAA Special Enrollment Rights

At or before enrollment, an employer’s group health plan must provide each eligible employee with a notice of their special enrollment rights under HIPAA. This notice may be included in the plan’s SPD.

HIPAA Privacy Notices

The HIPAA Privacy Rule requires covered entities (including group health plans and issuers) to provide a Notice of Privacy Practices (or Privacy Notice) to everyone who is the subject of protected health information (PHI). Health plans are required to send the Privacy Notice at certain times, including to new enrollees at the time of enrollment. Also, at least once every three years, health plans must either redistribute the Privacy Notice or notify participants that the Privacy Notice is available and explain how to obtain a copy. Self-insured health plans are required to maintain and provide their own Privacy Notices. However, special rules apply for fully insured plans, where the health insurance issuer, not the plan itself, is primarily responsible for the Privacy Notice.

Special Rules for Fully Insured Plans

The plan sponsor of a fully insured health plan has limited responsibilities with respect to the Privacy Notice, including the following:

If the sponsor of a fully insured plan has access to PHI for plan administrative functions, they are required to maintain a Privacy Notice and to provide the notice upon request.

If the sponsor of a fully insured plan does not have access to PHI for plan administrative functions, they are not required to maintain or provide a Privacy Notice.

A plan sponsor’s access to enrollment information, summary health information, and PHI that is released pursuant to a HIPAA authorization does not qualify as having access to PHI for plan administration purposes.

Model Privacy Notices are available through the Department of Health and Human Services.

WHCRA Notices

Plans and issuers must provide notice of participants’ rights to mastectomy-related benefits under the WHCRA at the time of enrollment and annually. The DOL’s compliance assistance guide includes model language for this disclosure.

SARs

Plan administrators required to file Form 5500 must provide participants with a narrative summary of the information in Form 5500, called a summary annual report (SAR). Amodel noticeis available from the DOL.

Group health plans that are unfunded (that is, benefits are payable from the employer’s general assets and not through an insurance policy or trust) are not subject to the SAR requirement. The plan administrator generally must provide the SAR within nine months of the close of the plan year. If an extension of time to file Form 5500 is obtained, the plan administrator must furnish the SAR within two months after the close of the extension period.

Wellness Program Notices

Group health plans that include wellness programs may be required to provide certain notices regarding the program’s design. As a general rule, these notices should be provided when the wellness program is communicated to employees and before employees provide any health-related information or undergo medical examinations. These notices are required in the following situations:

HIPAA Wellness Program Notice—HIPAA imposes a notice requirement on health-contingent wellness programs offered under group health plans. Health-contingent wellness plans require individuals to satisfy standards related to health factors (e.g., not smoking) to obtain rewards. The notice must disclose the availability of a reasonable alternative standard to qualify for the reward (and, if applicable, the possibility of waiver of the otherwise applicable standard) in all plan materials describing the terms of a health-contingent wellness program. The DOL’scompliance assistance guideincludes a model notice that can be used to satisfy this requirement.

ADA Wellness Program Notice—Employers with 15 or more employees are subject to the Americans with Disabilities Act (ADA). Wellness programs that include health-related questions or medical exams must comply with the ADA’s requirements, including an employee notice requirement. Employers must give participating employees a notice that tells them what information will be collected as part of the wellness program, with whom it will be shared, and for what purpose, as well as the limits on disclosure and the way information will be kept confidential. The U.S. Equal Employment Opportunity Commission (EEOC) has provided asample noticeto help employers comply with this ADA requirement.

ICHRA Notices

Employers may use individual coverage HRAs (ICHRAs) to reimburse their eligible employees for insurance policies purchased in the individual market or Medicare premiums. Employers with ICHRAs must notify eligible participants about the ICHRA and its interaction with the ACA’s premium tax credit. In general, this notice must be provided at least 90 days before the start of each plan year. Employers may provide this notice at open enrollment time if it is at least 90 days before the beginning of the plan year. A model notice is available for employers to use to satisfy this notice requirement.

________________________________

Enhance Your Employee Benefits Package. A competitive benefits package is key to keeping and attracting top talent.Assess your current benefits package and consider making necessary adjustments to include options, such as expanded mental health support, for example.

GENERAL HR

Review Employee Records. The fourth quarter is a good time to review your employee records and check record retention guidelines. Don’t forget to dispose of outdated termination and outdated job applications properly. With W2s around the corner, make sure all addresses and information are updated.

Develop and Distribute Your 2024 Calendar. Create and distribute a calendar outlining important dates, vacation time, pay dates, and company-observed holidays for 2024.

Review and Update Employee Handbook. Review your employee handbook to make sure it is up-to-date and addresses areas, such as employment law mandates, new COVID-related policies, guidelines for remote working, privacy policies, compensation and performance reviews, social media policies, attendance, and time-off, break periods, benefits, and procedures for termination, discipline, workplace safety, and emergency procedures.

PLEASE NOTE: This Checklist is not intended to be exhaustive nor should any discussion or opinions be construed as legal advice. Readers should contact legal counsel for legal advice. This information is for general reference purposes only. Because laws, regulations, and filing deadlines are likely to change, please check with the appropriate organizations or government agencies for the latest information and consult your employment attorney and/or benefits advisor regarding your responsibilities. In addition, your business may be exempt from certain requirements and/or be subject to different requirements under the laws of your state. (Updated Sept 3, 2023)

Contact us at (855) 667-4621 or email us at info@360peo.com

About this Session: Engaging your workforce and captivating them: How do you achieve this? During this session we discuss how to deploy engaging tactics with the right balance of frequency and educational impacts across a multi-generational workforce to engage your employees when it matters most..

Why We Love PEO This Valentine’s Day. Today we’re counting down our top 5 reasons why we love PEO. National Capabilities, Liability Protections, Technologies, One Vendor and PEO saves you money on HR staff. Try Our PEO Quoting Tool today.

Discover the future of employee wellbeing. From mental health strategies to tech-driven solutions and flexible work arrangements, this piece explores 5 trends shaping the workplace of tomorrow.

“This year’s rankings represent an expanded universe, with three new countries on the list—Colombia, Saudi Arabia, and the United Arab Emirates—bringing the total to over 2,300 hospitals in 28 countries. And the results show a remarkable cross-section of excellence across the world: Twenty-one countries are represented in the global top 150. The U.S. leads with 29 hospitals, followed by Germany with 16; Italy and France with 10 each; and South Korea with eight. Overall, there were 13 new hospitals in this year’s top 100. Among the biggest movers from last year’s rankings were No. 8 Northwestern Memorial Hospital (28 in 2022); No. 40 Seoul’s Samsung Medical Center (73) and No. 11 New York’s NYU Langone Hospitals (59).”

Top 10 Internationally:

1Mayo Clinic Rochester- United States 2Cleveland Clinic- United States 3Massachusetts General Hospital- United States 4The Johns Hopkins Hospital- United States 5Toronto General – University Health Network- Canada 6Karolinska Universitetssjukhuset- Sweden 7Charité – Universitätsmedizin- BerlinGermany 8AP-HP – Hôpital Universitaire Pitié Salpêtrière- France 9Singapore General Hospital- Singapore 10UCLA Health – Ronald Reagan Medical Center- United States

Top 20 Nationally:

1Mayo Clinic – Rochester 2ClevelandClinic 3MassachusettsGeneral Hospital 4TheJohns Hopkins Hospital 5UCLAHealth – Ronald Reagan Medical Center 6 Stanford Health Care – Stanford Hospital 7BrighamAnd Women’s Hospital 8NorthwesternMemorial Hospital 9TheMount Sinai Hospital 10New York-Presbyterian Hospital-Columbia and Cornell

11. University of Michigan Hospitals – Michigan Medicine 12 Cedars-Sinai Medical Center 13. UCSF Medical Center 14. Duke University Hospital 15. Hospital of the University of Pennsylvania – Penn Presbyterian 16. NYU Langone Hospitals 17. Mayo Clinic – Jacksonville 18. Russh University Medical Center 19. Mayo Clinic – Phoenix 20. Houston Methodist Hospital

Top 10 NY/NJ Metro Hospitals:

9

The Mount Sinai Hospital

83.98%

New York

NY

10

New York-Presbyterian Hospital-Columbia and Cornell

83.94%

New York

NY

16

NYU Langone Hospitals

81.23%

New York

NY

46

Morristown Medical Center

70.66%

Morristown

NJ

57

Hackensack University Medical Center

69.52%

Hackensack

NJ

117

Strong Memorial Hospital – University of Rochester

65.36%

Rochester

NY

121

Valley Hospital

65.30%

Ridgewood

NJ

130

North Shore University Hospital

65.21%

Manhasset

NY

148

Saratoga Hospital

64.71%

Saratoga Springs

NY

167

Overlook Medical Center

64.42%

Summit

NJ

Top 3 CT Hospitals:

35YaleNew Haven Hospital 158 St. Francis Hospital& Medical Center 201Griffin Hospital

Top 10 PA Hospitals:

15

Hospital of the University of Pennsylvania – Penn Presbyterian

Philadelphia

PA

54

Jefferson Health – Thomas Jefferson University Hospitals

Philadelphia

PA

58

UPMC Presbyterian & Shadyside

Pittsburgh

PA

64

Penn State Health – Milton S. Hershey Medical Center

Hershey

PA

76

Penn Medicine Chester County Hospital

West Chester

PA

103

Reading Hospital

Reading

PA

116

St. Luke’s Hospital Bethlehem

Bethlehem

PA

122

Doylestown Hospital

Doylestown

PA

153

Lancaster General Hospital

Lancaster

PA

168

Main Line Health – Lankenau Medical Center

Wynnewood

PA

Top 10 FL Hospitals:

17

Mayo Clinic – Jacksonville

Jacksonville

FL

45

Cleveland Clinic – Florida

Weston

FL

84

Tampa General Hospital

Tampa

FL

146

Sarasota Memorial Hospital

Sarasota

FL

149

St. Joseph’s Hospital – BayCare

Tampa

FL

172

Baptist Health Baptist Hospital

Miami

FL

176

Morton Plant Hospital

Clearwater

FL

179

Baptist Medical Center – Beaches

Jacksonville Beach

FL

183

Adventhealth Orlando

Orlando

FL

215

Cape Canaveral Hospital

Cocoa Beach

FL

NOTE: For patients and their physicians, these rankings and ratings should be seen as just a starting point. While this is helpful information to have, benefit plan participants should also research quality hospitals using transparency tools if these services are available through the health plan or benefits package. For a customized review of your commercial sponsored plan using latest tools and third part-tools please contact us today.

The IRS, yesterday, released the 2024 Health Savings Account (HSA) inflation adjustments. To be eligible to make HSA contributions, an individual must be covered under a high deductible health plan (HDHP) and meet certain other eligibility requirements.

New HSA 2024 limits are as follows:

2024

2023

HSA Annual Contribution Limit

$4,150; $8,300

$3,850 – Single; $7,750 – Family

HDHP Minimum Annual Deductible

$1,600; $3,200

$1,500 – Single; $3,000 – Family

HDHP Out-of-Pocket Maximum

$8,050; $16,100

$7,500 – Single; $15,000 – Family

Age 55+ Catch-Up Provision

$1,000; $2,000

$1,000- Single; $2,000 – Husband/Wife

Age 55 Catch Up Contribution

As in 401k and IRA contributions, you are allowed to contribute extra if you are above a certain age. If you are age 55 or older by the end of the year, you can contribute an additional $1,000 to your HSA. If you are married, and both of you are age 55, each of you can contribute an additional $1,000. A savvy strategy for high-income earners is to invest the money in your HSA for the long haul. Once you’re 65, you can take out tax-free distributions to cover Medicare premiums. If you withdraw money at that point for non-medical uses, you pay the same tax as you would on withdrawals from a pretax 401(k). But you can also take money out tax-free to reimburse yourself for prior years’ out-of-pocket medical expenses if you have the old receipts.

COVId-19 Update:

You can even use an HSA to save on a typical trip to the CVS. Thanks to a tax relief provision tucked in the last Covid-19 stimulus package, you can use the money you stash in an HSA or FSA (more on those later) for over-the-counter medications like Tylenol or Flonase as well as menstrual products like tampons and pads. That reverses Obamacare restrictions on OTC meds requiring a doctor’s prescription for them to be eligible for reimbursement.

HSA/HDHP Market Growth

HSA holders own the assets in the accounts and can build up substantial sums over time. Enrollment in HSA-compatible insurance plans has increased to 10 million earlier this year, from 1 million in March 2005, according to, America’s Health Insurance Plans (AHIP), a trade group.

HSAs were authorized starting in January 2004. Since then, AHIP has conducted a periodic census of health plans participating in the HSA/HDHP market.

The number of people with HSA/HDHP coverage rose to more than 11.4 in January 2011, up from 10.0 million in January 2010, 8.0 million in January 2009, and 6.1 million in January 2008.

30 percent of individuals covered by an HSA plan were in the small-group market, 50 percent were in the large-group market, and the remaining 20 percent were in the individual market.

14% of all workers in the private sector have access to a Health Savings Account acc. to the Bureau of Labor Statistics.

States with the highest levels of HSA/HDHP enrollment were California, Ohio, Florida, Texas, Illinois, and Minnesota.

HSA Advantages:

Opportunity to build savings – Unused money stays in your account from year to year and earns tax-free interest. The HSA also gives you an investment opportunity.

Tax-free contributions and earnings – You don’t pay taxes on contributions or earnings.

Tax-Free Money allowed for non-traditional Medical coverage– As per IRS Publication 502, unused money can be used for dental, vision, Lasik eye surgery, acupuncture, yoga, infertility, etc. Popular Examples

Portability – The funds belong to you, so you keep the funds if you change jobs or retire.

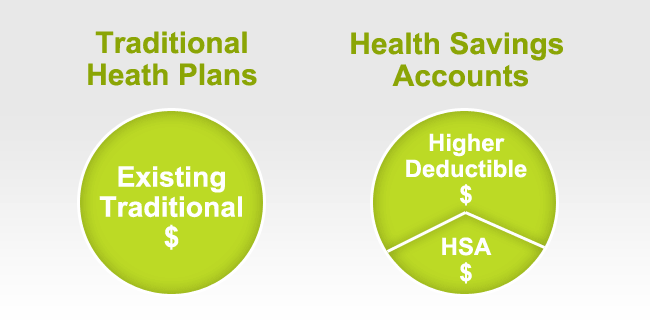

Our overall experience with HSAs has been positive when employer funding is at a minimum 50% using either the HSA or an HRA (Health Reimbursement Account-employer keeps unspent money). Traditional plans trend of higher copays and new in-network deductibles has also led to the popularity of an HSA.

Next Steps

Plan sponsors should update payroll and plan administration systems for the 2023 cost-of-living adjustments and should incorporate the new limits in relevant participant communications, such as open enrollment and communication materials, plan documents, and summary plan descriptions.

Is your HSA compliant? Which pre-tax qualified HSA, FSA, HRA spending card is right for you? Please contact our team at 360PEO (855)667-4621 for immediate answers. Stay tuned for updates as more information gets released. Sign up for the latest news updates.

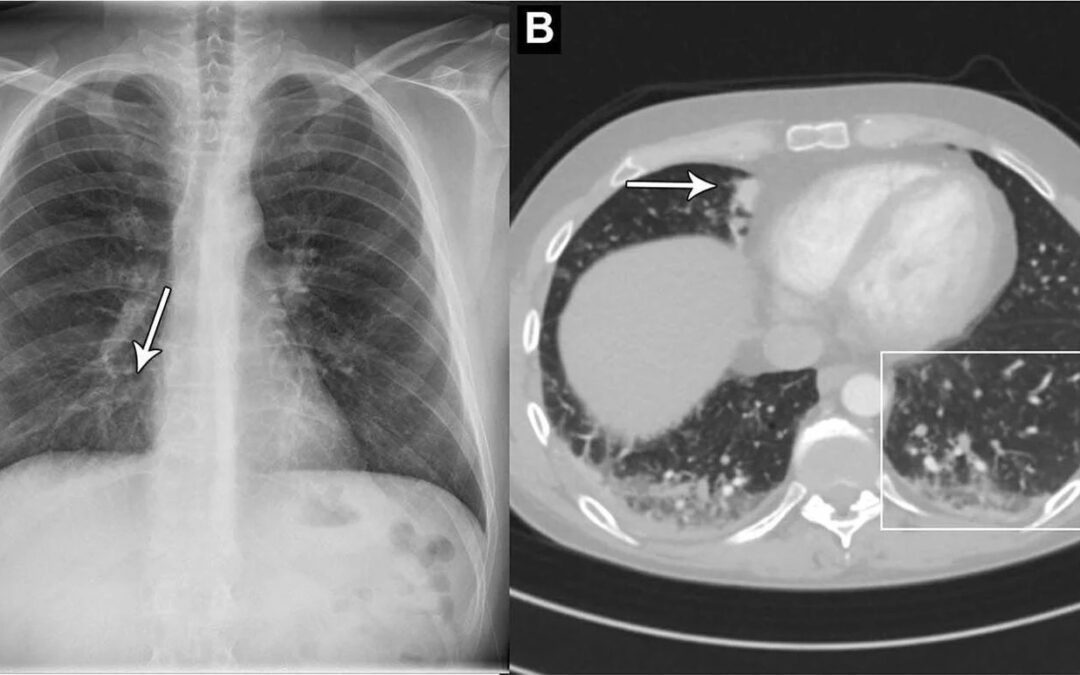

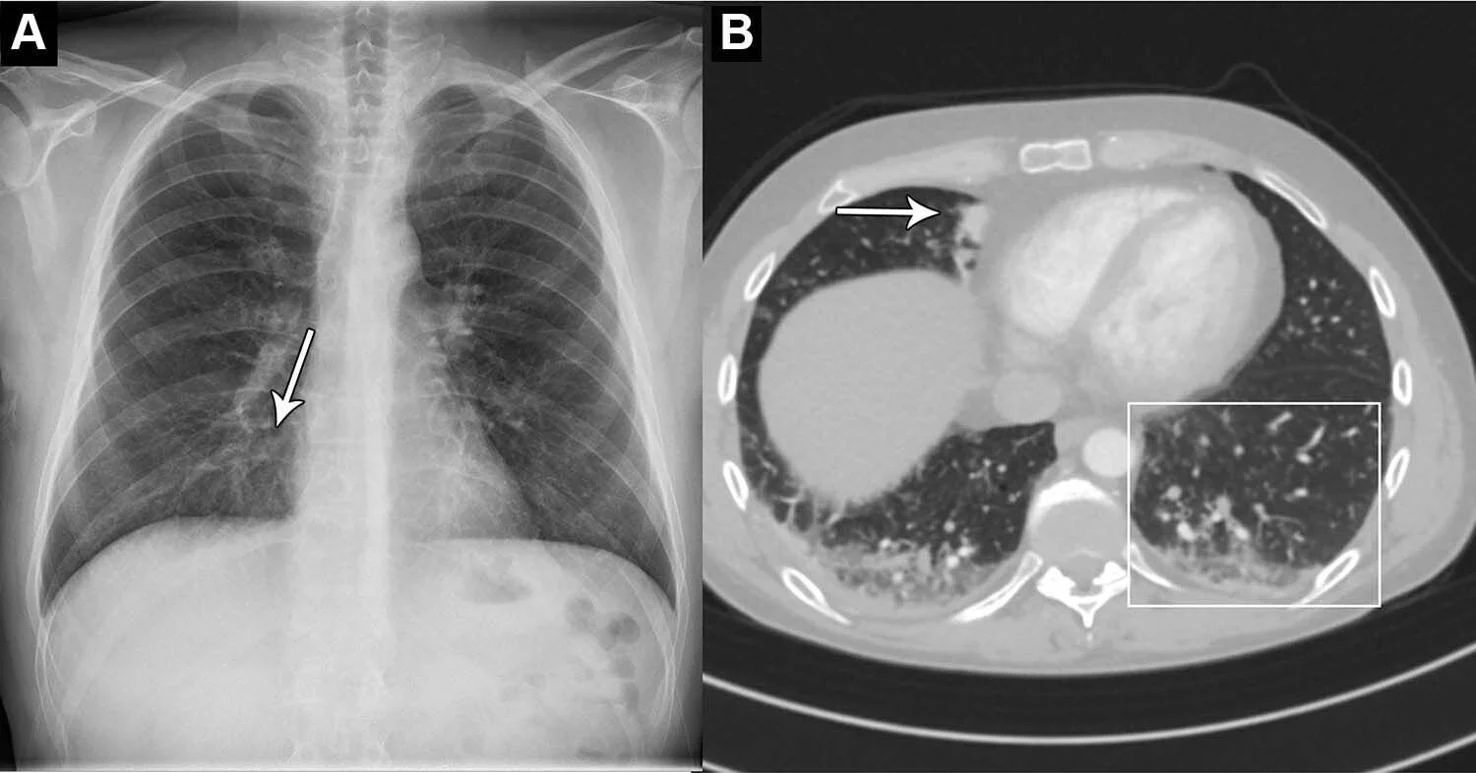

Artificial intelligence can help spot early signs of cancer in chest x-rays, according to a new study.

Scientists found that a state-of-the-art AI tool can identify normal and abnormal chest x-rays in a clinical setting.

Scientists said that an AI tool could accurately differentiate between normal and abnormal chest x-rays. (Photo via SWNS)

Chest X-rays are used to diagnose several conditions to do with the heart and lungs.

An abnormal chest X-ray can be an indication of a range of conditions, including cancer and chronic lung diseases.

Scientists say that an AI tool that can accurately differentiate between normal and abnormal chest X-rays would greatly reduce the heavy workload of radiologists.

Study co-author Dr. Louis Lind Plesner said: “There is an exponentially growing demand for medical imaging, especially cross-sectional such as CT and MRI.

“Meanwhile, there is a global shortage of trained radiologists.

“Artificial intelligence has shown great promise, but should always be thoroughly tested before any implementation.”

Dr. Plesner and his colleagues wanted to determine the reliability of using an AI tool that can identify normal and abnormal chest X-rays.

They used a commercially available AI tool to analyze the chest X-rays of 1,529 patients from four hospitals in Denmark.

Chest X-rays were included from emergency department patients, in-hospital patients and outpatients.

The X-rays were classified by the AI tool as either “high-confidence normal” or “not high-confidence normal,” as in normal and abnormal, respectively.

Two board-certified radiologists were used as the reference standard. A third radiologist was used in cases of disagreements.

Of the 429 chest X-rays that were classified as normal, 120 (28 percent) were also classified by the AI tool as normal. Those X-rays – 7.8 percent of the total – could be potentially safely automated by an AI tool.

The AI tool identified abnormal chest X-rays with a 99.1 percent of sensitivity.

Dr. Plesner, from the Department of Radiology at the Herlev and Gentofte Hospital in Copenhagen, said: “The most surprising finding was just how sensitive this AI tool was for all kinds of chest disease.

“In fact, we could not find a single chest X-ray in our database where the algorithm made a major mistake.

“Furthermore, the AI tool had a sensitivity overall better than the clinical board-certified radiologists.”

He said the AI tool performed particularly well at identifying normal X-rays of the outpatient group at a rate of 11.6 percent.

Dr. Plesener said the findings, published in the journal Radiology, suggest that the AI model would perform especially well in outpatient settings with a high prevalence of normal chest X-rays.

He added: “Chest X-rays are one of the most common imaging examinations performed worldwide.

“Even a small percentage of automatization can lead to saved time for radiologists, which they can prioritize on more complex matters.”

The editorial on the topic praised the potential to take care of 7.8% of all the normal readings for the radiologists, one of the key findings of the study, but suggests that as a labor-saving device, more research is needed to ensure radiologists aren’t putting patients at risk for a mere 7.8% reduction in workload.

The IRS has released the 2023 Flexible Savings Account (FSA) inflation adjustments. These changes will take place for plan years that begin on or after January 1, 2023.

For employers who currently allow the FSA maximum, unless told otherwise, OCA will automatically amend the new FSA maximum to reflect the 2023 increase. OCA will also be providing additional 2023 employee guides/marketing material in the upcoming days. *The limit also applies to limited-purpose FSAs.

On September 1, 2022, Empire BlueCross BlueShield will begin partnering with CareMount Medical, the largest independent, multi-specialty group in New York State, to provide access to affordable care throughout New York City, Westchester, Putnam, Dutchess, Columbia, and Ulster counties.

CareMount will now be part of Empire’s Blue Access and Connection Networks for all Large Group and Small Group members. This will mean greater access to more affordable care throughout Westchester and surrounding markets.

Contact us to learn how Empire can fit your employee’s needs.

Learn more about how we are successfully helping navigate SMB for 25+ years. If you have any questions or would like additional information, please contact us at 855-667-4621 or info@360peo.com.

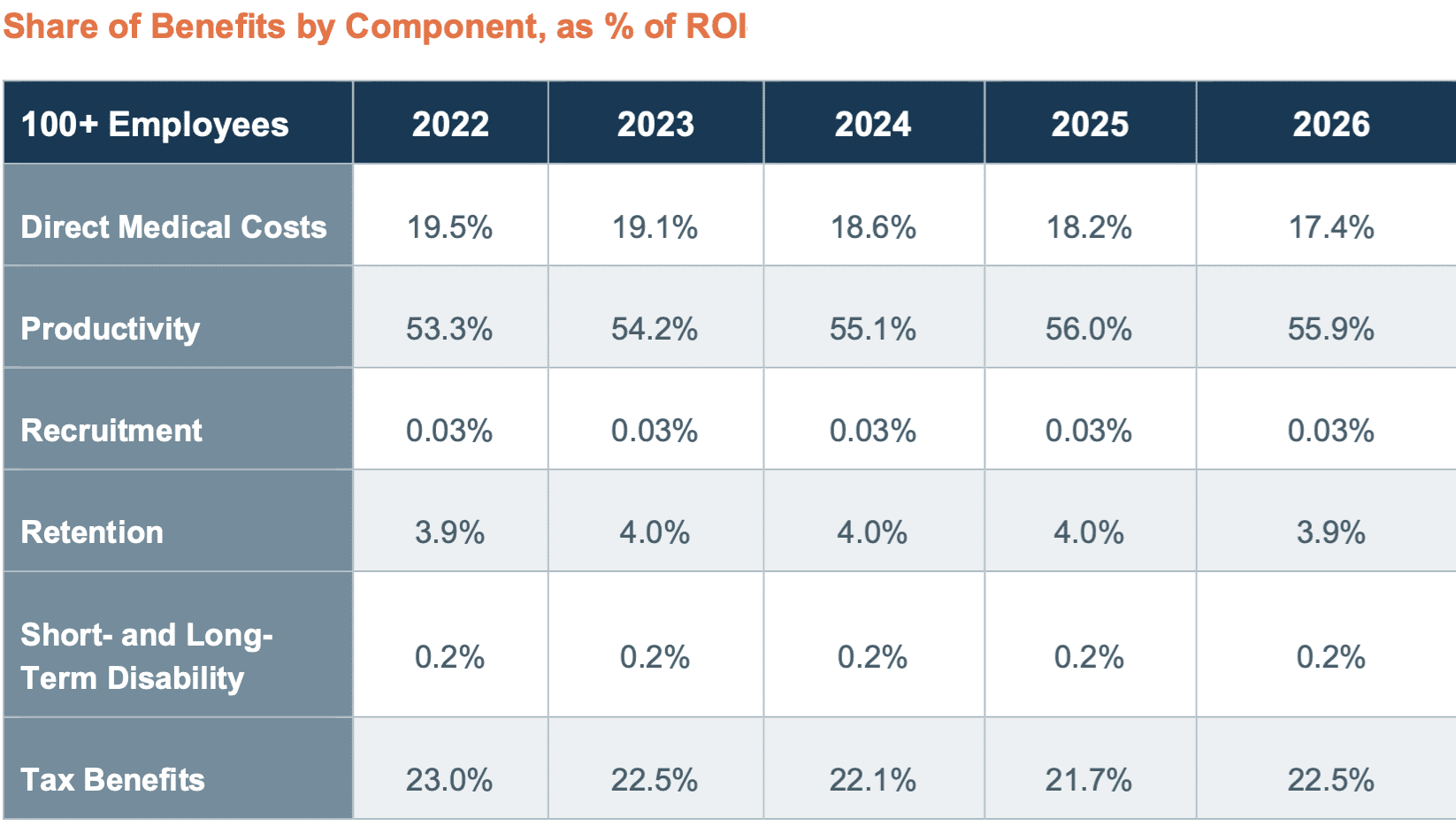

Health insurance is expensive, and we’ve all asked ourselves, “Is it really worth what I am paying?”. For employer-sponsored health insurance, the answer is a resounding YES it is. For every dollar employers spent on health insurance-related costs, they get back $1.47 according to a newstudy from Avalere Health. This figure in fact is expected to grow to 52% by 2026 from 47%.

The U.S. Chamber of Commerce commissioned the Avalere Health employer study that used publicly available data from the Bureau of Labor Statistics and the Congressional Budget Office to estimate the return on investment employer-sponsored health insurance provides employers with 100 or more employees. Improved employee productivity, reduced direct medical costs, and tax benefits were the primary aspects that generated benefits for employer-sponsored health plans. Employers who offered employer-sponsored health coverage and wellness programs had healthier employees and spent less on direct medical costs, Avalare found.

The Numbers

Employee productivity reflects the reductions in absenteeism and lost productivity after receiving employer-sponsored coverage. These productivity increases contributed an estimated $275.6 billion in employer benefits in 2022, or 53.3% of all benefits. By 2026, this is expected to rise to $346.6 billion or 55.9 percent of total ROI.

ROI of some of these key components includes $275.6 billion from improved productivity in 2022 and $346.6 billion in 2026, $101 billion from a reduction in direct medical costs in 2022 and $108 billion in 2026, and $119.2 billion or a 23% ROI from tax benefits in 2022 and $139.7 billion in 2026.

Employer-Sponsored Insurance(ESI) offerings can positively influence prospective employees’ decisions to join firms, reducing employer recruitment and vacancy costs. The study’s model assumes that 9% of individuals decide to accept a certain position based on ESI. The analysis estimates that firms with 100 or more employees derived $141M in employer benefits in 2022, growing to $167M in 2026.

Similarly, ESI positively affects the retention of employees. Avalere’s analysis estimates $20.3B in employer benefits from improved retention in 2022 and $24.3B in 2026.

Conclusion

The study finds that industries where firms generally made greater investments in ESI tended to result in larger ROI. Also, since costs associated with turnover and recruitment are positively associated with wages, Avalere estimates higher ROI in higher-wage industries. On the flip side of that same coin, lower ROI was associated with industries that typically have a lower investment in ESI and wellness programs, lower wages, and lower employee participation in ESI and wellness programs.

The full report including the methodology can be found here.

For more information on how Employer-Sponsored Insurance and a PEO can make difference for your small business please contact us at info@360peo.com or 855-667-4621.

How High Deductible Health Plans Can Set Employees Up for Financial Success

Overview

A common fear among employees can be that High Deductible Health Plans (HDHPs) expose them to too much risk. However, this misconception misses the near-certain long-term losses that come with not choosing a HDHP that includes an HSA. What employees are often missing is a full knowledge of the long-term financial impacts and risks associated with enrolling in an HDHP paired with HSA savings strategy, compared to a more traditional, low deductible PPO option. Employer contributions to HSAs can also set employees up for financial success and retirement readiness.

More Info

Join this complimentary webcast to discover how HSA-eligible plans are better for employees in the long run and can help improve their financial health. Topics discussed will include:

The short term risks that scare employees away from an HSA plan

The long term benefits that make HSAs a no-brainer

Ways to overcome employees’ apprehension towards HSAs to get them to enroll and contribute

And more…

Date: Wednesday, June 15 2022

Time: 2:00 p.m. ET

Cost: Complimentary

Day(s)

:

Hour(s)

:

Minute(s)

:

Second(s)

Samuel Kina, Ph.D. | Chief Analytics Officer | Picwell, Inc.

Bio

Samuel Kina, Ph.D. is the Chief Analytics Officer at Picwell, Inc. where he has led the company’s work in economic and predictive modeling since 2014, shortly after the company was founded. He has a wide range of experience in health policy and economics in the public, private, and non-profit sectors. He has advised several state and private health insurance exchanges, and he has provided economic and strategic support to several pharmaceutical manufacturers, health insurance companies, regulatory agencies, and Congress in matters related to health policy, intellectual property, antitrust regulation and FDA regulation and drug approval. Sam has taught courses in statistics, economics, and health policy, and his research has focused on the economics of the health insurance and pharmaceutical industries.

Prior to joining Picwell, he held positions at the Analysis Group, Congressional Budget Office, and the Alliance for Health Reform. Sam has a BA in Public Policy Analysis and Economics from Pomona College and a Ph.D. in Health Policy and Economics from Harvard University.

REGISTER NOW! (Not able to attend? We recommend you STILL REGISTER – you will receive an email with how to access the recording of the event)

Join Our Newsletter

Subscribe for news & resources about scaling your business

The IRS has released the 2023 Health Savings Account (HSA) inflation adjustments. To be eligible to make HSA contributions, an individual must be covered under a high deductible health plan (HDHP) and meet certain other eligibility requirements.

New HSA 2023 limits are as follows:

2023

2022

HSA Annual Contribution Limit

$3,850; $7,750

$3,650 – Single; $7,300 – Family

HDHP Minimum Annual Deductible

$1,500; $3,000

$1,400 – Single; $2,800 – Family

HDHP Out-of-Pocket Maximum

$7,500; $15,000

$7,050 – Single; $14,100 – Family

Age 55+ Catch-Up Provision

$1,000; $2,000

$1,000- Single; $2,000 – Husband/Wife

Age 55 Catch Up Contribution

As in 401k and IRA contributions, you are allowed to contribute extra if you are above a certain age. If you are age 55 or older by the end of the year, you can contribute an additional $1,000 to your HSA. If you are married, and both of you are age 55, each of you can contribute an additional $1,000. A savvy strategy for high-income earners is to invest the money in your HSA for the long haul. Once you’re 65, you can take out tax-free distributions to cover Medicare premiums. If you withdraw money at that point for non-medical uses, you pay the same tax as you would on withdrawals from a pretax 401(k). But you can also take money out tax-free to reimburse yourself for prior years’ out-of-pocket medical expenses if you have the old receipts.

COVId-19 Update:

You can even use an HSA to save on a typical trip to the CVS. Thanks to a tax relief provision tucked in the last Covid-19 stimulus package, you can use the money you stash in an HSA or FSA (more on those later) for over-the-counter medications like Tylenol or Flonase as well as menstrual products like tampons and pads. That reverses Obamacare restrictions on OTC meds requiring a doctor’s prescription for them to be eligible for reimbursement.

HSA/HDHP Market Growth

HSA holders own the assets in the accounts and can build up substantial sums over time. Enrollment in HSA-compatible insurance plans has increased to 10 million earlier this year, from 1 million in March 2005, according to, America’s Health Insurance Plans (AHIP), a trade group.

HSAs were authorized starting in January 2004. Since then, AHIP has conducted a periodic census of health plans participating in the HSA/HDHP market.

The number of people with HSA/HDHP coverage rose to more than 11.4 in January 2011, up from 10.0 million in January 2010, 8.0 million in January 2009, and 6.1 million in January 2008.

30 percent of individuals covered by an HSA plan were in the small group market, 50 percent were in the large-group market, and the remaining 20 percent were in the individual market.

14% of all workers in the private sector have access to a Health Savings Account acc. to the Bureau of Labor Statistics.

States with the highest levels of HSA/HDHP enrollment were California, Ohio, Florida, Texas, Illinois, and Minnesota.

HSA Advantages:

Opportunity to build savings – Unused money stays in your account from year to year and earns tax-free interest. The HSA also gives you an investment opportunity.

Tax-free contributions and earnings – You don’t pay taxes on contributions or earnings.

Tax-Free Money allowed for non-traditional Medical coverage– As per IRS Publication 502, unused money can be used for dental, vision, Lasik eye surgery, acupuncture, yoga, infertility, etc. Popular Examples

Portability – The funds belong to you, so you keep the funds if you change jobs or retire.

Our overall experience with HSAs has been positive when employer funding is at a minimum 50% using either the HSA or an HRA (Health Reimbursement Account-employer keeps unspent money). Traditional plans trend of higher copays and new in-network deductibles has also led to the popularity of an HSA.

Next Steps

Plan sponsors should update payroll and plan administration systems for the 2022 cost-of-living adjustments and should incorporate the new limits in relevant participant communications, such as open enrollment and communication materials, plan documents, and summary plan descriptions.

Is your HSA compliant? Which pre-tax qualified HSA, FSA, HRA spending card is right for you? Please contact our team at 360PEO (855)667-4621 for immediate answers. Stay tuned for updates as more information gets released. Sign up for the latest news updates.

Effective April 1, 2022, high-deductible health plans can once again offer first-dollar coverage for Telehealth and other remote services without making participants ineligible for health savings account (“HSA”) contributions. The relief runs only through the end of 2022. This relief allows individuals with High Deductible Health Plans (“HDHPs”) to receive free telehealth services prior to the satisfaction of their minimum deductible and remain eligible to make Health Savings Account (“HSA”) contributions.

Background

Individuals may contribute to an HSA if they are covered by a qualifying HDHP and do not have other disqualifying coverage. Generally, telehealth or other remote health care services are considered other health care coverage that, if provided before satisfaction of the required deductible, may be disqualifying for purposes of contributing to an HSA.

The Coronavirus Aid, Relief, and Economic Security Act (the “CARES Act”) were signed into law on March 27, 2020. Among other things, the CARES Act offered temporary relief related to telehealth and other remote care services when offered with an HDHP and HSA. Specifically, for plan years beginning on or before December 31, 2021, telehealth and other remote care services could be offered before satisfaction of the deductible without jeopardizing an individual’s eligibility to contribute to an HSA.

Employer Action

Employers offering HDHPs with HSAs should consider whether to re-implement (or continue) free telehealth as part of a benefit offering. Employers with calendar year plans may

have already re-introduced a cost associated with telehealth for HDHP/HSA participants once the CARES Act relief expired and should consider whether to waive those costs again given the temporary nature of this relief. Additionally, employers with non-calendar year plans should consider the administrative and communication burdens that may be imposed by providing relief that may expire prior to the end of the current plan year.

It is important that employers review these changes with their carriers, Third Party Administrators and telehealth vendors to understand their approach and communicate any changes with participants.

Learn more about how we are successfully helping navigate SMB for 20+ years. If you have any questions or would like additional information, please contact us at 855-667-4621 or info@360peo.com.

We already love Professional Employer Organization (PEO)– our clients do too. Today we’re counting down our top 5 reasons why we love PEO:

1.National Capabilities:

It ensures your compliance with local and federal laws, even if your business has locations in different states. Access to a national provider healthcare plan, not single state carriers

2. Liability Protections:

Some liability moves to the PEO service instead of your company.

3. It saves you money on HR staff.

Being part of a PEO gives you a clear cut idea of what your costs are going to be year in and year out. The PEOs work tirelessly to keep their insurance renewals down, so their clients won’t leave. Every year they work with the insurance carriers to introduce new plans and ways to reduce the costs of insurance to their clients. This gives you the ability to forecast and know precisely what your costs will be.

4. Technologies:

Online HR resources for self service issues Ability for employees to make personal changes on their own, online. Ability to track PTO (paid-time off).

5. One Vendor:

It streamlines HR tasks like payroll, taxes, employee benefits, worker’s compensation, 401K and HR administrative tasks.

Our PEO Quoting Tool ensures that we have first-hand insight as to what the small business owner needs to be successful. Click below for quote.

Free At-Home COVID-19 Test available via USPS. On Jan. 18, every home in the United States can order up to four free COVID-19 tests. January 19, Americans will be able to order free at-home rapid COVID tests from the government at COVIDTests.gov.

The federal guidance requires commercial insurers and group health plans (both fully insured and self-insured) to reimburse consumers for the cost of Over-the-Counter (OTC) COVID-19 diagnostic tests, with or without an order or clinical assessment by a healthcare provider.

Types of COVID Tests:

Antigen tests, which test for an active infection by detecting specific virus proteins. Most at-home tests and “rapid tests” performed by healthcare providers fall in this category.

Molecular tests, which test for an active infection by amplifying genetic material from the virus. These are considered the “gold standard” for diagnosing COVID, as they are generally more accurate than antigen tests. The most familiar test from this category is the polymerase chain reaction (or PCR) test, which requires lab processing.

Antibody tests, which are blood tests that determine if the body has had an immune response to the virus. These tests are not used for diagnosing an active infection.

How Will this work with your Insurer?

Consistent with the guidance Insurers will utilize existing member claims submission procedures to provide benefits without cost-share for OTC COVID-19 tests that members purchase, either online or through other retailers. In addition to the member demographic information that is normally filed with member-submitted claims, the members will be required to certify that the test was purchased for personal use and not for employment purposes.

Customers may receive reimbursement for up to 8 COVID-19 OTC tests per covered individual per calendar month without a health care provider prescription or individualized clinical assessment. For a family of four covered individuals, that equates to 32 tests per month.

Members with Empire Blue Cross, for example, will utilize A.I. apps such as Sydney App or online. Separately, Insurers such as UnitedHealthcare will initially offer for at-home COVID-19 tests are Walmart Pharmacy and Rite Aid Pharmacy. When using Walmart or Rite-Aid there will be no up-front cost and you will not have to submit a form for reimbursement. Note, you may be required to go to the pharmacy counter to obtain the test kits at no cost.

If you’re interested in hearing more about the advantages of partnering with a PEO, we’d love to talk to you. Fill out the form below or email info@medicalsolutionscorp.com for a FREE Consultation Today!

The information provided on this website is intended for informational purposes only. Millennium Medical Solutions Corp. does not offer legal or medical guidance. Those with legal or medical questions should seek appropriate assistance from a licensed professional. Stay up to date by signing up for Newsletter and Coronavirus Dashboard below.

You can get ahead of cold and flu season by embracing a few habits that can help support a healthy immune system.

Plus, boosting your natural immunity doesn’t have to be time-consuming or expensive.

You may be doing some of these things already. If not, take baby steps to build new habits, because trying to do too much too soon may lead to frustration.

What steps can you take to fit these five tips into your life?

1. Get a good night’s rest.

Like stress, sleep deprivation can reduce the effectiveness of your immune system and lead to a longer recovery time if you do get sick.

Practice good sleep habits like putting away your devices before bed and creating a wind-down routine to help you relax.

2. Watch your stress levels.

Stress can weaken your immune system, making it harder to fight off a cold or the flu. Try practicing stress-reduction techniques such as daily meditation or breathing exercises.

3. Keep your hands clean.

Wash your hands often, especially when entering or leaving public places or touching surfaces. Cleaning your hands with soap and water for at least 20 seconds can be the best way to remove germs. When that’s not possible, use a hand sanitizer with at least 60% alcohol.

4. Stay active.

Exercise can help alleviate stress and support your immune system — and physical activity doesn’t have to be intense to make a difference. To get started, you can try taking a daily walk or practicing gentle yoga poses.

5. Focus more on nutrition.

A healthy diet supports a healthy immune system. In addition to the supplements, you may already take, try to eat foods rich in vitamins and minerals, such as:

Citrus fruits

Spinach

Green tea

Shellfish

Cleveland Clinic: We’re now several months into the coronavirus pandemic, and we’re also fast-approaching peak season for yet another viral illness: influenza. Infectious disease specialist Kristin Englund, MD, explains the differences between COVID-19 and the flu, and shares steps we can all take to help us stay healthy this flu season.

For information about transparency providers and new tech tools contact us at info@medicalsolutionscorp.com or (855)667-4621.

sCMS and OSHA released interim final rules this week detailing the implementation of national vaccine requirements established by President Biden’s executive order in September.Yesterday, the Department of Labor released an unpublished version of the OSHA Emergency Temporary Standard (ETS).

The ETS is effective immediately and will cover 2/3rds of private employers. The OSHA ETS puts into effect the Biden Executive Order mandating all private employers with 100 or more employees ensure their employees are vaccinated against COVID-19, or submit negative weekly tests.

KEY Summary:

Covered Employers

Private employers with 100 or more employees enterprise-wide (across US locations) at the time these rules become effective

Independent contractors not included

Special franchisee, construction and staffing agency rules

Companies who grow will move into the covered group

State/local governments, including schools

Only state/local ordinances/laws that are not conflicting will have effect (i.e., if the state law prohibits vaccine mandates, OSHA ETS will supersede state law. OSHA ETS will be mandated.)

States with state OSHA plans may adopt these federal rules or similar rules. Some states are threatened with removal of state plan authority for failure to comply with laws as stringent as federal (e.g., UT & AZ)

Compliance Deadline

Within 30 days of publication (December 5)

Testing requirements within 60 days (January 4)

Mandate

Determine vaccination status of each employee

Obtain acceptable proof –

Maintain records/roster

Unvaccinated must test negative weekly if worker in workplace at least once a week or within 7 days before returning to work if worker is away from workplace a week or longer

Must wear face covering indoors or in occupied vehicle for work

Employer not required to pay for testing unless required by law or collective bargaining agreement

Employer not required to pay for face coverings

Notice

Employee must promptly notify of positive COVID test or receive diagnosis

Employer must remove employee from workplace, regardless of vaccination status

May not return to work until meeting criteria

Must provide paid time off for vaccination and recovery from side effects

In conclusion, employers subject to the ETS must determine whether they will take a vaccine-only or combined vaccine and testing/face covering approach to compliance and must develop the required written policies and communicate those policies to employees so they have ample time to receive their COVID-19 vaccines. Employers should work with legal counsel to develop their written policies and to address any reasonable accommodation requests received by employees.

If needing employment law assistance in implementing these new rules, contact your World Insurance Associates representative so that they can connect you a Jackson Lewis P.C. council in order to receive the WIA arrangement. For our PEO clients, please speak with in-house council and HR.

The information provided in this alert is not, is not intended to be, and shall not be construed to be, either the provision of legal advice or an offer to provide legal services, nor does it necessarily reflect the opinions of the agency, our lawyers, or our clients. This is not legal advice. Rather, the content is intended as a general overview of the subject matter covered.

Good news Bronx/Westchester. Oxford and Montefiore Health System announced moments ago that they have reached an agreement effective December 1, 2021 for UnitedHealthcare and Oxford employer-sponsored plans, as well as UnitedHealthcare’s Medicare Dual Special Needs Plan.

This resolves a split since Jan 1, 2021 which affected a significant percentage of local residents as both companies have a critical size of the market. Westchester and Bronx populations total nearly 2.5 million people. While this contract is resolved with titanic and a few Hospital Systems and Insurers left in the market we expect to see this trend to continue.

See below the official press release.

UnitedHealthcare and Montefiore Health System Renew Relationship

UnitedHealthcare and Montefiore Health System have reached a multi-year agreement that restores access to Montefiore’s hospitals and physicians for people enrolled in UnitedHealthcare and Oxford employer-sponsored plans as well as UnitedHealthcare’s Medicare Dual Special Needs Plan, effective Dec. 1, 2021.

We recognize that the care Montefiore provides is not only important but also personal to our members and we also know the negotiations process may have been difficult for them. Our top priority throughout this process was ensuring the people and employers we’re honored to serve in New York have access to quality, more affordable health care, and this new agreement helps accomplish that goal.

We thank our members and customers for their support and patience throughout this process. We are honored to continue supporting the more than 3.7 million individuals across New York who depend on us for access to quality and affordable health care.

Montefiore Hospitals & Health System

Facility Name

County

Montefiore Hospital (Moses Campus)

Bronx

Children’s Hospital at Montefiore

Bronx

Garnet Health MedJack D. Weiler Hospital (Einstein Campus)ical Center

Bronx

Montefiore Wakefield Hospital (Wakefield Campus)

Bronx

Burke Rehabilitation Hospital

Westchester

Montefiore Mount Vernon Hospital

Westchester

Montefiore New Rochelle Hospital

Westchester

Montefiore Nyack Hospital

Rockland

Montefiore St Luke’s Cornwall Hospital

Orange

White Plains Hospital

Bronx

Montefiore Hutchinson Campus

Bronx

Montefiore Medical Group

Westchester

Montefiore Medical Specialists of Westchester

Westchester

Neighboring Hospitals

Facility Name

County

Bon Secours Community Hospital BronxCare Hospital Center Garnet Health Medical Center Good Samaritan Hospital of Suffern New York Presbyterian Hudson Valley Hospital New York Presbyterian Lawrence Hospital NYC Health + Hospitals Jacobi NYC Health + Hospitals Lincoln NYC Health + Hospitals North Central Bronx St. Anthony Community Hospital St. Barnabas Hospital St. John’s Riverside Hospital Westchester Medical Center

Medicare Supplemental Plan F phased out for newly Medicare eligible? With the new 2022 open enrollment changes, it’s time to get the facts. Considering making changes to your coverage this fall or just want to learn more about this enrollment period?

During the Medicare open enrollment period – which runs from October 15 through December 7 – you can make a variety of changes (none of which involve medical underwriting):

Switch from Medicare Advantage toOriginal Medicareor vice versa.

Switch from one Medicare Advantage plan to another.

Switch from onePart D prescription planto another.

Join a Medicare Part D plan.

Drop your Part D coverage altogether.

1. Medicare Supplement Plans F and C are still available

While the Centers for Medicare and Medicaid (CMS) will no longer allow newly eligible Medicare beneficiaries to enroll in Medigap plans F and C, these plans aren’t disappearing completely. If you become eligible for Medicare before January 1, 2021 (and that’s everyone who can use the 2021 fall Medicare Open Enrollment Period), you can apply for these plans now and in the future—even if you aren’t already enrolled in Medigap.

If you become eligible for Medicare on or after January 1, 2020, you won’t be able to enroll in Plans F or C now or in the future.

2. The Part D ‘donut hole’ will close

In 2022, you’ll enter the donut hole when your spending + your plan’s spending reaches $4,430. And you leave the donut hole — and enter the catastrophic coverage level — when your spending + manufacturer discounts reach $7,050. Both of these amounts are higher than they were in 2021, and generally increase each year. Learn more about Part D.

3. Changes in Medicare Advantage and Part D plans

Every year, insurers make small changes to their Medicare Advantage and Part D plans. Typically, these changes include changes in premiums, deductibles, and other costs. Keep in mind, the Medicare program may not finalize these changes until right before fall Open Enrollment.

See the latest Medicare premiums and deductibles now or come back in October. We’ll share finalized changes as soon as they become available.

Refresh your general Medicare knowledge

While the Medicare program changes a bit each year, much of it stays the same. It never hurts to refresh your Medicare knowledge. We recommend starting with an Overview of Medicare. This Medicare Glossary could come in handy, too, as you read through insurance documents. See

Medicare Part B premiums increased this year by about 2.7% or $4 per month and high-income surcharges also rose modestly in 2021. For 2022 the Standard Part B premiums are projected to be $158.50/month from $148.50/month in 2021 or a 6.7% increase.

The wealthiest senior couples will be paying more than $12,000 a year in Medicare Part B premiums. Part B (the base and the surcharge) covers doctors’ and outpatient services. Medicare Part B Income-Related Monthly Adjustment Amounts.

5. Part B deductible also increased for 2021, and will increase again in 2022

Medicare B also has a deductible, which increased to$203 in 2021, up from$198 in 2020. For 2022, the Part B deductible isprojected to be $217. The Medicare Part B deductible only has to be paid once per year, unlike the Part A deductible, which has to be paid once perbenefit period.

Do you have to renew your plan?