The IRS & SSA announced the 2021 dollar limits for various benefits and compensation levels for retirement plans and IRAs. There are incremental changes but nonetheless worth bookmarking.

The contributions and retirement benefits for qualified retirement plans and individuals. Retirement Arrangements (IRAs) are subject to certain limits that are adjusted by the Secretary of the Treasury annually subject to cost-of-living.Highlightedbelow are the various 2020 and 2021 limits that impact IRA and retirement plans.

The limit on contributions to a traditional. or Roth IRA will remain unchanged in 2021 at $6,000. The limit that applies to IRA catch-up contributions (contributions for individuals age 50 and older) remains at $1,000.

Social Security

The Social. Security Administration (SSA) announced an increase in the taxable wage base (TWB) for 2021 to $142,800 (was $137,700 in 2020). Workers pay Social. Security tax on wages up to the TWB and some retirement plans use the TWB when allocating contributions or calculating benefits.

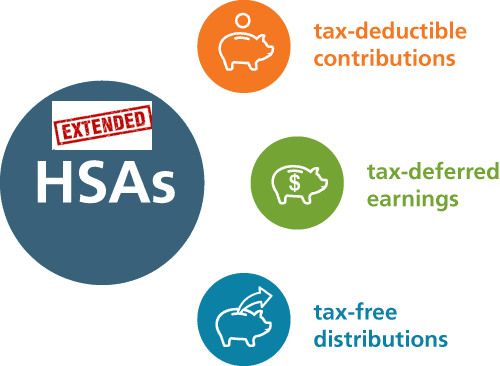

Although not a formal. retirement plan, health savings accounts (HSA) often factor into retirement savings. The IRS announced the following 2021 limits. These apply to individuals under a high-deductible-health-plan (HDHP). The minimum deductibles and maximum out-of-pocket expenses the IRS uses to define HDHPs are outlined below, as well.

Is your HSA compliant? Which pre-tax qualified HSA, FSA, HRA spending card is right for you? Please contact our team at 360PEO (855)667-4621 for immediate answers. Stay tuned for updates as more information gets released. Sign up for the latest news updates.

The subject matter in this communication is educational only and not rendering legal, accounting, investment advice, or tax advice. You should consult with appropriate counsel or other professionals on all matters pertaining to legal, tax, investment, or accounting obligations and requirements.

On Sept. 24, 2020, President Donald Trump issued an executive order outlining his health care plan, called the America First Health Care Plan. This Legal Update video explains further.

For information about transparency providers and new tech tools contact us at info@medicalsolutionscorp.com or (855)667-4621.

For more information on PEOs or a customized quote please submit your contact. We will be in touch ASAP.

BREAKING: HIT and Cadillac Tax Repealed

Congress has voted to fully repeal the Cadillac Tax and Health Insurance Tax effective January 1, 2021. This means the Health Insurance Tax will still be in place for 2020 and will be gone in 2021.

Both unpopular taxes with bipartisan approval delayed the Cadillac Tax but put the Health Insurance Tax(HIT) back in for 2020 earlier this summer. See Cadillac Tax Out Health Insurance Tax (HIT) Back In. Below are summaries of these two taxes that are now fully repealed.

Whats is the Health Insurance Tax (HIT)?

Health Insurance Tax: This tax included in the Affordable Care Act (ACA) increased the cost of health care coverage for consumers and employers in every state. The ACA imposed a new sales tax on health insurance that started at $8 billion in 2014, increased to $14.3 billion by 2018, and continued to increase each year.

The HIT costing an estimated 2.5%-3% added surcharge or an estimated $500/family annually and $241 for Seniors. Website Stop The Hit calculates $5,000 as the average tax for a 10 man small business for example.

Whats is the Cadillac Tax?

The Cadillac Tax was to take effect in 2022 and had been twice delayed since its original inception scheduled for Jan 2014. This tax called for a 40% excise tax on the amount of the aggregate monthly premium of each primary insured individual that exceeds the year’s applicable dollar limit, which will be adjusted annually to the Consumer Price Index plus 1%.

The 40% excise tax applies to the cost of employer health plan coverage exceeding certain threshold amounts, which were originally set for 2018 at $10,200 for individuals or $27,500 for families.

Originally, the Cadillac Tax was pushed back by the behest of Unions to 2018 from the original proposed 2014 date. Most Unions with generous health care packages would not be complaint within that time frame. For average Gold Plans in regions such as NY, the widely unpopular Cadilac Tax would have been felt.

Learn more about how we are successfully helping navigate SMB for 20+ years. If you have any questions or would like additional information, please contact us at 855-667-4621 or info@medicalsolutionscorp.com.

On Friday, June 5, President Trump signed the Paycheck Protection Program (PPP) Flexibility Act, clearing the way for more flexibility and forgiveness of the loans made through the PPP. Originally these loans, which were part of the CARES Act, were provided to help business owners cover payroll costs, rent, and utilities.

The newly enacted legislation states that:

Business owners now have 24 weeks to spend funds (up from eight weeks)

Business owners only need to spend 60% of the loan on payroll costs (down from 75%)

The covered period of the loan now ends December 31 instead of June 30

Business owners won’t have to make employer payroll tax payments through the end of 2020

The business will not lose any loan forgiveness eligibility if it can show that some employees declined to return to their jobs or the pre-pandemic headcount is no longer required

The payback period for new loan applicants has been extended from two years to a minimum of five for those not seeking, or who are ineligible, for forgiveness

If you’d like to find out more about how you can get better benefits so your employees use them when they need to, we’d like to show you how. Please contact us using form below or info@360peo.com or 855-667-4621.

The information provided on this website is intended for informational purposes only. 360PEO does not offer legal or medical guidance. Those with legal or medical questions should seek appropriate assistance from a licensed professional. Stay up to date by signing up for Newsletter and Coronavirus Dashboard below.

The IRS has released the 2021 Health Savings Account (HSA) inflation adjustments. To be eligible to make HSA contributions, an individual must be covered under a high deductible health plan (HDHP) and meet certain other eligibility requirements.

New HSA 2021 limits are as follows:

2021

2020

HSA Annual Contribution Limit

$3,600; $7,200

$3,550 – Single; $7,100 – Family

HDHP Minimum Annual Deductible

$1,400; $2,800

$1,400 – Single; $2,800 – Family

HDHP Out-of-Pocket Maximum

$7,000; $14,000

$6,900 – Single; $13,800 – Family

Age 55+ Catch-Up Provision

$1,000; $2,000

$1,000- Single; $2,000 – Husband/Wife

Age 55 Catch Up Contribution

As in 401k and IRA contributions, you are allowed to contribute extra if you are above a certain age. If you are age 55 or older by the end of the year, you can contribute an additional $1,000 to your HSA. If you are married, and both of you are age 55, each of you can contribute an additional $1,000. A savvy strategy for high-income earners is to invest the money in your HSA for the long haul. Once you’re 65, you can take out tax-free distributions to cover Medicare premiums. If you withdraw money at that point for non-medical uses, you pay the same tax as you would on withdrawals from a pretax 401(k). But you can also take money out tax-free to reimburse yourself for prior years’ out-of-pocket medical expenses if you have the old receipts.

COVId-19 Update:

You can even use an HSA to save on a typical trip to the CVS. Thanks to a tax relief provision tucked in the last Covid-19 stimulus package, you can use the money you stash in an HSA or FSA (more on those later) for over-the-counter medications like Tylenol or Flonase as well as menstrual products like tampons and pads. That reverses Obamacare restrictions on OTC meds requiring a doctor’s prescription for them to be eligible for reimbursement.

HSA/HDHP Market Growth

HSA holders own the assets in the accounts and can build up substantial sums over time. Enrollment in HSA-compatible insurance plans has increased to 10 million earlier this year, from 1 million in March 2005, according to, America’s Health Insurance Plans (AHIP), a trade group.

HSAs were authorized starting in January 2004. Since then, AHIP has conducted a periodic census of health plans participating in the HSA/HDHP market.

The number of people with HSA/HDHP coverage rose to more than 11.4 in January 2011, up from 10.0 million in January 2010, 8.0 million in January 2009, and 6.1 million in January 2008.

30 percent of individuals covered by an HSA plan were in the small group market, 50 percent were in the large-group market, and the remaining 20 percent were in the individual market.

14% of all workers in the private sector have access to a Health Savings Account acc. to the Bureau of Labor Statistics.

States with the highest levels of HSA/HDHP enrollment were California, Ohio, Florida, Texas, Illinois, and Minnesota.

HSA Advantages:

Opportunity to build savings – Unused money stays in your account from year to year and earns tax-free interest. The HSA also gives you an investment opportunity.

Tax-free contributions and earnings – You don’t pay taxes on contributions or earnings.

Tax-Free Money allowed for non-traditional Medical coverage– As per IRS Publication 502, unused money can be used for dental, vision, Lasik eye surgery, acupuncture, yoga, infertility, etc. Popular Examples

Portability – The funds belong to you, so you keep the funds if you change jobs or retire.

Our overall experience with HSAs has been positive when employer funding is at a minimum 50% using either the HSA or an HRA (Health Reimbursement Account-employer keeps unspent money). Traditional plans trend of higher copays and new in-network deductibles has also led to the popularity of an HSA.

Next Steps

Plan sponsors should update payroll and plan administration systems for the 2021 cost-of-living adjustments and should incorporate the new limits in relevant participant communications, such as open enrollment and communication materials, plan documents, and summary plan descriptions.

Is your HSA compliant? Which pre-tax qualified HSA, FSA, HRA spending card is right for you? Please contact our team at Millennium Medical Solutions Corp (855)667-4621 for immediate answers. Stay tuned for updates as more information gets released. Sign up for the latest news updates.

As COVID-19 unfolds, the importance of a PEO for a Small Business becomes evident. How can you protect your employees while also managing costs? Here are examples of how our PEO clients have benefited.

1. Rapid Law Changes

With recent CARES Act and FFCRA(Families First Coronavirus Response Act) to help struggling businesses, overwhelming info and regulations have mounted for the small business owner. Who is eligible for benefits? Tax credits? Furloughs and COBRA? Is their business Essential? Paid Sick Leave eligibility and additional tax credit entitlement?

PEOs provide a full team of experts who anxiously awaited the legislation, final rulings, and updates on all the Acts. They spend countless hours diving into legal jargon to answer business owners’ questions. Then, PEOs work alongside organizations to implement processes that assist in keeping the business compliant. They also help employees through the difficult time, with the livelihood of the business always in mind.

2. PEOs help with Paycheck Protection Program (PPP) loans through the CARES Act

Lenders are asking for historical payroll data and tax reports quickly produced by a PEO’s HRIS System. Many small businesses without HR help find these systems financially draining. Example: Needed 940/941 reporting is issued which can be sent to SBA Lender. Also, several leading PEO’s have supported clients with NYS Shared Loans Program.

Working with clients to understand options.

3. Payroll Burden

Payroll administration is now a nightmare. Tracking the FFCRA emergency sick leave and expanded FMLA separately from regular sick and FMLA leave has thrown a wrench in many payroll processors’ systems. Add on any furloughed or terminated employee reporting and tracking, and now the job has doubled.

Instead, our PEO Clientsy are spending their time on mission-critical work that could make or break the business. Additionally, their payroll is processed by professionals who have the time and expertise to know the nuances of payroll and payroll tax laws with back up teams of professionals in place.

4. Staffing Needs – On-Boarding and Terminations

A minimum 75% of PPP loans must be spent on staffing costs. Companies that had previously furloughed or terminated employees find they need to hire employees back. This comes with additional paperwork and many employee questions, such as whether benefits wait periods start over.

Conversely, when businesses do need to furlough or terminate employees, the PEO is a great guide for compliance. The layoff process, COBRA, paperwork including givernement reporting are supported.

5. HR Excellence

Partnering with a PEO is much like gaining access to a full-service HR division, with a team of HR experts who are up-to-date with new and changing employment laws and able to identify ways to streamline your HR.

According to a report conducted by the National Association of Professional Employer Organizations (NAPEO), PEOs provide access to more HR services at a cost that is close to $450 lower per employee, compared to companies that manage their HR services in-house.

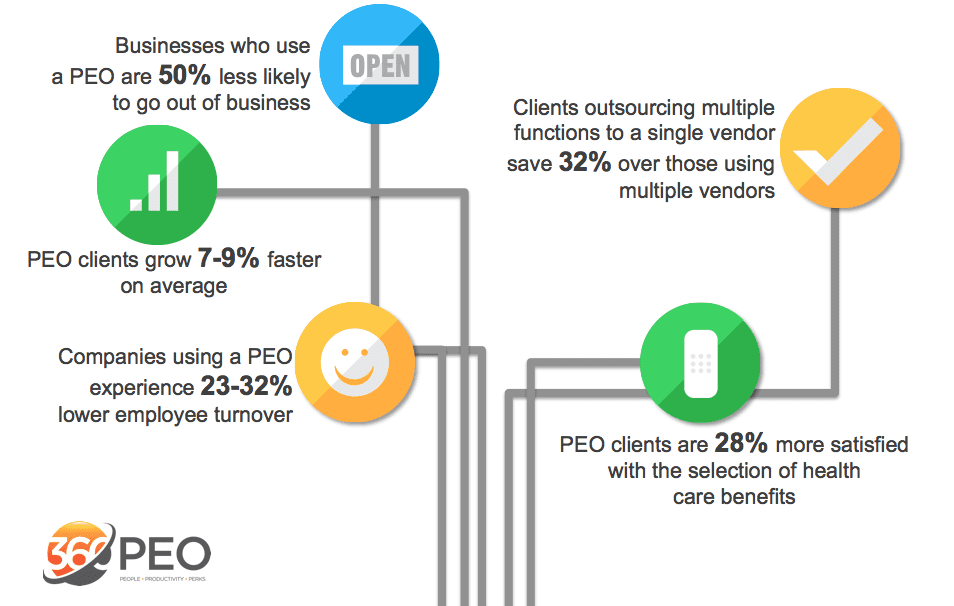

Studies show that businesses in a PEO arrangement grow 7-9 percent faster, have 10-14 percent lower turnover, and are 50 percent less likely to go out of business.

6. Affordable and Better Benefits

By joining a large group risk-pool a a PEO can help employers gain access to high quality employee benefits, such as health insurance options with stable and affordable rates. Due to costs, small businesses often find high-quality employee benefits out of reach. The savings on health insurance alone can pay for the PEO itself.

If you’re interested in hearing more about the advantages of partnering with a PEO, we’d love to talk to you. Fill out the form below or email info@medicalsolutionscorp.com for a FREE Consultation Today!

The information provided on this website is intended for informational purposes only. Millennium Medical Solutions Corp. does not offer legal or medical guidance. Those with legal or medical questions should seek appropriate assistance from a licensed professional. Stay up to date by signing up for Newsletter and Coronavirus Dashboard below.

As we watch, wait and see the evolution of this Corona Virus outbreak, it is important that employers plan. This is not a situation where you want to panic should this hit your business.

What we know about the virus

Coronaviruses are an extremely common cause of colds and other upper respiratory infections. The symptoms can include a cough, possibly with a fever and shortness of breath. There are some early reports of non-respiratory symptoms, such as nausea, vomiting, or diarrhea. Many people recover within a few days. However, some people — especially the very young, elderly, or people who have a weakened immune system — may develop a more serious infection, such as bronchitis or pneumonia.

Should you worry about catching this virus?

Unless you’ve been in close contact with someone who has the coronavirus — right now, this typically means a traveler from Wuhan, China who actually has the virus — you’re likely to be safe. In the US, for example, all five cases of the virus were recent travelers to Wuhan. The CDC maintains the risk is low to Americans, however, “we need to be preparing as if this is a pandemic, but I continue to hope that it is not,” said Dr. Nancy Messonnier, director of the CDC’s National Center for Immunization and Respiratory Diseases.

How can I protect myself?

Much like prevention of the spread of any other infectious disease, basic hygiene principles are key to curbing the spread of this virus.

Wash your hands often with soap and water for at least 20 seconds. Use an alcohol-based hand sanitizer that contains at least 60 percent alcohol if soap and water are not available.

Avoid touching your eyes, nose and mouth with unwashed hands.

Avoid close contact with people who are sick.

Stay home when you are sick.

Cover your cough or sneeze with a tissue, then throw the tissue in the trash.

Clean and disinfect frequently touched objects and surfaces.

Be mindful of:

Employee wellbeing. Monitor updates from public health officials and governments and keep employees informed and educated about the outbreak and any steps being taken to safeguard their health. Encourage employees to stay home when sick and telecommute if the outbreak worsens.

Travel policies. As of Monday, January 27th, the CDC has issued a stronger warning about travel, urging Americans to reconsider travel anywhere in China, issuing a stronger level 4 warning for the specific province where Wuhan is located, stating: “Do not travel to Hubei province, China” due to the coronavirus outbreak. The Centers for Disease Control and Prevention urges people to seek medical care right away if they had traveled to Wuhan in the past two weeks and develop a fever, cough or trouble breathing. It says older adults and people with underlying health conditions may be most at risk for severe illness from the virus.

Potential supply chain interruption. Identify operational and/or revenue impacts from potential disruptions to key suppliers and vendors. Also consider the possibility of sourcing good or parts from alternative suppliers.

Insurance coverage. Review insurance policies, prepare for potential claims, and consult your broker if you have questions.

SHRM Webcast: Coronavirus: Legal and Workplace Implications Thursday, March @ 2PM ET. Get the facts. Lead your organization’s response to the coronavirus crisis. Learn the proper steps to take to keep your workforce safe, implications of federal laws and more. You must be an active SHRM member to attend.

Please contact us for further information or if you need assistance creating a workable plan.

Contact us at (855) 667-4621 or email us at info@360peo.com

Congress has voted to fully repeal the Cadillac Tax and Health Insurance Tax effective January 1, 2021. This means the Health Insurance Tax will still be in place for 2020 and will be gone in 2021.

Both unpopular taxes with bipartisan approval delayed the Cadillac Tax but put the Health Insurance Tax(HIT) back in for 2020 earlier this summer. See Cadillac Tax Out Health Insurance Tax (HIT) Back In. Below are summaries of these two taxes that are now fully repealed.

Whats is the Health Insurance Tax (HIT)?

Health Insurance Tax: This tax included in the Affordable Care Act (ACA) increased the cost of health care coverage for consumers and employers in every state. The ACA imposed a new sales tax on health insurance that started at $8 billion in 2014, increased to $14.3 billion by 2018, and continued to increase each year.

The HIT costing an estimated 2.5%-3% added surcharge or an estimated $500/family annually and $241 for Seniors. Website Stop The Hit calculates $5,000 as the average tax for a 10 man small business for example.

Whats is the Cadillac Tax?

The Cadillac Tax was to take effect in 2022 and had been twice delayed since its original inception scheduled for Jan 2014. This tax called for a 40% excise tax on the amount of the aggregate monthly premium of each primary insured individual that exceeds the year’s applicable dollar limit, which will be adjusted annually to the Consumer Price Index plus 1%.

The 40% excise tax applies to the cost of employer health plan coverage exceeding certain threshold amounts, which were originally set for 2018 at $10,200 for individuals or $27,500 for families.

Originally, the Cadillac Tax was pushed back by the behest of Unions to 2018 from the original proposed 2014 date. Most Unions with generous health care packages would not be complaint within that time frame. For average Gold Plans in regions such as NY, the widely unpopular Cadilac Tax would have been felt.

Learn more about how we are successfully helping navigate SMB for 20+ years. If you have any questions or would like additional information, please contact us at 855-667-4621 or info@360.com.

For more information on PEOs or a customized quote please submit your contact. We will be in touch ASAP.

BREAKING: HIT and Cadillac Tax Repealed

Congress has voted to fully repeal the Cadillac Tax and Health Insurance Tax effective January 1, 2021. This means the Health Insurance Tax will still be in place for 2020 and will be gone in 2021.

Both unpopular taxes with bipartisan approval delayed the Cadillac Tax but put the Health Insurance Tax(HIT) back in for 2020 earlier this summer. See Cadillac Tax Out Health Insurance Tax (HIT) Back In. Below are summaries of these two taxes that are now fully repealed.

Whats is the Health Insurance Tax (HIT)?

Health Insurance Tax: This tax included in the Affordable Care Act (ACA) increased the cost of health care coverage for consumers and employers in every state. The ACA imposed a new sales tax on health insurance that started at $8 billion in 2014, increased to $14.3 billion by 2018, and continued to increase each year.

The HIT costing an estimated 2.5%-3% added surcharge or an estimated $500/family annually and $241 for Seniors. Website Stop The Hit calculates $5,000 as the average tax for a 10 man small business for example.

Whats is the Cadillac Tax?

The Cadillac Tax was to take effect in 2022 and had been twice delayed since its original inception scheduled for Jan 2014. This tax called for a 40% excise tax on the amount of the aggregate monthly premium of each primary insured individual that exceeds the year’s applicable dollar limit, which will be adjusted annually to the Consumer Price Index plus 1%.

The 40% excise tax applies to the cost of employer health plan coverage exceeding certain threshold amounts, which were originally set for 2018 at $10,200 for individuals or $27,500 for families.

Originally, the Cadillac Tax was pushed back by the behest of Unions to 2018 from the original proposed 2014 date. Most Unions with generous health care packages would not be complaint within that time frame. For average Gold Plans in regions such as NY, the widely unpopular Cadilac Tax would have been felt.

Learn more about how we are successfully helping navigate SMB for 20+ years. If you have any questions or would like additional information, please contact us at 855-667-4621 or info@medicalsolutionscorp.com.

A Texas appeals court ruled yesterday that the Obamacare individual mandate unconstitutional and sends law back to lower court.

The US of Appeals issued its decision in the Texas v. United States case. The case challenged the constitutionality of the ACA’s individual mandate in light of the Tax Cuts and Jobs Act of 2017, which zeroed out the individual mandate penalty. The appellate court was reviewing the lower court’s ruling that found that the individual mandate, with no accompanying tax penalty, is unconstitutional and that the individual mandate is such an essential part of the ACA that the ACA cannot function without the individual mandate in place.

In the appellate court’s ruling, it agreed that the individual mandate is unconstitutional because it can no longer be read as a tax, and there is no other constitutional provision that justifies this exercise of congressional power. However, when reviewing whether the individual mandate could be separated from the rest of the ACA, the appellate court sent that question back to the district court to provide additional analysis of the provisions of the ACA as they currently exist that was not provided in the lower court’s previous decision.

This ruling is not final and is expected to be engaged in appeals for the next several months, which will likely culminate in a hearing before the Supreme Court. This means that the ACA continues to be the law of the land and compliance with the ACA is still being enforced. Coverage for the 2020 plan year remains unaffected by the ruling.

If you have questions about the impact of this ruling, contact info@360peo.com.

What You Need to Know About Medicare 2018 Infographic

This timely infographic walks seniors through the differences between traditional Medicare and Medicare Advantage vs. Supplement Plans + a helpful plain English glossary.

Open Enrollment ends Dec 7, 2017, for Jan 1, 2018 effective date. Enroll by phone advantage at (855) 667-4621.

We are certified and appointed to sell senior plans with leading health insurers in order to help people in New York currently enrolled in Medicare or those who are aging into Medicare (turning 65) with a wide variety of options. Some of these are Medicare Advantage (HMO, PPO), supplement plans, and Part “D” prescription plans (PDP,s).

There are also some special enrollment periods (SEP) available to individuals under certain conditions. The Annual Enrollment Period (AEP) for Medicare is October 15 to December 7 this year. Those currently on Medicare can shop around and switch their plans at this time. The initial enrollment period (IEP) of 7 months. This is from 3 months prior to your 65th birthday, the month of your birthday, and the 3 months following your birth month. It is wise to contact an expert to help you find the coverage that best suits you during these enrollment periods. You can call or email us at any time for comprehensive, “no pressure” advice.

You can start getting plan information for 2018 premiums and benefits.

October 15 — December 7

This is the Annual Election Period (AEP). During this time, you can make changes to your existing Medicarehealth or prescription drug plan or select a new plan for 2018.

January 1 — February 14

This is the Medicare Advantage Disenrollment Period. During this time, you can prospectively disenroll from your Medicare Advantage (MA) plan and return to Original Medicare.

If you are turning 65:

– If you aren’t getting Social Security (for instance, because you are still working), you will need to sign up for Medicare benefits. You should contact Social Security three months before you turn age 65. – You can enroll in a Medicare plan starting three months before the month of your 65th birthday, the month of your birthday, and for up to three months after your 65th birthday, for a total period of seven months.

Contact Us Now Learn how our Agency is helping businesses thrive in today’s economy. Please contact us at info@360peo.com or (855)667-4621.

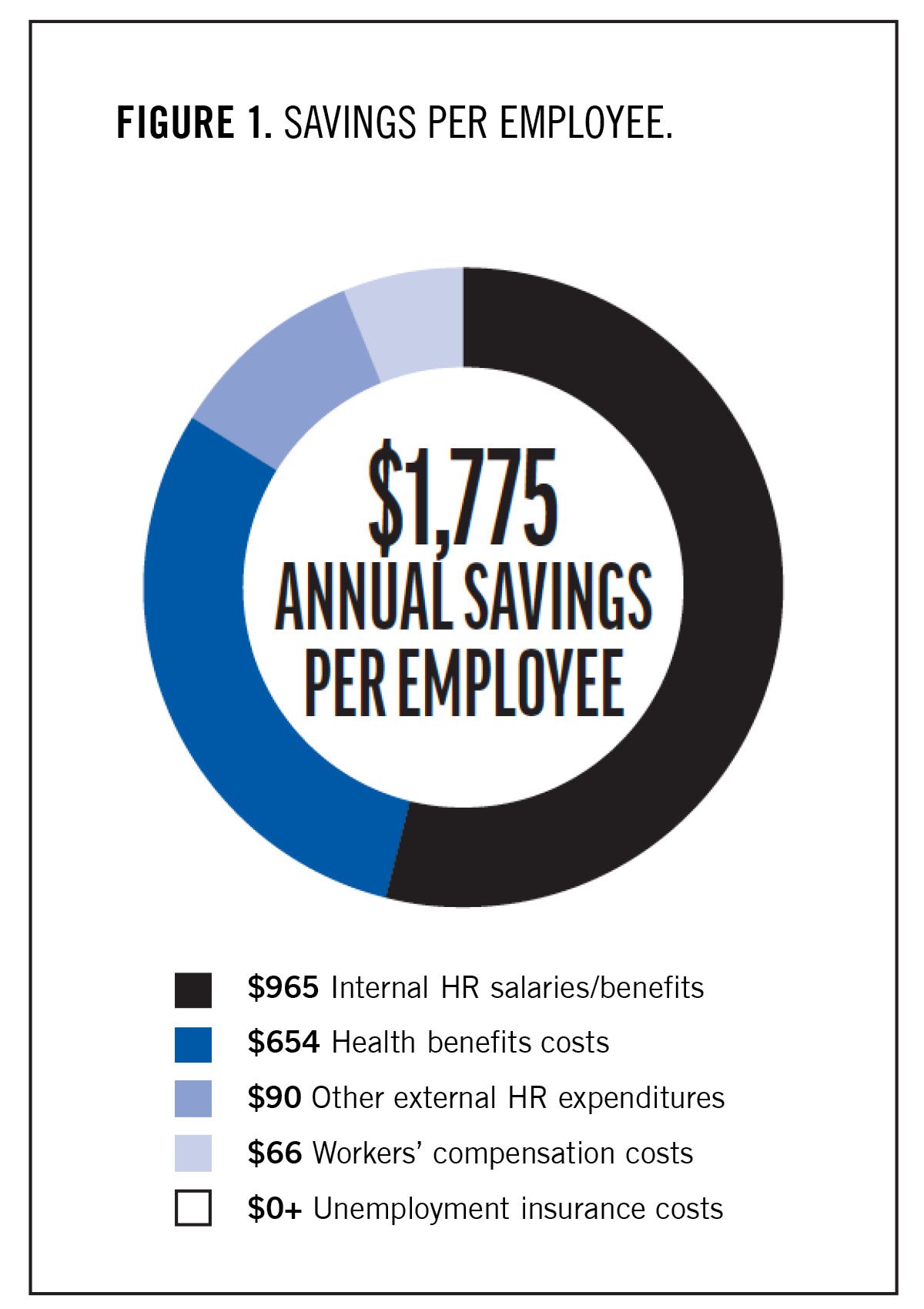

The ROI on a PEO is 27.2% according to a new 2019 study released today by the National Association of Professional Employer Organizations (NAPEO) .

The new report focused solely on costs and calculated savings for PEO clients in five HR-related areas:

HR personnel costs

Health benefits

Workers’ compensation

Unemployment insurance (UI)

Other external expenditures in areas related directly to HR services (payroll, benefits, etc.)

An annual per employee savings of $1,775 is reached according to the study. Notable findings are lower employee turnover, higher rates of both employee and revenue growth, and enhanced employee benefit offerings.

PEOs provide HR, payroll, benefits, workers’ comp, and regulatory compliance assistance to small and mid-sized companies. By providing these services, PEOs help businesses improve productivity, increase profitability, and focus on their core mission. Through PEOs, the employees of small businesses gain access to employee benefits such as 401(k) plans; health, dental, life, and other insurance; dependent care; and other benefits typically provided by large companies. A copy of the full study is availablehere.

The number of small and medium-sized employers using professional employer organizations (PEO) continues to increase each year. Often, it is thought that the growth of the PEO industry is due mainly to the benefits business owners see from this partnership. However, owners aren’t the only ones who gain from working with a PEO.

Small business employees, too, stand to benefit from the services and solutions offered by PEOs today. Let’s take a look at a few examples of the positive outcomes that small business workers see when their employer works with a PEO.

1. Better Benefits

One of the most well-known advantages to using a PEO is gaining improved, modern benefits and perks. And while better benefits help employers retain and recruit talent, these enhanced perks often provide even greater for employees.

When working with a PEO, employees are given access to a wide-variety of personalized benefits, including:

By having solid HR policies, a comprehensive benefit package, and employee perks, you are able to create a safe and happy workplace that helps you attract quality employees and retain them to reduce the cost of turnover.

2. Workers’ Compensation Savings

Over the last few years, the workers’ compensation market has gotten a lot tougher for business owners. PEOs help businesses secure competitive rates for workers’ compensation insurance. That can sometimes be challenging for start-up companies, companies with past losses or those with high-risk jobs. PEOs have flexible workers’ compensation programs with more affordable rates than stand-alone policies and staff who help manage the cost of claims, coordinate return-to-work programs and recommend safety training

In most cases, it will be a more cost effective option than the traditional market can offer. We can also include Employment Practices Liability insurance which covers lawsuits arising from wrongful termination, discrimination, and sexual harassment. Issues that are becoming more common in today’s workplace.

3. Solve HR Issues

Federal, state and local regulations related to HR are more voluminous and complex than ever. Most businesses don’t have the staff for the in-depth subject matter expertise needed to adequately navigate wage and hour regulations and ensure compliance with the full range of employment and tax laws. When small and mid-sized businesses work with a PEO, they get a team of compliance experts who stay current with all the rules and regulations that apply to employers.

A PEO also helps manage HR risk by helping clients:

Create an employee handbook to include anti-discrimination and harassment policies

Familiarize themselves with wage and hour laws

Pay employees in accordance with the law

Pay employees in a timely manner

4. Compliance Relief

PEOs are responsible for staying up-to-date on the latest federal and state labor laws and regulations. This not only saves you time, but also the frustration that comes with trying to make sense of and implement many of these changes.

By staying up-to-date on these changes, you can avoid hefty fines and disgruntled employees.

5. Modern HR Tech

This desire for modern technology has also become an expectation for HR tasks that employees are asked to perform, such as requesting PTO, going through benefit enrollment, and submitted their hours.

The majority of PEOs offer their clients the kind of HR tech that employees want and need. Some even have mobile apps that make tasks as simple as possible for employees!

And most PEOs, through their HR technology, can offer small business employees learning and development programs and software that much larger organizations use.

A great HRIS System is fundamental today. By meeting employee expectations, employers help boost the happiness and ultimately retention of their workforce.

6. Employee Happiness

Enhanced benefits, robust learning and development programs, and easy-to-use, modern technology all help to boost the employee experience.

For employees, increased happiness makes their connection to their work and employer greater. And for employers, happy employees mean improved productivity and lesser chance of turnover – studies from the National Association of Professional Employer Organizations (NAPEO) have shown that PEOs help their clients reduce turnover by 10% to 14%.

A happier workplace and workforce are good outcomes for everyone and working with a PEO can help achieve these goals!

7. Competitive Business and Personal PEO Insurance Quotes

360PEO can also provide competitive quotes on all of your personal insurance needs. We work with several industry partners to help clients find coverage for many commercial lines of insurance, such as Group Long Term Care Insurance, Executive Benefits, General Liability, Property, and Commercial Auto.

We also offer personal lines insurance such as renter’s policies, home insurance, and life insurance.

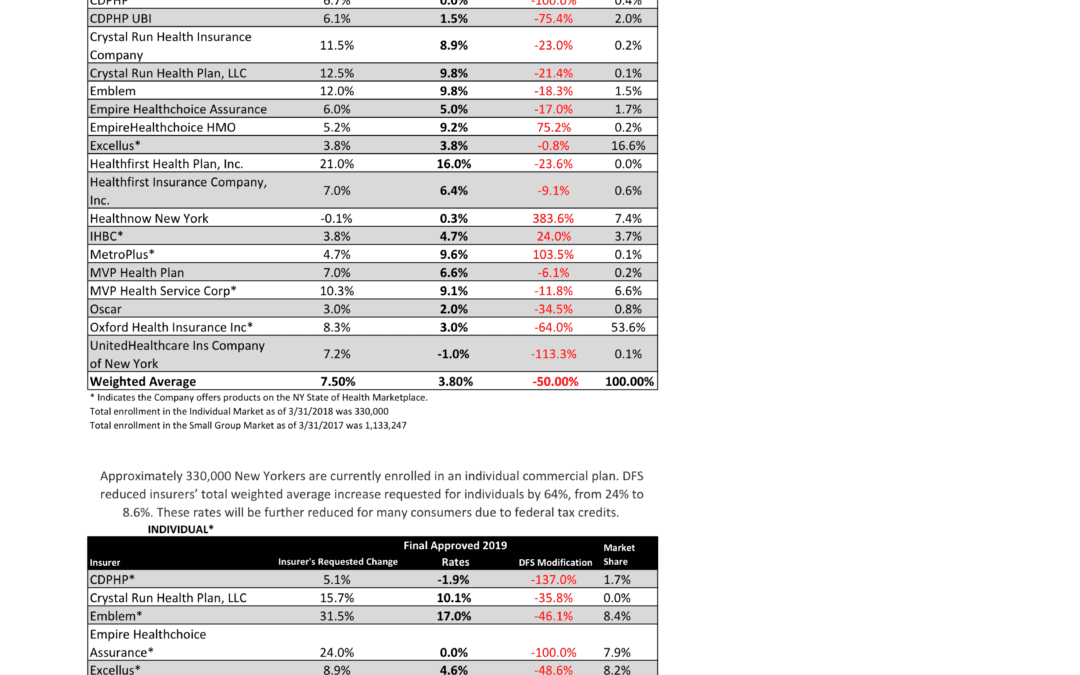

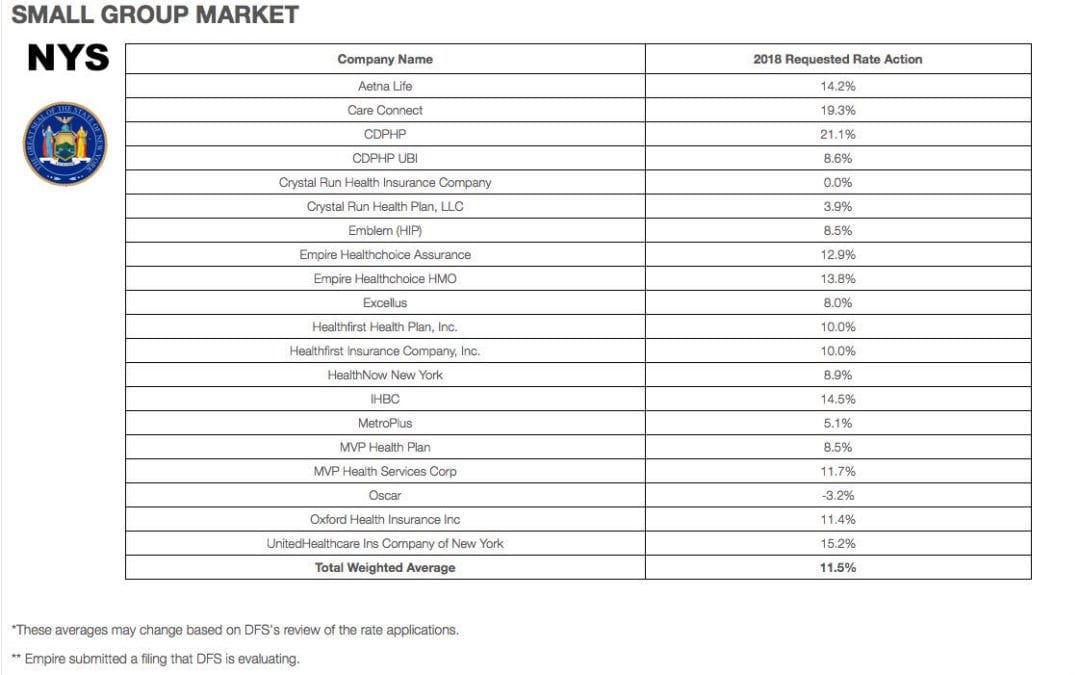

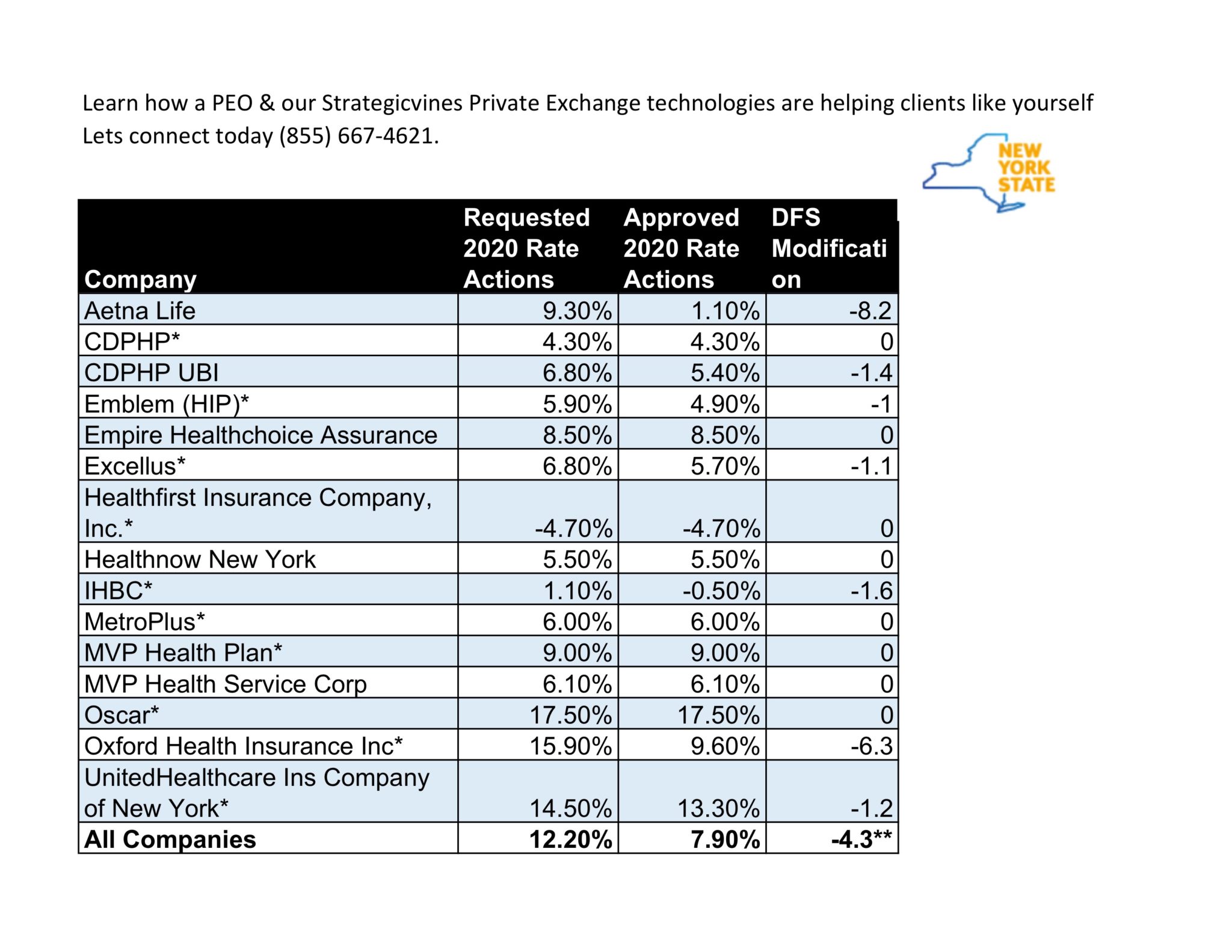

NYS has approved 2020 health inusrance rate requests today. Small group rates increase 7.9% and 6.8 8.6% for individuals.

As per NY State Law, Health Insurers are required to send out early notices of rate request filings to groups and subscribers see original –NYS 2020 Rate Requests. Despite only 3 months of mature claims data experience for 2019 health insurers’ original requests were noticeably below average. Ultimately NYS reduced this request substantially by approximately 55%.

The 2020 small group rate increase was in line at 7.9% vs 2019’s approval of 7.5%. This reflect a stabilizing ACA market. Insurers’ financial performance improved nationwide last year to its highest level since the passage of the law. The average medical-loss ratio, which represents the portion of premiums spent on medical claims and quality improvement, was 70% last year in the individual market nationwide. That led to plans paying $800 million in rebates for failing to meet requirements on medical spending, according to the Kaiser Family Foundation.

Rate Factors

The state noted that premiums increases main driver are medications. “The drug costs account for the largest share of medical expenses, followed by inpatient hospital costs, and outpatient hospital costs.”

More than one million New Yorkers are enrolled in small group plans, which cover employers with 1 to 100 employees. Insurers requested an average rate increase of 12.2% in the small group market. DFS cut the weighted average requested rate increases by 4.3 percentage points, or 35%, from 12.2% to 7.9% for 2020, saving small businesses over $313 million. The federal ACA Health Insurance Tax, which was reimposed for 2020, accounts for approximately 3% of these rates. Without this tax, the increase would have been 4.7%. A number of small businesses will also be eligible for tax credits that may lower those premium costs even further.

Health Insurance Tax is Back

The HIT (Health Insurance Tax) is back. For Small business, this translates to an estimated 2.5%-3% added surcharge. For States like NYS where there is already approx. 16% added surcharge to high premiums, this becomes daunting. It is no surprise the unpopular HIT was suspended. In 2017, payers escaped making $13.9 billion in payments due to the moratorium, according to a 2018 analysis by Oliver Wyman, commissioned by UnitedHealth Group. This may have saved consumers billions on their insurance coverage.“The taxes on health insurance are non-deductible for federal tax purposes for health insurers,” the report explained.

Website Stop The Hit calculates $5,000 as the average tax for a 10-man small business for example.Calculates how the HIT affects your State and your business, here. Take action now: tell Congress to repeal the HIT! Join small business owners across the country in stopping the HIT. Sign the petition here.

The 3.7 million Worksite Employees employed by PEOs earned a total of $176 billion.

They represent 15 percent of all employment by private sector employers that have 10 to 99 employees (chosen because this is the size range of most PEO clients) and 2.4 percent of civilian employment in the United States.

Between 2008 and 2017, the number of worksite employees employed in the PEO industry grew at a compounded annual rate of 8.3 percent. This is roughly 14 times higher than the compounded annual growth rate of employment in the economy overall during the same period.

The total employment represented by the PEO industry is roughly the same as the combined number of employees for Walmart (United States only), Amazon, IBM, FedEx, Starbucks, AT&T, Wells Fargo, Apple, and Google. Those companies include the two largest retailers, the largest technology company, the largest transportation company, the largest telecommunications provider, the largest financial services firm, the largest specialty restaurant chain, plus the two most highly valued firms in the world based on stock market valuation.

Key Findings

Businesses in a PEO arrangement grow 7-9 percent faster, have 10-14 percent lower turnover, and are 50 percent less likely to go out of business.

PEOs are able to offer a broad array of HR services at a lower cost, and offer access to retirement plans to small businesses that may not otherwise sponsor them.

PEOs provide services to 175,000 small and mid-sized businesses, employing 3.7 million people.

There are 907 PEOs in the U.S.

Administrative costs are around $450 lower per employee for businesses that use a PEO.

What is Co-Emplyment

The PEO relationship involves a contractual allocation and sharing of certain employer responsibilities between the PEO and the client, as delineated in a contract typically called a client service agreement (CSA).

For the obligations a PEO agrees to take on with respect to its clients, the PEO assumes specific employer rights, responsibilities, and risks through the establishment and maintenance of a relationship with the workers of the client. More specifically, a PEO establishes a contractual relationship with its clients whereby the PEO:

May assume certain employment responsibilities for specified purposes regarding the workers at the client locations.

May reserve a right of direction and control of the employees with respect to particular matters.

Shares or allocates employment responsibilities with the client in a manner consistent with the client maintaining its responsibility for its product or service.

Remits wages and withholdings of the client’s workers.

Issues Form W-2s for the compensation paid under its Employer Identification Number.

Reports, collects and deposits employment taxes with local, state and federal authorities.

A PEO provides integrated services to effectively manage critical human resource responsibilities and employer risks for clients. A PEO delivers these services by establishing relationships with the client’s employees and administering certain employer rights, responsibilities, and risks as agreed with the client.

The roles of the PEO and the client depend upon the facts and circumstances of each relationship — that is, each obligation should be examined individually as employment responsibilities are assigned in the parties’ CSA. Each party will be responsible for certain obligations of employment, while both parties might share responsibility for other obligations and be “an” employer, but neither party is “the” employer for all purposes.

Both the PEO and the client company establish a relationship with worksite employees. The PEO might engage with worksite employees with respect to specific matters involving human resource management and compliance with employment requirements, while the client company directs and controls worksite employees in the client’s day-to-day operations as well as the manufacturing, production, and delivery of its products and services.

The client company provides worksite employees with the tools, instruments, and places to work. Some PEOs provide assistance and suggestions to clients when it comes to offering worksite employees a workplace that is safe, conducive to productivity and operated with best practices with employment rules and regulations. Additionally, the PEO assists clients and worksite employees with workers’ compensation insurance and a broad range of employee benefits programs.

PEOs create a real relationship with worksite employees over certain matters. This relationship exists in fact, not just in form. PEOs often assist with the risks attendant to the personnel functions of the worksite employees. PEOs manage liabilities by monitoring new employment trends and requirements and developing policies and procedures for their clients and the worksite employees, as stated in the client service agreement.

*information provided by NAPEO An Economic Analysis: The PEO Industry Footprint in 2018 Whitepaper. https://www.napeo.org/

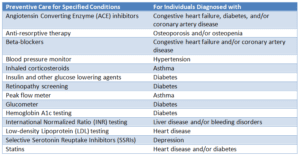

Last week, the IRS added care for a range of chronic conditions to the list of preventive care benefits that may be provided by an HSA compatible high deductible health plans (HDHP). Notice 2019-45, lists the new types of medical care that may be treated as preventive care for this purpose.

Individuals covered by an HSA compatible HDHP generally may establish and deduct contributions to a Health Savings Account (HSA) as long as they have no disqualifying health coverage or not enrolled in Medicare. To qualify as a high deductible health plan, an HDHP generally may not provide benefits for any year until the Federal (not health plan) minimum deductible for that year is satisfied.

The IRS together with the Department of Health and Human Services, has determined that certain medical care services received and items purchased, including prescription drugs, for certain chronic conditions should be classified as preventive care. The following services and items for individuals with the specified chronic conditions listed are treated as preventive care.

Learn how our Agency is helping businesses thrive in today’s economy. Please contact us at info@360PEO.com or (855)667-4621.

Last week the House voted the unpopular Obamacare Cadillac Tax to be permanently repealed 419-6. However, much like a bad cold, the Health Insurance Tax (the HIT) is back for 2020. Website Stop The Hit calculates $5,000 as the average tax for a 10 man small business for example.

Who’s affected?

No one escapes the $16 billion HIT. The return of the Health Insurance Tax (HIT) means higher costs and fewer jobs for hardworking Americans. Absent immediate Congressional action to delay the HIT, small businesses and families will face $500 on average in higher premiums for 2020. To make matters worse, the increased cost burden on small businesses from the HIT could result in the U.S. workforce being reduced by 152,000 to 286,000 jobs over a decade. Te HIT is projected to increase premiums for seniors by $241.

How much for 2020?

For Small business, this translates to an estimated 2.5%-3% added surcharge. For States like NYS where there is already approx. 16% added surcharge to high premiums, this becomes daunting. It is no surprise the unpopular HIT was suspended. In 2017, payers escaped making $13.9 billion in payments due to the moratorium, according to a 2018 analysis by Oliver Wyman, commissioned by UnitedHealth Group. This may have saved consumers billions on their insurance coverage.“The taxes on health insurance are non-deductible for federal tax purposes for health insurers,” the report explained.

In some states, such as Vermont, the price of insurance would have more than quadrupled. The payer trade group published a fact sheet on this. “Allowing a tax to resume in 2020 valued at an annual level of $16 billion, would saddle individual market consumers, small businesses, state Medicaid programs, and Medicare Advantage enrollees with higher health care costs,

Can this be repealed?

Relief from the health insurance tax would result in real savings to the American people. We strongly urge Congress to provide an additional two-year suspension of the health insurance tax by passing H.R. 1398.

Calculates how the HIT affects your State and your business, here.

Take action now: tell Congress to repeal the HIT! Join small business owners across the country in stopping the HIT. Sign the petition here.

Learn more about how we are successfully helping navigate SMB for 20+ years. If you have any questions or would like additional information, please contact us at 855-667-4621 or info@360PEO.com.

The IRS has released the 2020 Health Savings Account (HSA) inflation adjustments. To be eligible to make HSA contributions, an individual must be covered under a high deductible health plan (HDHP) and meet c ertain other eligibility requirements.

New HSA 2020 limits are as follows:

2020

2019

HSA Annual Contribution Limit

$3,550 $7,100

$3,500 – Single $7,000 – Family

HDHP Minimum Annual Deductible

$1,400 $2,800

$1,350 – Single $2,700 – Family

HDHP Out-of-Pocket Maximum

$6,900 $13,800

$6,750 – Single $13,300 – Family

Age 55+ Catch-Up Provision

$1,000 $2,000

$1,000- Single $2,000 – Husband/Wife

Age 55 Catch Up Contribution-As in 401k and IRA contributions, you are allowed to contribute extra if you are above a certain age. If you are age 55 or older by the end of year, you can contribute additional $1,000 to your HSA. If you are married, and both of you are age 55, each of you can contribute additional $1,000

HSA/HDHP Market Growth

HSA holders own the assets in the accounts and can build up substantial sums over time. Enrollment in HSA-compatible insurance plans has increased to 10 million earlier this year, from 1 million in March 2005, according to, America’s Health Insurance Plans (AHIP), a trade group.

HSAs were authorized starting in January 2004. Since then, AHIP has conducted a periodic census of health plans participating in the HSA/HDHP market.

The number of people with HSA/HDHP coverage rose to more than 11.4 in January 2011, up from 10.0 million in January 2010, 8.0 million in January 2009, and 6.1 million in January 2008.

30 percent of individuals covered by an HSA plan were in the small group market, 50 percent were in the large-group market, and the remaining 20 percent were in the individual market.

14% of all workers in the private sector that have access to a Health Savings Account acc. to Bureau of Labor Statistics.

States with the highest levels of HSA/HDHP enrollment were California, Ohio, Florida, Texas, Illinois and Minnesota.

HSA Advantages:

HSA plans are one of the most tax-effective ways to reduce health insurance costs. The amounts contributed are allowed as a full deduction on your tax return and as long as any amounts taking out of the account are used for medical costs, they are completely tax-free including any earnings.

Opportunity to build savings – Unused money stays in your account from year to year and earns tax-free interest. The HSA also gives you an investment opportunity.

Tax-free contributions and earnings – You don’t pay taxes on contributions or earnings.

Tax Free Money allowed for non-traditional Medical coverage– As per IRS Publication 502, unused moneys can be used for dental, vision, lasik eye surgery, acupuncture, yoga, infertility, etc. Popular Examples

Portability – The funds belong to you, so you keep the funds if you change jobs or retire.

Our overall experience with HSAs have been positive when employer funding is at minimum 50% using either the HSA or an HRA (Health Reimbursement Account-employer keeps unspent money). Traditional plans trend of higher copays and new in network deductibles has also led to the popularity of an HSA.

Is your HSA compliant? Which pre-tax qualified HSA, FSA, HRA spending card is right for you? Please contact our team at Millennium Medical Solutions Corp (855)667-4621 for immediate answers. Stay tuned for updates as more information gets released. Sign up for latest news updates.

All businesses today are aware that a healthy workforce translates to a happier and more productive employees. Nearly a quarter of participants in SHRM’s latest benefits survey plan to increase their Health & Wellness benefits, whose percentage was a higher than other categories such as professional and career development, flexible work schedules, retirement and family-friendly policies. One unusual offering, workstations that allow people to stand, soared to 44% from just 13% in 2013 when the data was first tracked.

Helping your employees strive towards physical, emotional, mental, and even spiritual well-being can lead to increased productivity and employee longevity. But how can you offer wellness programs that your employees will actually use and find beneficial? There’s no one size fits all solution, and the best way to get started is to invite employee input. Need some inspiration? Here are 5 employee wellness programs that might be the right fit for your company this coming year:

1. Online Wellness/Health Screening

Did you know many health nurses today pay your employees to take an online health risk assessment? Covered members receive a lump sum benefit payment once a year if they complete certain health-related activities (i.e. routine screenings, programs like smoking cessation and weight reduction, and more). Payment options range from $50 to $150. Empire Blue Cross, for example, pays up to $300 for this including smoking cessation online questionnaire and a flu vaccination.

2. Gym Reimbursements

You might not be able to build a gym at the office, but that doesn’t mean you can’t take advantage of your neighborhood businesses. Did you know most health care compare today offer up to $400 annual gym reimbursement? Most include a $200 spousal gym reimbursement as well.

3. Start a Walking Group

This solution is easy, free, and can be employee-driven. Failing to take breaks leads to burnout and eventually employee resentment. Encourage employees to take frequent breaks, but not just to the break room for more artificial lighting and a caffeine boost. Rally eager employees to lead morning, lunch, and/or after-work walking groups. The fresh air is energizing, boosts creativity, and helps feed social wellness needs, too.

4. Create a Healthy Challenge That Isn’t Based on Numbers

Although some businesses have success with Biggest Loser-style in-office challenges, it can also trigger disordered eating. Instead of focusing on numbers, focus on more subjective goals—like how many consecutive days fresh, local fresh vegetables can be part of a lunch. Kicking off these challenges with a brief intro to the importance of a healthy diet for life can help employees re-think their choices.

5. Seek Help from Outside Resources

There are several organizations that employers can turn to for information, research and guidance on wellness programs. Below are just a few for you to explore for helpful ideas on how to develop a culture of health in your organization.

HERO is a national non-profit dedicated to identifying and sharing best practices in the field of workplace health and well-being (HWB). Their mission is to improve the health and well-being of workers, their spouses, dependents and retirees. Check out the wealth of information on their site, including research studies and a blog.

The Health Project is a tax-exempt not-for-profit corporation formed to bring about critical attitudinal and behavioral changes in addressing the health and well-being of Americans. The Health Project focuses on improving personal health care practices and supporting population health by reaching adults where they spend most of their waking hours: at work. Many organizations have adopted health promotion (wellness) programs that encourage good health habits and improved understanding of how individual workers and their families can more effectively use health services.

Harvard Health Newsletters are free newsletters targeted to individuals with the purpose of providing educational information to help them invest in their own health or the health of their families.

CLICK HERE

Contact us to learn more about how health and wellness benefits can help you attract and retain your top talent.

Breaking: IRS released Notice extending the due dates for the 2018 information reporting requirements for employers to furnish information on returns and statements regarding minimum essential coverage provided to individuals.

Specifically, the notice extends the due date for furnishing the following to individuals: the 2018 Form 1095-B, Health Coverage, and the 2018 Form 1095-C, Employer-Provided Health Insurance Offer and Coverage, from January 31, 2019 to March 4, 2019.

Lastly, IRS extends the good-faith relief in Notice 2016-70 that applied to filings in 2015 to 2016 and 2017 and now to 2018. This relief applies to missing and inaccurate taxpayer identification numbers and dates of birth, as well as other information required on the return or statement.

To show good faith efforts to qualify for this relief, filers must meet applicable deadlines. However, IRS recognizes that late filers may still be able avoid penalties by showing reasonable cause for missing the due dates.

Contact Us Now Sign up for compliance alerts. Learn how our Agency is helping businesses thrive in today’s economy. Please contact us at info@360PEO.com or (855)667-4621.

The information provided herein is not written or intended as tax or legal advice and may not be relied on for purposes of avoiding any federal tax penalties. Entitiesor persons distributing this information are not authorized to give tax or legal advice. Individuals are encouraged to seek specific advice from their personal tax orlegal counsel.

The New York State Department of Financial Services (DFS) announced the updated Paid Family Leave premium rate and covered payroll limit for 2019. The NY DFS publishes a new employee contribution rate and wage cap each September 1st for the upcoming year to accommodate the graduation of benefits in from 2018 to 2021.

The following chart can be used to help explain these changes to your employees:

Year

Max Annual Covered Payroll

Premium Rate

Maximum Annual EE Contribution

Benefit %

Max Weekly Benefit

Benefit Duration

2018

$67,908

.00126

$85.56

50%

$652.96

8 Weeks

2019

$70,570*

.00153

$107.97

55%

$746.41

10 Weeks

HOW TO CALCULATE CONTRIBUTIONS?

• EMPLOYEE EARNING: $200,000 OR $3,846.15 WEEKLY WAGE.153% x $3.846.15 = $5.88 (Paid up after 19 weeks) *

• EMPLOYEE EARNING: $100,000 OR $1,923.07 WEEKLY WAGE.153% x $1,923.07 = $2.94 (Paid up after 37 weeks) *

• EMPLOYEE EARNING: $70,569 OR $1,357.10 WEEKLY WAGE.153% x $1,357.10 = $2.08 (Paid up after 52 weeks) *

• EMPLOYEE EARNING: $38,812.80 OR $746.40 WEEKLY WAGE.153% x $746.40 = $1.14 (Paid up after 52 weeks) *

Note: Employers may not collect contributions in excess of $107.97 * Such employee will have satisfied their maximum annual contribution

Almost every HR administrator I’ve talked to says that managing benefits and HR can be time-consuming and error-prone. We believe this can be solved with the combined power of the broker and technology. Together, they provide a flexible, customizable HR and benefits technology solution that helps employers save time, reduce errors, and increase employee engagement.

Take on-boarding as an example. Employee Onboarding is an important HR function that directly impacts the engagement levels of new employees in the first few days. That’s why it is no longer treated as just another administration input. At the employer end, it makes sense to invest in an extended and intensive employee onboarding program. This is because, hiring a person involves a lot of contingent costs, and it is best that an employee once hired is retained for the long term. Research shows that employees have a higher chance of leaving the organization within the first 18 months. An effective new employee onboarding program can prevent just that, saving your company time, cost, and other expensive resources. An onboarding program can thus go a long way in improving the efficiency of hiring.

An Introduction to EaseCentral

Our clients are benefiting of going paperless with SF-based tech partner, Easecentral. As a leading provider of HR and benefits software, EaseCentral understands that the thoughtof changing your benefits enrollment process can be overwhelming. But if working with morethan 1,000 insurance agencies and 40,000 businesses has taught us anything, it’s thatswitching to online enrollment is worth it.

“We believe that an electronic trail is better than a paper trail”

In the words of our cleinst “We believe that an electronic trail is better than a paper trail”. For most clinets under 50 employees a full HRIS system can get punishingly expensive.A leading payroll company charges all incluisve package for $45/month. This pricey journey of HR and benefits technolog can be a turn-off. When we asked our clients if they were interested in an affordable online enrollment that that works with underlying insurance managed by us and payroll the answer is invariably “thats a no brainer”.

After we introduced EaseCentral, it did not take very long to acclimate to using the system. Our Agency help clients with the initial setup. With inutitive system clients hit the ground running. Employees do not need a lot of help either. In 2016, the first year we used EaseCentral had been successful. We walked employees through how to use EaseCentral. Soon after, they experienced their first open enrollment with technology and without paper.

HR and Benefits Technology in Action

Joe, our long time client and partner of a successful NYC Law Firm told me that he benefited the most from EaseCentral during open enrollment.“I have saved a significant amount of time managing documents, filing forms and no longer have to worry about where it all is”.

Before online enrollment, Joe used a manual checklist to keep track of all of the documentation and paperwork. “With EaseCentral’s HR and benefits technology, I save about 20 hours of work during open enrollment due to online submission of insurance forms. Additionally, each employee at Cyber Advisor saves at least one hour,” said Joe.

Joe also touched on the value of using EaseCentral for new hires’ benefits enrollment. “Not only does the system save me two hours of work per new employee, but my employees appreciate the flexibility the system gives them when choosing their benefits,” he said. This flexibility includes being able to determine what the plan is and what it will cost and viewing and enrolling in benefits at home with dependents.

How Employees Use It

1.First, employees are presented with only the benefit plans they are eligible for.

2.Employees can enroll in all benefit types, including short-term and long-termdisability, HSAs, and telemedicine.

3.Each benefit plan includes in-depth summaries that provide deductible amounts and co-pays. If carriers have educational content like videos, employees can view those inside EaseCentral too.

4.Employees can view side-by-side plan comparisons with the cost per pay period tohelp them determine which plan brings them and their family the most value.

5.EaseCentral also provides the accurate cost to the employee of each benefit planthey’re eligible for, and takes into account factors like dependents. Because thisprocess is completed entirely online, employees can share these details with theirdependents at home if they choose to.

ONLINE ENROLLMENT TECHNOLOGY

The benefits of online enrollment continue to make waves forbusinesses across the nation. Research shows that nearly 8million businesses will be moving their benefits and HRprocesses online by 2024.Businesses across the country are increasinglyadopting online enrollment software. These are some of the ways, using both technology and a personal touch, you can create a whole world of difference for the new employee. It is about engaging them during their initial time in order to create a sense of belonging and loyalty to the organization so that they remain in the company for a long time to come.

Are you interested in more information on expereincing 21st century HR, Payroll and Benefits Tech integrations? Please join us for Weekly Demo on Thursdays 4PM EST.

This article was originally published on the BambooHR blog.At BambooHR, we believe in people.

We believe that the most valuable resources an organization has are its human resources. And we believe in showing employees how valuable they are to the organization. That’s why we encourage offering valuable benefits and perks to employees, and it’s why we have created a culture of appreciation within our own company.

Learn More About Our Compensation Software

It’s a philosophy that’s not necessarily new—the idea that employees who are treated better perform better—but it’s starting to gain momentum in the professional world. Around the world, companies are beginning to realize that offering major benefits like flexible work schedules, unlimited PTO, and unique perks like a vacation reimbursement program can do wonders for morale and productivity.

Unfortunately, despite the growing body of evidence in favor of this philosophy, many employers are still skeptical and reluctant to offer much beyond a steady paycheck. To help convince naysayers that pampering employees promotes productivity, we asked industry professionals about their experiences with offering benefits and perks. The response was overwhelming, and each CEO, COO, and HR professional that responded was in favor of them.

Here, we share with you their insights, experiences and advice. We hope it will inspire you to go and do likewise. It’s our firm belief that as you use benefits and perks to show your workforce that their contributions are appreciated and that they are valued as individuals, you will see engagement levels increase, retention rates improve, and your organization will become more attractive to prospective employees.

The Impact of Benefits and Perks on Employee Engagement and Retention

It’s been a decade since the 2008 economic recession, and as the economy continues to recover, it’s increasingly an employee’s market. This is a fact that’s not lost on those in charge of hiring and retaining employees. Patrick Colvin, Strategic HR Business Partner at the USA Today Network, put it this way:

“Due to the improved economic and job market conditions, the advantage has shifted from the employer to the job seeker, and organizations need to recognize the correlation between benefits and employee retention. In today’s hiring market, a generous benefits package is essential for engaging and retaining your talent.”

It’s becoming harder and harder for employers to ignore: the healthier the job market, the easier it is for employees to jump ship when they find something better. Attracting and keeping employees takes offering them a position at a company where their work is seen as a valuable contribution.

“Benefits and perks are a huge part of employee engagement and retention,” says Mary Pharris of Fairygodboss. “For companies to attract top talent and retain them, competitive benefit packages are essential. Employees rely on a variety of benefits from employers, so making sure you’re offering competitive and desired benefits will help you in attracting talent.”

While not everyone agrees that attracting talent is the goal of perks and benefits, the belief in its power to boost engagement and retention is both ubiquitous and unanimous. “While benefits are not a large driver of talent acquisition,” says Jody Ordioni, Founder of Brandemix, “they have a tremendous positive impact on engagement and retention, especially now that millennials represent 30+ percent of today’s workforce.”

Most importantly, offering a generous benefits package has a non-trivial impact, observable by many businesses. According to Lee Fisher, HR manager at Blinds Direct, “For us, these perks are tremendously important, from the moment an applicant sees a job ad and applies for a job here. Five or six years down the line, employee benefits continue to play a major role in keeping our valuable team members happy.”

It seems every company that’s putting this philosophy into practice is noticing a difference. “Company benefits play a huge role in employee retention,” says Steve Pritchard, founder of Cuuver. “It’s a two-way street; if an employer is flexible and offers great benefits, staff are generally more likely to want to stay working for them and appreciate the perks they are being offered that they may not get at another company.”

Is There a Downside to Benefits and Perks?

Finding Balance

Despite the growing evidence, some businesses are still skeptical. The high price of some benefits may intimidate a cost-conscious professional. Some even believe their workforce can’t be trusted with the freedom and responsibility of benefits like flexible work schedules. Some don’t think they need or deserve such luxuries.

It may even be a simple lack of thinking outside the box on the part of the employer. Whatever the reason, each employer may be overlooking an important fact—that without their team, they don’t have a business. Benefits and perks are investments in your workforce, and they pay dividends in the form of loyalty and dedication to the company. Lisa Oyler, HR director at Access Perks, agrees:

We always say that no company has ever suffered from trying to be more empathetic to their customers and employees. The cost and effort are worth it when you consider the huge advantages of employee engagement and retention and the costs of turnover and disengagement.

Steve Pritchard of Cuuver put it this way:

In my experience, employees are very appreciative of the perks they are given and do not abuse them. I can’t say this will be the same in every business, but because these benefits are there to make them happier, employees generally make the most of them and perform better. Some companies believe that having strict rules and no extra benefits is the way to go – which is why they don’t hold on to their best staff members for very long.

There are several strategies—which can be implemented simultaneously—for achieving a balance between keeping costs in check and offering a generous benefits package.

Mollie Delp, HR specialist at Workshop Digital proposes one way: “Everyone has to be mindful that you still have to get your work done and that client needs will always come first.”

Wayne Sleight, COO of 97th Floor proposes another strategy: “Giving people more stuff won’t make them happier, but perks that support the company’s values, mission, and purpose will.”

Lisa Oyler offers us a third reason: “And as long as managers are setting clear expectations for employees, there shouldn’t be many issues with over-abuse of benefits. After all, benefits are only going to pay off for the company when employees use them.”

Obstacles on the Path

Even if you decide that your employees are worth the investment, there are hurdles to clear on the road to successfully implementing your benefits and perks. The biggest is friction between the previous company culture and the new policies, as pointed out by Jody Ordioni, founder of Brandemix:

The one negative I’ve become aware of is when managers aren’t on board with the benefits culture; i.e. if an organization encourages remote work but one’s manager requires all employees to be on-site, it creates a culture of resentment which could have an opposite effect from the desired results.

Matt Bentley, Founder of CanIRank echoes the sentiment: “If you are the type of Manager that…[is] more suited to micromanaging, then a flexible work environment may not be suited to you as you will naturally feel you need to double check what all of your staff are doing day-to-day.”

That’s not the only way managers and directors can undermine the positive aspects of employee benefits. Half-hearted commitment can be just as detrimental as outright opposition. In the words of Robin Schwartz, managing partner of MFG Jobs: “Before offering a new benefit or perk, it’s important to ensure that your organization has the means to make it permanent. The downside of introducing new perks is seeing them be taken away because they cost more than expected or just weren’t sustainable.”

In the end, if the benefits and perks are carefully planned and strategically implemented, the rewards will outweigh the costs.

The Most Effective Benefits and Perks

So what benefits and perks you should be offering? Which ones give you the highest return on investment? We think Patrick Colvin’s take sums it up best:

“The fact of the matter is, after health insurance, the most desirable perks and benefits are those that offer flexibility while improving work-life balance.”

Flexible Work Schedule/Telecommuting

By far the most ubiquitous, popular, and highly recommended benefit among business owners and management teams was a flexible work schedule (usually including telecommuting & work-from-home options). This is largely due to the much-discussed “work-life balance.” Michelle Hayward, CEO, and Founder of Bluedog Design thinks that flexible work schedules should see even more use:

The most under-appreciated and under-utilized perk in a modern workplace is flexibility. With accountability to the team in mind, employees are empowered to make decisions to attend a child’s school performance or to work from home when life happens or plan flex hours to make a commute less stressful.

Robin Schwartz agrees:

Flexible work schedules! Being able to occasionally work remotely as well as being able to shift hours that best fit an employee’s life and job goes a really long way in keeping employees happy and [maintaining] engagement. Knowing they are encouraged to balance their work and life is a great perk.

Matt Bentley firmly believes in the value of “no office and no fixed schedule. If people want to go snowboarding on a Monday morning, they can. Encouraging a healthy work-life balance is still the most appreciated perk.” So does Amanda J. Ponzar, Chief Marketing Officer at Community Health Charities: “For employees to bring their best selves to work and perform, they need flexibility to enjoy outside interests and family, truly integrating work and life.” Dana Case, Director of Operations at MyCorporation.comdoes as well:

I find that one of the most desirable employee perks is being able to provide flexible scheduling options to all of your team members…By accommodating the scheduling needs of your team members and their personal lives, you’ll see how much they feel appreciated and are motivated to work hard for the business.

Mary Pharris sees it as a must for working women, one with fewer and fewer excuses not to implement:

From our research, we know that women’s job satisfaction is directly related to job flexibility. More and more employees are wanting flexible work environments. In large part, I think this is because life isn’t confined to the hours before or after work. Employees want the option to take care both of personal and professional responsibilities on their own terms, and with so much technology to make working remotely easy, it’s increasingly easier for employees to satisfy this.

Far from stifling or inhibiting productivity, this benefit seems to enhance it, according to our responders. Lee Fisher puts it this way:

We’ve come to realize that flexible-working is one of the biggest benefits for our staff. When we give our team the option to adapt their hours and work locations, they appreciate our flexibility and in turn produce even better results. It’s a simple perk, but a seriously important one.

It also enables your team to be productive no matter where they are in the world, and no matter how scattered each member may be. Michael Hollauf, CEO and Co-Founder of Meister Task is a staunch proponent of digital collaboration, stating:

We’ve also enabled flexible working, encouraging employees to work from wherever they work best. To allow this, we encourage all team members to be available on Slack during working hours and track their tasks in our task management tool, so that all team members can stay in the loop with project progress, even when working across different locations.

So if your work doesn’t physically require the team’s presence in order to be completed, strongly consider offering them the flexibility to do the work on their own terms.

Generous/Unlimited Vacation

A close second to flexible work schedules is loosening the reins on PTO. Many employers keep a tight grip on both vacation days and personal leave (in some cases verbally or culturally discouraging the use of even those days that are permissible by company policy). According to the experts who responded, this is a serious mistake. Not only does this create a serious liability in the form of unused PTO, it tends to result in team members experiencing burnout and, frequently, leaving the company for more favorable employment.

When asked what one benefit he would most recommend, Steve Pritchard answered:

A generous amount of time off. Giving employees plenty of opportunities to pursue their personal passions and unwind from work can go a long way towards improving their performance when they are at work. This ensures they don’t become frustrated with the lack of ability to take more than one vacation a year or take a few long weekends.

He wasn’t the only one. Mollie Delp concurred, saying:

Unlimited Vacation – to give the team the flexibility and reassurance that they can feel comfortable taking time off without penalty goes a long way. They don’t have to stress over a random Friday or afternoon where they need to be somewhere else (for themselves or family) and how it will overall effect their time off at the end of the year. One of our core values is to be empowered to be awesome in work and life, and we want to be sure our team knows we stand behind this, and that they have the flexibility to take care of their life and those around them when needed.

So did Patrick Colvin:

If I could recommend a single perk for employees, it would be flexible or unlimited vacation time. This perk shifts the focus from employees just putting in hours to placing an emphasis on production and great results. It allows employees to take ownership causing them to consider what’s best for both themselves as well as the organization. Most importantly it sends an important message to employees and prospective employees about the company culture and values.

The key, however, seems to be making sure your team knows that when you say “take some time for yourself,” that you really mean it. Lisa Oyler put it this way:

“Give employees plenty of time off to reboot and spend quality time with their families – but also set clear expectations that [they] don’t need to have their phones out or be ready to take a work call. Let them unplug!”

Incentives/Gamification

Another great way to increase engagement is through prizes, bonuses, awards and other incentives. Turning work into a competition or game can motivate your team to do their best. It even works internationally, according to Christian Rennella, VP of HR & CoFounder of elMejorTrato.com:

“After 9 years of hard work and having gone from 0 to 134 employees, I can assure you that the best strategy is ‘gamification’…Thanks to this gamification we were able to improve our retention by 31.1 percent.”

Business managers who utilize incentives will often see that extra push once there are valuable items and experiences on the line. For instance, some companies offer a round of golf, 5-star brunch, or extended weekends if certain projects are completed ahead of schedule. This simple gesture is often enough encouragement for workers to get their act together and step up their game.

Health Insurance

Health insurance is usually the most expensive benefit (by a wide margin), but it’s also the most sought after. Paying for insurance out of pocket is expensive, and paying doctors’ bills without insurance is even worse, so it makes sense why applicants make career decisions based largely on insurance benefits.

This is most apparent amongst millennials, who frequently value insurance above all other benefits, according to Jody Ordioni:

“Studies show that health is the most important benefit to millennials, and therefore, offering a suite of benefits that relate to health (on-site health clinic, 100-percent paid health/dental/vision benefits) would be my top recommendations.”

Additional Ideas for Engaging and Retaining Your Team

We received a great deal of feedback in our survey regarding creative and innovative ideas that help sweeten the deal for prospective and current employees. Here are some of the ones we liked the best.

Free Food

“We hold ‘Pizza and Presentations’ twice a month, where we treat our employees to a catered lunch in one of our conference rooms. Not only does this allow our team to enjoy time together and receive updates about each department’s projects, it provides everyone a chance to celebrate milestones in the company. This is a great way to say thank you to your employees for their hard work.” — Emily Burton of Fueled

“We find that often it’s small things that matter. Like setting out bowls of healthy snacks throughout the office a couple days each week. It’s nice for the employees, good for health, but it also brings groups to the break rooms, where they can mingle and get to know people outside their own departments. The same concept applies to volunteer opportunities, and our highly competitive (yet still fun) 5k.” — Lisa Oyler

“The one we love the most is our ‘Monday Breakfast.’…we do it every two weeks and we order food from a local restaurant. It’s a great start of the week, we come to work and chat about how the weekend went, and start the day and week on a positive note.” — Tatiana of Enhancv