The employer reporting deadlines are delayed, not deleted! When are the 1095 filing forms due?

Form

Delivered to the Employee

Delivered to the IRS (Paper)

Delivered to the IRS (Electronically)

1095-C

3/2/2017

2/28/2017

3/31/2017

1094-C

N/A

2/28/2017

3/31/2017

What does this mean?

Similar to last year, the IRS is making an accommodation to employers to prepare their forms. The filings are still due to the IRS as per the original deadline. Our HR/Payroll parters are still prepared to help your compliance needs and meet all of the deadlines and reporting burdens.

For a copy of Notice, please click on the link below:

https://www.irs.gov/pub/irs-drop/n-16-70.pdf

Please contact our team for immediate answers on your HR/Payroll/Compliance needs at Millennium Medical Solutions Corp (855)667-4621 for immediate answers.

Note: This delay does not impact the timing of Form 1095 A, Health Insurance Marketplace Statement. 1095 A is the form you receive if you purchase your health insurance through the Marketplace and not through your employe

The 2017 Election Results and ACA is a hot topic creating buzz. With the outcome of the 2016 elections now official, the Republicans will hold the majority in both chambers of Congress and control of the White House beginning in 2017. Our posting CLINTON VS TRUMP ON HEALTHCARE was a general summary of their differences on Healthcare.

Since President-elect Trump ran on a platform of “Replace and Repeal” of the Affordable Care Act (ACA), we anticipate that acting on this campaign promise will be one of the top priorities of the new Trump administration. We anticipate there will be significant disruption for individuals, employers, brokers and carriers across the country.

Republicans will likely need to use the process of Budget Reconciliation to pass legislation through the Senate, given the party did not secure enough seats to control a filibuster-proof supermajority. In other words, the legislation can pass in the Senate with a simple majority vote and not a super majority (which requires 60 votes). Reconciliation can be used to take away some, but not all, of the ACA. It is anticipated that certain provisions of the ACA would be targeted such as Medicaid expansion, the availability of subsidies and premium tax credits in the Marketplace, and the employer and individual mandate. It cannot be used to remove non-budgetary provisions (for example, insurance mandates like “to age 26”). In addition, it is conceivable that a Trump administration may simply direct various federal agencies (such as the Department of Labor) to not enforce certain ACA provisions.

The Republicans have not laid out a specific plan on what will replace the ACA. Generally, the party has supported the existing employer-based system (with some party members calling for limits on the tax exclusion). Based on published white papers on the President-elect Trump’s website, other aspects of a healthcare overhaul plan may include:

Tax credits for purchasing individual health insurance;

Expansion of Health Savings Accounts and HighDeductible Health Plans;

Continuation of the prohibition on pre-existing condition exclusions from health insurance;

High risk pools;

Interstate sales of insurance; andMedical malpractice reform.

The process to repeal and replace the ACA will take time and nothing will happen between now and the New Year. Open enrollment is currently underway in the Marketplaces across the country and it is expected that individual policies (and subsidies for lower and middle-income individuals) will be available to enrollees as of January 1, 2017. What is unknown is whether the Trump administration and subsequent legislation will affect the Marketplace and subsidies in mid-2017 or instead phase out this coverage after the 2017 calendar year.

The employer mandate (for applicable large employers);

Form 1094-C and 1095-C reporting for CalendarYear 2016;

Any ACA taxes and fees for self-funded plans to pay directly (such as reinsurance fees); and

Plan design changes applicable to plan years thatbegin on or after January 1, 2017.

In addition, all other federal law mandates impacting employer health and welfare plans such as ERISA,HIPAA, COBRA, Code Section 125, the Mental Health Parity and Addiction Equity Act, and the Service Contract Act / Davis Bacon and Related Acts are still good law. There has been no indication that these non-ACA laws are targeted for repeal or replacement.

Stay tuned for updates as more information gets released. Sign up for latest news updates. Please contact our team on your 2017 health plan renewal at Millennium Medical Solutions Corp (855)667-4621 for immediate answers.

In yesterday’s surprise announcement, NJ regulators will be shutting down Health republic NJ for 2017 “because of its hazardous financial condition”. This marks the demise of the second Metro area healthcare co-op with the same name-sake Health Republic but different managed healthcare co-op, see Health Republic NY Shutting Down Nov 30.

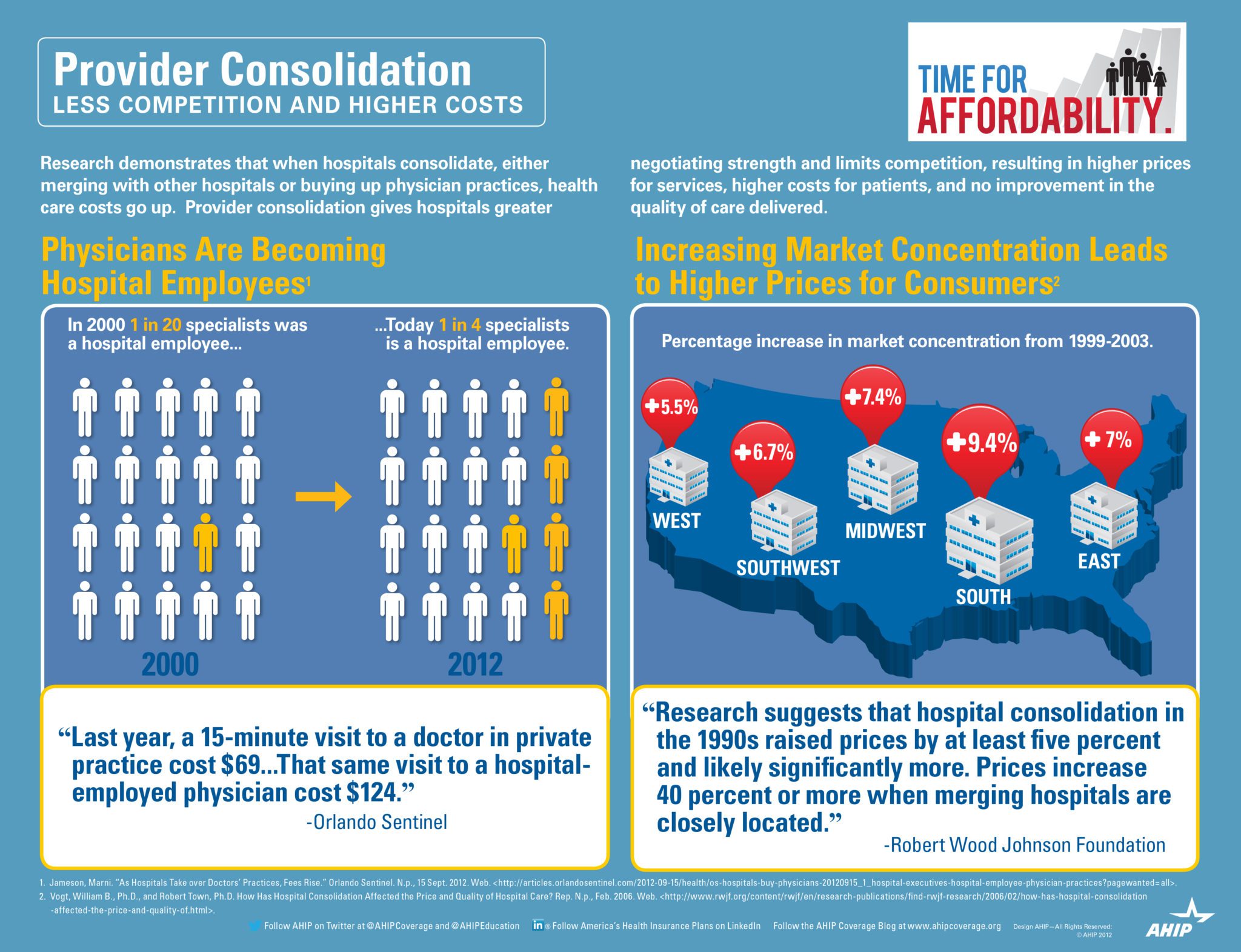

Since Obamacare’s rollout in the fall of 2013, 16 co-ops that launched with money from the federal government have collapsed. Now, just six co-ops—Wisconsin’s Common Ground Healthcare Cooperative; Maryland’s Evergreen Health Cooperative; Maine Community Health Options; Massachusetts’ Minuteman Health; Montana Health Cooperative; and New Mexico Health Connections—remain.

In a bizarre twist of fate or unintended Affordable Care Act design flaw small affordable startups not only have to gain new client footholds but also support large established companies “with sicker patients”. Start-ups, by contrast, with much lower rate of diagnosed sick patients essentially pay into this tax. This tax is part of the risk adjustment program intended to stabilize Insurers who took on sicker patients and spread this risk. While some correctly blame too low pricing and some miscalculated business decision-making the inherent extra tax doomed the majority of the original 16 co-ops.

Health Republic in fact grew steadily and made money the first 9 months of 2015. However, HRNJ lost 17.6 million end of 2015 and is choking off at this $46.3 million payment to the government through the risk adjustment program. This is considered one of the 3 R’s of the reinsurance program – risk corridor, reinsurance and risk adjustment that were intended to level the playing field. The first “R”—“reinsurance”—subsidizes insurers that attract individual customers who rack up particularly high medical bills. The second—“risk adjustment”—requires insurers with low-cost patients to make payments to plans that share the benefits with those who insured higher-cost ones. And the third, called “risk corridors,” is a program to subsidize health plans whose total medical expenses for all their Obamacare customers overshoot a target amount.

The co-ops received less money than they initially anticipated last year under Obamacare’s risk corridor program, which resulted in the collapse of at least five co-ops and a $5 billion class action lawsuit filed by 6 state’s co-ops – ” Oregon-based insurer Moda Health Plan Inc., Blue Cross Blue Shield of North Carolina, Pittsburgh-based Highmark Inc., and the failed CoOportunity Health, which was based in West Des Moines, Iowa, and Health Republic Insurance Co. of Oregon, which was based in Lake Oswego.”

“The risk corridor program, however, has been an unmitigated debacle. In December 2014, the Republican Congress voted to prohibit the Obama administration from spending any money on the program, decrying it as a bailout for the insurance companies. Sen. Marco Rubio, then thought to be a leading GOP presidential contender for 2016, was particularly vocal in pillorying the program.

Unlike all those symbolic “repeal Obamacare” votes, Congress actually succeeded in blocking those risk corridor payments, and it hit Obamacare hard. Insurers filed claims seeking $2.9 billion, but under the limits imposed by the GOP there was less than $400 million available to make good on those payments. The end result: insurers initially received only 12.6 cents for each dollar they had counted on. Many of the new Obamacare co-op plans that went out of business blamed their collapse in part on the fact that they’d been counting on the full payments to keep them solvent.”

Regrettably, in a Presidential year no one wants to touch this burning hot potato. Perhaps NJ’s handling of this pressure cooker and taking 2017 off may be the best course of action after all.

9/16/16 Addendum:

As of Monday, September 19, 2016, the portal for Health Republic Insurance will be shut down, as they are no longer accepting new business for the year.

The New Jersey State Department of Banking and Insurance has also provided a list of FAQs related to the shutdown and how it affects individuals, small employers, brokers and providers. For more information, click here.

As always, our team is here to assist you and to help you grow your business.

Clinton vs Trump Healthcare. A helpful overview from SHRM on the differences between the Candidates. They presumably agree on repealing the Cadillac Tax and well-needed price transparencies.

HILLARY CLINTON’S HEALTH CARE REFORM PLAN:

Defend the Affordable Care Act. Clinton will continue to defend the ACA against Republican efforts to repeal it.

Lower out-of-pocket costs like copays and deductibles. The average deductible for employer-sponsored health plans rose from $1,240 in 2002 to about $2,500 in 2013. Clinton believes that workers should share in slower growth of national health care spending through lower costs.

Reduce the cost of prescription drugs. Prescription drug spending accelerated from 2.5 percent in 2013 to 12.6 percent in 2014. It’s no wonder that almost three-quarters of Americans believe prescription drug costs are unreasonable. Clinton believes we need to demand lower drug costs for hardworking families and seniors.

Build on the Affordable Care Act and require plans to provide three sick visits without counting toward deductibles every year. The Affordable Care Act required nearly all plans to offer many preventive services, such as blood pressure screening and vaccines, with no cost-sharing at all. But because average deductibles have more than doubled over the past decade, many Americans would have to pay a significant cost out-of-pocket toward their deductible if they get sick and need to see a doctor. Clinton’s plan will build on the Affordable Care Act by requiring insurers and employers to provide up to three sick visits to a doctor per year without needing to meet the plan’s deductible first.

Provide a new, progressive refundable tax credit of up to $5,000 per family for excessive out-of-pocket costs. For families that still struggle with prescription drug costs even after out-of-pocket limits on drug spending and free primary care visits, Clinton’s plan will provide progressive, targeted new relief. Americans with health coverage will be eligible for a new refundable tax credit of up to $2,500 for an individual, or $5,000 for a family, available to those with substantial out-of-pocket health care costs. The credit will be available to insured Americans with qualifying out-of-pocket health expenses in excess of five percent of their income, and who are not eligible for Medicare or claiming existing deductions for medical costs. This refundable, progressive credit will help middle-class Americans who may not benefit as much from currently-available deductions for medical expenses. This tax cut will be fully paid for by demanding rebates from drug manufacturers and asking the most fortunate to pay their fair share.

Enforce and Broaden the ACA’s Transparency Provisions. Americans deserve real-time, updated, and reliable information to guide them in selecting a health plan, navigating changes to their out-of-pocket costs in their existing plan, choosing a doctor, and determining how much they will need to pay for a prescription drug. Clinton’s plan will vigorously enforce existing law under the Affordable Care Act and adopt further steps to make sure that employers, providers, and insurers provide this information through clear and accessible forms of communication so that Americans can make informed choices about their coverage and realize meaningful savings.

Repeal ACA -Modify existing law that inhibits the sale of health insurance across state lines. As long as the plan purchased complies with state requirements, any vendor ought to be able to offer insurance in any state. By allowing full competition in this market, insurance costs will go down and consumer satisfaction will go up.

Tax deductible health insurance premium payments. Allow individuals to fully deduct health insurance premium payments from their tax returns under the current tax system. -Allow individuals to use Health Savings Accounts (HSAs). Contributions into HSAs should be tax-free and should be allowed to accumulate. These accounts would become part of the estate of the individual and could be passed on to heirs without fear of any death penalty. These plans should be particularly attractive to young people who are healthy and can afford high-deductible insurance plans. These funds can be used by any member of a family without penalty. The flexibility and security provided by HSAs will be of great benefit to all who participate.

Price transparency. Require price transparency from all healthcare providers, especially doctors and healthcare organizations like clinics and hospitals. Individuals should be able to shop to find the best prices for procedures, exams or any other medical-related procedure.

Reform mental health programs. Families, without the ability to get the information needed to help those who are ailing, are too often not given the tools to help their loved ones. There are promising reforms being developed in Congress that should receive bi-partisan support.

Block-grant Medicaid to the states. Nearly every state already offers benefits beyond what is required in the current Medicaid structure. The state governments know their people best and can manage the administration of Medicaid far better without federal overhead. States will have the incentives to seek out and eliminate fraud, waste and abuse to preserve our precious resources.

Remove barriers to entry into free markets for drug providers that offer safe, reliable and cheaper products. Though the pharmaceutical industry is in the private sector, drug companies provide a public service. Allowing consumers access to imported, safe and dependable drugs from overseas will bring more options to consumers.

Add our blog & sign up for newsletter on latest in Healthcare Reform News. Please contact us for a free evaluation on your group’s benefits at 855-667-4621.

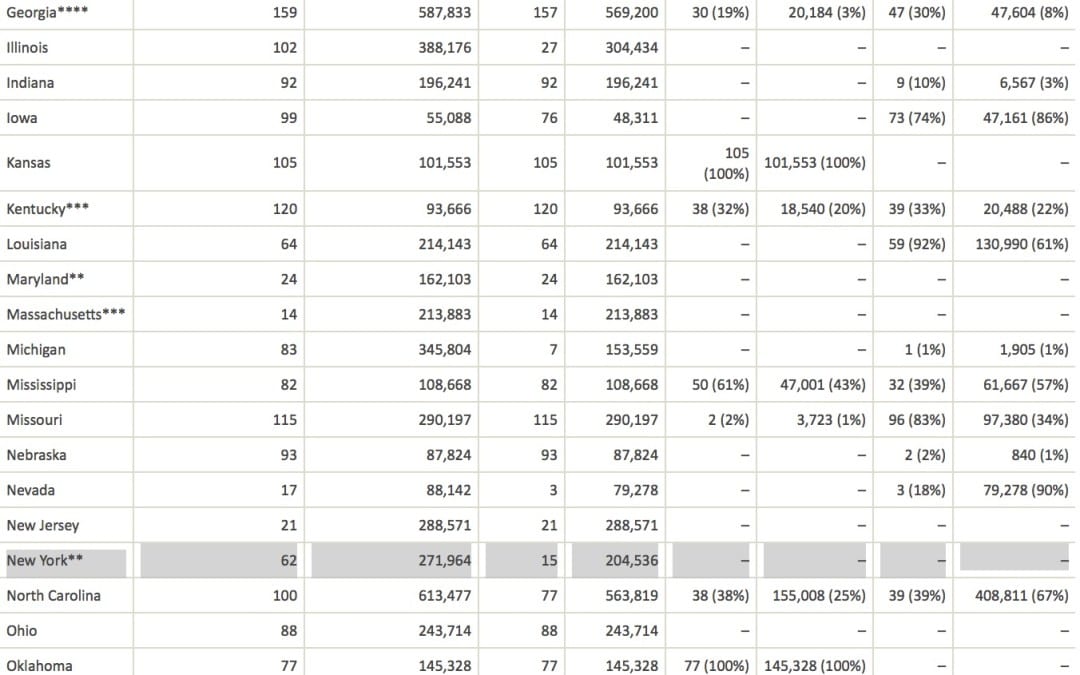

So far, New York and Nevada have confirmed that UnitedHealth plans to remain on their ACA exchanges next year. The company has also filed plans to participate in Virginia for 2017. Wisconsin said it hasn’t received an exit notice from UnitedHealth, and that it doesn’t comment on insurers’ business plans. A representative of Covered California, the state’s Obamacare exchange, said plan participation is confidential until it’s announced later this year.

UnitedHealthcare will drop out of most ACA Exchanges by 2017 as reported in Modern Healthcare. Just how significant is this to the market? Realistically, United took a cautious wait and see approach. In NYS, for example, they have been the most expensive plan on the Obamacare Exchange Marketplace. They expect to lose over a billion dollars in this space for 2015 and 2016, so to them it makes no sense to stay in that market. The concern for the individual market is to expect large pricing increases in 2017 to reflect the higher risk than the safer Group Market.

UnitedHealth, which had about 795,000 ACA customers as of March 31, warned in November that it was posting losses on ACA policies. In December, the company said it should have stayed out of the individual exchange market longer. UnitedHealth also is withdrawing from some related state insurance markets for small businesses.

See United-healthcare Individual members enrolled by State:

UnitedHealthcare will drop ACA exchanges

MODERN HEALTHCARE By Bob Herman April 19, 2016

UnitedHealth Group CEO Stephen Hemsley said Tuesday the health insurance and services conglomerate will pull out of most of its Affordable Care Act marketplaces. But the company won’t bail on the exchanges completely and will sell individual plans in a “handful” of states.

“We cannot broadly serve it on an effective and sustained basis,” Hemsley told analysts and investors on a conference call. UnitedHealth has fully or partially exited five states so far—Arkansas, Georgia, Louisiana, Michigan and Oklahoma, according to various news reports.

The company sold plans in 34 states for this policy year and did not disclose which states it will stay in. Insurers that sell plans through the federal HealthCare.gov portal have until May 11 to file rates for 2017 plans.

A new analysis from the Kaiser Family Foundation, however, notes that UnitedHealth’s exits would only have a modest effect on competition and prices nationally since it has a small ACA footprint and charged higher premiums from the outset.

UnitedHealth recorded an additional $125 million loss on its individual ACA plans, meaning the company’s total ACA losses for 2015 and 2016 will exceed $1 billion. UnitedHealth signed up many sicker-than-expected members, ending the first quarter with 795,000 public exchange enrollees, which is only a fraction of the ACA’s individual market.

The insurer also overpriced its plans in 2015 after barely participating on the exchanges in 2014. UnitedHealth expects its exchange membership will decline to 650,000 by the end of the year.

But despite those heavy losses, which UnitedHealth previewed late last year, the company’s other lines of business like Medicare Advantage and Optum have been making money at a healthy clip. UnitedHealth’s profit climbed 14% year over year, totaling $1.6 billion in the first three months of this year. Adjusted earnings per share rose 17% to $1.81, beating estimates on Wall Street.

Revenue soared almost 25% to $44.5 billion in the first quarter, putting UnitedHealth on pace to hit $182 billion of revenue for the year. The Minnetonka, Minn.-based company recorded double-digit revenue growth across every major segment, including employer, Medicaid, Medicare Advantage and its Optum health services business. UnitedHealth now covers the medical care of nearly 47.7 million Americans.

UnitedHealth’s medical-loss ratio, which shows how much of its premium dollars were spent on medical care or “quality improvement” programs, was 81.7% in the quarter. That was up slightly from the 81.4% posted in the same quarter last year, which UnitedHealth attributed to the leap day.

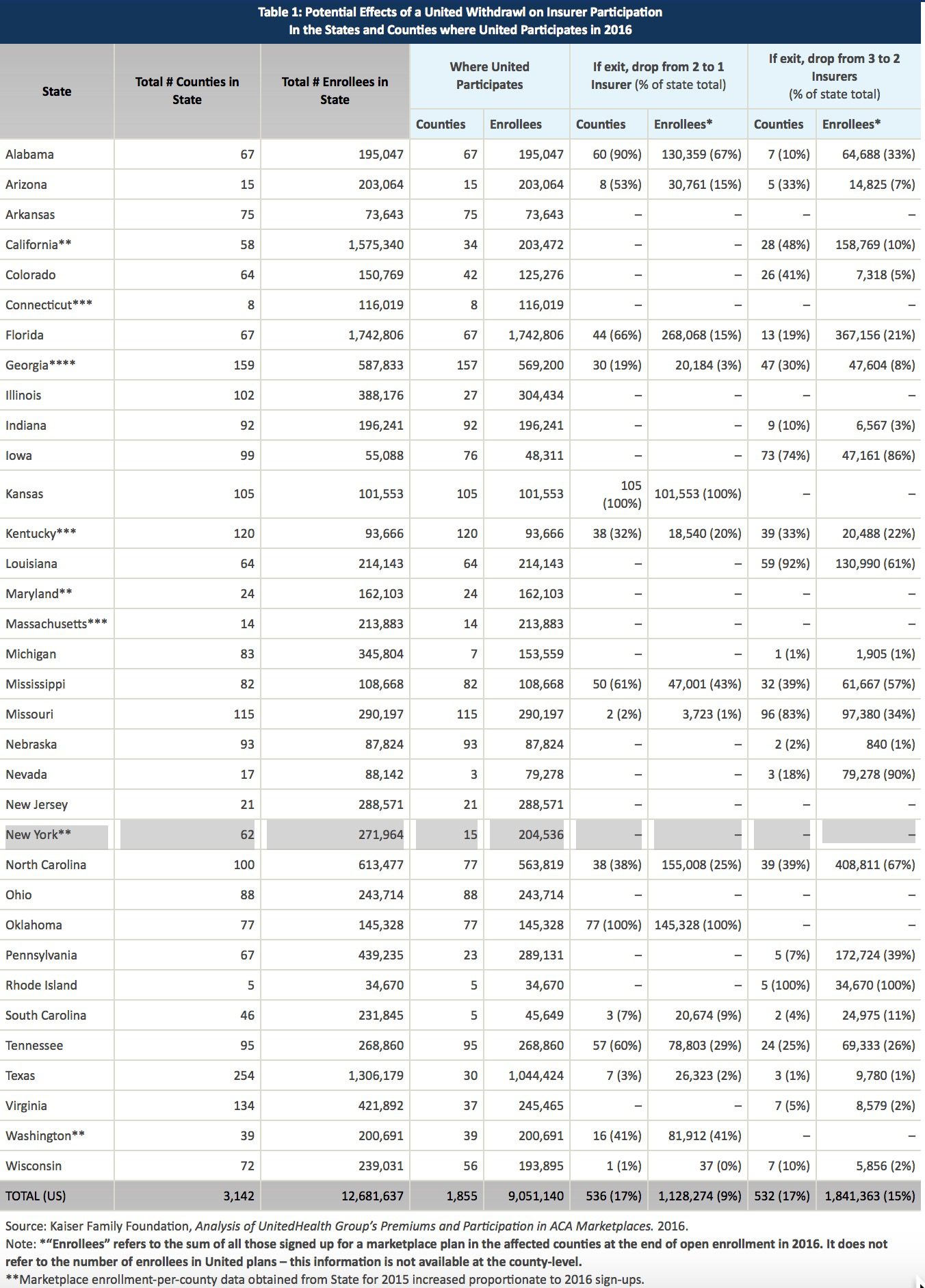

Insurance mergers aka Mergersurance Mania continues at a steady pace with April 2016 Florida’s approval of Anthem Blue Cross and CIGNA merger. This is one month after Florida approved the Aetna and Humana merger. Investors have given their blessings to be sure while 10 States have also given approval. The Anthem Cigna $54 billion merger leaves only three national major providers of health care. Worries remain about the potential effect on consumers and the rising cost of health care.

Health Insurers consolidation argument are that they need to be able to merge in order to absorb added costs and blunted profit margins under the Affordable Care Act. Additionally, medical groups and hospitals groups have merged themselves rapidly giving them negotiation cost controls. This has traditionally been trending in smaller regional markets but are now also felt in major US Cities.

Evidence indeed is pointing to expected large insurance increases due to overwhelming market domination by hospitals. While Doctors and AMA are rightfully concerned about Insurer mergers the vast majority are now working for a Hospital System or Medical IPA.

Without public outcry there seems to be lax Regulator oversight and the arms race should not come as a surprise. On the local level we have yet to see a recent example of hospital merger that was curtailed.

This goes well beyond political partisanship. In a tight Presidential race it is important to understand that whether or not one supports a Single Payer we all suffer. This is bad for consumers, providers and tax payer all around. In an Oligopoly health care system with lack of competition the U.S. tax payers are also stuck with inflated costs.

established companies “with sicker patients”. Start-ups, by contrast, with much lower rate of diagnosed sick patients essentially pay into this tax. This tax is part of the risk adjustment program intended to stabilize Insurers who took on sicker patients and spread this risk. While some correctly blame too low pricing and some miscalculated business decision-making the inherent extra tax doomed the majority of the original 16 co-ops.

established companies “with sicker patients”. Start-ups, by contrast, with much lower rate of diagnosed sick patients essentially pay into this tax. This tax is part of the risk adjustment program intended to stabilize Insurers who took on sicker patients and spread this risk. While some correctly blame too low pricing and some miscalculated business decision-making the inherent extra tax doomed the majority of the original 16 co-ops.